Next Generation Advanced Battery Market Size

| Study Period | 2020 - 2029 |

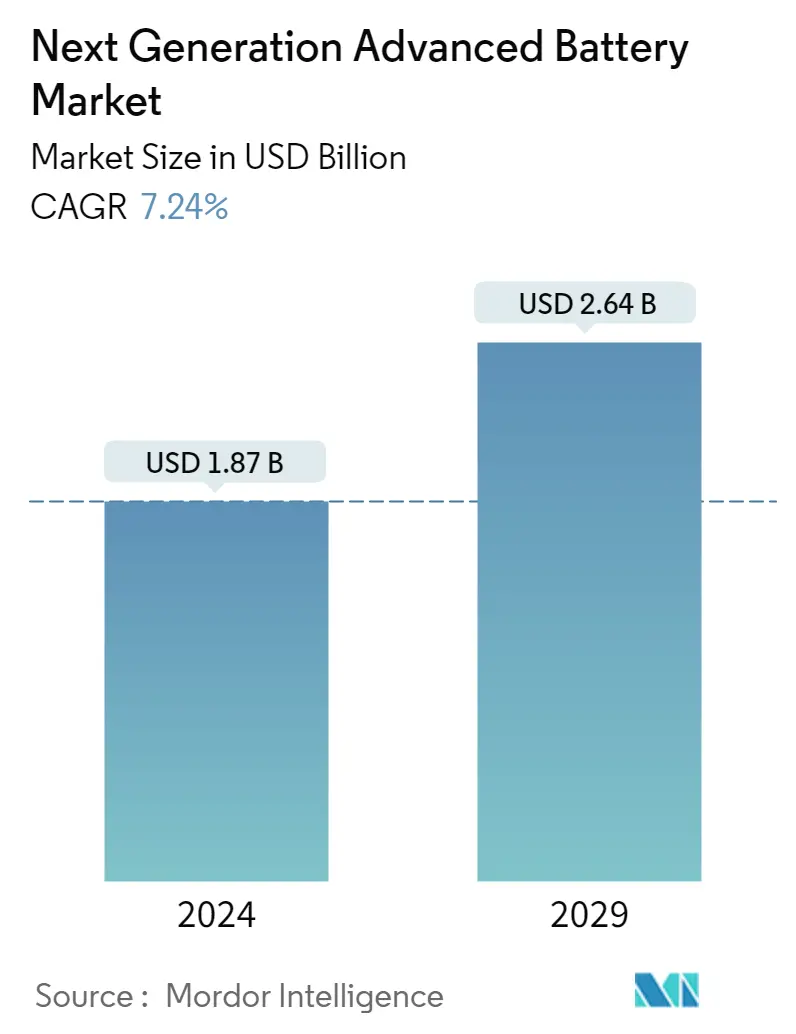

| Market Size (2024) | USD 1.87 Billion |

| Market Size (2029) | USD 2.64 Billion |

| CAGR (2024 - 2029) | 7.24 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Next Generation Advanced Battery Market Analysis

The Next Generation Advanced Battery Market size is estimated at USD 1.87 billion in 2024, and is expected to reach USD 2.64 billion by 2029, growing at a CAGR of 7.24% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

- Over the long term, the growing demand and increasing adoption of electric vehicles are expected to drive the growth of the market studied.

- On the other hand, high manufacturing and R&D costs are expected to hamper the growth of Next-Generation advanced batteries during the forecast period.

- Nevertheless, the development of manufacturing facilities for next-generation advanced batteries is likely to create lucrative growth opportunities for the Next-Generation advanced battery market in the forecast period.

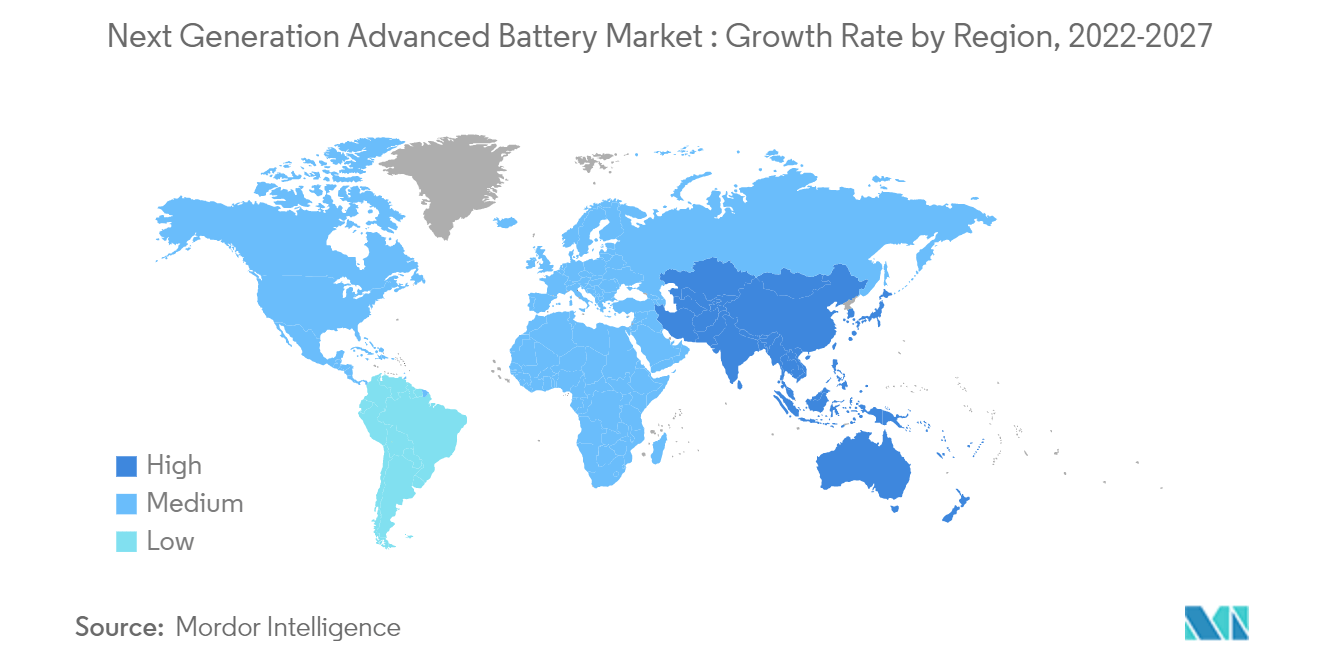

- Asia-Pacific region dominates the market and is also likely to witness the highest CAGR during the forecast period. This growth is attributed to the increasing investments, coupled with adoption of consumer electronics and electric vechiles in the countries of this region including India, China and Japan.

Next Generation Advanced Battery Market Trends

This section covers the major market trends shaping the Next Generation Advanced Battery Market according to our research experts:

Transportation Segment Expected to Dominate the Market

- The electrification of the transportation system is gaining popularity, and various government mandates have accelerated the adoption of electric vehicles, which directly aids the growth of next-generation advanced batteries in the transportation sector.

- In 2021, automobile giants announced that General Motors will stop selling petrol and diesel models by 2035, and Audi AG plans to stop producing such vehicles by 2033. The carmakers are rushing to electrify their electric cars, which has led the company to invest in advanced batteries for more efficient and profitable electric vehicles.

- In April 2022, Honda Motors announced that it would invest USD 39.84 billion in electrification and software technologies to accelerate its business globally for the next ten years. It will also build a demonstration production line for all-solid-state batteries in North America, allocating approximately USD 342.65 million. The investment company plans to launch two mid-to-large-scale electric vehicles (EV) models by 2024 with a partnership with General Motors.

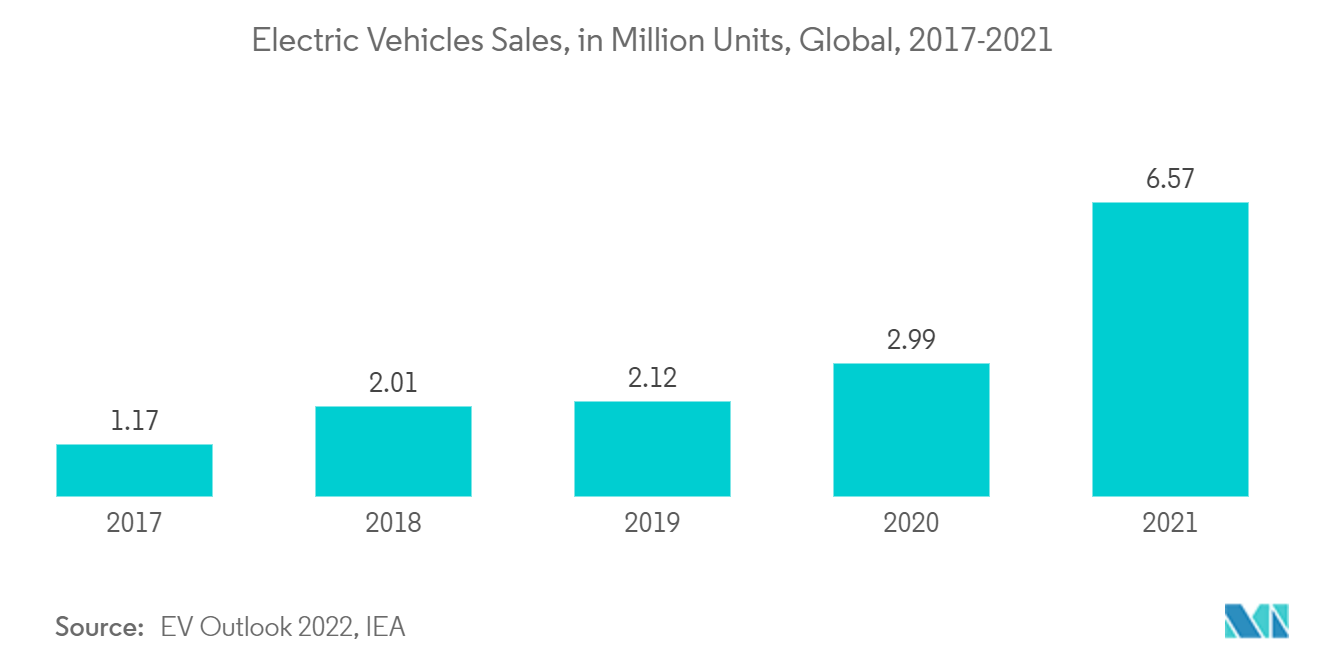

- According to the International Energy Agency (IEA), the global electric vehicle stock increased from 1.25 million in 2015 to about 10.2 million in 2020. In 2020, battery-electric vehicles accounted for most of the electric vehicles at about 6.85 million, and plug-in hybrid electric vehicles were about 3.35 million.

- Furthermore, aluminium-air batteries have an advantage over the conventional lithium-ion battery as the aluminium acts as a fuel where air reacts with the metal via an electrolyte to produce power. It has a travel range similar to gasoline-powered cars and a higher energy density than the lithium-ion battery. However, it lacks government policy support and attention from automakers to make it a popular battery energy storage system for electric vehicles.

- In December 2021, Mercedes Benz, a German car manufacturer, announced to invest of USD 100 million in a wide range of electric cars. The company also intends to integrate solid-state battery technology into a limited number of vehicles within the next five years. Mercedes Benz plans to invest tens of millions into Factorial Energy, a battery company to develop solid-state batteries.

- In April 2022, Nissan Motor Company planned to bring laminated solid-state batteries to the market by 2028, with the beginning of a prototype production facility. It is a part of Nissan's Ambition 2030 strategy, plus an investment of USD 17 billion for the four new electric vehicle concepts.

- Overall, automobile manufacturers are investing heavily in developing solid-state batteries and metal-air batteries, making automobiles one of the major sectors of the next-generation advanced battery market.

Asia-Pacific to Dominate the Market

- As of 2021, China, India, and Japan were the potential markets for the next generation advanced battery technology in the Asia-Pacific region.

- As of March 2022, China's battery energy storage capacity reached 3 GW, representing an increase of 76.5% compared to 1.7 GW in 2019. Furthermore, the Chinese Government is expected to increase its battery storage capacity to 100 GW by 2030. Such scenarios are creating vast opportunities for various next-generation advanced battery developers in the region.

- According to the China Energy Storage Alliance (CNESA), the refinement of policy related to grid ancillary services - energy storage's primary application - as well as policy developments in regions including Qinghai, Guangdong, Jiangsu, inner Mongolia, and Xinjiang, have created a wave of energy storage construction and development in China. Such government policies will likely boost the demand for advanced battery technologies during the forecast period.

- At present, various development projects and investments in the next generation advanced battery technologies are happening in China. In July 2021, CATL unveiled the first next-generation sodium-ion battery and its AB battery pack solutions. Also, CATL's quest to shift the electric vehicle market toward a sodium-ion cell received a boost from the central government after the Ministry of Industry and Information Technology announced the creation of standards for such battery types.

- In addition to the scenario in China, in January 2022, Japan's National Institute for Material Science (NIMS) and the Softbank Corp. developed a lithium-air battery with an energy density of over 500Wh/kg-significantly higher than currently lithium-ion batteries. The research team confirmed that this battery could be charged and discharged at room temperature. The battery developed by the team shows the highest energy densities and best cycle life performances. These results signify a major step toward the practical use of lithium-air batteries.

- The lithium-air batteries are expected to have the potential to be the ultimate rechargeable batteries: they are lightweight and high capacity, with theoretical energy densities several times that of currently available lithium-ion batteries. Because of these potential advantages, they may use various technologies, such as drones, electric vehicles, and household electricity storage systems.

- Further, "Make in India" is a high-priority movement for India and has already provided incentives to produce electric cars. Batteries for cars and grid storage are high on the agenda for manufacturing in India. The EV market for two-wheelers, three-wheelers, cars, and minibusses is more price-sensitive than performance sensitive. If the next generation advanced batteries have a price advantage over a comparable lithium-ion battery whose performance parameters are marginally higher, it would still find a better market opportunity in India than elsewhere. The advanced batteries made with economies of scale have huge market potential in India.

- In March 2022, India approved bids for four companies to avail incentives under the PLI Scheme for the Advanced Chemistry Cell (ACC) Battery Storage Manufacturing. Reliance New Energy Solar Limited, Ola Electric Mobility Private Limited, Hyundai Global Motors Company Limited, and Rajesh Exports Limited received incentives under India's INR 181 billion program to boost local battery cell production. Under the scheme, selected ACC battery storage manufacturers were expected to set up a production facility within two years. Such government-supportive incentives are expected to create an environment for the future development of the next generation advanced battery market.

- Therefore, the above-mentioned factors are expected to drive the next-generation advanced battery market in the Asia-Pacific region during the forecast period.

Next Generation Advanced Battery Industry Overview

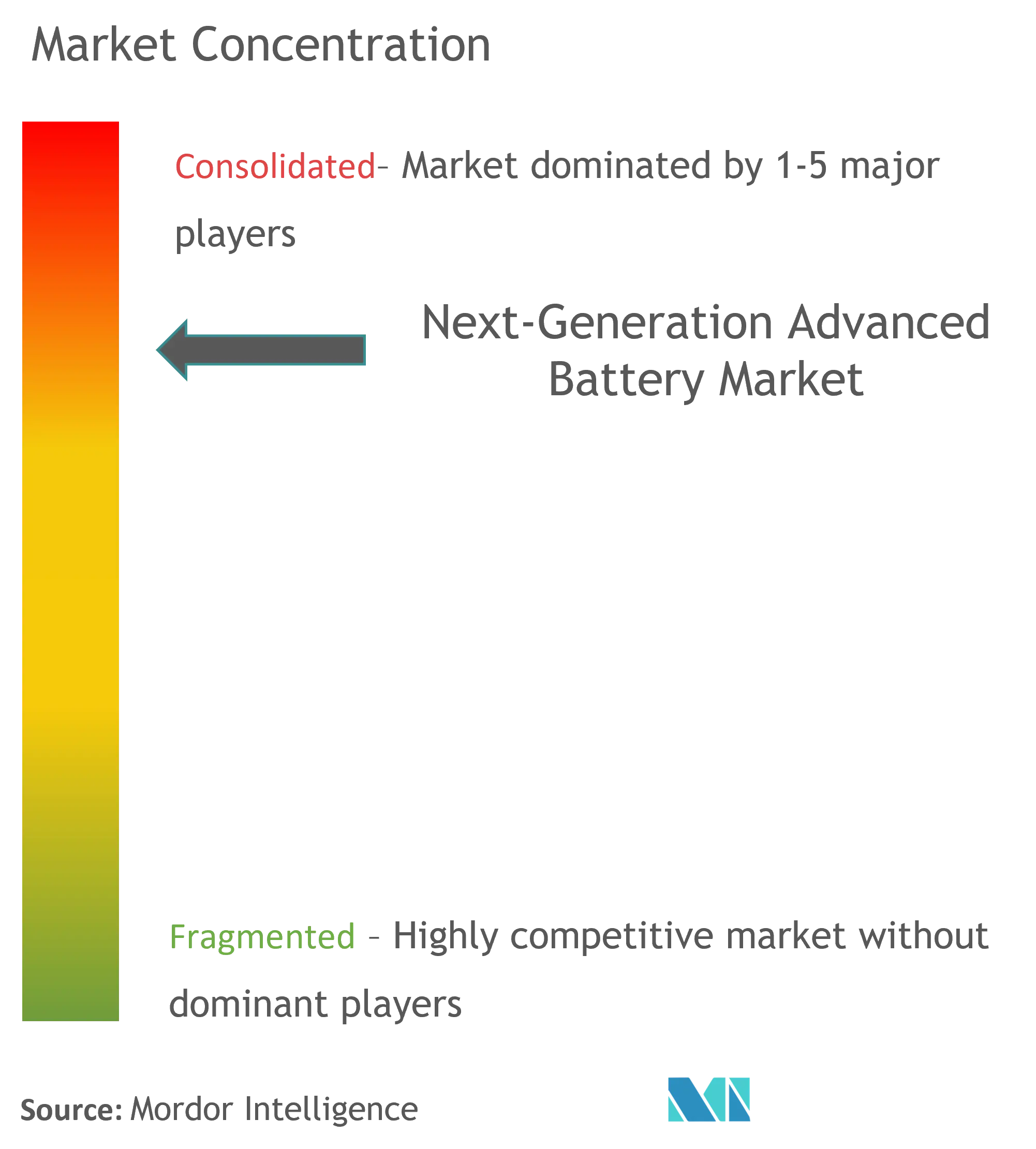

The next-generation advanced battery market is moderately consolidated in nature. Some of the major players in the market (in no particular order) include Sion Power Corporation, Contemporary Amperex Technology Co. Ltd, PolyPlus Battery Co. Inc., GS Yuasa Corporation, and Saft Groupe SA.

Next Generation Advanced Battery Market Leaders

-

Contemporary Amperex Technology Co Ltd

-

PolyPlus Battery Co Inc.

-

GS Yuasa Corporation

-

Ilika PLC

-

Johnson Matthey PLC

*Disclaimer: Major Players sorted in no particular order

Next Generation Advanced Battery Market News

- In February 2022, the US Department of Energy announced that it would provide USD 2.91 billion to boost the production of advanced batteries used in stationary energy storage systems and electric vehicles, as directed by the Bipartisan Infrastructure Law.

- In January 2022, Mercedes-Benz and ProLogium signed a technology cooperation agreement to develop next-generation battery cells. Mercedes Benz plans to go all-electric by 2030. With its solid-state battery R&D and manufacturing know-how, ProLogium is likely to be a strong partner for Mercedes Benz.

Next Generation Advanced Battery Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2027

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.2 Restraints

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Technology

5.1.1 Solid Electrolyte Battery

5.1.2 Magnesium Ion Battery

5.1.3 Next-generation Flow Battery

5.1.4 Metal-Air Battery

5.1.5 Lithium-Sulfur Battery

5.1.6 Other Technologies

5.2 End User

5.2.1 Consumer Electronics

5.2.2 Transportation

5.2.3 Industrial

5.2.4 Energy Storage

5.2.5 Other End Users

5.3 Geography

5.3.1 North America

5.3.2 Asia-Pacific

5.3.3 Europe

5.3.4 South America

5.3.5 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Pathion Holding Inc.

6.3.2 GS Yuasa Corporation

6.3.3 Johnson Matthey PLC

6.3.4 PolyPlus Battery Co. Inc.

6.3.5 Ilika PLC

6.3.6 Sion Power Corporation

6.3.7 LG Chem Ltd

6.3.8 Saft Groupe SA

6.3.9 Contemporary Amperex Technology Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Next Generation Advanced Battery Industry Segmentation

The advanced next-generation batteries are the upgraded version of existing batteries that have higher efficiency and cheaper unit cost. The Next-Generation advanced battery market is segmented by technology, end user, and geography. By technology, the market is segmented into solid electrolyte battery, magnesium ion battery, next-generation flow battery, metal-air battery, lithium-sulfur batteries, and other technologies. By end user, the market is segmented into consumer electronics, transportation, industrial, energy storage, other end users. The report also covers the market size and forecasts for the solar PV inverters market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| Technology | |

| Solid Electrolyte Battery | |

| Magnesium Ion Battery | |

| Next-generation Flow Battery | |

| Metal-Air Battery | |

| Lithium-Sulfur Battery | |

| Other Technologies |

| End User | |

| Consumer Electronics | |

| Transportation | |

| Industrial | |

| Energy Storage | |

| Other End Users |

| Geography | |

| North America | |

| Asia-Pacific | |

| Europe | |

| South America | |

| Middle-East and Africa |

Next Generation Advanced Battery Market Research FAQs

How big is the Next Generation Advanced Battery Market?

The Next Generation Advanced Battery Market size is expected to reach USD 1.87 billion in 2024 and grow at a CAGR of 7.24% to reach USD 2.64 billion by 2029.

What is the current Next Generation Advanced Battery Market size?

In 2024, the Next Generation Advanced Battery Market size is expected to reach USD 1.87 billion.

Who are the key players in Next Generation Advanced Battery Market?

Contemporary Amperex Technology Co Ltd, PolyPlus Battery Co Inc., GS Yuasa Corporation, Ilika PLC and Johnson Matthey PLC are the major companies operating in the Next Generation Advanced Battery Market.

Which is the fastest growing region in Next Generation Advanced Battery Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Next Generation Advanced Battery Market?

In 2024, the Asia-Pacific accounts for the largest market share in Next Generation Advanced Battery Market.

What years does this Next Generation Advanced Battery Market cover, and what was the market size in 2023?

In 2023, the Next Generation Advanced Battery Market size was estimated at USD 1.74 billion. The report covers the Next Generation Advanced Battery Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Next Generation Advanced Battery Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Next Generation Advanced Battery Industry Report

Statistics for the 2024 Next Generation Advanced Battery market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Next Generation Advanced Battery analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.