Market Size of Europe Flight Training And Simulation Industry

| Study Period | 2019-2029 |

| Base Year For Estimation | 2023 |

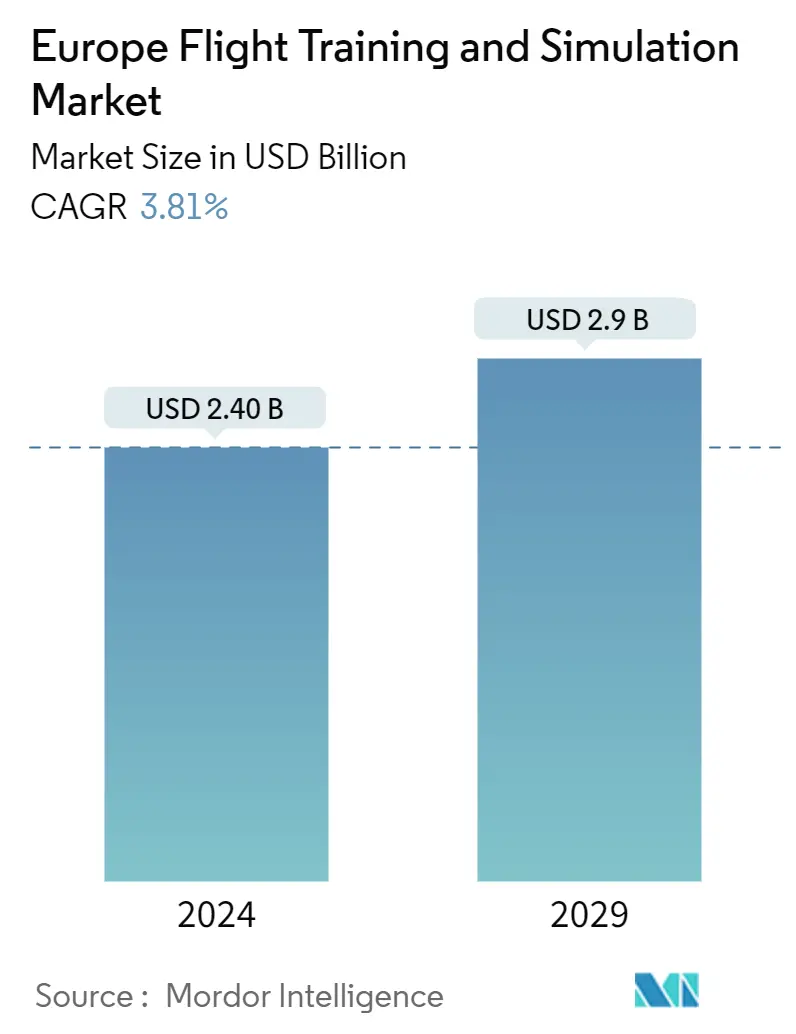

| Market Size (2024) | USD 2.40 Billion |

| Market Size (2029) | USD 2.9 Billion |

| CAGR (2024 - 2029) | 3.81 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Europe Flight Training and Simulation Market Analysis

The Europe Flight Training And Simulation Market size is estimated at USD 2.40 billion in 2024, and is expected to reach USD 2.9 billion by 2029, growing at a CAGR of 3.81% during the forecast period (2024-2029).

Increasing passenger traffic is encouraging airlines to procure new aircraft, which, in turn, is creating an acute pilot shortage. Thus, aviation training institutes in the region are modernizing their training capabilities via procuring new simulator equipment to train a larger batch of aviation aspirants per year while adhering to the certification criteria of the regulatory agencies.

Another driver for the market is the increasing demand for well-trained aviation pilots in Europe. As the aviation industry experiences continuous expansion and modernization, there is a growing demand for skilled pilots and crew members. Flight training and simulators play a critical role in providing realistic and immersive training experiences, enabling aspiring aviators to acquire the necessary skills in a safe and controlled environment.

Regulatory initiatives and standards set by aviation safety authorities also contribute to the market's growth. Compliance with stringent safety regulations necessitates standardized training programs, driving the adoption of advanced flight training and simulation systems. These systems enable training schools to align their programs with regulatory requirements, ensuring that pilots receive training that meets the highest safety standards.

Despite the demand, the adoption of flight simulators may be deterred by the inherently steep operational and maintenance costs that are multi-fold higher than the initial procurement price. Setting up a flight training institute requires a high initial investment in acquiring and maintaining advanced flight simulation systems. The cost of implementing state-of-the-art simulators can be restraining, particularly for smaller aviation training organizations and emerging players in the market.

Europe Flight Training and Simulation Industry Segmentation

Flight simulators artificially recreate the environment for pilot training purposes. They deliver the knowledge of flying and provide the pilot experience of reacting in emergencies. Aircraft flight simulators expose commercial aircraft and business jet pilots to real-time situations, such as bad weather, loss of electronics, incidents like tire blowouts on landing, and hydraulic failures.

The European flight training and simulation market is segmented by simulator type, training capability, and geography. By simulator type, the market has been segmented into full flight simulators (FFS) and flight training devices (FDS). By training capability, the market has been segmented into rotorcraft and fixed-wing. The report also offers the market size and forecasts for six countries across the region. For each segment, the market sizing and forecasts have been done based on value (USD).

| Simulator Type | |

| Full Flight Simulator (FFS) | |

| Flight Training Devices (FTD) |

| Training Capability | |

| Rotorcraft | |

| Fixed-Wing |

| Geography | |

| United Kingdom | |

| France | |

| Germany | |

| Poland | |

| Spain | |

| Italy | |

| Rest of Europe |

Europe Flight Training And Simulation Market Size Summary

The European flight training and simulation market is poised for steady growth, driven by the increasing demand for skilled aviation professionals amid rising passenger traffic and the subsequent need for new aircraft. This demand is prompting aviation training institutes to enhance their capabilities by investing in advanced simulator equipment, which allows for the training of larger cohorts of pilots while meeting stringent regulatory standards. The market is further bolstered by regulatory initiatives that mandate standardized training programs, ensuring that pilots receive training that adheres to the highest safety standards. Despite the high initial investment and maintenance costs associated with flight simulators, the market continues to expand, particularly in the fixed-wing segment, which dominates due to the growth in commercial aviation and the need for pilots trained on new aircraft models.

Germany stands out as a key player in the European flight training and simulation market, benefiting from its robust aerospace infrastructure and world-class training institutions. The country's proactive government support and strategic positioning as an aviation hub attract aspiring pilots and simulation technology companies, reinforcing its dominance in the sector. Major industry players like CAE Inc., L3Harris Technologies Inc., Thales, FlightSafety International Inc., and The Boeing Company hold significant market shares, contributing to the semi-consolidated nature of the market. Recent developments, such as the establishment of new training centers and the introduction of innovative training technologies, underscore the ongoing evolution and expansion of the market, with Germany's influence expected to grow as demand for skilled aviation professionals continues to rise.

Europe Flight Training And Simulation Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Simulator Type

-

2.1.1 Full Flight Simulator (FFS)

-

2.1.2 Flight Training Devices (FTD)

-

-

2.2 Training Capability

-

2.2.1 Rotorcraft

-

2.2.2 Fixed-Wing

-

-

2.3 Geography

-

2.3.1 United Kingdom

-

2.3.2 France

-

2.3.3 Germany

-

2.3.4 Poland

-

2.3.5 Spain

-

2.3.6 Italy

-

2.3.7 Rest of Europe

-

-

Europe Flight Training And Simulation Market Size FAQs

How big is the Europe Flight Training And Simulation Market?

The Europe Flight Training And Simulation Market size is expected to reach USD 2.40 billion in 2024 and grow at a CAGR of 3.81% to reach USD 2.9 billion by 2029.

What is the current Europe Flight Training And Simulation Market size?

In 2024, the Europe Flight Training And Simulation Market size is expected to reach USD 2.40 billion.