Asia-Pacific Plastic Bottles And Containers Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

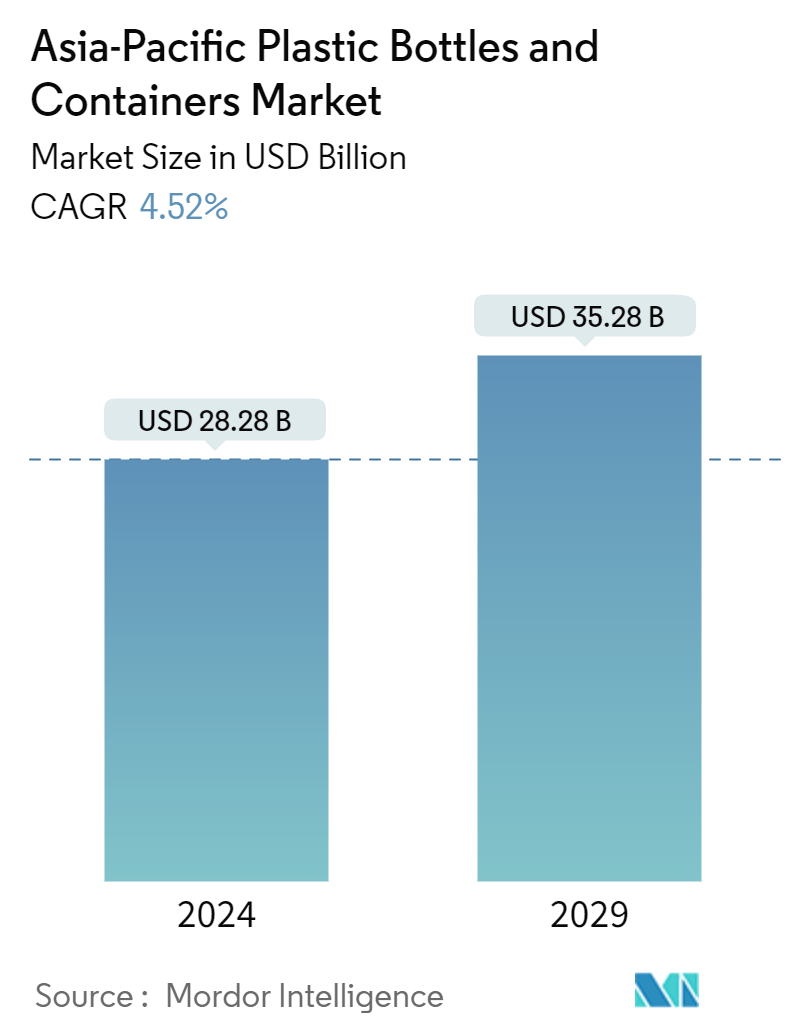

| Market Size (2024) | USD 28.28 Billion |

| Market Size (2029) | USD 35.28 Billion |

| CAGR (2024 - 2029) | 4.52 % |

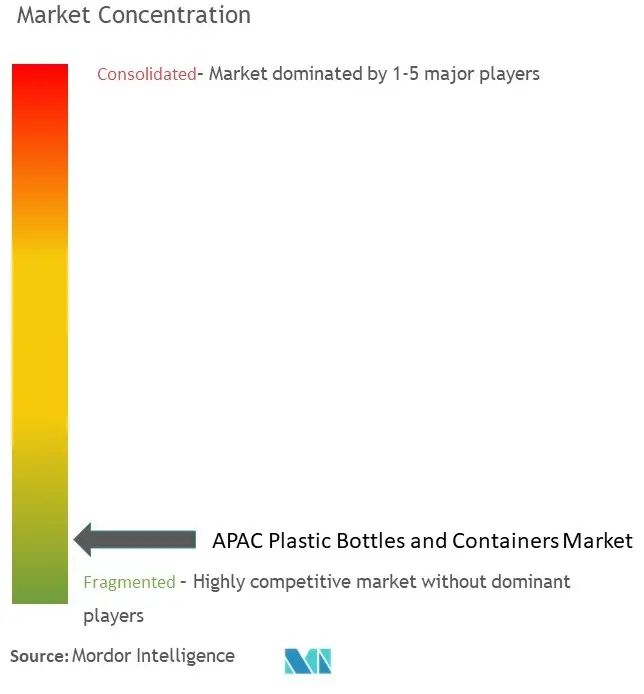

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Asia-Pacific Plastic Bottles And Containers Market Analysis

The Asia-Pacific Plastic Bottles And Containers Market size is estimated at USD 28.28 billion in 2024, and is expected to reach USD 35.28 billion by 2029, growing at a CAGR of 4.52% during the forecast period (2024-2029). In terms of production volume, the market is expected to grow from 19.60 million metric tons in 2024 to 24.5 million metric tons by 2029, at a CAGR of 4.57% during the forecast period (2024-2029).

- Plastic packaging has become popular among consumers over other products, as plastic material is lightweight and unbreakable, making it easier to handle. Even major manufacturers prefer to use plastic packaging, owing to the lower cost of production. Moreover, the introduction of polymers, such as polyethylene terephthalate (PET) and high-density polyethylene (HDPE), is expanding the applications of plastic bottles. The market has been witnessing an increasing demand for PET bottles.

- Plastic bottles and containers made of polyethylene terephthalate, polypropylene, and polyethylene are widely used as the material is lightweight and easily recyclable, making it the preferred choice among the end-users. The cost-effective nature of plastic material and dependence on packaged, processed food and various beverages will influence the studied market over the forecast period.

- Plastics have been increasingly adopted due to their lightweight properties because lightweight plastic packaging can preserve energy in transporting packed goods and lower emissions. The lightweight properties of plastic are the primary advantage of expanding the market. Compared to other materials, such as glass, which is much heavier than plastic, more trips are required while transporting.

- The market's growth can also be attributed to the expanding range of applications across diverse industries in the region. For instance, within the pharmaceutical industry, plastic bottles offer a reliable packaging option for tablets, syrups, and capsules due to their moisture-resistant properties that maintain product stability. In personal care and cosmetics, plastic bottles are an ideal option for packaging shampoos, conditioners, lotions, and creams, owing to their durability and visual appeal.

- However, with growing concerns about plastic pollution, manufacturers and consumers are also inclining themselves toward other packaging materials that offer environment-friendly properties. The consumption of aluminum and glass might witness rising adoption rates owing to their high recyclability. This is expected to hinder the growth of the market studied.

- Nevertheless, the Asia-Pacific region has experienced improved and better economic growth and dynamic demographic changes that have significantly influenced the region's development. The growth of organized retail, including supermarkets and hypermarkets, has heightened the demand for packaged goods. These outlets require extensive packaging to cater to the diverse needs of consumers, driving the overall market.

Asia-Pacific Plastic Bottles And Containers Market Trends

Polyethylene Terephthalate (PET) Segment Holds Major Market Share

- Plastic bottles made from PET are widely replacing heavy and fragile glass bottles since they offer reusable packaging for mineral water and other beverages, allowing a more economical transportation process.

- With its clarity and natural CO2 barrier properties, PET has wide applications and is easily blown into a bottle or molded into any other shape. PET properties can be improved with colorants, UV blockers, oxygen barriers/scavengers, and other additives to develop a bottle to match a brand's specific needs.

- PET has become one of the vital packaging materials among bottle manufacturers across the region. PET's versatility in accommodating different shapes and sizes has provided unparalleled alternatives to conventional glass and metal containers, making it a highly desirable choice in the packaging industry.

- Polyethylene terephthalate (PET) bottles are gaining a presence in various product areas. Low cost, low weight, and ongoing developments in printing technology have led to PET bottles gaining popularity among premium consumers.

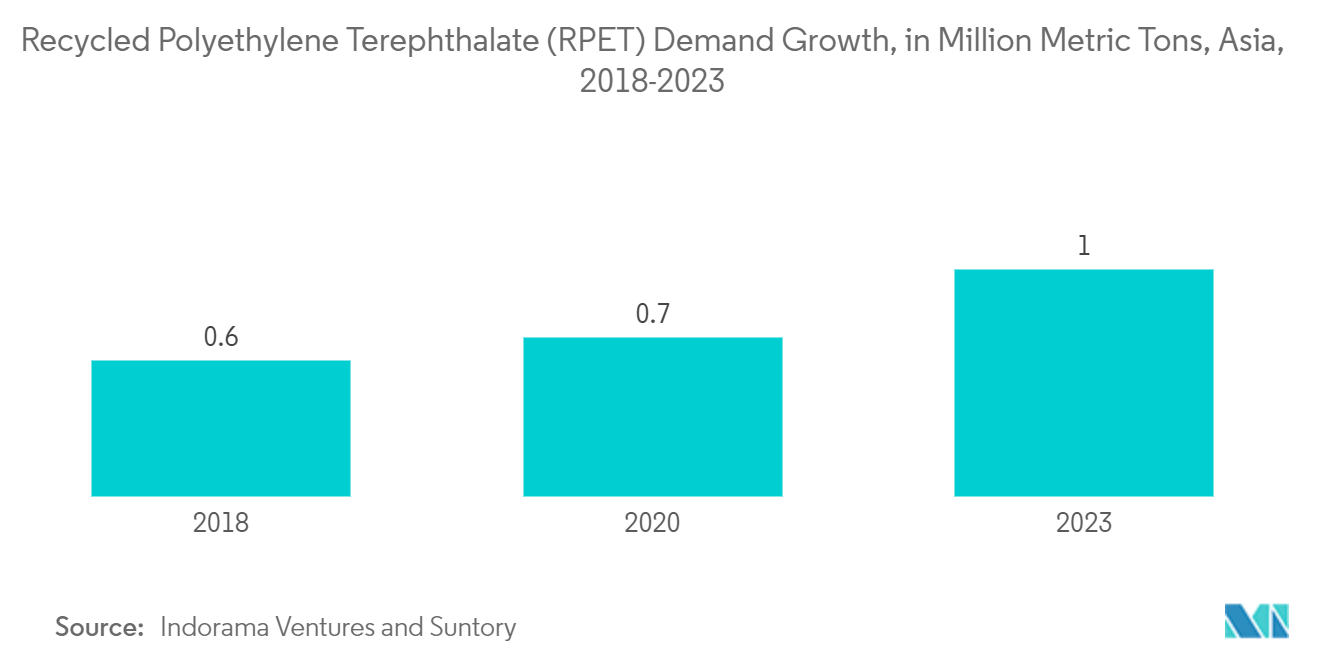

- As per the report of Indorama Ventures, a sustainable chemical company, the demand for recycled polyethylene terephthalate (RPET) in Asia is expected to increase constantly from 0.6 million metric tons in 2018 to approximately 1 million metric tons in 2023.

- Further, in September 2023, Indorama Ventures Public Company Limited notified that it had recycled 100 billion post-consumer PET bottles. This has diverted 2.1 million tons of waste, preserved 2.9 million tons of carbon footprint, and helped in establishing a circular economy for PET. Indorama Ventures spent more than USD 1 billion on the waste collection of used PET bottles.

- The future of PET recycling closely revolves around technological advancements that make the process more efficient, cost-effective, as well as environmentally friendly. The ability to collect, process, and transform used PET products into new packaging materials provides an immense opportunity to reduce dependency on virgin resources, therefore mitigating environmental waste.

China Expected to Hold Significant Market Share

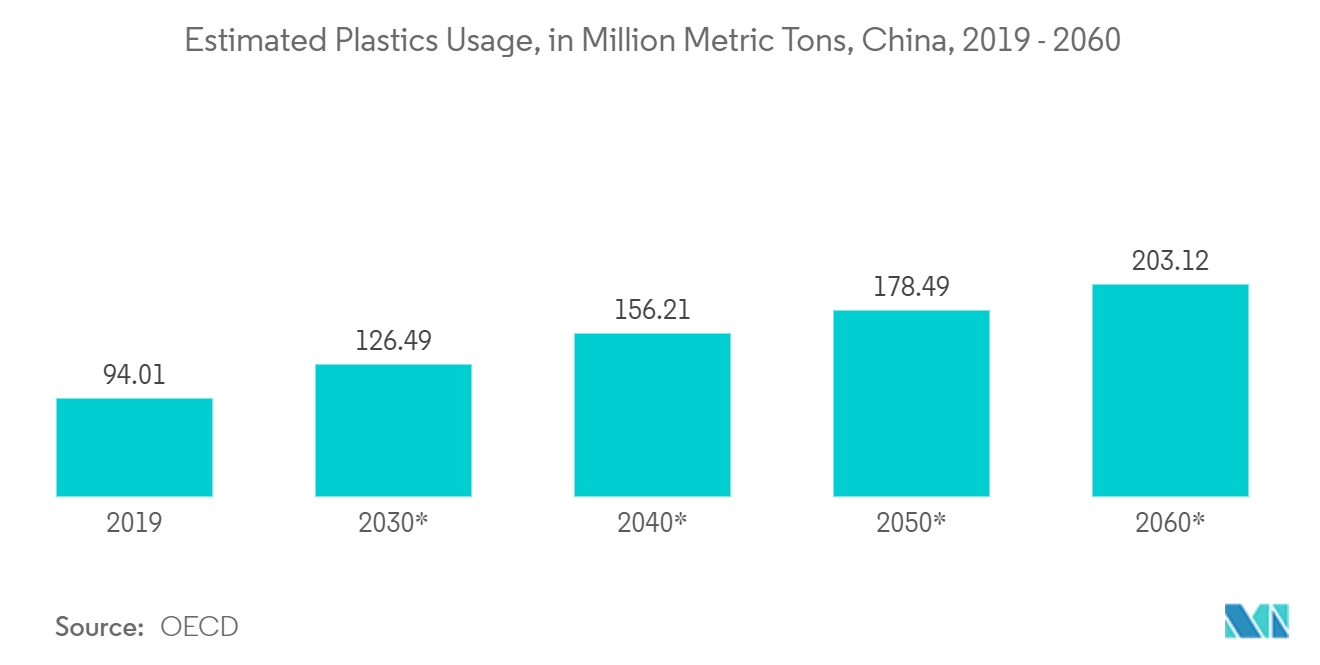

- China is one of the major producers and consumers of plastic globally. According to the OECD, China's plastics use is projected to grow considerably over the next four decades, reaching more than 203.12 million metric tons by 2060. The growing dependence on plastic bottles and containers made using PET (Polyethylene Terephthalate), HDPE (High-Density Polyethylene), and other polymers for food & beverage, pharmaceutical, and personal care industries has increased the focus on the production and export of plastics from China.

- According to data from the International Trade Center (ITC), China's largest export of plastic products is to the United States of America. China exported 292.6 million tons of plastic products to the USA in 2023, which was 8.00% higher than the previous year. The high potential growth opportunity in plastic trade is expected to increase the country's demand for plastic in the coming years.

- China is witnessing a shift in its focus on sustainable and eco-friendly practices to promote recycled plastic. This has resulted in beverage manufacturers such as Coca-Cola using recycled plastic as part of their strategy to reduce their environmental footprint.

- In April 2024, Coca-Cola Company, a United States-based beverage company, launched Coca-Cola Original, Coca-Cola No Sugar, and Coca-Cola Plus bottles made from recycled polyethylene terephthalate (rPET) in Hong Kong.

- China has been prompting merchants and delivery companies to reduce "unreasonable" plastic wrapping and increase garbage incineration rates in cities to about 800,000 tons per day by 2025, up from 580,000 tons currently. Such developments are expected to increase the country's recyclable plastic packaging demand.

Asia-Pacific Plastic Bottles And Containers Industry Overview

The Asia Pacific Plastic Bottles and Containers market is fragmented with the presence of major players like Gerresheimer AG, Pact Group Holdings Limited, Alpla Group, Berry Global Inc., and Alpha Packaging Pvt. Ltd. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2023 - Manjushree Technopack entered into a collaboration agreement with the bottle-to-bottle grade recycling division of Ganesha Ecosphere Group to co-develop and supply food and non-food grade packaging products made of recycled plastics. The partnership sets to serve the brands in complying with the new (Plastic Waste Management) PWM rules while supporting the Indian government’s ambitious target of replacing up to 60% of virgin plastic with recycled plastic by FY29. The partnership also aims to help create a circular economy and accelerate the adoption of 100% recycled plastic bottles.

- December 2023 - Pact Group, an Australia-based company, in partnership with Cleanway Waste Management, Asahi Beverages, and Coco-Cola Europacific Partners, opened a PET bottle recycling plant in Melbourne. The Circular Plastics Australia (PET) plant will convert used plastic bottles into high-quality food-grade resin, which will be used to make new recycled PET beverage bottles and other packaging products. The facility is equipped to produce 2.5 tons of rPET resin per hour and 20,000 tons of rPET resin each year.

Asia-Pacific Plastic Bottles And Containers Market Leaders

-

Gerresheimer AG

-

Pact Group Holdings Limited

-

Alpla Group

-

Berry Global Inc.

-

Alpha Packaging Pvt. Ltd

*Disclaimer: Major Players sorted in no particular order

Asia-Pacific Plastic Bottles And Containers Market News

- April 2024 - Manjushree Technopack revealed its plan to acquire the plastics packaging business of Oricon Enterprises Limited for an enterprise value of INR 520 crore (USD 62.97 million). The acquired business includes Oriental Containers, a manufacturer of plastic caps and closures and preforms mostly used in beverages. Two manufacturing plants located in Goa and Odisha are part of the acquisition. The combined business is set to have a wider array of molds, machines, and SKUs strengthen unit economics due to operational synergies, and deepen key customer relationships.

- February 2024 - Sinopec Yangzi, a global petrochemical producer subsidiary, initiated the relaunch of its PP manufacturing facility in China. The relaunched facility is anticipated to boast a production capacity of 80,000 PP annually. This strategic development is a part of the company’s policy to ensure the high production capability of its facilities.

APAC Plastic Bottles & Containers Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Intensity of Competitive Rivalry

4.3.5 Threat of Substitute Products

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Adoption of Lightweight Packaging Methods

5.1.2 Changing Demographic and Lifestyle Factors

5.2 Market Restraints

5.2.1 Growing Environmental Concerns Over the Use of Plastics

6. MARKET SEGMENTATION

6.1 By Raw Materials

6.1.1 Polyethylene Terephthalate (PET)

6.1.2 Polypropylene (PP)

6.1.3 Low-Density Polyethylene (LDPE)

6.1.4 High-Density Polyethylene (HDPE)

6.1.5 Other Raw Materials

6.2 By End-user Vertical

6.2.1 Beverages

6.2.1.1 Bottled Water

6.2.1.2 Carbonated Soft Drinks

6.2.1.3 Dairy-based

6.2.1.4 Other Beverages

6.2.2 Food

6.2.3 Cosmetics

6.2.4 Pharmaceuticals

6.2.5 Household Care

6.2.6 Other End-user Verticals

6.3 By Country

6.3.1 China

6.3.2 India

6.3.3 Japan

6.3.4 Australia and New Zealand

6.3.5 South East Asia

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Gerresheimer AG

7.1.2 Pact Group Holdings Limited

7.1.3 Alpla Group

7.1.4 Berry Global Inc.

7.1.5 Alpha Packaging Pvt. Ltd

7.1.6 Mauser Packaging Solutions (Bway Holding Corporation)

7.1.7 Greiner Packaging International GmbH

7.1.8 Retal Industries Limited

7.1.9 Zhejiang Xinlei Packaging Co. Ltd

7.1.10 Shenzhen Zhenghao Plastic & Mold Co. Ltd

7.1.11 Manjushree Technopack Limited

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Asia-Pacific Plastic Bottles And Containers Industry Segmentation

For this study, bottles are defined as rigid plastic containers with an open cap medium or a dispensing interface (such as a dropper, nozzles, pumps, sprays, etc.) that are primarily used by the manufacturer to pack fluid products. Containers are defined as rigid plastic containers that have only an open cap or closure medium for dispensing and usually contain very high or very minimal quantities of product (jars, canisters, buckets/pails, boxes, gallons, tubs, etc.) and are considered in this category. Unlike bottles, the containers classified in this section are, in most cases, re-usable and have a high demand from aftermarket sales as compared to the demand or consumption from manufacturers.

The scope is limited to B2B demand. The estimates exclude the weight of the content that is packed inside the plastic bottles and containers.

The Asia-Pacific plastic bottles and containers market is segmented by raw materials (polyethylene terephthalate (PET), polypropylene (PP), low-density polyethylene (LDPE), high-density polyethylene (HDPE), other raw materials), end-user vertical (beverages [bottled water, carbonated soft drinks, dairy-based, other beverages], food, cosmetics, pharmaceuticals, household care, other End-user verticals), by country (China, India, Japan, Australia and New Zealand, Southeast Asia, and Rest of Asia Pacific). The report offers market forecasts and size in volume (metric tons) and value (USD) for all the above segments.

| By Raw Materials | |

| Polyethylene Terephthalate (PET) | |

| Polypropylene (PP) | |

| Low-Density Polyethylene (LDPE) | |

| High-Density Polyethylene (HDPE) | |

| Other Raw Materials |

| By End-user Vertical | ||||||

| ||||||

| Food | ||||||

| Cosmetics | ||||||

| Pharmaceuticals | ||||||

| Household Care | ||||||

| Other End-user Verticals |

| By Country | |

| China | |

| India | |

| Japan | |

| Australia and New Zealand | |

| South East Asia |

APAC Plastic Bottles & Containers Market Research FAQs

How big is the Asia-Pacific Plastic Bottles And Containers Market?

The Asia-Pacific Plastic Bottles And Containers Market size is expected to reach USD 28.28 billion in 2024 and grow at a CAGR of 4.52% to reach USD 35.28 billion by 2029.

What is the current Asia-Pacific Plastic Bottles And Containers Market size?

In 2024, the Asia-Pacific Plastic Bottles And Containers Market size is expected to reach USD 28.28 billion.

Who are the key players in Asia-Pacific Plastic Bottles And Containers Market?

Gerresheimer AG, Pact Group Holdings Limited, Alpla Group, Berry Global Inc. and Alpha Packaging Pvt. Ltd are the major companies operating in the Asia-Pacific Plastic Bottles And Containers Market.

What years does this Asia-Pacific Plastic Bottles And Containers Market cover, and what was the market size in 2023?

In 2023, the Asia-Pacific Plastic Bottles And Containers Market size was estimated at USD 27.00 billion. The report covers the Asia-Pacific Plastic Bottles And Containers Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Asia-Pacific Plastic Bottles And Containers Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

APAC Plastic Bottles & Containers Industry Report

Statistics for the 2024 APAC Mild Hybrid Vehicles market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. APAC Mild Hybrid Vehicles analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.