Cathode Material Market Size

| Study Period | 2019 - 2029 |

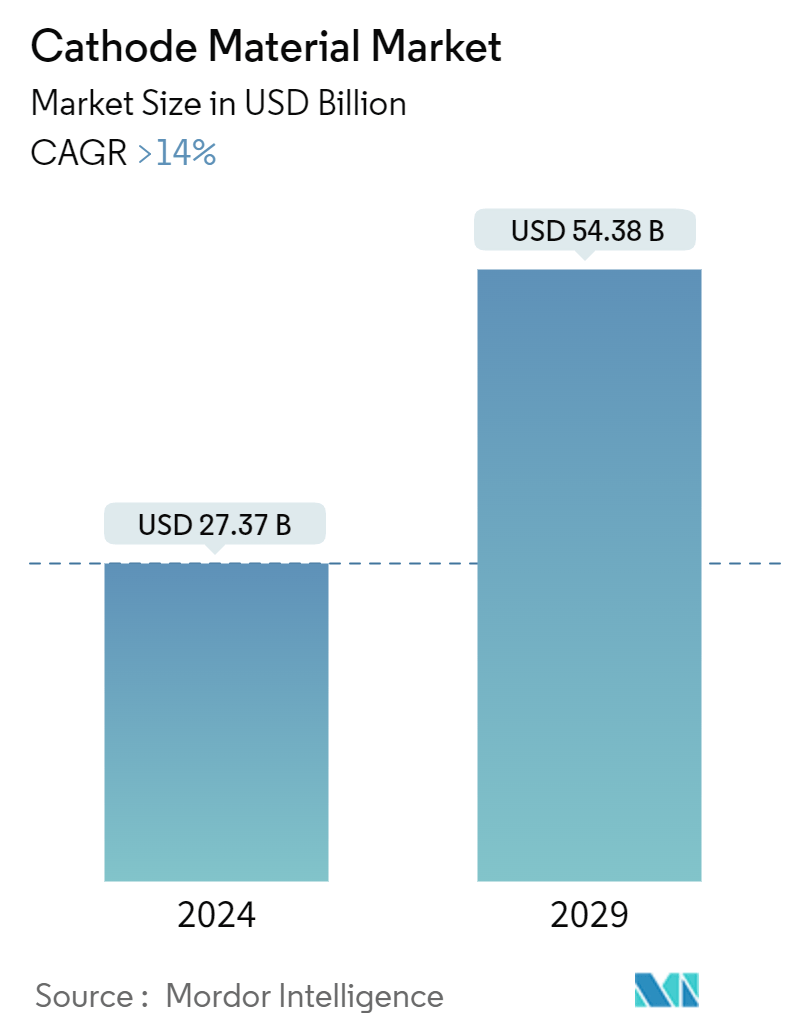

| Market Size (2024) | USD 27.37 Billion |

| Market Size (2029) | USD 54.38 Billion |

| CAGR (2024 - 2029) | > 14.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Cathode Material Market Analysis

The Cathode Material Market size is estimated at USD 27.37 billion in 2024, and is expected to reach USD 54.38 billion by 2029, growing at a CAGR of greater than 14% during the forecast period (2024-2029).

The COVID-19 pandemic had a mixed impact on the global cathode materials market. While there was a temporary slowdown in the manufacturing and automotive sectors, which are major consumers of cathode materials, the growth in electric vehicles (EVs) and renewable energy sectors remained strong. Nevertheless, in 2021, the industry showed signs of recovery and consequently increased its market demand again.

- Over the medium term, increasing demand from electric vehicle manufacturers and increasing demand from consumer electronics are some of the factors driving the growth of the market studied.

- On the flip side, the stringent safety regulations for batteries through storage and transportation are restraints for the market's growth.

- However, the ongoing research and advancement in cathode material and efficient electrolytes may offer opportunities for market growth.

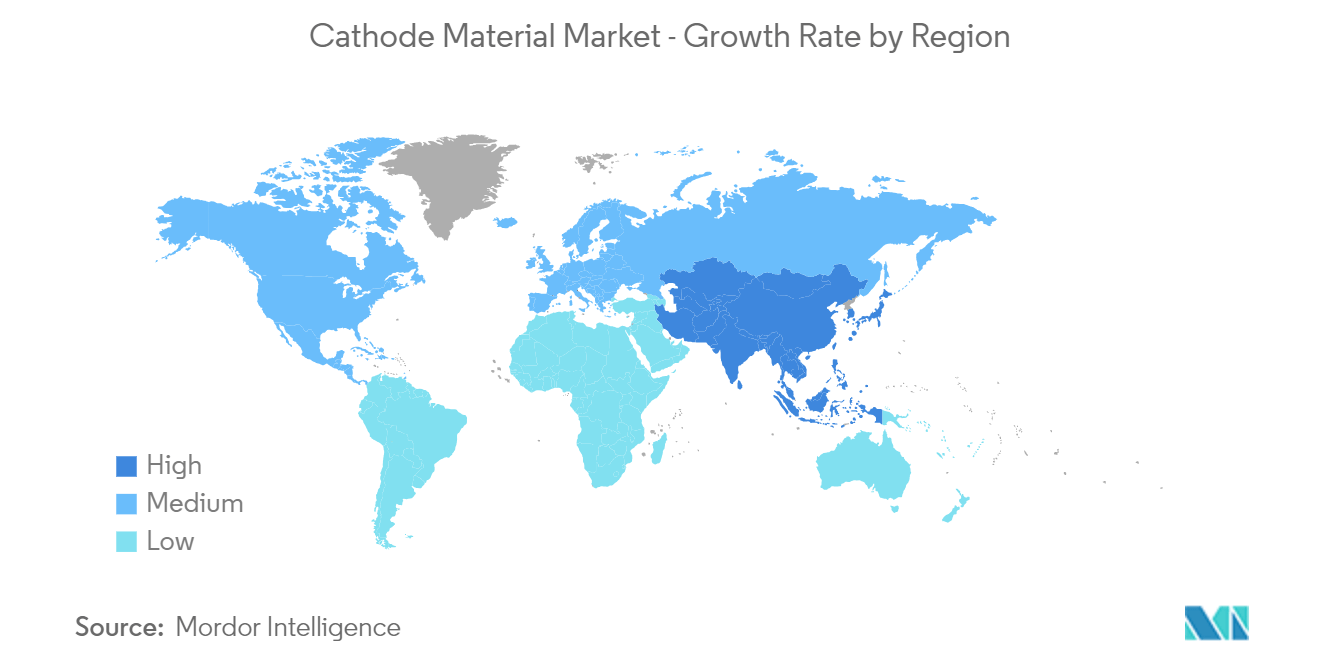

- Asia-Pacific dominates the market, owing to the growing application of cathode material in the automotive industry, which augments the demand for cathode material.

Cathode Material Market Trends

Automotive Industry to Dominate the Market

- The automotive sector dominates due to the extensive consumption of cathode material in vehicle batteries. Increasing fuel demand and reduced Li-ion battery prices have encouraged automobile manufacturers to invest more in electric vehicles.

- The global demand for electric vehicles is rising on account of factors such as increasing investments by governments across the world toward the development of electric vehicles and charging stations.

- Additionally, rising environmental concerns have further benefited the demand for electric vehicles. The large-scale production of EV batteries has resulted in lowering the cost of the batteries, which has fueled the demand for electronic vehicles among the people. The EV battery is one of the significant components of the electric vehicle. Thus, surging demand for electric vehicles is anticipated to benefit the production of cathode materials used in the batteries.

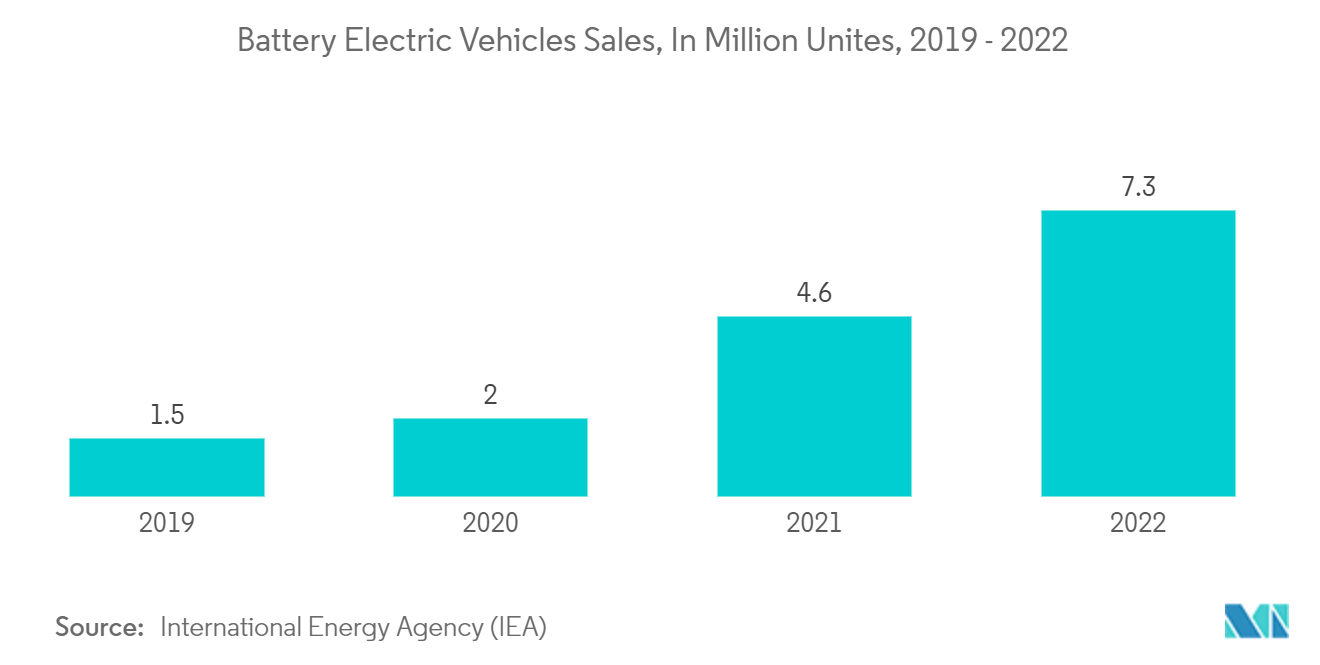

- According to the International Energy Agency (IEA), electric car (including both battery electric vehicles and hybrid electric vehicles) markets observed exponential growth in 2022 as sales globally exceeded 10 million. A total of 14% of all new cars sold in 2022 were electric.

- Furthermore, as per IEA estimates, by the end of 2023, a total of 14 million electric vehicles were sold, representing a 35% Y-o-Y increase.

- Owing to the increased demand for electric vehicles, automotive lithium-ion (Li-ion) battery demand also observed an increase of about 65% and was valued at 550 GWh in 2022 compared to about 330 GWh in 2021.

- Thus, due to the abovementioned point, the automotive (electric vehicle) industry is likely to grow significantly, which, in turn, is expected to enhance the demand in the market studied.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is home to countries like China, India, and Japan, which are among the largest and fastest-growing markets for electric vehicles and electronics products.

- In the year 2022, China was the frontrunner in the global electric vehicles market, accounting for around 60% of global electric car sales. More than 50% of the world’s electric cars are made in China.

- In 2022, electric car sales in India, Thailand, and Indonesia observed significant growth, and collectively, sales of electric cars in these countries were around 80,000 units, which was an increase of more than 200% compared to 2021.

- In India, EV and component manufacturing are gaining significant momentum due to a supportive government incentive program of about USD 3.2 billion that has attracted investments totaling USD 8.3 billion.

- Furthermore, to increase the adoption of EVs, the government of Thailand and Indonesia are also strengthening their policy support schemes.

- The world's largest electronics production base is in China. The fastest growth in the electronics sector has been recorded for electrical products, such as mobile phones, televisions, and computers.

- According to the National Bureau of Statistics, the Chinese electronics market grew by 13% in 2022 compared to 10% growth in 2021. The estimated growth rate for 2023 was 7%. The Chinese market is the largest in the world, even more significant than the combined markets of all industrialized countries.

- Hence, with all such applications and robust demand in the region, Asia-Pacific is expected to be the largest market during the forecast period.

Cathode Material Industry Overview

The cathode material market is partially fragmented in nature, with a number of players operating in the market. Some of the major companies in the market (not in any particular order) are Sumitomo Metal Mining Co. Ltd, Johnson Matthey, BASF SE, Targray, and Umicore.

Cathode Material Market Leaders

-

Sumitomo Metal Mining Co., Ltd.

-

Johnson Matthey

-

BASF SE

-

Targray

-

Umicore

*Disclaimer: Major Players sorted in no particular order

Cathode Material Market News

- February 2024: POSCO announced the construction of the world's largest battery cathode plant cluster for producing cathode materials for nickel, cobalt, and aluminum (NCA) batteries in Gwangyang. The plant will have a production capacity of 52,500-ton cathode materials.

- December 2023: LG Chem started construction for America's largest cathode plant in Tennessee, United States, with a production capacity of 60,000-ton annual production capacity

- October 2023: Umicore announced the expansion of its EV battery materials production by increasing its production capacity for cathode active materials (CAM) and precursor cathode active materials (PCAM) at its plant in Ontario, Canada.

Cathode Materials Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing demand from Automotive Industry

4.1.2 Increasing Production of Electronics Products

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Safety Issues with Transportation and Storage

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

5.1 By Battery Type

5.1.1 Lead-Acid

5.1.2 Lithium-Ion

5.1.3 Other Battery Types (Alkaline Battery, Nickel Cadmium Battery, etc)

5.2 By Material

5.2.1 Lithium Iron Phosphate

5.2.2 Lithium Cobalt Oxide

5.2.3 Lithium-Nickel Manganese Cobalt

5.2.4 Lithium Manganese Oxide

5.2.5 Lithium Nickel Cobalt Aluminium Oxide

5.2.6 Lead Dioxide

5.2.7 Other Materials (Sodium Iron Phosphate, Oxyhydroxide, and Graphite)

5.3 By Application

5.3.1 Automotive

5.3.2 Consumer Electronics

5.3.3 Power Tools

5.3.4 Energy Storage

5.3.5 Other Applications (Medical Devices, Aerospace Components, etc)

5.4 By Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Spain

5.4.3.6 NORDIC Countries

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 Rest of the World

5.4.4.1 South America

5.4.4.2 Middl East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 3M

6.4.2 BASF SE

6.4.3 Hitachi Ltd

6.4.4 Johnson Matthey

6.4.5 LG Chem

6.4.6 Mitsubishi Chemical Corporation

6.4.7 MITSUI MINING & SMELTING CO. LTD

6.4.8 POSCO FUTURE M

6.4.9 PROTERIAL, Ltd.

6.4.10 Sumitomo Metal Mining Co. Ltd

6.4.11 Targray

6.4.12 Umicore

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Advancement in Cathode Material and Efficient Electrolyte

7.2 Other Opportunities

Cathode Material Indsutry Segmentation

Cathode materials are used as voltage-limiting and energy-limiting electrodes in batteries. Cathode materials are widely used in lithium-ion batteries for energy storage, and commonly used batteries have cathode materials as a major component.

The cathode material market is segmented by battery type, material, application, and geography. By battery type, the market is segmented into lead-acid, lithium-ion, and other battery types (alkaline battery, nickel-cadmium battery, etc.). By material, the market is segmented into lithium iron phosphate, lithium cobalt oxide, lithium-nickel manganese, lithium manganese oxide, lithium cobalt nickel, aluminum oxide, lead dioxide, and other materials (sodium iron phosphate, oxyhydroxide, and graphite). By application, the market is segmented into automotive, consumer electronics, power tools, energy storage, and other applications (medical devices, aerospace components, etc). The report also covers the market size and forecasts for the market in 18 countries worldwide. For each segment, the market sizing and forecasts are provided in terms of value (USD).

| By Battery Type | |

| Lead-Acid | |

| Lithium-Ion | |

| Other Battery Types (Alkaline Battery, Nickel Cadmium Battery, etc) |

| By Material | |

| Lithium Iron Phosphate | |

| Lithium Cobalt Oxide | |

| Lithium-Nickel Manganese Cobalt | |

| Lithium Manganese Oxide | |

| Lithium Nickel Cobalt Aluminium Oxide | |

| Lead Dioxide | |

| Other Materials (Sodium Iron Phosphate, Oxyhydroxide, and Graphite) |

| By Application | |

| Automotive | |

| Consumer Electronics | |

| Power Tools | |

| Energy Storage | |

| Other Applications (Medical Devices, Aerospace Components, etc) |

| By Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Cathode Materials Market Research FAQs

How big is the Cathode Material Market?

The Cathode Material Market size is expected to reach USD 27.37 billion in 2024 and grow at a CAGR of greater than 14% to reach USD 54.38 billion by 2029.

What is the current Cathode Material Market size?

In 2024, the Cathode Material Market size is expected to reach USD 27.37 billion.

Who are the key players in Cathode Material Market?

Sumitomo Metal Mining Co., Ltd., Johnson Matthey, BASF SE, Targray and Umicore are the major companies operating in the Cathode Material Market.

Which is the fastest growing region in Cathode Material Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Cathode Material Market?

In 2024, the Asia Pacific accounts for the largest market share in Cathode Material Market.

What years does this Cathode Material Market cover, and what was the market size in 2023?

In 2023, the Cathode Material Market size was estimated at USD 23.54 billion. The report covers the Cathode Material Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Cathode Material Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Cathode Materials Industry Report

Statistics for the 2024 Cathode Materials market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Cathode Materials analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.