Bio-based Polymers Market Size

| Study Period | 2019-2029 |

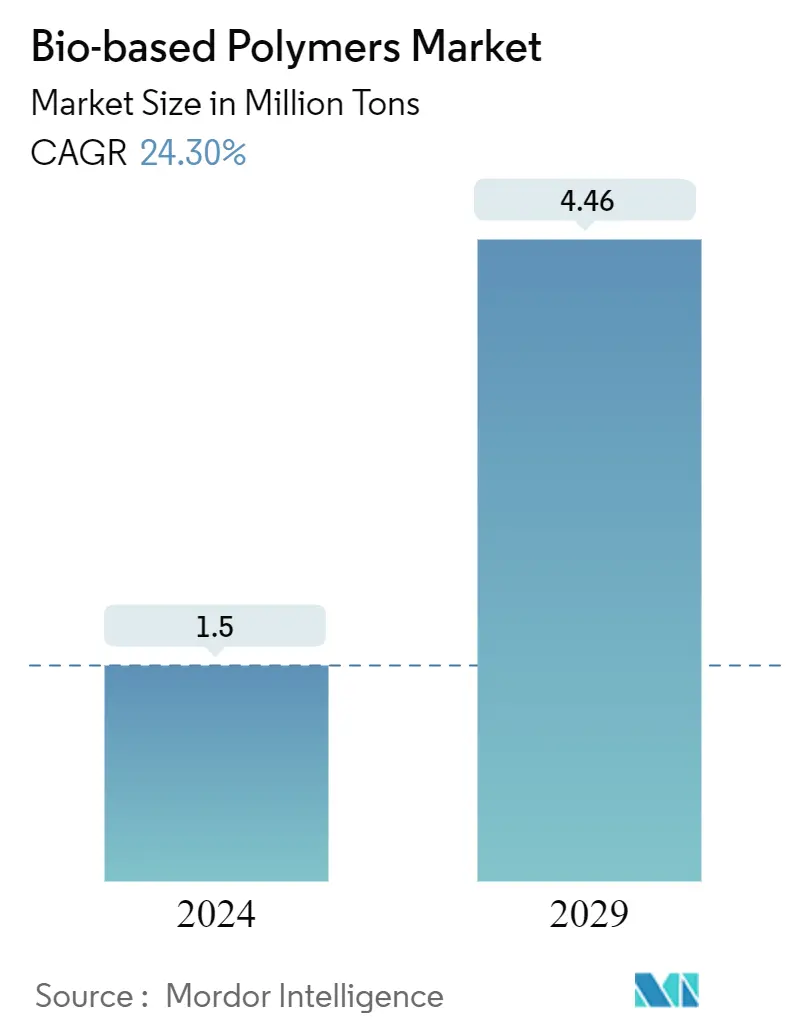

| Market Volume (2024) | 1.5 Million tons |

| Market Volume (2029) | 4.46 Million tons |

| CAGR (2024 - 2029) | 24.30 % |

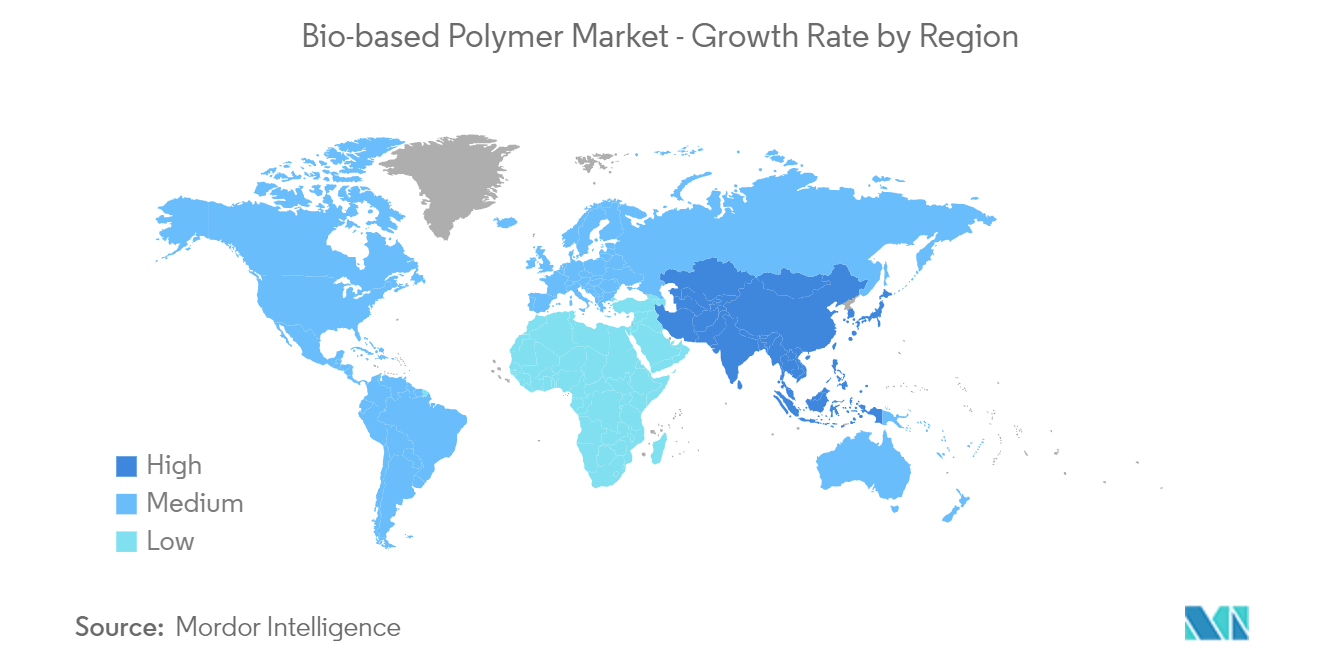

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Bio-based Polymers Market Analysis

The Bio-based Polymers Market size is estimated at 1.5 Million tons in 2024, and is expected to reach 4.46 Million tons by 2029, growing at a CAGR of 24.30% during the forecast period (2024-2029).

The Bio-based Polymers Market size is expected to grow from 1.21 million tons in 2023 to 3.59 million tons by 2028, at a CAGR of 24.30% during the forecast period (2023-2028).

COVID-19 impacted the bio-based polymer market's growth. However, the increased demand for packaged food and online food deliveries during the pandemic and post-pandemic propelled the consumption of packaging coatings, which resulted in the consumption of bio-based polymers.

- Over the short term, increasing demand for sustainable plastics is one of the major factors driving market demand.

- On the flip side, the performance issue with bioplastics and the high prices associated with bio-based polymers compared to petroleum-based polymers are expected to hinder the growth of the market studied.

- The increasing applications of biodegradable plastics are likely to present an opportunity in the future.

- Moreover, the packaging industry dominates the market and is expected to grow during the forecast period.

Bio-based Polymers Market Trends

Increasing Demand from Packaging Industry

- Packaging is one of the largest markets for bio-based polymers. These polymers exhibit excellent clarity and gloss, resistance to food fats and oils, and an aroma barrier. Additionally, they also provide stiffness, twist retention, and printability to the packaging.

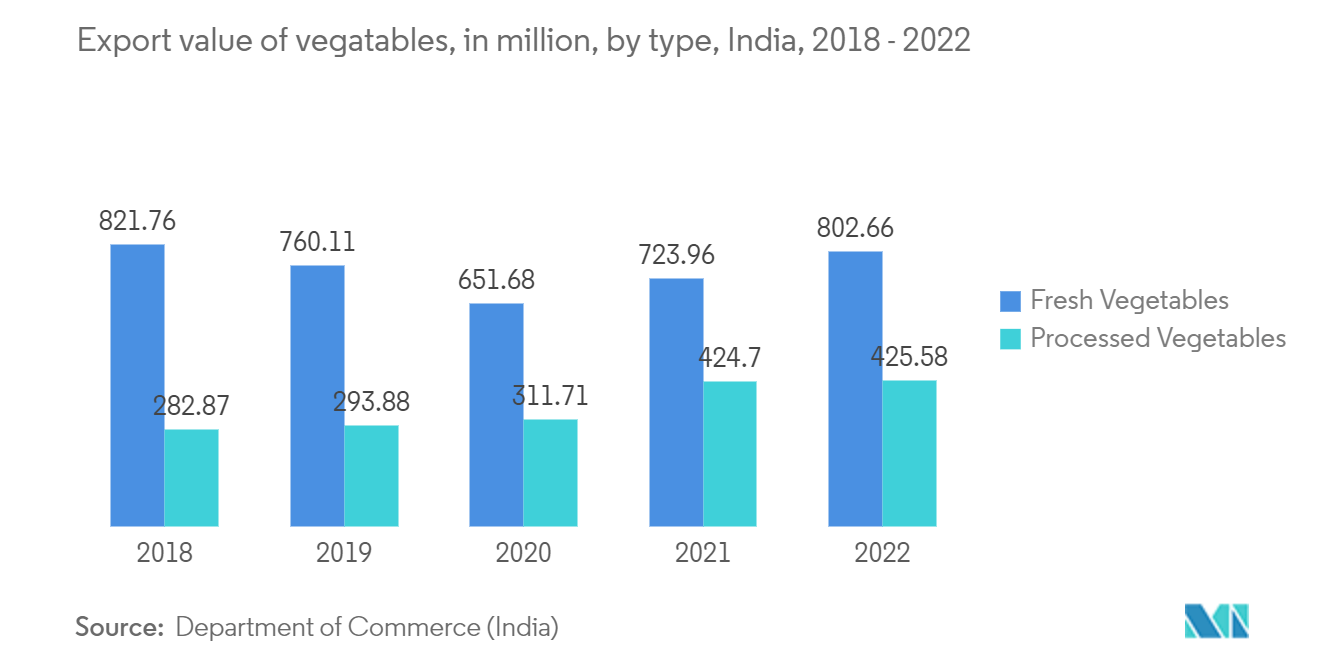

- Bio-based polymers are mostly used in fruit and vegetable packaging in supermarkets, for bread bags and bakery boxes, bottles, envelopes, display carton windows, and shopping or carrier bags, among others. For instance, according to the Department of Commerce (India), the export value of fresh vegetables from India amounted to about USD 802 million in the fiscal year 2022. For processed vegetables, the value stood at nearly USD 425 million in the same year, which shows an increase of 10.87% from the fresh vegetable segment and 0.21% from processed vegetables compared with 2020. Therefore, an increase in the exports of fresh and processed vegetables is expected to create demand for bio-based polymers in the country.

- The bio-based polymer market for packaging is growing rapidly in the European and North American regions. The increasing intervention of the FDA and related organizations in terms of food safety is largely promoting the usage of biodegradable and food-grade plastics for beverage and snack consumption.

- The restaurant chains and food processing industries are increasingly adapting biodegradable materials for food packaging. Consumer awareness is also rising rapidly, especially in emerging economies, in terms of food safety, as some plastics are proven carcinogenic.

- The growth in developing regions, like Asia-Pacific, South America, and the Middle East, is expected to increase in the near future due to the improving food packaging standards of various food and safety organizations.

- Moreover, the higher ease of disposing of biodegradable polymers has further added to their growing demand from the packaging industry.

Europe Region to Dominate the Market

- Europe holds the largest share of bio-based polymers and dominates the global market.

- Public awareness and government initiatives in the region have supported the use of biodegradable polymers in carrier bags, food packaging, food services (cutlery, etc.), and organic waste caddy liners, among others.

- Various countries in the region have been focusing on offering more eco-friendly packaging. This has increased the demand for polylactic acid in the packaging sector.

- The United Kingdom (UK) is among the leading countries in Europe, where the demand for bio-based polymer packaging has been increasing. The higher awareness about the sustainability factors of packaging products, along with recent government initiatives, are creating a favorable market scenario for the growth of the studied market in the country.

- The ban on single-use plastics is among the primary factors that will directly impact the demand for bio-based polymer packaging products. For instance, in 2021, the UK government announced plans to ban single-use plastic cutlery, plates, and polystyrene cups in England to tackle plastic pollution.

- Several existing vendors, as well as startups operating in the packaging industry, are also taking the initiative to promote bio-based polymer packaging in the country. For instance, in June 2022, Magical Mushroom Company, a UK-based company, secured funding of EUR 3.4 million (USD 3.31 million) for its plant-based sustainable packaging.

- Currently, the packaging sector in the United Kingdom has annual sales of GBP 11 billion, and it employs more than 85,000 people.

- The European Union (EU) is working towards the 2050 net-zero emissions goal and tackling the increasing environmental and sustainability crises by implementing the European Green Deal. The inclination towards a more sustainable society is intertwined with the European economy's production, use, and disposal of plastic.

- The growing need for small-size packaging and the growing consumption habits associated with the change in lifestyles are anticipated to propel the demand for bio-based polymers over the forecast period.

Bio-based Polymers Industry Overview

The bio-based polymer market is partially consolidated by nature. Some of the major players in the market (not in any particular order) include BASF SE, Covestro AG, BIOTEC Biologische Naturverpackungen GmbH & Co. KG., thyssenkrupp AG, and NatureWorks LLC, among others.

Bio-based Polymers Market Leaders

-

Covestro AG

-

BASF SE

-

thyssenkrupp AG

-

NatureWorks LLC

-

BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

*Disclaimer: Major Players sorted in no particular order

Bio-based Polymers Market News

The recent developments pertaining to the major players in the market will be covered in the complete study.

Bio-based Polymers Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Preference toward Eco-friendly Polymers to Preserve Environment

4.1.2 Regulation on Non-degradable Polymers in Many Countries

4.1.3 Increasing Consumer Awareness in Developed and Developing Nations

4.1.4 Non-toxic Nature of Biodegradable Polymers

4.2 Restraints

4.2.1 Higher Price Compared to Petroleum-based polymers

4.2.2 Low Awareness in Low Income Countries

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION

5.1 Type

5.1.1 Starch-based Plastics

5.1.2 Poly Lactic Acid (PLA)

5.1.3 PolyHydroxy Alkanoates (PHA)

5.1.4 Polyesters (PBS, PBAT, and PCL)

5.1.5 Cellulose Derivatives

5.2 Application

5.2.1 Agriculture

5.2.2 Textile

5.2.3 Electronics

5.2.4 Packaging

5.2.5 Healthcare

5.2.6 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 Rest of World

5.3.4.1 Brazil

5.3.4.2 Saudi Arabia

5.3.4.3 Rest of the World

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 BASF SE

6.4.2 Biologische Naturverpackungen GmbH & Co. KG.

6.4.3 Cardia Bioplastics

6.4.4 Covestro AG

6.4.5 Corbion

6.4.6 Cortec Group Management Services, LLC

6.4.7 DuPont de Nemours, Inc.

6.4.8 FKuR

6.4.9 FP International

6.4.10 Innovia Films

6.4.11 Merck KGaA

6.4.12 YIELD10 BIOSCIENCE, INC. (Metabolix Inc.)

6.4.13 NatureWorks LLC

6.4.14 Novamont SpA

6.4.15 Rodenburg Biopolymers

6.4.16 SHOWA DENKO K.K.

6.4.17 thyssenkrupp AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increasing Applications of Bio-degradable Plastics

7.2 Increasing Research in Drug Delivery

7.3 Rising Regulations in Emerging Countries

Bio-based Polymers Industry Segmentation

Bio-based materials are derived from plants and are biodegradable. Similarly, bio-based polymers are also derived from plants such as corn, sugarcane, vegetable oil, soybeans, cellulose, and others. These polymers are also known as next-generation polymers, which are used to reduce the use of fossil fuels. Cellulose and starch were the first bio-based polymers invented and used in textiles, packaging construction, and other applications. The bio-based polymers market is segmented by type, application, and geography (Asia-Pacific, North America, Europe, and the rest of the world). By type, the market is segmented into starch-based plastics, polylactic acid, polyhydroxy alkanoates, polyesters, and cellulose derivatives. By application, the market is segmented into agriculture, textiles, electronics, packaging, healthcare, and other applications. The report also covers the market size and forecasts for the bio-based polymers market in 13 countries across major regions. The report offers market sizes and forecasts for each segment based on volume (tons).

| Type | |

| Starch-based Plastics | |

| Poly Lactic Acid (PLA) | |

| PolyHydroxy Alkanoates (PHA) | |

| Polyesters (PBS, PBAT, and PCL) | |

| Cellulose Derivatives |

| Application | |

| Agriculture | |

| Textile | |

| Electronics | |

| Packaging | |

| Healthcare | |

| Other Applications |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

|

Bio-based Polymers Market Research Faqs

How big is the Bio-based Polymers Market?

The Bio-based Polymers Market size is expected to reach 1.5 million tons in 2024 and grow at a CAGR of 24.30% to reach 4.46 million tons by 2029.

What is the current Bio-based Polymers Market size?

In 2024, the Bio-based Polymers Market size is expected to reach 1.5 million tons.

Who are the key players in Bio-based Polymers Market?

Covestro AG, BASF SE, thyssenkrupp AG, NatureWorks LLC and BIOTEC Biologische Naturverpackungen GmbH & Co. KG. are the major companies operating in the Bio-based Polymers Market.

Which is the fastest growing region in Bio-based Polymers Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Bio-based Polymers Market?

In 2024, the Europe accounts for the largest market share in Bio-based Polymers Market.

What years does this Bio-based Polymers Market cover, and what was the market size in 2023?

In 2023, the Bio-based Polymers Market size was estimated at 1.14 million tons. The report covers the Bio-based Polymers Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Bio-based Polymers Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Bio-based Polymers Industry Report

Statistics for the 2024 Biopolymers market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Biopolymers analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.