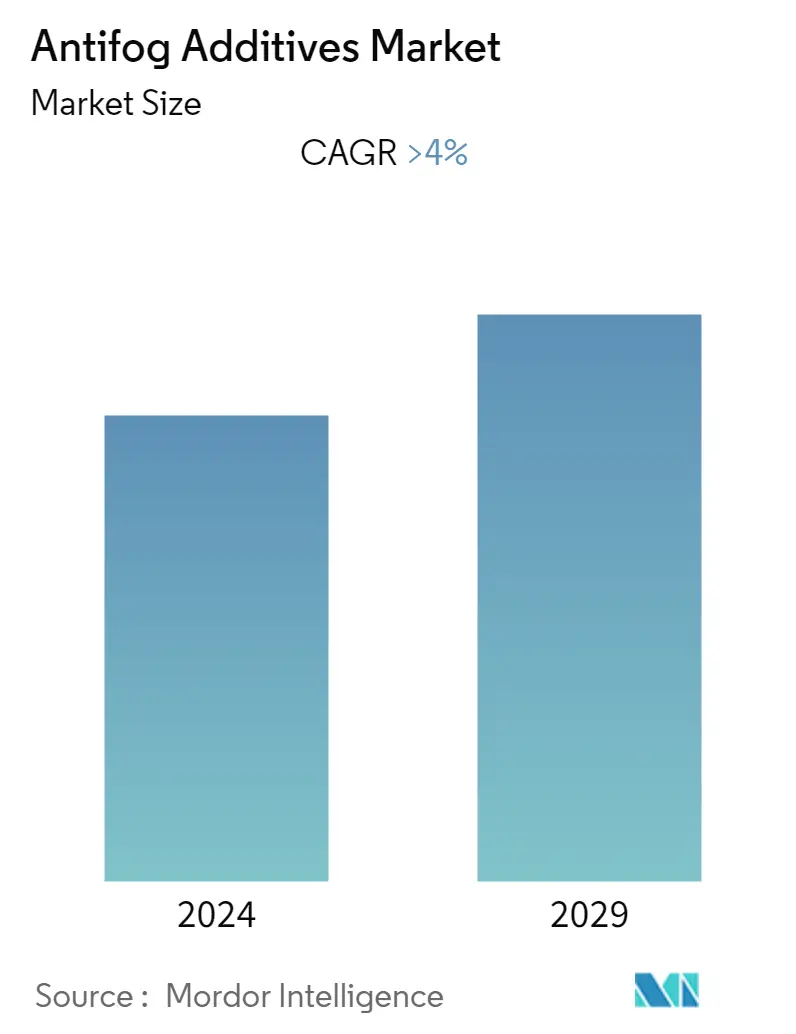

Anti-Fog Additives Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | > 4.00 % |

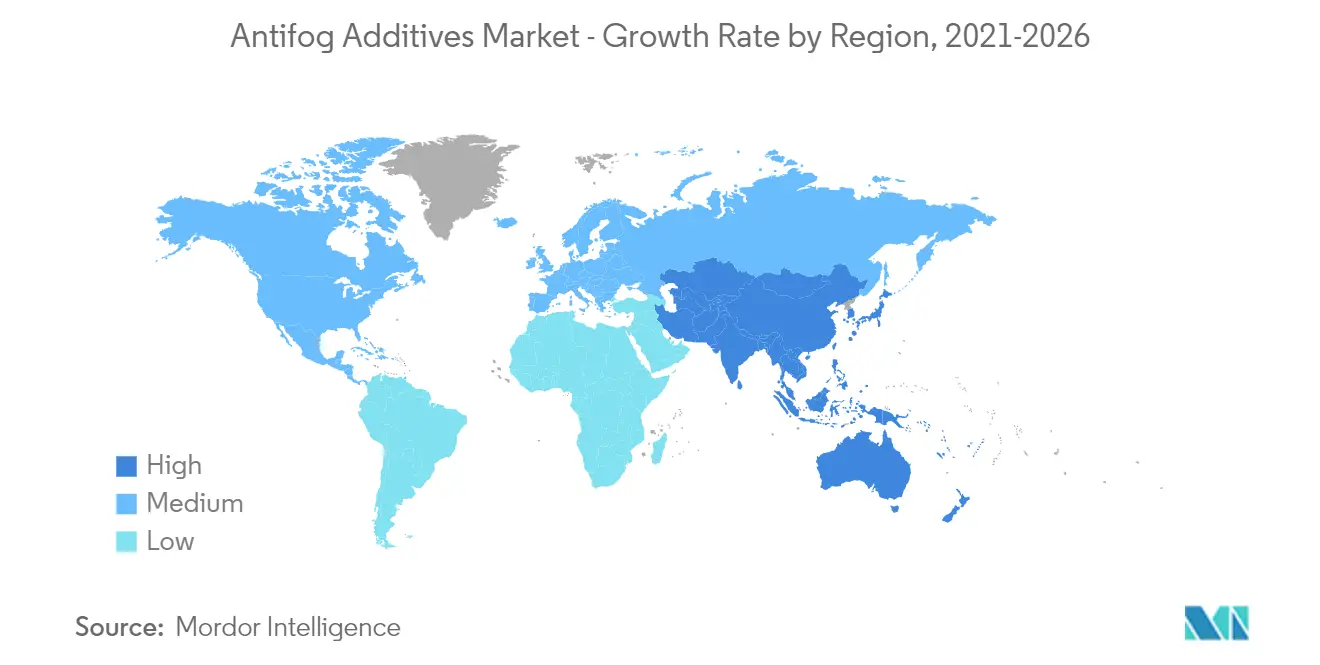

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

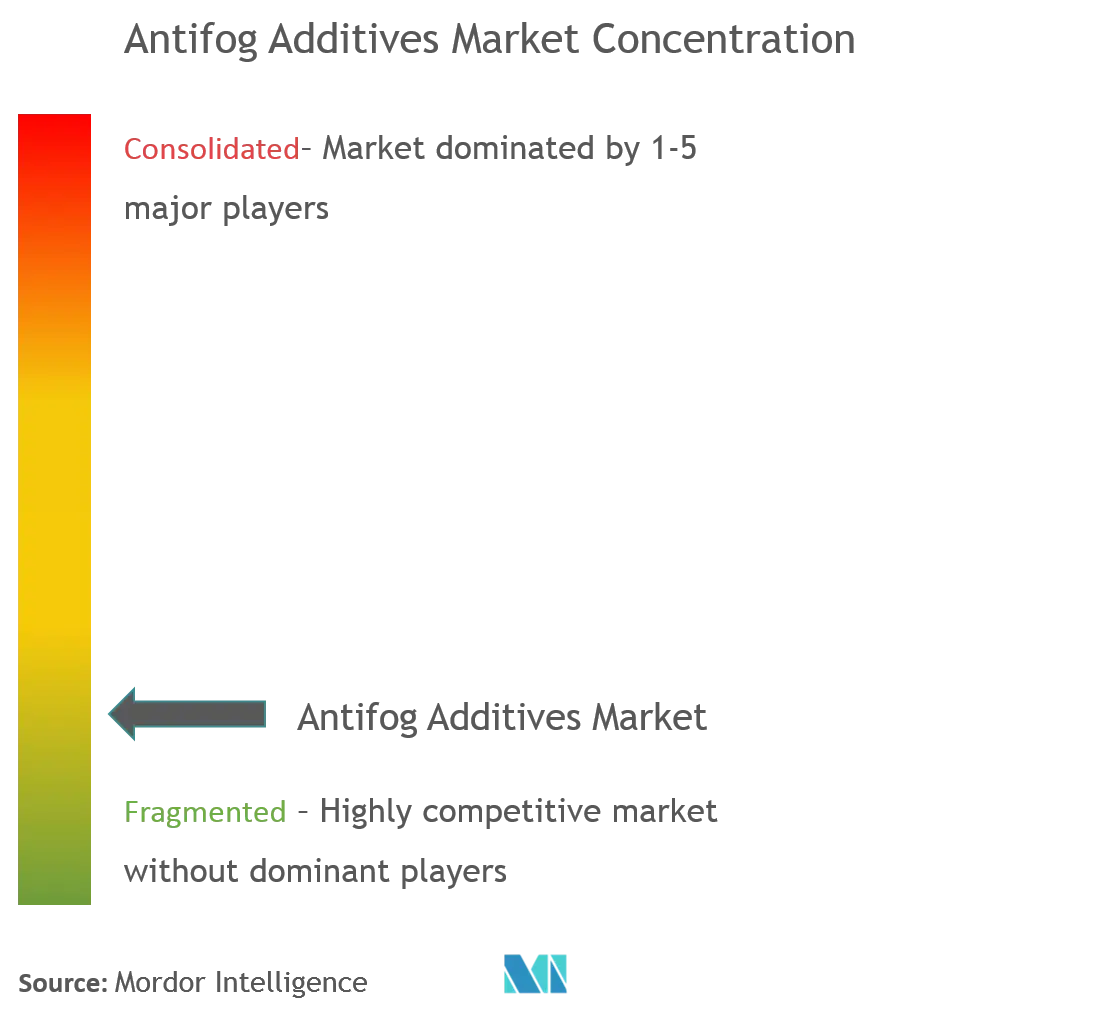

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Anti-Fog Additives Market Analysis

The antifog additives market is projected to register a CAGR of more than 4% during the forecast period (2021-2026).

COVID-19 has positively impacted the food packaging industry due to increased consumer awareness of fresh and safe deliveries, which is expected to boost the market for antifog films. For instance, according to the Ministry of Foof and Drug Safety (MFDS), processed food and vegetable imports in South Korea increased by around 6,000 ton in 2020 to hit 281,222 ton, compared to 275,424 ton in 2019. The revenue from the global food and beverage industry was valued at over USD 240 billion in 2020, which increased significantly from approximately USD 158 billion in 2019. Antifog additives, which are predominantly used in the production of films, create antifogging properties, thus protecting vegetables, fruits, meat, etc. Owing to these factors, the market for antifog additives is estimated to grow substantially through the forecast period.

- Over the medium term, increasing demand for agricultural and food packaging films and growing demand for coating films for mirrors and goggles are expected to drive the market.

- Strict government policies, hazardous waste production at the time of film production, and the negative impact of the COVID-19 pandemic act as restraints for market growth.

- On the other hand, there is a demand from the food and beverage sector for the packaging of processed foods to prevent the packaged food from spoiling and the formation of fog, which reduces visibility. This is projected to propel the antifog additives market.

- Asia-Pacific holds the largest market share, with the highest demand coming from India, China, and Japan.

Anti-Fog Additives Market Trends

This section covers the major market trends shaping the Anti-Fog Additives Market according to our research experts:

Increasing Demand from Packaging Films Application

- Fogging phenomenon occurs when freshly packed food items are placed in refrigerated storage. Fogging can be most commonly seenwhen there is a temperature differential between the outside and inside of an enclosed atmosphere. To overcome this problem, anti-fogs are often employed to control the condensation of water in the packaging.

- Antifog additives are primarily used in the production of polymer films to induce an antifogging property in them, which are further used for the packaging of food items, such as vegetables, fruits, breads, among others.

- Anti-fog additives lower the surface tension of the film surface and allow the water droplets to spread into a thin film and flow off from the film. They help in achieving higher transparency and ensure that water is not collected at the bottom of packaging, which could shorten shelf life of the product.

- In food-packaging, the antifog additive enhances product appeal and shelf life. When food is packed in a film where water droplets can form, it will aid to damage produce and the presence of water will allow the produce to rot.

- Additionally, anti-fogging additives benefit food packaging by maintaining its clarity and transparency so that its contents can be clearly seen by the consumer at the point of sale. By adding anti-fogging additives to food packaging films, condensed water droplets are spread into a thin transparent layer rather than remaining droplets. In general, food packaging only requires short-term anti-fogging performance that lasts the lifetime of the packaged food.

- In the Asia-Pacific region, there has been an increase in the acceptance of packaged food. The packaging industry is also poised to expand, thus, supporting the growth of plastic additives in the region. China has the second-largest packaging industry in the world. The country is expected to witness consistent growth during the forecast period, owing to the rise of customized packaging in the food segment, along with increasing exports.

- Owing to all these factors, the demand for antifog additives in the packaging films sector is projected to grow in the coming years.

Asia-Pacific Region to Dominate the Market

- The growing awareness about the benefits of using antifog additives in food and agricultural packaging in countries of Asia-Pacific, particularly in India, China, and Japan, has propelled the antifog additives market.

- The availability of large arable land in countries like China and India and the increasing adoption of technological advancements in agriculture to yield high-quality crops will likely stimulate the market growth of antifog additives.

- Further, the gradual shifting of people toward packaged and processed food due to hectic lifestyles is expected to enhance the demand for antifog additives. According to Interpak, in China, total packaging in the foodstuff packaging category is expected to reach 447 billion units in 2023.

- The strict rules and regulations imposed by the governments of countries like India and China have changed the market dynamics and have increased the focus on using antifog additives for food packaging and processing.

- India is one of the major consumers of packaged foods and beverages. According to the Packaging Industry Association of India (PIAI), the packaging industry is expected to grow at 22% during the forecast period. However, this growth was affected during 2020 due to the halted manufacturing activities in the first quarter of 2020.

- The demand for frozen foods in India is expected to witness a growth rate of approximately 17% in the next few years. Moreover, with the Indian government focusing on the food processing sector, the supply of processed agri-foods is expected to rise over the next five years, which, in turn, may stimulate the demand for antifog additives in the country.

- According to IBEF, in India, 55% of the packaging uses plastic, among which PVC films are widely used, dominating the food packaging market.

- In Japan, the food and beverage industry is expected to reach over USD 31 billion by 2025. This growth can be attributed to the increase in the demand for packaged foods and beverages, coupled with the increasing affordability of consumers. This expected growth in the food and beverage industry is estimated to influence the demand in the market positively.

- The aforementioned factors, along with government support, have helped the growth of the antifog additives market.

Anti-Fog Additives Industry Overview

The antifog additives market is fragmented with players accounting for marginal shares of the market. Some of the companies in the market are LyondellBasell Industries Holdings B.V. , Croda International PLC, Emery Oleochemicals, Avient, and DuPont.

Anti-Fog Additives Market Leaders

-

Emery Oleochemicals

-

Croda International Plc

-

LyondellBasell Industries Holdings B.V.

-

Avient

-

DuPont

*Disclaimer: Major Players sorted in no particular order

Anti-Fog Additives Market News

- In Dember 2020, Emery Oleochemicals announced a new distributor agreement with IMCD. IMCD Benelux will represent Emery's Green Polymer Additives business unit to distribute and provide technical support for Emery's natural-based lubricants, antistatic and antifogging agents, release agents, as well as their special plasticizers.

- In August 2018, LyondellBasell completed its acquisition of A.Schulman, Inc., a global supplier of performance plastic compounds, composites, and powders.

Anti-Fog Additives Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from Agriculture Industry

4.1.2 Surging Demand from Packaging Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Hazardous Waste Production During Film Production

4.2.2 Negative Impact of COVID-19 Pandemic

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION

5.1 Type

5.1.1 Glycerol Esters

5.1.2 Polyglycerol Esters

5.1.3 Sorbitan Esters of Fatty Acids

5.1.4 Other Types

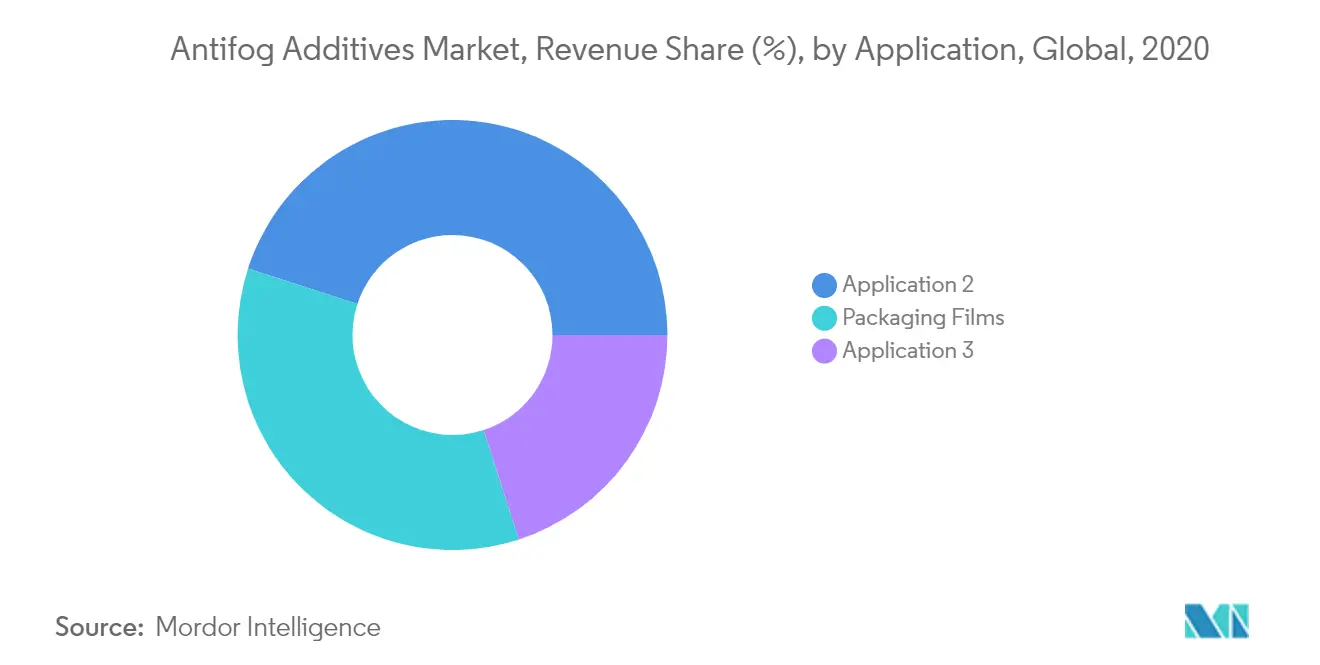

5.2 Application

5.2.1 Agricultural Films

5.2.2 Packaging Films

5.2.3 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) Analysis**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Avient

6.4.2 Corbion

6.4.3 Croda International PLC

6.4.4 Dupont

6.4.5 Emery Oleochemicals

6.4.6 Evonik Industries AG

6.4.7 Guangzhou CARDLO Biotechnology Co. Ltd

6.4.8 High Grade Industries India Pvt. Ltd

6.4.9 IR Tubes

6.4.10 LyondellBasell Industries Holdings BV

6.4.11 Palsgaard

6.4.12 PCC Chemax Inc.

6.4.13 Polyfill Technologies Pvt. Ltd

6.4.14 Rapidmasterbatches

6.4.15 SILIBASE SILICONE

6.4.16 Surya Masterbatches

6.4.17 Taprath Elastomers LLP

6.4.18 Ultra-Plas Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Awareness ����vlog��ý Usage of Antifog Additives in Processed Food

7.2 Other Opportunities

Anti-Fog Additives Industry Segmentation

The chemicals that prevent water condensation in small droplets on surfaces are known as antifog additives. The antifog additives market is segmented by type, application, and geography. By type, the market is segmented into glycerol esters, polyglycerol esters, sorbitan esters of fatty acids, and other types. By application, the market is segmented into agricultural films, packaging films, and other applications. The report also covers the market sizes and forecasts for the antifog additives market in 15 countries across major regions. The market sizing and forecasts have been done for each segment based on revenue (in USD million).

| Type | |

| Glycerol Esters | |

| Polyglycerol Esters | |

| Sorbitan Esters of Fatty Acids | |

| Other Types |

| Application | |

| Agricultural Films | |

| Packaging Films | |

| Other Applications |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Anti-Fog Additives Market Research FAQs

What is the current Antifog Additives Market size?

The Antifog Additives Market is projected to register a CAGR of greater than 4% during the forecast period (2024-2029)

Who are the key players in Antifog Additives Market?

Emery Oleochemicals , Croda International Plc, LyondellBasell Industries Holdings B.V., Avient and DuPont are the major companies operating in the Antifog Additives Market.

Which is the fastest growing region in Antifog Additives Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Antifog Additives Market?

In 2024, the Asia Pacific accounts for the largest market share in Antifog Additives Market.

What years does this Antifog Additives Market cover?

The report covers the Antifog Additives Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Antifog Additives Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Antifog Additives Industry Report

Statistics for the 2024 Antifog Additives market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Antifog Additives analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.