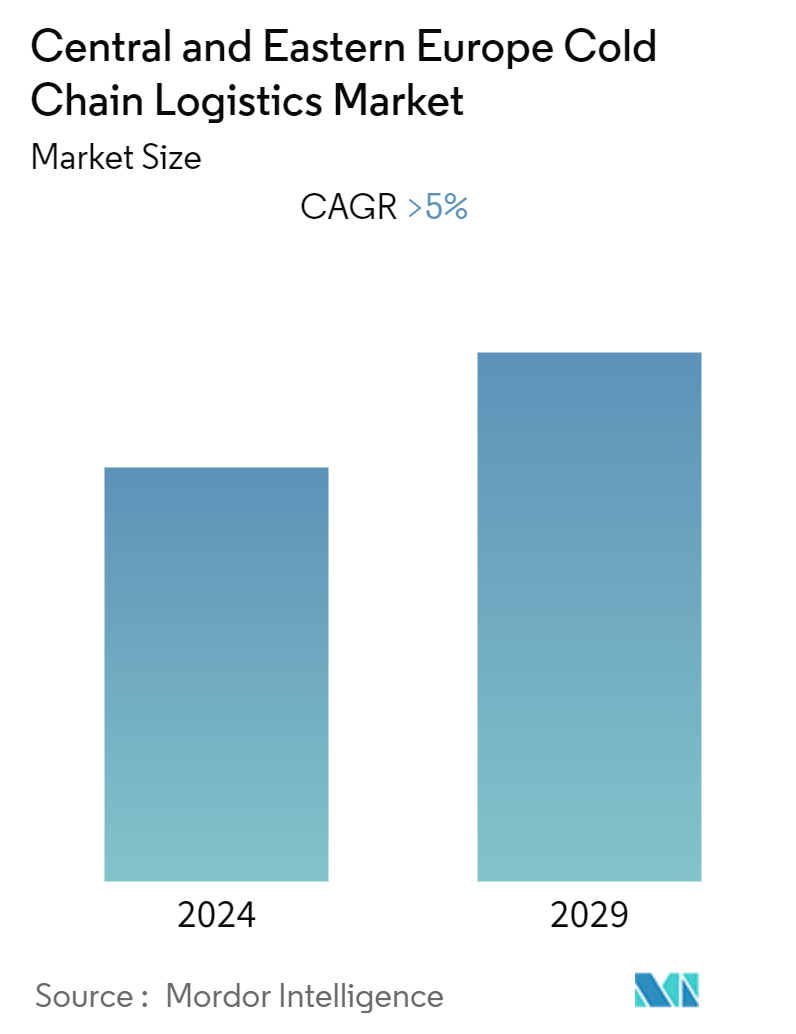

Central and Eastern Europe Cold Chain Logistics Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR (2024 - 2029) | > 5.00 % |

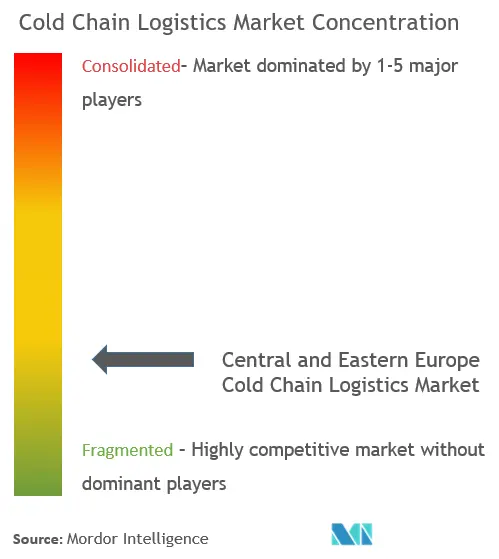

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Central and Eastern Europe Cold Chain Logistics Market Analysis

The Central And Eastern Europe Cold Chain Logistics Market is expected to register a CAGR of greater than 5% during the forecast period.

The central and Eastern Europe cold chain logistics market is estimated to register a CAGR greater than 5% during the forecast period (2022-2027).

Initially, when lockdown measures driven by the COVID-19 pandemic started in March 2020, consumers began panic buying and stockpiling items, with a focus on shelf-stable products. This reduced reefer trucking demands in the EU during Q1 and Q2 2020. The tourist accommodation industry in the EU also saw a sharp decline due to travel restrictions in March and April 2020, which also impacted the expected seasonal demand for reefer goods. However, the situation eased and demand picked up slowly over the next few weeks due to increased sales of alcohol and other beverages.

Labor shortages, increasing energy costs, market consolidation, and a reconfiguration in global food supply chains are some of the challenges in the European cold chain warehousing sector. Labor and energy are the two dominant cost components at European facilities. In 2020, labor accounted for 44% of total costs, with energy accounting for 15%. Covid-19 has pushed food companies to rethink their supply chain designs. The war in Ukraine and subsequent sanctions have accelerated this process.

Because the reconfigured supply chains will change where materials and products are stored, the cold storage sector is directly impacted. Many food companies have opted for just-in-case because the sector has seen a rise in occupancy rates - up to 90%.

Monitoring, storage, and transportation are important factors in the cold chain to avoid degradation in the quality of shipments. Cold chain logistics are anticipated to witness significant growth over the years, owing to the rise in the need for cold chain logistics in the pharmaceutical industry. At present, Germany dominates the market. The Europe cold chain logistics market is driven by growing penetration of e-commerce in the industry, changing lifestyles, increasing tech-driven logistics services, rising number of the refrigerated warehouse, and the growing pharmaceutical sector.

Central and Eastern Europe Cold Chain Logistics Market Trends

Pharmaceutical Industry Driving the Growth of the Market

The pharmaceutical industry was historically not a big consumer of cold chain logistics since the majority of its drugs had no such requirement. Only in the recent past, there has been an explosion of cold chain activities with the growing acceptance of a new class of drugs called biologics. They have only recently come into the world of medicine but have already taken the market by storm, not only in terms of their treatment capability but also in terms of the demands they are placing on the pharmaceutical supply chain. Most biologics require both temperature and time-controlled distribution.

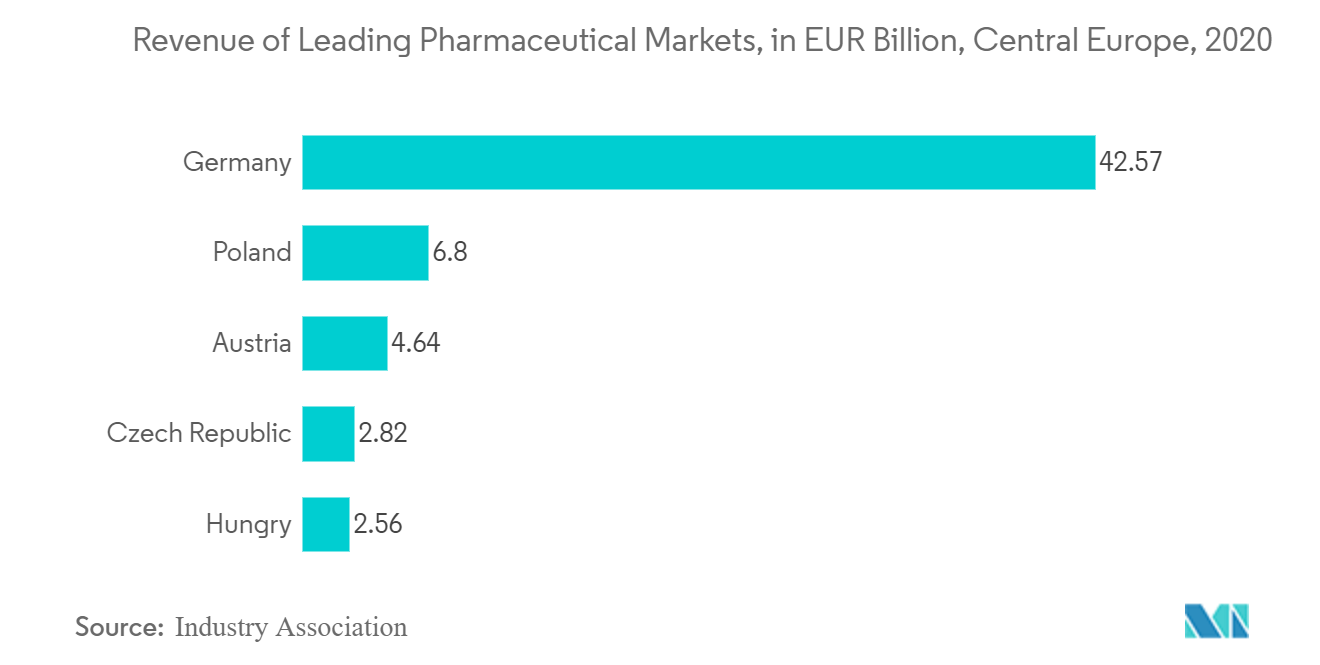

Central Europe is more developed compared to Eastern Europe and most pharmaceutical companies have a strong presence in Central Europe. Countries such as Switzerland, Austria, Poland, and Hungary have a large number of pharmaceutical companies that serve globally.

The pharmaceutical industry in Germany is highly regarded and follows its tradition as the 'world's pharmacy.' Consequently, Germany constitutes a primary pharmaceutical market and the fourth-largest worldwide after the USA, China, and Japan. Furthermore, Germany is the most prominent pharmaceutical manufacturing location within the European Union and ranks second in Europe after Switzerland. Moreover, Germany has the second-highest figures worldwide after the USA in biopharmaceutical production.

As the pharmaceutical sector grows, the companies are looking beyond traditional markets for globalized, traceable, secure and compliant supply chains providing services including cold-chain solutions, storage in multiple temperature zones, reverse logistics and advanced tracking technologies, which ensure total supply chain visibility, and reporting on merchandise flows across all modes of transport.

E-commerce Increasing the Demand for Cold Chain Logistics

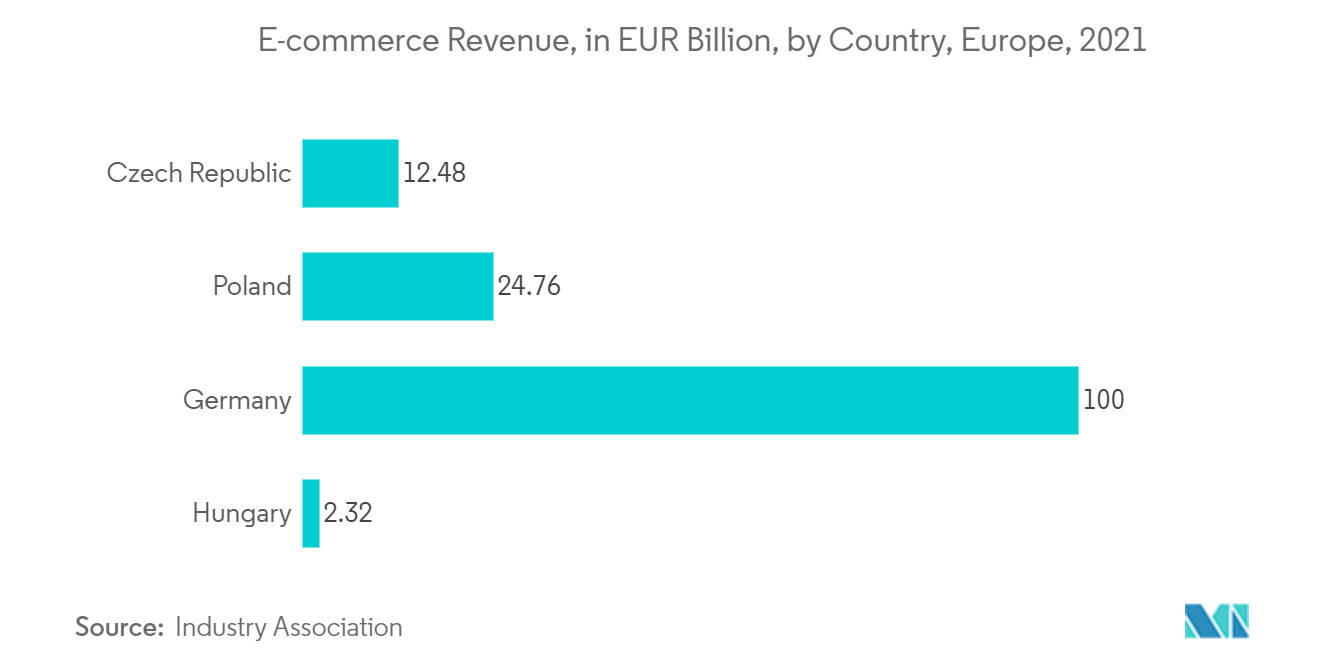

European e-commerce has grown steadily over the past years, especially since the outbreak of the coronavirus. According to recent figures, online sales are contributing an increasing share of total retail sales in the European continent. In 2021, this share came to 19% in Central and Western Europe. This is a rise of 6% when compared to 2019, before the pandemic.

Ecommerce sales in Europe grew from EUR 621 billion in 2019 and were worth EUR 757 billion in 2020. Most of the online turnover is still being generated in Western Europe, which accounts for approximately 70% of total European online retail turnover. Central and Eastern Europe together show a 7% share of European e-commerce.

Cold Chain logistics are the systems in which companies store, package, and ship perishable goods, There are many different elements to cold chain services, from storage practices and packaging methods all the way to properly managing the inventory of perishable goods. For e-commerce businesses, the only way they can see long-term growth and success is by streamlining and optimizing their cold chain logistics.

Central and Eastern Europe Cold Chain Logistics Industry Overview

The central and Eastern Europe cold chain logistics market is fragmented in nature aiding the domestic as well as international transportation of temperature-sensitive goods. It is undergoing developments with the introduction of solar-powered refrigerated units, multi-temperature trucks, and freight optimization software. International and local players like Kuehne + Nagel, Noatum Logistics, MSC Mediterranean Shipping Company, Lineage Logistics Holdings, Blue Water Shipping and many such companies are operational in the market.

Central and Eastern Europe Cold Chain Logistics Market Leaders

-

Nordfrost

-

PLG Logistics & Warehousing

-

Baltic Logistic Solutions

-

Nagel-Group

-

FRIGO Coldstore Logistics

*Disclaimer: Major Players sorted in no particular order

Central and Eastern Europe Cold Chain Logistics Market News

- March 2021 : Danone Sp. z o.o., part of the global food company Danone, extends its cooperation with Kuehne+Nagel in Poland for another seven years. In conjunction, a new distribution center spanning 11,079 sqm has been opened in Ruda Śląska. The facility is equipped to store goods at a controlled temperature of 4 - 6°C, including co-packing in cold and ambient chambers. While unloading and loading goods, product integrity is ensured by insulated cooling aprons, gates and platforms.

- June 2021 : Lineage Logistics, one of the world's leading and most innovative temperature-controlled industrial REIT and logistics solutions providers, announced it has reached an agreement to acquire Kloosterboer Group ('Kloosterboer'), a leading independent integrated platform for temperature-controlled storage, logistics and value-added services in Europe. The transaction is subject to regulatory clearance and completion of the employee consultation process. Kloosterboer consists of eleven facilities across the Netherlands, France, Germany, Canada and South Africa.

Central and Eastern Europe Cold Chain Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Dynamics

4.2.1 Drivers

4.2.2 Restraints

4.3 Value Chain / Supply Chain Analysis

4.4 Industry Policies and Regulations

4.5 Technological Developments in the Sector

4.6 Industry Attractiveness - Porter's Five Forces Analysis

4.7 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

5.1 By Service

5.1.1 Storage

5.1.2 Transportation

5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

5.2 By Temperature

5.2.1 Chilled

5.2.2 Frozen

5.3 By Application

5.3.1 Fruits and Vegetables

5.3.2 Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.)

5.3.3 Fish, Meat and Poultry

5.3.4 Processed Food

5.3.5 Pharmaceutical (Including Biopharma)

5.3.6 Bakery and Confectionery

5.3.7 Other Applications

5.4 By Geography

5.4.1 Poland

5.4.2 Slovakia

5.4.3 Czech Republic

5.4.4 Hungary

5.4.5 Romania

5.4.6 Rest of Central and Eastern Europe

6. COMPETITIVE LANDSCAPE

6.1 Market Concentration Overview

6.2 Company Profiles

6.2.1 Nordfrost

6.2.2 PLG Logistics and Warehousing

6.2.3 Baltic Logistic Solutions

6.2.4 Nagel-Group

6.2.5 FRIGO Coldstore Logistics

6.2.6 Magnum Logistics OU

6.2.7 NewCold

6.2.8 Beno-Trans

6.2.9 Gartner KG

6.2.10 Wilms Frozen Food Service*

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. DISCLAIMER

Central and Eastern Europe Cold Chain Logistics Industry Segmentation

Cold chain logistics consists of the storage and transportation of temperature-sensitive products along the supply chain by using thermal refrigerated packaging methods and logistical planning so that the integrity of these shipments is protected. Cold chain products are transported through various means such as refrigerated railcars & trucks, reefers & air cargos, refrigerated cargo ships, and others. Major elements of cold chain logistics consist of cooling systems, cold storage, cold transport, and cold processing & distribution.

The Central and Eastern Europe Cold Chain Logistics Market is segmented by service, temperature, application, and geography. By service, the market is segmented into storage, transportation, and value-added services. By temperature, the market is segmented into chilled and frozen. By application, the market is segmented into fruits and vegetables, dairy products, fish, meat and poultry, processed food, pharmaceutical, bakery and confectionery, and other applications. By geography, the market is segmented into Poland, Slovakia, the Czech Republic, Hungary, Romania, and the Rest of Central and Eastern Europe.

| By Service | |

| Storage | |

| Transportation | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| By Temperature | |

| Chilled | |

| Frozen |

| By Application | |

| Fruits and Vegetables | |

| Dairy Products (Milk, Butter, Cheese, Ice Cream, etc.) | |

| Fish, Meat and Poultry | |

| Processed Food | |

| Pharmaceutical (Including Biopharma) | |

| Bakery and Confectionery | |

| Other Applications |

| By Geography | |

| Poland | |

| Slovakia | |

| Czech Republic | |

| Hungary | |

| Romania | |

| Rest of Central and Eastern Europe |

Central and Eastern Europe Cold Chain Logistics Market Research FAQs

What is the current Central and Eastern Europe Cold Chain Logistics Market size?

The Central and Eastern Europe Cold Chain Logistics Market is projected to register a CAGR of greater than 5% during the forecast period (2024-2029)

Who are the key players in Central and Eastern Europe Cold Chain Logistics Market?

Nordfrost, PLG Logistics & Warehousing, Baltic Logistic Solutions, Nagel-Group and FRIGO Coldstore Logistics are the major companies operating in the Central and Eastern Europe Cold Chain Logistics Market.

What years does this Central and Eastern Europe Cold Chain Logistics Market cover?

The report covers the Central and Eastern Europe Cold Chain Logistics Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Central and Eastern Europe Cold Chain Logistics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Central and Eastern Europe Cold Chain Logistics Industry Report

Statistics for the 2024 Central and Eastern Europe Cold Chain Logistics market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Central and Eastern Europe Cold Chain Logistics analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.