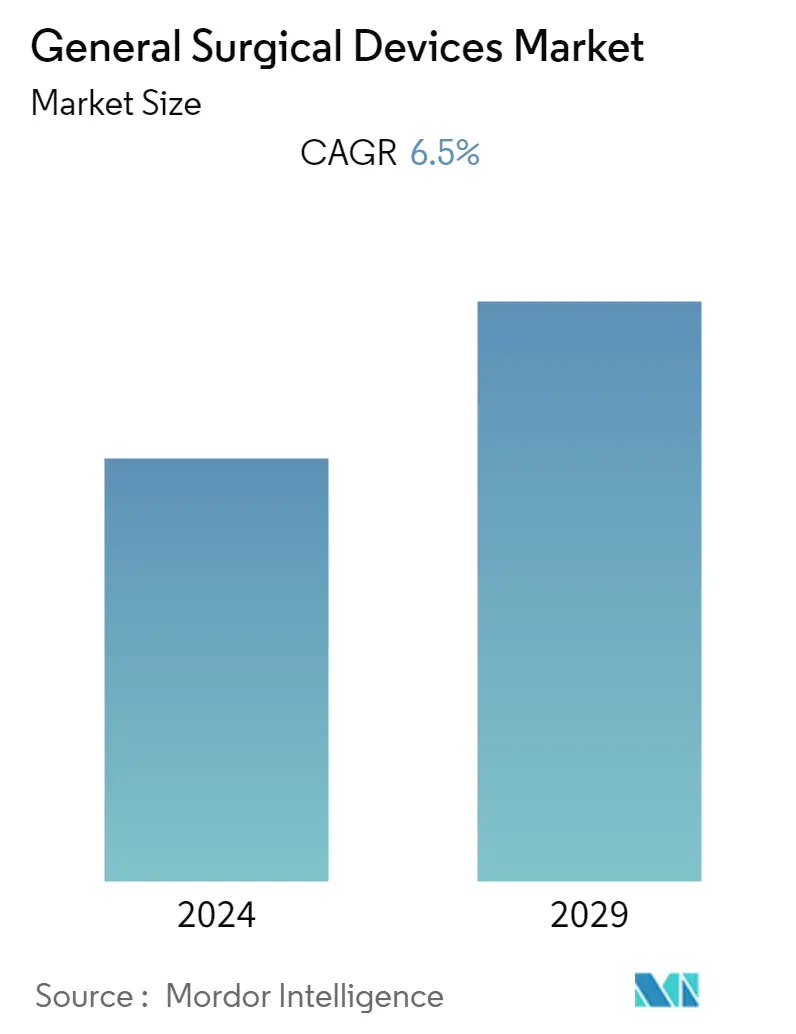

General Surgical Devices Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 6.50 % |

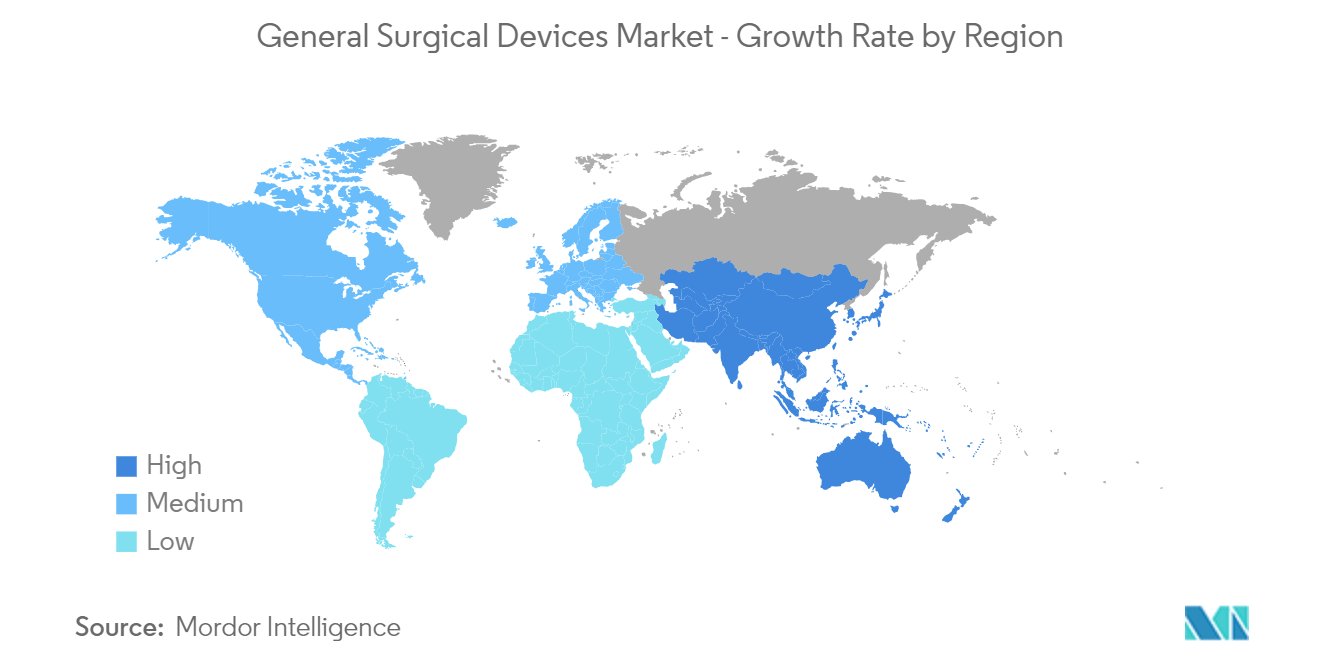

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

General Surgical Devices Market Analysis

The general surgical devices market is expected to register a CAGR of nearly 6.5% during the forecast period.

The pandemic significantly impacted the studied market since the volume of surgeries significantly declined during the pandemic, owing to the stringent guidelines by the regulatory authorities to avoid non-emergent surgeries. For instance, according to the article published in the NIH in October 2021, there was a 42.8% decline in general surgery admission across the globe. Thus, the general surgical devices market was significantly impacted by COVID-19. However, as the pandemic restrictions were eased, the market is expected to witness significant growth in the coming years due to the increase in the adoption of surgical procedures coupled with rapid technological advancements in general surgical devices.

The key factors propelling the market include the rising use of minimally invasive devices, rising chronic diseases, and increasing healthcare expenditure. Additionally, the increasing acceptance of MIS in different parts of the world is propelling the growth of the market. For instance, the Australian Institute of Health and Welfare report published in July 2022 reported that 60,393 Cholecystectomy procedures, 42,418 appendicectomy procedures, and 45,186 inguinal hernia repairs were performed in Australia during 2020-2021. Such a high proportion of the laparoscopic procedures performed are propelling the growth of the market.

In addition, traffic accidents are a major cause of injury that leads to surgical procedures across the globe. For instance, according to the Planning and Statistics Authority Qatar, the total number of major traffic accident cases were risen from 717 in January 2022 to 788 in January 2023. Thus, an increase in accident cases is expected to raise the demand for surgical procedures, contributing to the general surgical devices market growth over the forecast period.

Furthermore, the key players' increase in general surgical device launches and strategic partnerships are expected to augment the market growth over the forecast period. For instance, in September 2021, Olympus launched POWER SEAL advanced bipolar surgical energy devices to strengthen its surgical portfolio. Similarly, in May 2023, SSI Mantra achieved the significant milestone of 100 successful surgeries within six months of its commercial launch in India. Also, the SSI Mantra was first commercially installed at the Rajiv Gandhi Cancer Institute, New Delhi, in July 2022.

Thus, owing to the increase in surgery cases, rise in injuries, and strategic activities by the key players, the studied market is expected to witness significant growth over the forecast period. However, stringent regulatory frameworks and improper reimbursement for surgical devices are expected to hinder market growth.

General Surgical Devices Market Trends

Handheld Device is Expected to Witness a Significant Growth in the General Surgical Devices Market Over the Forecast Period

Hand-held surgical devices and equipment are nonpowered, hand-held, or hand-manipulated devices such as scalpels, forceps, and retractors intended to be used in various general surgical procedures. The development of advanced devices, like robotic handheld surgical devices for laparoscopic interventions, enhances a surgeon's skills. Many innovations have been made due to the need for high reliability, accuracy, and patient safety. Factors such as a rise in cesarean sections, increased product launches, and advancements in handheld surgical devices are expected to augment the segment's growth. For instance, according to the WHO June 2021 update, cesarean section use continues to rise globally, accounting for more than 1 in 5 (21%) childbirths in 2021. If this trend continues, by 2030, the highest rates are likely to be in Eastern Asia(63%), Latin America and the Caribbean (54%), Western Asia (50%), Northern Africa (48%), Southern Europe (47%) and Australia and New Zealand (45%). Moreover, several countries are also experiencing a rise in surgical procedures owing to the rising burden of non-communicable diseases and injuries.

Moreover, the key player focused on strategic partnerships, mergers, and acquisitions to launch innovative and technologically advanced products to fuel the market demand. For instance, in November 2021, Orthalign launched Lantern, the latest handheld innovative tool for knee replacement surgery. Similarly, in November 2021, Smith & Nephew expanded its Cori handheld robotic system to Europe, Australia, New Zealand, India, and Canada. The CORI surgical system is an advanced handheld robotics-assisted platform for total and uni-compartmental knee arthroplasty. The solution is ideal for outpatient surgery and ambulatory surgical centers (ASCs).

Thus, owing to the rise in surgical procedures and the strategic launch of advanced handheld devices, the studied segment is expected to grow significantly over the forecast period.

North America is Expected to Witness a Healthy Growth Over the Forecast Period

North America is expected to hold a notable market share in the studied market throughout the forecast period due to the rise in the adoption of minimally invasive surgical procedures and established healthcare systems coupled with the presence of key players. Further, the increase in injuries due to sports activities and road accidents also bolsters the demand for general surgical devices in North America. For instance, according to the National Safety Council (NSC), in July 2021, 526,000 injuries were reported due to personal exercise, 500,000 players were injured due to basketball, 457000 to bicycling, and 341,000 to football. NSC also reported that 199,000 swimming injuries were treated in the emergency room. Spine, shoulder, head, and knee injuries accounted for more than 50% of these injuries.

Similarly, an increase in surgery cases in Canada is likely to bolster the general surgery devices market over the forecast period. For instance, according to the June 2022 update by Canadian Institute for Health Information, among the approximately 110,000 joint replacements performed in 2020-2021, more than 7,300 were performed as day surgery, representing a four-fold increase from the previous year. Hence, an increase in surgical procedures leads to a rise in the adoption of general surgical devices, thereby driving the market growth.

Besides, key activities by the market players, such as mergers and acquisitions, partnerships, and product launches, help propel the region's market growth. For instance, in November 2022, Olympus launched the moresolution Power Morcellator, manufactured by TROKAMED GmbH and available in the U.S. through a distribution agreement with Olympus America, Inc. The moresolution Morcellator is designed for advanced gynecologic procedures with large, calcified tissue specimens. Similarly, in June 2022, Xenco Medical expanded its ASC surgical device portfolio through the FDA clearance and launch of its Multilevel CerviKit.

Thus, owing to the increase in sports injuries the rise in surgical procedures, and strategic activities by the key players, North America is expected to witness significant growth over the forecast period.

General Surgical Devices Industry Overview

The general surgical devices market is highly fragmented and focused because of the presence of many large, medium, and small players. Some of the major players in the market are B. Braun SE, Boston Scientific Corporation, Cadence Inc., Conmed Corporation, and Johnson & Johnson, among others.

General Surgical Devices Market Leaders

-

Boston Scientific Corporation

-

Cadence Inc.

-

Conmed Corporation

-

Johnson & Johnson

-

B. Braun SE

*Disclaimer: Major Players sorted in no particular order

General Surgical Devices Market News

- February 2023: OSSIO, Inc., an orthopaedic fixation technology company, introduced the new OSSIOfiber Compression Staple, the next step towards becoming the gold standard in orthopaedic fixation. OSSIOfiber Compression Staples offers stronger, bio-integrative compression to surgeons during orthopaedic surgery.

- January 2023: Organon, a global women's healthcare company, invested in Claria Medical, Inc., a privately-held company developing an investigational medical device being studied during minimally invasive laparoscopic hysterectomy. The agreement also grants Organon the option to acquire Claria Medical. Claria's initial investigational device, the Claria System, uses an intelligent uterine containment and extraction system to improve the hysterectomy procedure for patients and physicians.

General Surgical Devices Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Demand for Minimally Invasive Devices

4.2.2 Growing Cases of Injuries and Accidents

4.2.3 Increasing Healthcare Expenditures in Emerging Economies

4.3 Market Restraints

4.3.1 Stringent Government Regulations and Improper Reimbursement for Surgical Devices

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Product

5.1.1 Handheld Devices

5.1.2 Laproscopic Devices

5.1.3 Electro Surgical Devices

5.1.4 Wound Closure Devices

5.1.5 Trocars and Access Devices

5.1.6 Other Products

5.2 By Application

5.2.1 Gynecology and Urology

5.2.2 Cardiology

5.2.3 Orthopaedic

5.2.4 Neurology

5.2.5 Other Applications

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 B. Braun SE

6.1.2 Boston Scientific Corporation

6.1.3 Cadence Inc.

6.1.4 Conmed Corporation

6.1.5 Integer Holdings Corporation

6.1.6 Johnson & Johnson

6.1.7 Getinge (Maquet Holding BV & Co. KG)

6.1.8 Medtronic

6.1.9 Olympus Corporations

6.1.10 Stryker Corporation

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

General Surgical Devices Industry Segmentation

As per the scope of the report, general surgical devices are cutting instruments for creating incisions or removing tissue. Surgical instruments allow surgeons to open the soft tissue, remove the bone, dissect and isolate the lesion, and remove or obliterate the abnormal structures as a treatment. The general surgical devices market is segmented by product (handheld devices, laparoscopic devices, electro-surgical devices, wound closure devices, trocars, access devices, and other products), application (gynecology and urology, cardiology, orthopedic, neurology, other applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| By Product | |

| Handheld Devices | |

| Laproscopic Devices | |

| Electro Surgical Devices | |

| Wound Closure Devices | |

| Trocars and Access Devices | |

| Other Products |

| By Application | |

| Gynecology and Urology | |

| Cardiology | |

| Orthopaedic | |

| Neurology | |

| Other Applications |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

General Surgical Devices Market Research FAQs

What is the current General Surgical Devices Market size?

The General Surgical Devices Market is projected to register a CAGR of 6.5% during the forecast period (2024-2029)

Who are the key players in General Surgical Devices Market?

Boston Scientific Corporation, Cadence Inc., Conmed Corporation, Johnson & Johnson and B. Braun SE are the major companies operating in the General Surgical Devices Market.

Which is the fastest growing region in General Surgical Devices Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in General Surgical Devices Market?

In 2024, the North America accounts for the largest market share in General Surgical Devices Market.

What years does this General Surgical Devices Market cover?

The report covers the General Surgical Devices Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the General Surgical Devices Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

General Surgical Devices Industry Report

Statistics for the 2024 General Surgical Devices market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. General Surgical Devices analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.