Market Size of Data Center Accelerator Industry

| Study Period | 2019 - 2029 |

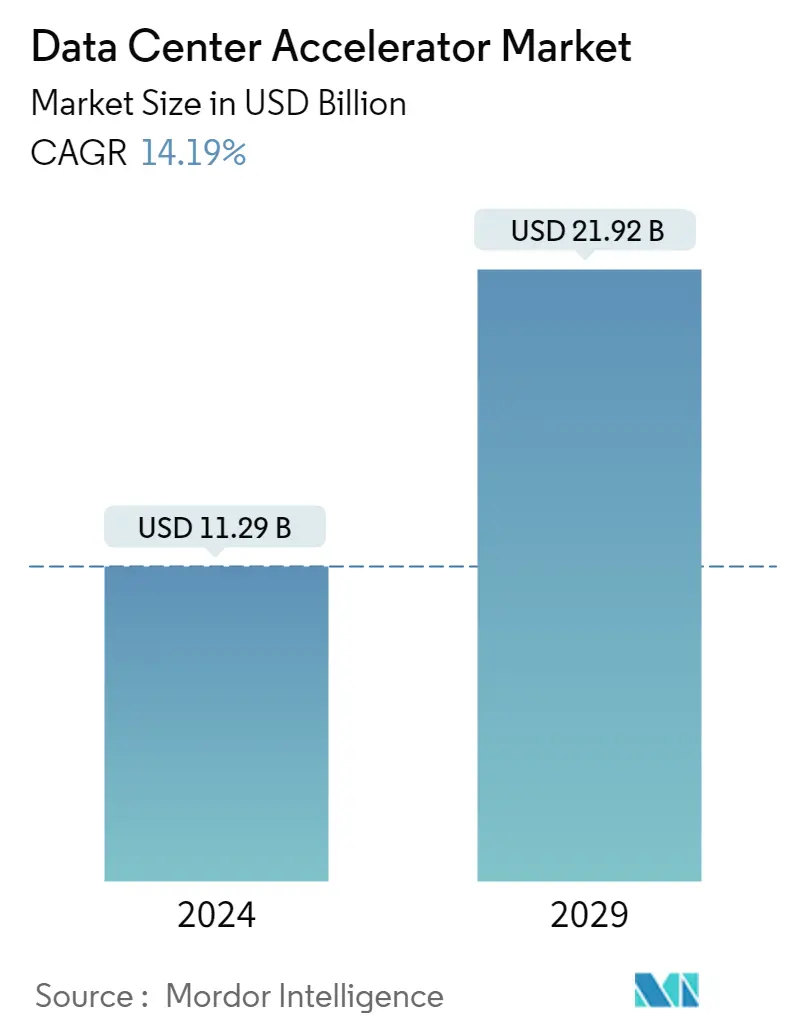

| Market Size (2024) | USD 11.29 Billion |

| Market Size (2029) | USD 21.92 Billion |

| CAGR (2024 - 2029) | 14.19 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Data Center Accelerator Market Analysis

The Data Center Accelerator Market size is estimated at USD 11.29 billion in 2024, and is expected to reach USD 21.92 billion by 2029, growing at a CAGR of 14.19% during the forecast period (2024-2029).

The growing demand for artificial intelligence in HPC data centers and the increasing usage of cloud-based services likely drive the data center accelerator market over the coming years.

- From scientific discoveries to artificial intelligence (AI), modern data centers are crucial to solving some of the world's most critical challenges. These advanced data centers are transforming to increase networking bandwidth and optimize workloads like artificial intelligence. Datacenter administrators also expect a lower total cost of ownership, lower power, and new services.

- The ever-increasing demands on the data center are pushing existing infrastructure to its limit, driving the need for adaptable solutions that can optimize performance across a broad range of workloads and extend the lifecycle of existing infrastructure, thus, ultimately reducing TCO. Players have been actively expanding their product portfolio to capture this demand and gain market recognition.

- Further, most computing system growth would stem from higher demand for AI applications at cloud computing data centers. At these locations, GPUs are now used for almost all training applications. However, as ASICs enter the market, GPUs would likely become more customized to meet the demand for Deep Learning (DL). In addition to ASICs and GPUs, FPGAs would also have a crucial role in future AI training, primarily for specialized data center applications that must reach the market quickly or require customization, such as those for prototyping new DL applications.

- The lack of feasibility of providing to small businesses, limiting its utilization scope to medium and large organizations, and the increased cost of these accelerators are expected to act as market restraints.

- The COVID-19 pandemic has posed additional stress on the overall economy across sectors. It has also shifted focus towards a digital economy. One of China's top cloud computing providers, Alibaba Cloud, is investing billions in building next-generation data centers to support digital transformation needs in a 'post-pandemic world. In April last year, Alibaba Cloud announced it would invest RMB 200 billion (USD 28.99 billion) in core technologies and future-oriented data centers over the next three years.

Data Center Accelerator Industry Segmentation

Datacenter accelerators are hardware designed and used to process visual data. It is a hardware device or software program that improves the overall performance of computers. Datacenter accelerators help increase consumer-driven data demand and use AI-based services to drive the demand for AI-centric data centers.

The scope of the study covers revenues accrued by companies offering the critical types of processors, such as CPU, GPU, FPGA, and ASIC, across various applications, namely high-performance computing, artificial intelligence, and others. The study also covers key regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

| By Processor Type | |

| CPU (Central Processing Unit) | |

| GPU (Graphics Processing Unit) | |

| FPGA (Field-Programmable Gate Array) | |

| ASIC (Application-specific Integrated Circuit) |

| By Application | |

| High-performance Computing | |

| Artificial Intelligence | |

| Other Applications |

| By Geography | |

| North America | |

| Europe | |

| Asia Pacific | |

| Latin America | |

| Middle East & Africa |

Data Center Accelerator Market Size Summary

The Data Center Accelerator Market is poised for significant growth, driven by the increasing demand for artificial intelligence and cloud-based services. Modern data centers are evolving to enhance networking bandwidth and optimize workloads, particularly in AI and high-performance computing (HPC). This transformation is necessitated by the growing demands on data centers, which require adaptable solutions to optimize performance and extend the lifecycle of existing infrastructure. The market is witnessing active expansion as players broaden their product portfolios to meet this demand. The introduction of application-specific integrated circuits (ASICs), graphics processing units (GPUs), and field-programmable gate arrays (FPGAs) is reshaping the landscape, with FPGAs offering promising growth opportunities due to their flexibility and cost-effectiveness in data center applications.

The Asia-Pacific region is expected to be a major contributor to the global demand for data center accelerators, fueled by substantial investments in IT infrastructure. Countries like Australia and India are seeing significant developments in data center capabilities, driven by both local and multinational players. The market is characterized by the presence of both global giants and small to medium enterprises, with key players like Intel, NVIDIA, and AMD leading the charge. Strategic partnerships, acquisitions, and investments in new technologies are common as companies strive to enhance their offerings and maintain a competitive edge. The market's growth is further supported by the increasing reliance on big data analytics and the need for optimized data processing solutions in cloud computing environments.

Data Center Accelerator Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Value Chain Analysis

-

1.3 Industry Attractiveness - Porter's Five Force Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Intensity of Competitive Rivalry

-

1.3.5 Threat of Substitute Products

-

-

1.4 Assessment of Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Processor Type

-

2.1.1 CPU (Central Processing Unit)

-

2.1.2 GPU (Graphics Processing Unit)

-

2.1.3 FPGA (Field-Programmable Gate Array)

-

2.1.4 ASIC (Application-specific Integrated Circuit)

-

-

2.2 By Application

-

2.2.1 High-performance Computing

-

2.2.2 Artificial Intelligence

-

2.2.3 Other Applications

-

-

2.3 By Geography

-

2.3.1 North America

-

2.3.2 Europe

-

2.3.3 Asia Pacific

-

2.3.4 Latin America

-

2.3.5 Middle East & Africa

-

-

Data Center Accelerator Market Size FAQs

How big is the Data Center Accelerator Market?

The Data Center Accelerator Market size is expected to reach USD 11.29 billion in 2024 and grow at a CAGR of 14.19% to reach USD 21.92 billion by 2029.

What is the current Data Center Accelerator Market size?

In 2024, the Data Center Accelerator Market size is expected to reach USD 11.29 billion.