Consumer Electronics Optoelectronics Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

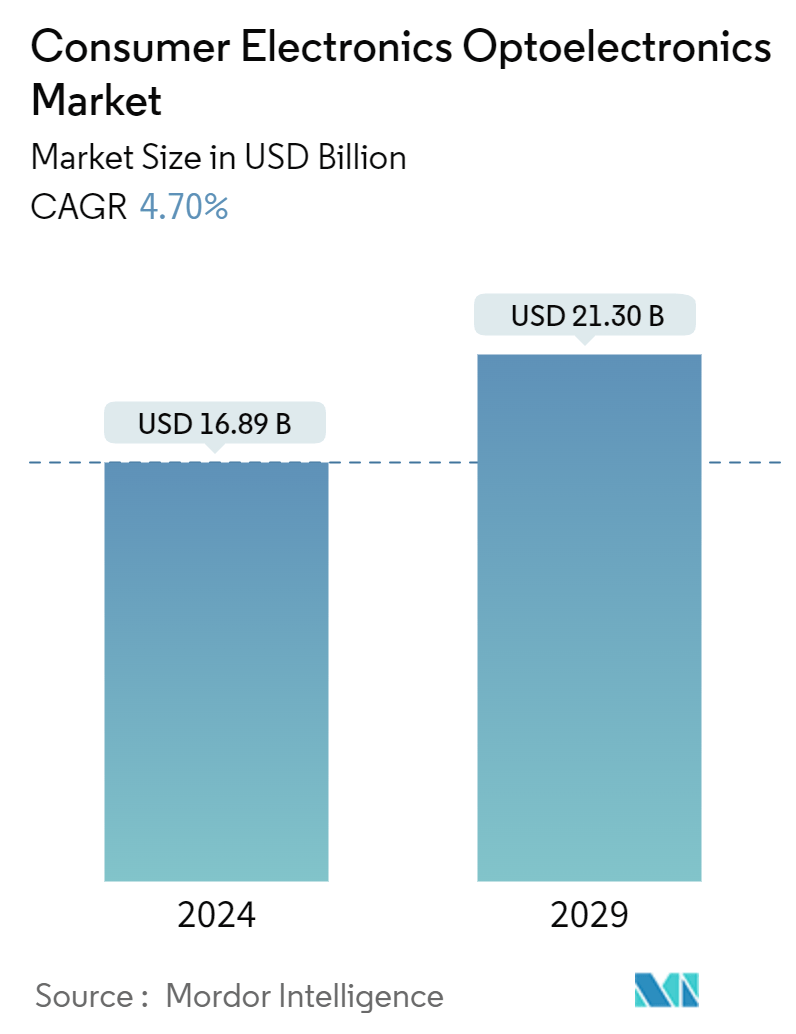

| Market Size (2024) | USD 16.89 Billion |

| Market Size (2029) | USD 21.30 Billion |

| CAGR (2024 - 2029) | 4.70 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Consumer Electronics Optoelectronics Market Analysis

The Consumer Electronics Optoelectronics Market size is estimated at USD 16.89 billion in 2024, and is expected to reach USD 21.30 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

- The global consumer electronics market is poised for growth, largely propelled by the widespread adoption of smartphones. Factors such as technological advancements, the rollout of 5G, and a culture of innovation are set to boost this demand further. As technology continues to advance at a significant pace, the demand for more efficient, powerful, and compact optoelectronics increases. Innovations such as 5G connectivity, the Internet of Things (IoT), and artificial intelligence (AI) require advanced semiconductor devices to support their functionality, driving the market forward.

- Most consumer electronics, including laptops, mobile phones, game consoles, microwaves, and refrigerators, operate with optoelectronics such as LEDs, image sensors, photovoltaic cells, and laser diodes. The high demand for these devices is a vital factor encouraging the growth of the market.

- Moreover, several smartphone manufacturers focus on launching technologically advanced smartphones to gain a competitive edge, further driving market growth. For instance, in April 2024, Redmi unveiled a new version of the Redmi Note 13 Pro+ 5G. This unique phone edition is referred to as the Redmi Note 13 Pro+ 5G World Champions Edition or the AFA Edition in India. The Redmi Note 13 Pro+ 5G runs on a MediaTek Dimensity7200-Ultra SoC paired with a maximum of 12 GB RAM and 512 GB storage.

- In recent years, LED televisions have gained significant traction among consumers owing to their power-saving features. LED TVs, utilizing light-emitting diodes (LED) for backlighting, boast superior energy efficiency. In contrast, the majority of LCD TVs rely on cold cathode fluorescent lamps (CCFL), leading to a notable disparity in power consumption. This variance translates to potential power savings of around 30%.

- Supply chain disruptions restrict semiconductor devices, including optoelectronics mass production. Geopolitical conflicts have further disrupted the semiconductor supply chain, impacting the global supply chain and hampering the production of consumer electronics. Further, in 2024, the Israel-Hamas conflict is expected to cause further disruption to the worldwide semiconductor supply chain.

- Rising inflation rates are driving up the costs of goods and services, notably consumer electronics. These elevated costs erode purchasing power for consumers and businesses, consequently restricting market growth. The war between Russia and Ukraine, high energy costs, and stricter emissions standards have been noted as the primary reasons for the continued shortage of raw materials such as copper, which are expected to hamper the production process of optoelectronics.

Consumer Electronics Optoelectronics Market Trends

Image Sensors are Expected to Hold Major Market Share

- The rising sales of consumer electronics, such as televisions, laptops, computers, and home appliances, significantly drive the demand for image sensors. According to the Consumer Technology Association, from 2012 to 2021, the United States witnessed a consistent rise in retail revenue within the consumer electronics market. Projections indicate that by 2024, the retail sales for consumer electronics in the United States are set to hit a staggering USD 512 billion. In 2023, OLED TVs were anticipated to rake in USD 2.3 billion in revenue, while portable gaming consoles were poised to bring in USD 1.5 billion.

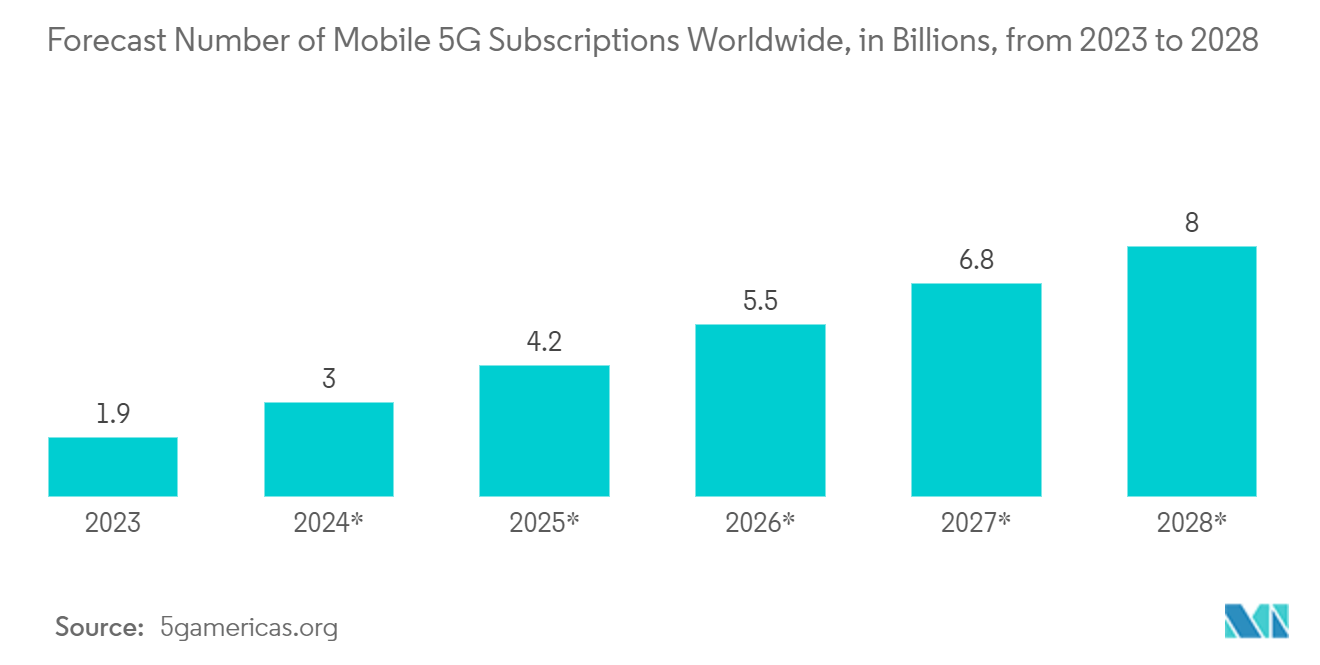

- Moreover, the rising 5G smartphone penetration worldwide creates immense market opportunities for optoelectronics vendors. For instance, according to Ericsson, the number of smartphone mobile network subscriptions worldwide reached almost 7 billion in 2023, and it is forecasted to exceed 7.7 billion by 2028. China, India, and the United States have the highest number of smartphone mobile network subscriptions.

- Further, with the advancement of technology, image sensors are becoming much smaller, affordable, and more power-efficient. Key vendors are witnessing a significant increase in the sales of cameras and smartphones, which are expected to create significant demand for image sensors. For instance, Canon Inc., one of the leading vendors in the camera market, registered revenue growth in 2023, an increase of 3.7% from 2022. The 2023 revenue reported JPY 4.18 billion (USD 28.335 billion). The company’s net profit increased by 8.4% in 2023 compared to 2022.

- Key market vendors are focusing on product launches and new product innovations to fulfill consumer demand. For instance, in February 2024, Sony launched the First Global Shutter Image Sensor in the Alpha 9 III Camera. The camera features advanced video capabilities, such as 4K 120p recording without cropping and a Sony Cinetone feature for enhanced image quality.

- In March 2024, Sony launched a new CMOS image sensor fab in Thailand for the imaging and sensing business. The new fab, “Building 4,” will be used for the assembly of image sensors for automotive applications and the mass production of laser diodes. Such factors are projected to foster market growth.

China is Expected to Witness a High Market Growth Rate

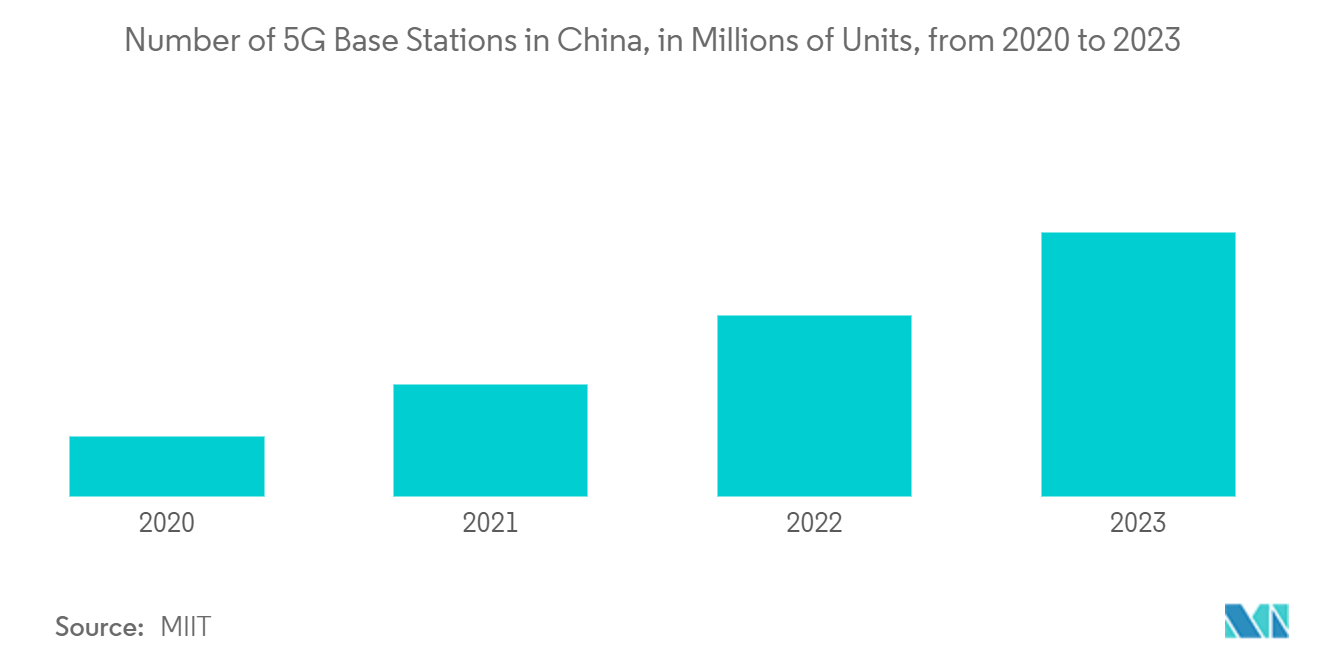

- China is expected to hold a major market share in the consumer electronics optoelectronics market. The rising 5G penetration across the major countries of the region drives the demand for 5G smartphones, laptops, and tablets. For instance, China, in collaboration with its government, has made substantial progress in expanding its 5G network nationwide.

- The country's major telecom operators—China Mobile, China Unicom, and China Telecom—have led the construction of robust 5G infrastructure in urban centers and key regions. This initiative has enabled millions of users to access high-speed, reliable internet services across China. The deployment of base stations has now reached a critical stage.

- With the rising proliferation of 5G smartphones, many players are introducing image sensors targeted for 5G smartphones, which is contributing positively to the market. In March 2024, Huawei, China's leading telecommunications equipment firm, unveiled its latest 5G smartphone in April 2024. The P70 series, heralded as Huawei's next flagship, was slated for an early debut next month. Following a pattern akin to Samsung Electronics, which rolled out its Galaxy S series in the first half and the Z series later, Huawei introduced its P series in the year's first half and planned to introduce the Mate series in the latter half. The upcoming P70 series will feature the Kirin 9000S chip, a component also found in the Mate 60 series. Notably, the Mate 60 series, which made its debut in August 2023, showcased a 5G chip crafted using Huawei's proprietary 7-nanometer (nm) process, catching global attention.

- Further, the household appliance sector in China has evolved into a multi-billion dollar industry. By April 2024, the retail sales value for household appliances and consumer electronics in China exceeded CNY 64 billion (USD 8.85 billion). Such growth in the Chinese household appliances sector is primarily driven by rising individual incomes and increasing urbanization, which is expected to drive the demand for optoelectronics in the country.

Consumer Electronics Optoelectronics Industry Overview

The consumer electronics optoelectronics market is fragmented and features key players like Vishay Intertechnology Inc., Omnivision Technologies Inc., Samsung Electronics, SK Hynix Inc., and Sony Corporation. Market participants strategically leverage partnerships and acquisitions to bolster their product portfolios and establish a sustainable competitive edge.

- In July 2024, Samsung Electronics unveiled three cutting-edge mobile image sensors: the Isocell HP9, Isocell GNJ, and Isocell JN5. Samsung designed these sensors to cater to the escalating demands of smartphone users, who increasingly seek superior camera quality and performance for their primary and secondary cameras.

- In February 2024, Gpixel Microelectronics launched the GSENSE3243BSI, a monochrome rolling shutter CMOS image sensor. The sensor has 8192 x 5232 resolution, a 43 MP camera, 31.1 diagonal field, 3.2 μm pixel size, and up to 100 fps frame rate. It comprises flexible ROIs and on-chip binning, making it capable of attaining higher frame rates at lower resolutions. The new sensor has a dynamic range of 74.7 dB at 14-bit HDR and 80.8dB at 14-bit HDR x 4.

Consumer Electronics Optoelectronics Market Leaders

-

Sony Corporation

-

Vishay Intertechnology Inc.

-

Omnivision Technologies Inc.

-

Samsung Electronics

-

SK Hynix Inc.

*Disclaimer: Major Players sorted in no particular order

Consumer Electronics Optoelectronics Market News

- March 2024: OMNIVISION, a prominent global semiconductor solutions developer, unveiled its latest innovation, the OV50K40. This cutting-edge smartphone image sensor, powered by TheiaCel technology, achieves a high dynamic range (HDR) comparable to the human eye in a single exposure. The OV50K40 is poised to redefine industry standards, particularly for flagship rear-facing main cameras.

- November 2023: Onsemi announced a strategic shift to commence the internal production of CMOS image sensors (CIS) in 2024. This move is a notable departure from its traditional approach of relying on external partners for manufacturing.

Consumer Electronics Optoelectronics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumption and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Demand for 5G Smartphones, and Laptops

5.1.2 Technology Advancements, and AI Developments will Drive the Growth

5.2 Market Restraints

5.2.1 High Manufacturing and Fabricating Costs

5.2.2 Challenges With Energy Loss and Heating of Optoelectronic Devices

6. MARKET SEGMENTATION

6.1 By Device Type

6.1.1 LED

6.1.2 Laser Diode

6.1.3 Image Sensors

6.1.4 Optocouplers

6.1.5 Photovoltaic cells

6.1.6 Other Device Types

6.2 By Geography***

6.2.1 United States

6.2.2 Europe

6.2.3 Japan

6.2.4 China

6.2.5 South Korea

6.2.6 Taiwan

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 SK Hynix Inc.

7.1.2 Panasonic Corporation

7.1.3 Samsung Electronics

7.1.4 Omnivision Technologies Inc.

7.1.5 Sony Corporation

7.1.6 Ams Osram AG

7.1.7 Signify Holding

7.1.8 Vishay Intertechnology Inc.

7.1.9 Texas Instruments Inc.

7.1.10 LITE-ON Technology Corporation

7.1.11 Rohm Company Limited

7.1.12 Mitsubishi Electric Corporation

7.1.13 Broadcom Inc.

7.1.14 Sharp Corporation

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

Consumer Electronics Optoelectronics Industry Segmentation

Optoelectronic devices are electronic devices and systems that involve the study, detection, and control of light. They are considered a sub-field of photonics and are used to convert electrical energy into light or vice versa. The study tracks the revenue accrued through the sale of consumer electronics optoelectronics by various players worldwide. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market.

The consumer electronics optoelectronics market is segmented by device type (LED, laser diode, image sensors, optocouplers, photovoltaic cells, and other device types) and geography (United States, Europe, China, Japan, Korea, Taiwan, and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Device Type | |

| LED | |

| Laser Diode | |

| Image Sensors | |

| Optocouplers | |

| Photovoltaic cells | |

| Other Device Types |

| By Geography*** | |

| United States | |

| Europe | |

| Japan | |

| China | |

| South Korea | |

| Taiwan |

Consumer Electronics Optoelectronics Market Research FAQs

How big is the Consumer Electronics Optoelectronics Market?

The Consumer Electronics Optoelectronics Market size is expected to reach USD 16.89 billion in 2024 and grow at a CAGR of 4.70% to reach USD 21.30 billion by 2029.

What is the current Consumer Electronics Optoelectronics Market size?

In 2024, the Consumer Electronics Optoelectronics Market size is expected to reach USD 16.89 billion.

Who are the key players in Consumer Electronics Optoelectronics Market?

Sony Corporation, Vishay Intertechnology Inc., Omnivision Technologies Inc., Samsung Electronics and SK Hynix Inc. are the major companies operating in the Consumer Electronics Optoelectronics Market.

What years does this Consumer Electronics Optoelectronics Market cover, and what was the market size in 2023?

In 2023, the Consumer Electronics Optoelectronics Market size was estimated at USD 16.10 billion. The report covers the Consumer Electronics Optoelectronics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Consumer Electronics Optoelectronics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Consumer Electronics Optoelectronics Industry Report

Statistics for the 2024 Consumer Electronics Optoelectronics market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Consumer Electronics Optoelectronics analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.