3D Printing Filament Market Size

| Study Period | 2024 - 2029 |

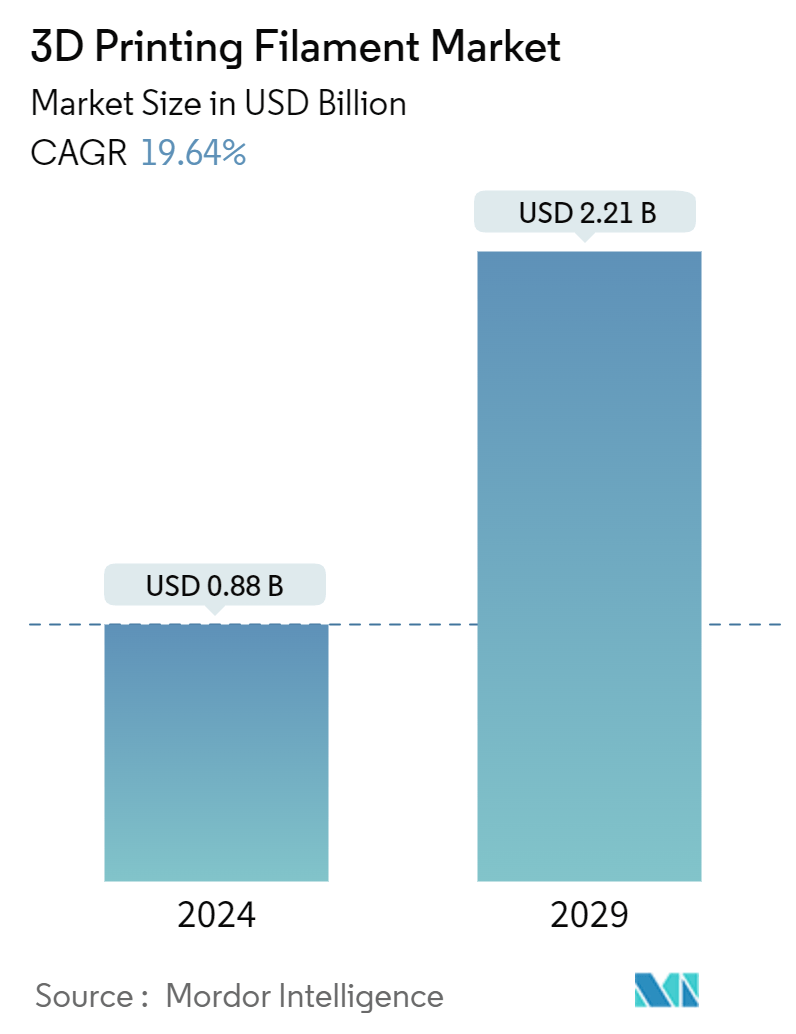

| Market Size (2024) | USD 0.88 Billion |

| Market Size (2029) | USD 2.21 Billion |

| CAGR (2024 - 2029) | 19.64 % |

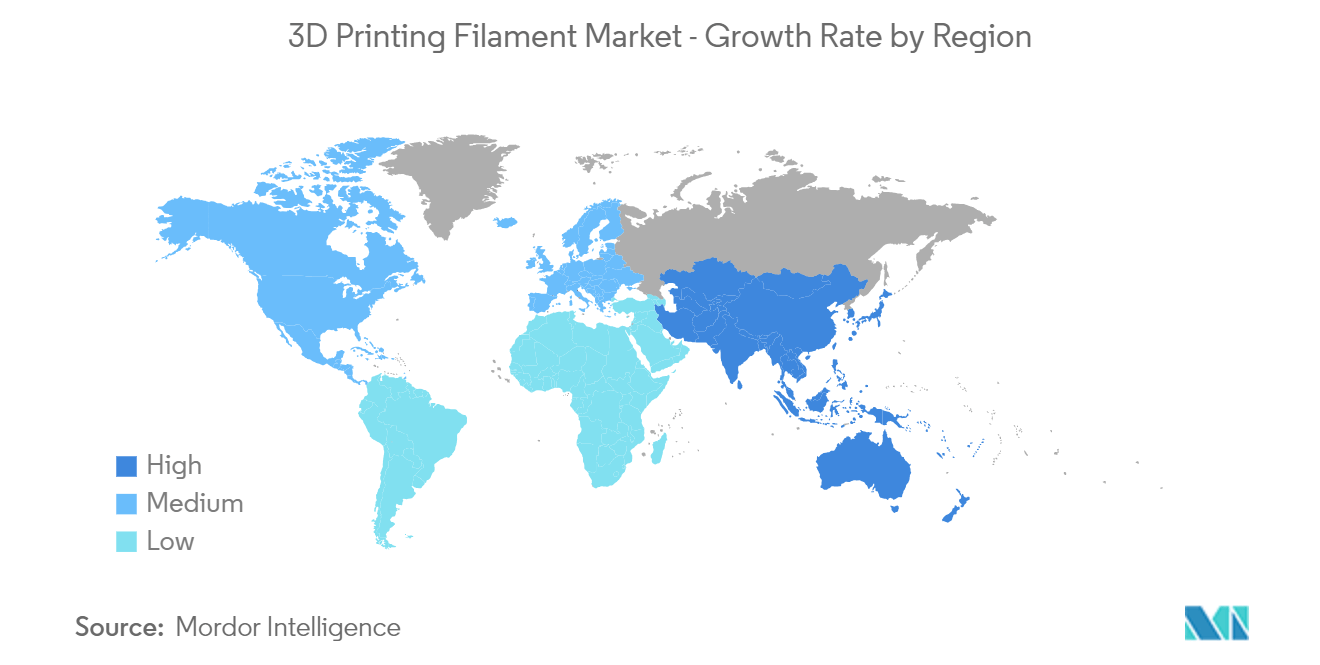

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

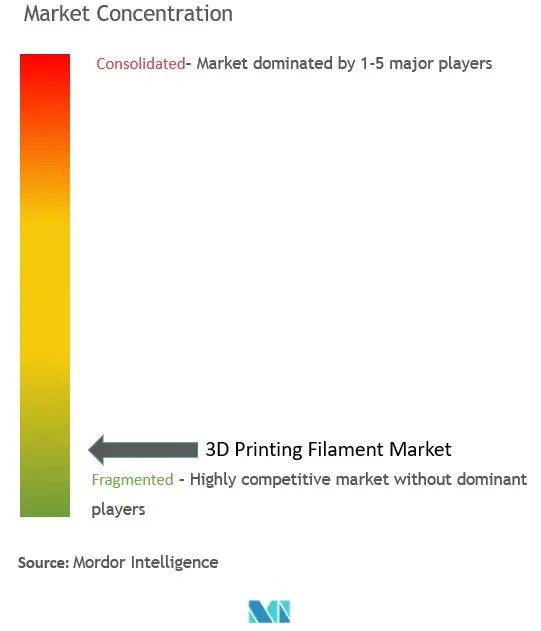

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

3D Printing Filament Market Analysis

The 3D Printing Filament Market size is estimated at USD 0.88 billion in 2024, and is expected to reach USD 2.21 billion by 2029, growing at a CAGR of 19.64% during the forecast period (2024-2029).

The COVID-19 outbreak caused nationwide lockdowns across the world, disruption in manufacturing activities and supply chains, and production halts, all of which had a negative impact on the market in 2020. However, conditions began to improve in 2021-2022, and the market is expected to grow year-on-year during the forecast period.

- The growing usage of 3D printing filaments in manufacturing applications, along with mass customization associated with 3D printing, is expected to drive the market growth during the forecast period.

- Conversely, high capital investment requirements in 3D printing may hinder the market's growth.

- 3D printing innovation in the medical industry and advancements in 3D printing materials may act as growth opportunities for the market studied in the future.

- Europe is expected to dominate the market with the largest market share during the forecast period.

3D Printing Filament Market Trends

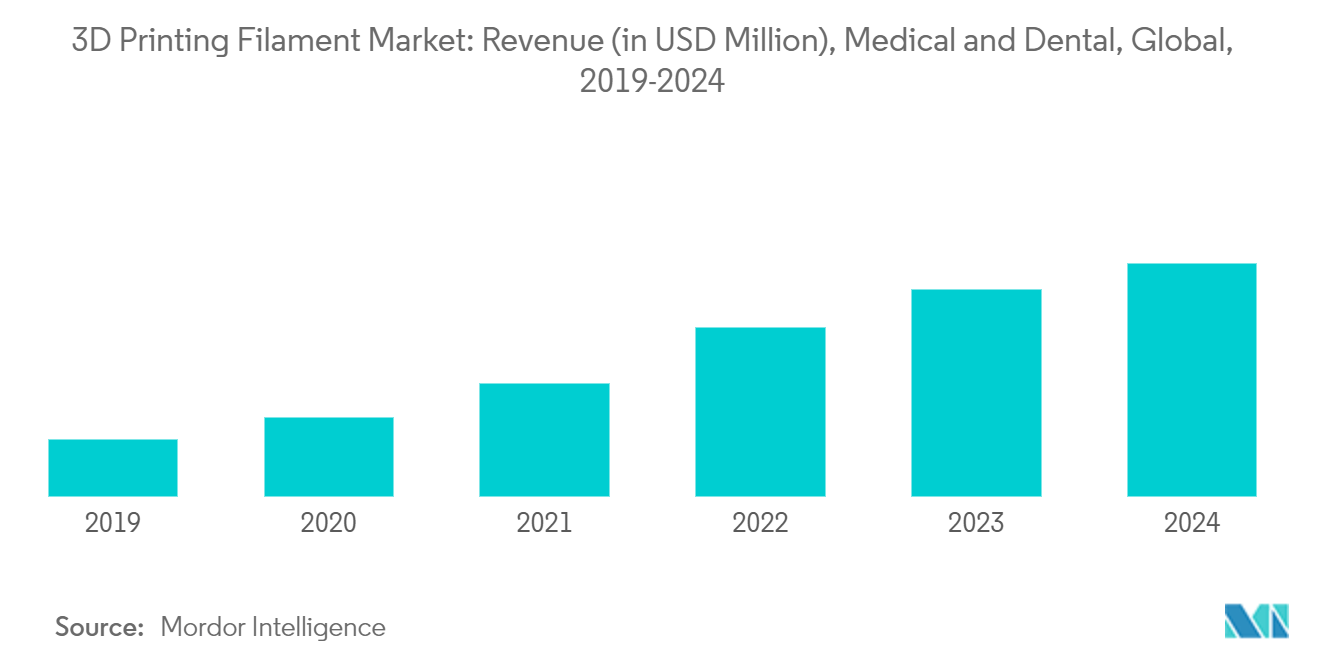

Increased Demand from the Medical and Dental Segment May Facilitate Market Growth

- The medical and dental industry is the leading industry that uses 3D printing filaments. It contributes to around 30-35% of the total applications of 3D printing filaments.

- 3D printing technology using different filaments allowed the creation of tissues and organoids, surgical tools, patient-specific surgical models, and custom-made prosthetics as applications in the medical and dental industry. These 3D-printed objects significantly contribute to the advancement and development of the industry.

- Medical devices produced by 3D printing include orthopedic and cranial implants, surgical instruments, dental restorations such as crowns, and external prosthetics.

- In March 2023, Invibio broadened its selection of implantable-grade PEEK-OPTIMA polymers by adding a filament specifically designed for fused filament additive manufacturing of medical devices.

- In August 2022, Lithoz, a 3D ceramic printing company, reported the first half of the year as the most successful in its history due to the increased order of its products. The company offers a wide range of ceramic 3D printers for various medical, dental, and industrial applications.

- Owing to all the above-mentioned factors, this segment is expected to grow rapidly in the market studied over the forecast period.

Europe to Dominate the Market

- Germany is the largest economy in Europe in terms of GDP. Germany, the United Kingdom, and France are among the fastest-emerging economies globally.

- As of October 2023, an average of approximately 11% of Europe's gross domestic product (GDP) was spent on healthcare, and expenditure on medical technology per capita was around EUR 312 (USD 337).

- According to MedTech Europe, over 33,000 medical technology companies are present in Europe. Most of them are located in Germany, followed by Italy, the United Kingdom, France, and Switzerland. Small and medium-sized companies (SMEs) make up around 95% of the medical technology industry.

- The German aerospace industry includes more than 2,300 firms located across the country, with Northern Germany recording the highest concentration of firms. The country hosts many production bases for aircraft interior components and materials, largely in Bavaria, Bremen, Baden-Württemberg, and Mecklenburg-Vorpommern.

- According to the Department for International Trade, the electronics industry in the United Kingdom contributes GBP 16 billion (~USD 19.53 billion) each year to the local economy. The country currently holds 40% of the share in the available electronics design industry in Europe. Current expertise within the industry is focused on integrated circuits (ICs), RFIDs, optoelectronics, and electronic components.

- France has been witnessing an increase in aircraft manufacturing and assembly operations in recent times as it is a major manufacturing base for manufacturers such as Airbus, Safran, Embraer, and Daher-Socata.

- Moreover, according to Air & Cosmos-International, France is expected to spend EUR 413 billion (USD 447.13 billion) on defense between 2024 and 2030 under its latest military programming law (LPM). This can substantially boost the country's consumption of 3D printing filament in the future.

- All the factors mentioned above are expected to boost the demand for 3D printing filament in the region.

3D Printing Filament Industry Overview

The 3D printing filament market is highly fragmented, with a few major players dominating a significant portion. Some of the major companies (not in any particular order) operating in the market include Stratasys Ltd, SABIC, BASF SE, Evonik Industries AG, and Mitsubishi Chemical Corporation.

3D Printing Filament Market Leaders

-

Stratasys Ltd.

-

SABIC

-

BASF SE

-

Evonik Industries AG

-

Mitsubishi Chemical Corporation

*Disclaimer: Major Players sorted in no particular order

3D Printing Filament Market News

- February 2024: Evonik Industries AG launched its INFINAM FR 4100 L 3D printing resin, designed for use with digital light processing (DLP) 3D printing technology. This resin is used to manufacture touch, pliable, and flame-retardant parts.

- February 2024: Solvay spun off its specialty business to an independent company, Syensqo. All 3D printing-related activities of Solvay are projected to be integrated into and ultimately become Syensqo businesses.

- October 2023: Evonik Industries AG introduced a new carbon fiber reinforced PEEK filament that can be processed in common extrusion-based 3D printing technologies, such as fused filament fabrication (FFF), and is suitable for use in long-term 3D-printed medical implants.

- June 2023: Mitsubishi Chemical Corporation announced its distribution collaboration with FormFutura to make the company an official distribution partner for Mitsubishi Chemical’s portfolio of 3D printing filaments.

3D Printing Filament Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Usage in Manufacturing Applications

4.1.2 Mass Customization Associated with 3D Printing

4.2 Restraints

4.2.1 High Capital Investment Requirement in 3D Printing Process

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Metals

5.1.1.1 Titanium

5.1.1.2 Stainless Steel

5.1.1.3 Other Metals

5.1.2 Plastics

5.1.2.1 Polyethylene Terephthalate (PET)

5.1.2.2 Polylactic Acid (PLA)

5.1.2.3 Acrylonitrile Butadiene Styrene (ABS)

5.1.2.4 Nylon

5.1.2.5 Other Plastics

5.1.3 Ceramics

5.1.4 Other Types

5.2 Application

5.2.1 Aerospace and Defense

5.2.2 Automotive

5.2.3 Medical and Dental

5.2.4 Electronics

5.2.5 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Vietnam

5.3.1.8 Indonesia

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 Russia

5.3.3.7 NORDIC

5.3.3.8 Turkey

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Qatar

5.3.5.6 Egypt

5.3.5.7 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 BASF SE

6.4.2 Covestro Ag

6.4.3 DOW

6.4.4 DSM

6.4.5 Evonik Industries Ag

6.4.6 Keene Village Plastics

6.4.7 Mitsubishi Chemical Corporation

6.4.8 SABIC

6.4.9 Solvay

6.4.10 Shenzhen Esun Industrial Co. Ltd

6.4.11 Stratasys

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 3D Printing Innovation in the Medical Industry

7.2 Advancements in 3D Printing Materials

3D Printing Filament Industry Segmentation

3D printer filament is a type of printing material used by the FFF-type 3D printer. It is one of the most common 3D printing materials in the world. It is mostly made of thermoplastic. However, metal, ceramics, and other materials are also used to make 3D printing filaments.

The 3D printing filament market is segmented by type, application, and geography. By type, the market is segmented into metals, plastics, ceramics, and other types (carbon fiber, etc.). By application, the market is segmented into aerospace and defense, automotive, medical and dental, electronics, and other applications (tool-making, etc.). The report also covers the market sizes and forecasts for the 3D printing filament market in 27 countries across major regions. For each segment, the market sizes and forecasts are provided based on revenue (USD).

| Type | |||||||

| |||||||

| |||||||

| Ceramics | |||||||

| Other Types |

| Application | |

| Aerospace and Defense | |

| Automotive | |

| Medical and Dental | |

| Electronics | |

| Other Applications |

| Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

3D Printing Filament Market Research FAQs

How big is the 3D Printing Filament Market?

The 3D Printing Filament Market size is expected to reach USD 0.88 billion in 2024 and grow at a CAGR of 19.64% to reach USD 2.21 billion by 2029.

What is the current 3D Printing Filament Market size?

In 2024, the 3D Printing Filament Market size is expected to reach USD 0.88 billion.

Who are the key players in 3D Printing Filament Market?

Stratasys Ltd., SABIC, BASF SE, Evonik Industries AG and Mitsubishi Chemical Corporation are the major companies operating in the 3D Printing Filament Market.

Which is the fastest growing region in 3D Printing Filament Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in 3D Printing Filament Market?

In 2024, the Europe accounts for the largest market share in 3D Printing Filament Market.

What years does this 3D Printing Filament Market cover, and what was the market size in 2023?

In 2023, the 3D Printing Filament Market size was estimated at USD 0.71 billion. The report covers the 3D Printing Filament Market historical market size for years: . The report also forecasts the 3D Printing Filament Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

3D Printing Filament Industry Report

Statistics for the 2024 3D Printing Filament market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. 3D Printing Filament analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.