Europe Connected Car Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

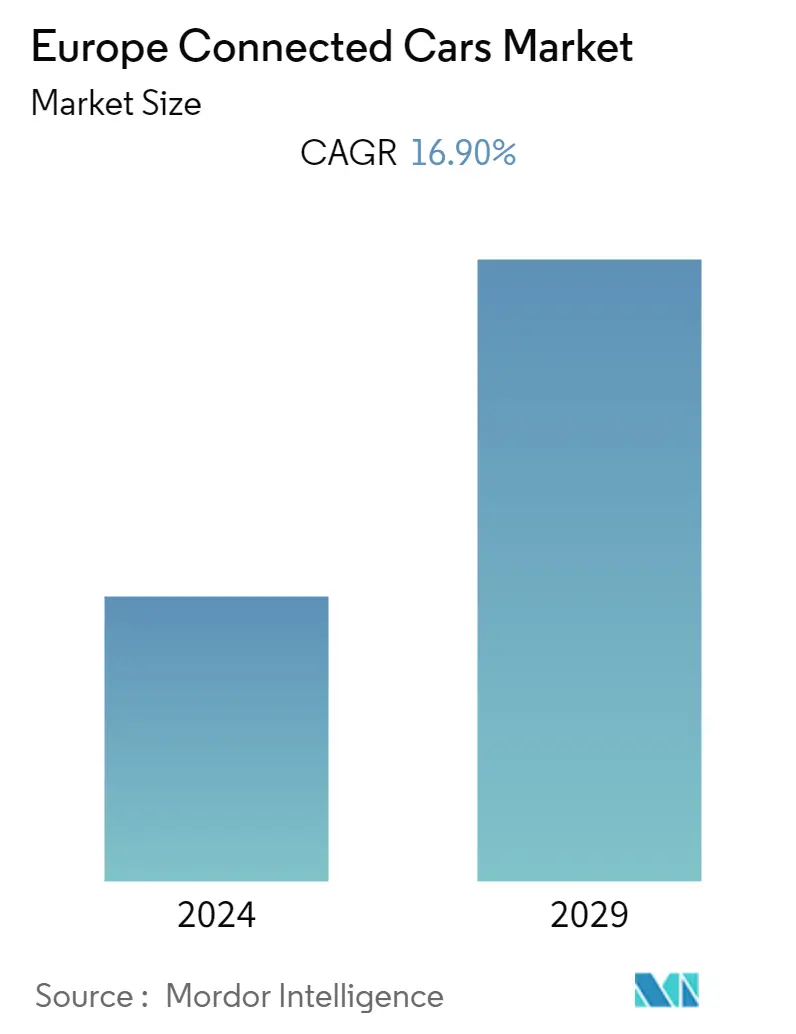

| CAGR | 16.90 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Connected Car Market Analysis

The Europe Connected Cars Market was valued at USD 10.63 billion in 2021 and shall surpass the net valuation of USD 26.95 billion by 2027 while registering a solid CAGR growth of 16.2% during the forecast period (2022-2027).

The COVID-19 pandemic had a partial impact on the European-connected cars market. Although the stringent lockdown and social distancing norms indirectly affected the market by reducing the number of vehicle sales registered in 2020, the technical research into implementing the connected car system was continued remotely. The pandemic has also forced people to prefer private transport, which is expected to raise car sales worldwide, and, consequently, the connected cars market.

Over the medium-term, as European Union has framed several regulatory frameworks and ambitious goals to boost connected car networks, such favorable policies will positively impact the market. In April 2022, Data Act prosed by the EU offers a set of principles required for accessing data from connected products. This includes the right to access and share data and contractual business-to-business data exchange rights. This technological dominance and government frameworks drive the demand for connected cars in the EU.

There is a growing demand for connected car devices as they help monitor vehicles and drivers by exchanging critical information between nearby infrastructure and vehicles. Europe is home to many of the largest automotive technology manufacturers. Through innovative platforms, IoT and telematics together have enhanced connectivity, communications, and responses that offer infotainment, safety, security, and increased vehicle management to drivers, passengers, and commuters.

European Union accounts for almost 30% of the globally connected car fleet. Europe is also known for its extensive technological OEMs, which work in domains such as in-car entertainment, navigation, and in-car connectivity (for example, through Bluetooth), which have evolved rapidly over the last decade.

Europe Connected Car Market Trends

This section covers the major market trends shaping the Europe Connected Cars Market according to our research experts:

Introduction of 5G Network and Increased Use of IoT Applications

The automotive industry is crucial to Europe's GDP. The automotive sector provides for 6.1% of total EU employment, and with the rising demand for high-performing cars, connected car makers may offer lucrative opportunities for European manufacturers.

The advent of 5G is the most crucial for the development of the connected car market during the forecast period. This technology allows car owners to effectively communicate with other cars on the road, creating an unprecedented level of collaboration, which is impossible for human drivers. The fifth-generation wireless technology is expected to connect almost everything around us with an ultra-fast, highly reliable, and fully responsive network. 5G will allow us to leverage the full potential of advanced technologies such as artificial intelligence, virtual reality, and the Internet of Things (IoT). Thus, companies are focusing on the utilization and development of 5G in cars to gain a competitive edge over other players in the market.

Increased availability of 5G networks across the region is expected to make it easier for connected cars to manage vehicle speeds along smart motor highways and the future data source for vehicle-to-vehicle communication that may aid collision avoidance systems. Several use cases of 5G network connectivity implemented in European cars indicate the growing demand for the connected cars market.

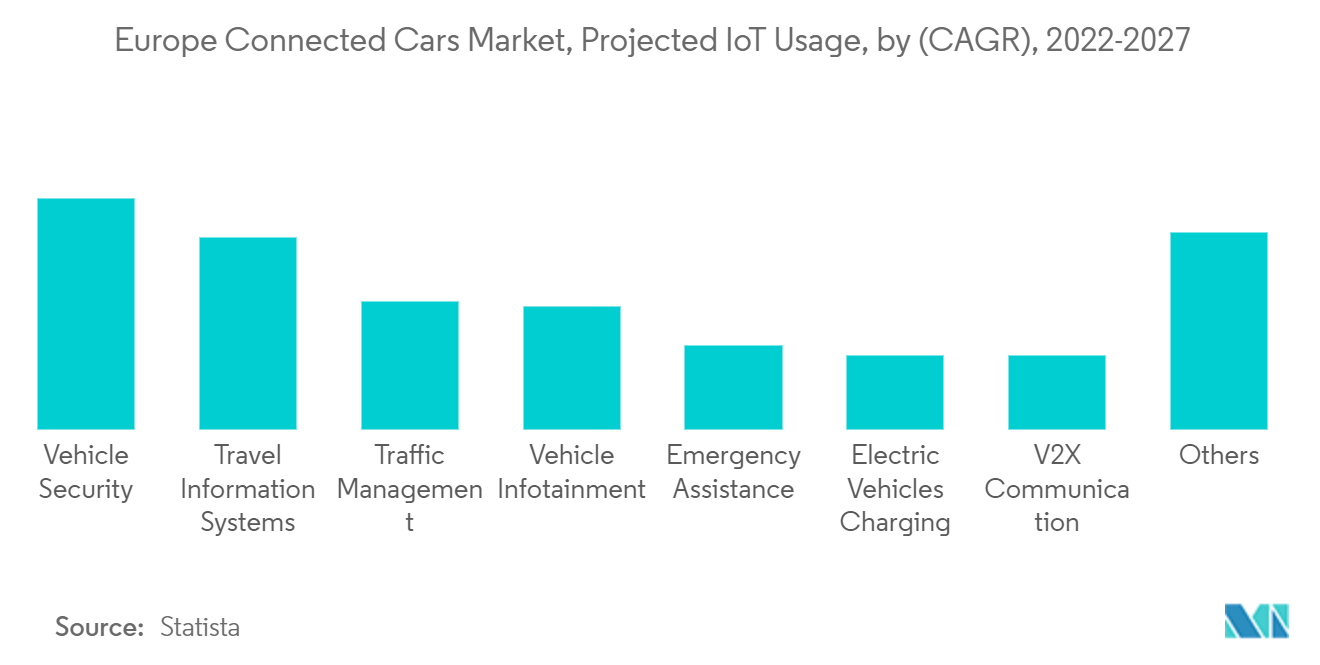

Internet of Things (IoT) has seen an exponential increase in usage in the region. The different aspects of vehicles needing IoT as a technology base for connected cars, autonomous driving, and vehicle security have risen. They are projected to increase in the coming years during the forecast period.

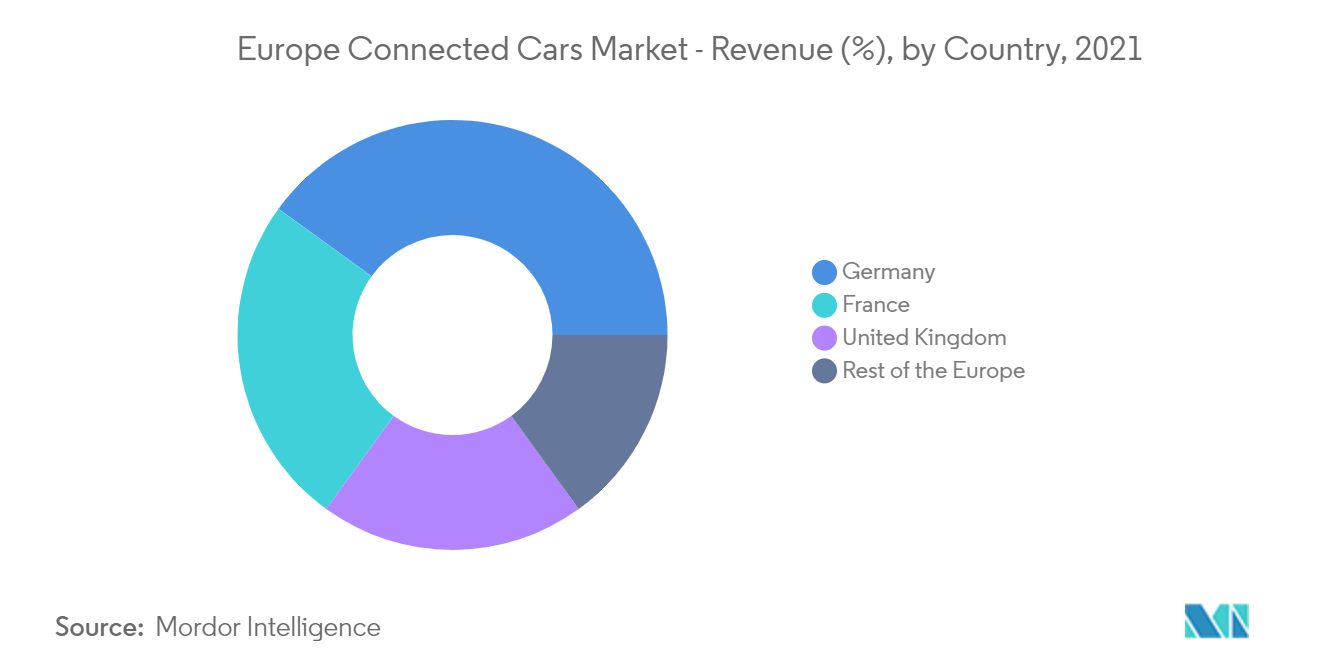

Germany to Remain Epi-Centre for Connected Car Market Growth

Among all the European Union nations, Germany showcased itself as the major bedrock for the rising demand for connected cars.

Various companies in the region are partnering with other industry players to develop new technologies for autonomous vehicles. Most of the autonomous vehicles' electric powertrains were being employed, which is good for countries to reach their emission targets.

New technologies, such as Artificial Intelligence and its subset, Machine Learning, Computer Vision, IoT, Cloud Technologies, Smart Robotics, and Mobility, are fostering innovation in the connected and autonomous car industry, supported by governments to boost connected car sales.

Several automakers in Germany are designing, testing, and manufacturing autonomous/driverless cars, which involves huge expenditure; hence companies are focusing on improving R&D by adopting various collaborations and agreements. This, in turn, has elevated the growth potential of the connected cars market in EU.

- In May 2022, Mercedes got a huge order for Level 3 self driving vehicles from its consumer base. These vehicles are equipped with the drive pilot mode, which shall enable the key features of connected cars and driverless cars.

Moreover, with ongoing research and development across all the automakers in Germany, the connected cars market is expected to witness major boost during the forecast period.

Europe Connected Car Industry Overview

The European connected cars market is moderately consolidated with players such as Continental AG, Denso Corporation, Robert Bosch GmbH, Autoliv, Harman International, and Delphi Automotive LLP. As the demand for connected systems is growing in the region, the connected-car manufacturers are trying to have the edge over their competitors by making joint ventures and partnerships and launching new products with advanced technology. For Instance:

- In May 2022, Harman and Amazon announced that there are working under a constructive alliance to develop secure and reliable connected vehicle solutions. The development of advanced software-defined vehicles shall help the several challenges faced by OEMs in terms of safety and reliability.

- In March 2022, Denso Corporation organized a software innovation program under its new mobility-centered society. The training program included ADAS vision sensor recognition technology and voluntary activities to train cloud computing engineers.

- In October 2021, GENIVI Alliance, a collaborative firm developing open standards and software for in-vehicle transmission systems, announced its organizational rebrand as Connected Vehicle Systems Alliance (COVESA). This new brand shall signify the company's emerging technical focus on connected vehicle systems, which includes in-vehicle, in-cloud, and on-edge services.

Players in the market are creating alliances with key services providers of 5G and IOT to develop more reliable integrated connected car services.

Europe Connected Car Market Leaders

-

Continental AG

-

Robert Bosch GmbH

-

Autoliv Inc.

-

Harman

-

Denso Corp.

*Disclaimer: Major Players sorted in no particular order

Europe Connected Car Market News

- In May 2022, Volkswagen Group and SEAT SA announced their strategic vision to mobilize EUR 10 billion for electrifying Europe. Under this plan, companies will construct battery plants to fast forward goals with the 62 national and international companies, benchmark firms, and Transformation programs for electric and connected vehicles.

- In February 2021, Robert Bosch announced a partnership with Microsoft to build, develop, and deploy a vehicle development platform to streamline the production of components required to produce connected vehicles by integrating Bosch's component technology with Microsoft's cloud services.

- In February 2021, Harman - a wholly-owned subsidiary of Samsung Electronics Co. Ltd, announced the acquisition of Savari Inc. in a strategic move to develop vehicle-to-everything (V2X) communication technology using a 5G network to be installed on automotive platforms and devices.

Europe Connected Car Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Drivers

4.2 Market Restraints

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Buyers/Consumers

4.3.2 Bargaining Power of Suppliers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size in Value USD Billion)

5.1 By Technology Type

5.1.1 Navigation

5.1.2 Entertainment

5.1.3 Safety

5.1.4 Vehicle Management

5.1.5 Other Technology Types

5.2 By Connectivity Type

5.2.1 Integrated

5.2.2 Embedded

5.2.3 Tethered

5.3 By Vehicle Connectivity Type

5.3.1 V2Vehicle

5.3.2 V2Infrastructure

5.3.3 V2X

5.4 By End-User Type

5.4.1 OEM

5.4.2 Aftermarket

5.5 By Country

5.5.1 Germany

5.5.2 France

5.5.3 United Kingdom

5.5.4 Rest of Europe

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles*

6.2.1 Continental AG

6.2.2 Denso Corporation

6.2.3 Robert Bosch GmbH

6.2.4 Autoliv Inc.

6.2.5 Harman International

6.2.6 Delphi Automotive LLP

6.2.7 Audi AG

6.2.8 BMW Group

6.2.9 Diamler AG

6.2.10 Verizon Communication

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Europe Connected Car Industry Segmentation

A connected car is a vehicle connected to the internet, in other words, WLAN ( Wireless local area network). This helps the vehicles to share car data with external devices/services. The market studies thus cover all the technological aspects and latest developments in the market.

The European connected cars market is segmented by technology type, Connectivity type, Vehicle connectivity type, end-user type, and country. By technology type, the market is segmented into navigation, entertainment, safety, vehicle management, and other technology types. By connectivity type, the market is segmented into integrated, embedded, and tethered. By vehicle connectivity type, the market is segmented into V2Vehicle, V2Infrastructure, and V2X.

By end-user type, the market is segmented into OEM and aftermarket; by country, the market is segmented into Germany, France, the United Kingdom, and the Rest of Europe. For each segment, market sizing and forecast have been done on the basis of value (USD billion).

| By Technology Type | |

| Navigation | |

| Entertainment | |

| Safety | |

| Vehicle Management | |

| Other Technology Types |

| By Connectivity Type | |

| Integrated | |

| Embedded | |

| Tethered |

| By Vehicle Connectivity Type | |

| V2Vehicle | |

| V2Infrastructure | |

| V2X |

| By End-User Type | |

| OEM | |

| Aftermarket |

| By Country | |

| Germany | |

| France | |

| United Kingdom | |

| Rest of Europe |

Europe Connected Car Market Research FAQs

What is the current Europe Connected Cars Market size?

The Europe Connected Cars Market is projected to register a CAGR of 16.90% during the forecast period (2024-2029)

Who are the key players in Europe Connected Cars Market?

Continental AG, Robert Bosch GmbH, Autoliv Inc., Harman and Denso Corp. are the major companies operating in the Europe Connected Cars Market.

What years does this Europe Connected Cars Market cover?

The report covers the Europe Connected Cars Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Europe Connected Cars Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Europe Connected Car Industry Report

Statistics for the 2024 Europe Connected Car market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Europe Connected Car analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.