Green Logistics Market Size

| Study Period | 2020 - 2029 |

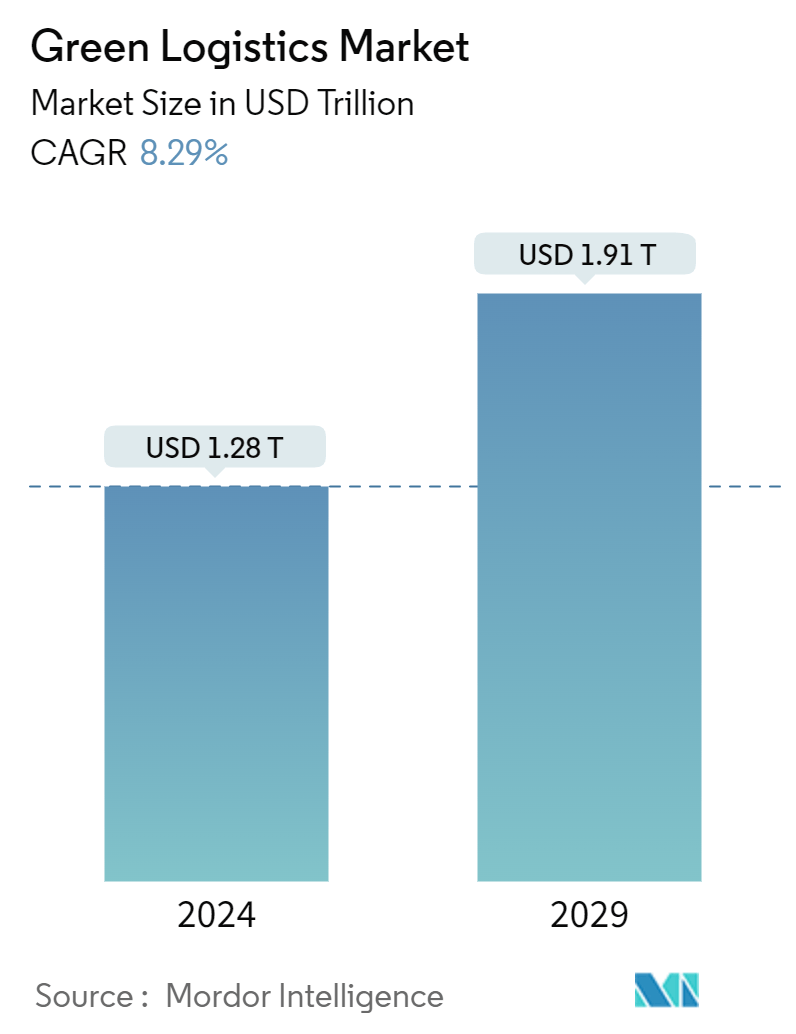

| Market Size (2024) | USD 1.28 Trillion |

| Market Size (2029) | USD 1.91 Trillion |

| CAGR (2024 - 2029) | 8.29 % |

| Largest Market | Asia Pacific |

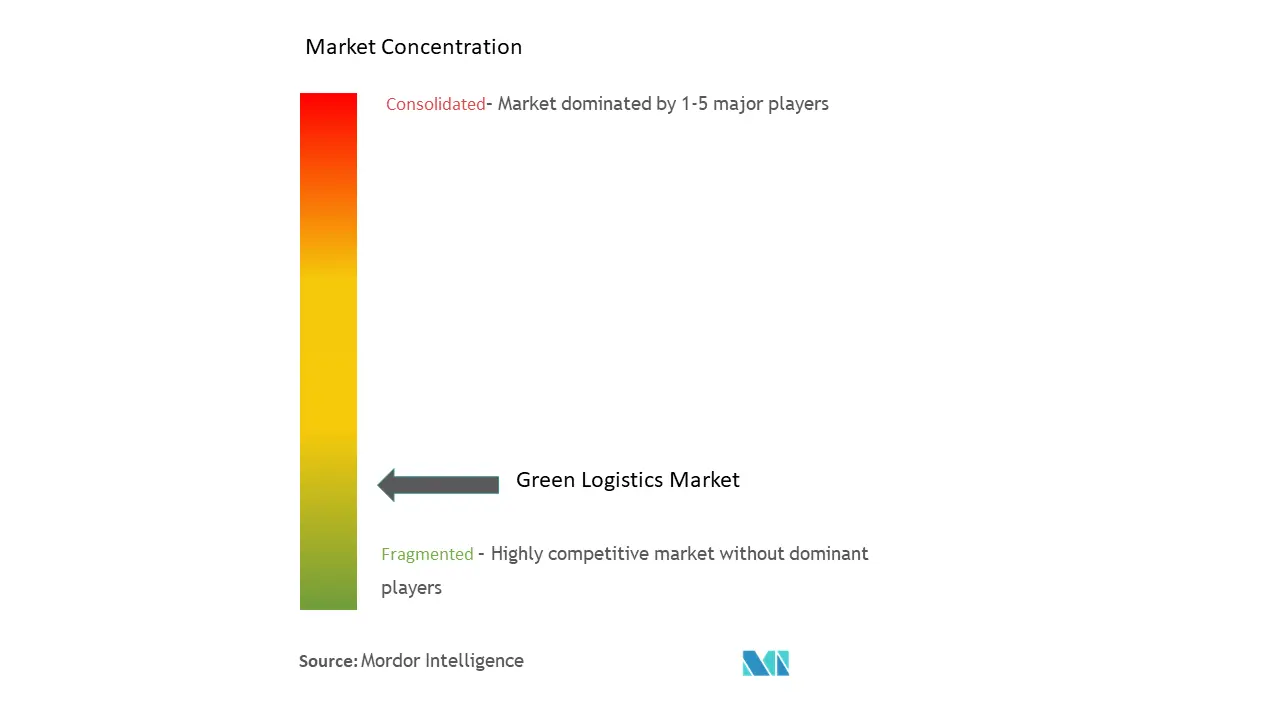

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Green Logistics Market Analysis

The Green Logistics Market size is estimated at USD 1.28 trillion in 2024, and is expected to reach USD 1.91 trillion by 2029, growing at a CAGR of 8.29% during the forecast period (2024-2029).

The growth of the green logistics market is stimulated by factors such as increased corporate social responsibility (CSR) activities undertaken by logistics undertakings, growing EV adoption in the transport sector, rising environmental legislation, and increasing use of artificial intelligence in the global supply chain.

Alternative fuels, such as hybrid electric and biodiesel vehicles, are increasingly used by companies like UPS, DHL, or FedEx. Efficient storage and packaging help reduce the amount of materials used and single-use plastic containers. Reusable containers, which help to reduce waste and costs related to packaging disposal, are a further strategy.

Businesses are increasingly switching to electric vehicles to meet these evolving delivery needs. EV fleets have lower operating costs and less disruption than gas or diesel vehicles, at half the price of electricity per mile and no need for repairs or oil changes.

In 2022, almost 66,000 electrical buses and 60,000 medium and heavier trucks were sold worldwide, about 4.5% of all buses and 1.2 % of truck sales.

To address environmental challenges, China, as the largest economy in the Asia Pacific region, is actively promoting green logistics practices. Investments in electric vehicles, clean energy sources, and intelligent transport systems have been made in the country. Japan, which has been known to embrace green technologies, particularly hybrids and electric vehicles, is now seeing the adoption of sustainable fuels by logistics companies.

In 2022, China sold 54,000 new EV buses and is expected to sell approximately 52,000 M&H trucks, accounting for 18% or 4% of all sales in the country and around 85 % worldwide. Moreover, many buses and trucks are made by China's brands in Latin America, North America, and Europe.

For example, Yusen Logistics Co. Ltd launched a new service in April 2023 called "Yuksen Book & Claim," which uses sustainable aviation fuel and enables its customers to grow sustainably using air freight forwarding.

Green Logistics Market Trends

The Demand for Green Warehouses is Rising

Several critical factors, like the emergence of multi-channel distribution networks, a growing focus on green initiatives, and sustainability to reduce waste in logistics operations, are driving the development of intelligent warehousing markets.

In the face of a worldwide climate crisis, continuing with existing warehouse practices that increase energy consumption and waste generation is impossible. Sustainable storage is emerging as a beacon of hope in the fight against these challenges. Sustainable warehousing offers an innovative approach that benefits enterprises and the environment by emphasizing the effective use of resources, reducing carbon emissions, and promoting renewables.

To achieve international visibility between 3PL and 4PL service providers, building warehouses that meet recognized global standards such as BREEAM and LEED is essential. The growth trend is expected to continue, with demand to increase by 16.6% to reach 61.5 million sq. ft and the supply correspondingly rising to 61.9 million sq. ft by 2026, which will be an increase of 15.8% from the 2023 estimated numbers.

In August 2023, Infor announced that Zofri will implement the Infor WMS warehouse management system to improve customer service, one of the most critical performance indicators in the supply chain. The Infor WMS solution will be deployed in the cloud, powered by AWS (Amazon Web Services), and implemented by Cerca Technology, Infor's partner in Latin America.

In May 2023, Manhattan Associates announced its re-imagined Manhattan Active Yard Management solution to expand its vision of a unified supply chain. By redesigning yard management to work seamlessly with its industry-leading warehouse and transportation management solutions on a single cloud-native platform, Manhattan is completing the digital unification of distribution and logistics, where they come together in the physical world.

Asia-Pacific dominates the market

The region's market is growing as emerging economies such as India adjust to the Fourth Industrial Revolution and adopt new digital technologies.

In addition, India focuses on improving logistics infrastructure and promoting electric vehicles in the sector. For example, in January 2023, as part of its global transition to carbon-free operations by 2040, FedEx Express increased its fleet by installing 30 Ace TATA electric vehicles in India. In the area of Green Logistics, South Korea has also been making progress with implementing initiatives to reduce emissions and improve logistics effectiveness.

Asia Pacific is further investing in projects in the green supply market. For instance, India is committed to reducing its emissions intensity by 45% by 2030 and achieving net zero emissions by 2070. To ensure that the green logistics sector reduces its environmental impact and embraces green mobility, this commitment is supported by a capital investment of USD 4,200 million (INR 35,000 crore) for energy transition.

Other countries such as Australia, Singapore, and New Zealand are progressively adopting sustainable logistics practices in Asia-Pacific. To reduce their carbon footprint, freight companies in Singapore have adopted electric vehicles and several renewable solutions. Ninja Van Singapore has introduced initiatives like an EV test pilot program or relaunching eco-friendly versions of its products to minimize the environmental impact and contribute to a sustainable logistics sector.

Green Logistics Industry Overview

The Green Logistics market is relatively fragmented, with large global players and small and medium-sized local players, with quite a few players occupying the market share. Governments and regulators worldwide adopt stringent environmental regulations and policies, which have been significant drivers of the green transport market. Different aspects of logistics operations, such as emission control, waste management, energy efficiency, and sustainability, are provided for in these Regulations.

On the other hand, there is a remarkable growth opportunity for market players operating on the market due to growing environmental awareness in end-use sectors, increasing demand for intelligent green warehouses, and increased development of lidar drones for last-mile delivery and warehouse. Significant players include United Parcel Service, AI Futtaim Logistics, Bollore Logistics, Yusen Logistics Co. Ltd, and DHL International GmbH.

Green Logistics Market Leaders

-

United Parcel Service

-

AI Futtaim Logistics

-

Bollore Logistics

-

Yusen Logistics Co., Ltd

-

DHL International GmbH

*Disclaimer: Major Players sorted in no particular order

Green Logistics Market News

• June 2023: DHL Global Forwarding, the division of Deutsche Post AG specializing in air and ocean freight, formed a strategic partnership with IAG Cargo in the Sustainable Aviation Fuel (SAF) field. As part of this collaboration, DHL has entered into a contract to acquire 11.5 million liters of SAF, contributing to reducing transport emissions categorized under Scope 3 in 2023.

• May 2023: Bolloré Logistics, a subsidiary of Bollore SE, extended its fleet in India with a commercial electric vehicle. It is ideal for last-mile deliveries due to its high mobility and low carbon impact.

• April 2023: DHL, a Deutsche Post DHL Group subsidiary, launched a new tool to assist clients in reducing their carbon impact. The DHL GoGreen Dashboard is an emission-tracking solution for large, wide customers, providing transparency in line with established industry standards such as the Global Logistics Emissions Council (GLEC) Framework.

Green Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Growing adoption of EVs in the logistics industry

4.2.2 Increase in adoption of artificial intelligence (AI) in the global logistics industry

4.3 Market Restraints

4.3.1 Dependency on fossil fuels, majority for transportation

4.3.2 The high costs of implementing green procurement practices discourage potential investors

4.4 Market Opportunity

4.4.1 Increased environmental consciousness among end-use industries

4.4.2 Rise in development of lidar drones for last mile delivery and warehouses

4.5 Value Chain / Supply Chain Analysis

4.6 Porter's Five Force Analysis

4.6.1 Threat of New Entrants

4.6.2 Bargaining Power of Buyers/Consumers

4.6.3 Bargaining Power of Suppliers

4.6.4 Threat of Substitute Products

4.6.5 Intensity of Competitive Rivalry

4.7 Impact of Covid-19 on the Market

5. MARKET SEGMENTATION

5.1 By End User

5.1.1 Healthcare

5.1.2 Manufacturing

5.1.3 Automotive

5.1.4 Banking and Financial services

5.1.5 Retail and E-commerce

5.1.6 Others

5.2 By Business Type

5.2.1 Warehousing

5.2.2 Distribution

5.2.3 Value-Added Services

5.3 By Mode of Operation

5.3.1 Storage

5.3.2 Roadways Distribution

5.3.3 Seaways Distribution

5.3.4 Others

5.4 Geography

5.4.1 North America

5.4.1.1 US

5.4.1.2 Canada

5.4.1.3 Mexico

5.4.2 Europe

5.4.2.1 Germany

5.4.2.2 UK

5.4.2.3 France

5.4.2.4 Russia

5.4.2.5 Spain

5.4.2.6 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 India

5.4.3.2 China

5.4.3.3 Japan

5.4.3.4 South Korea

5.4.3.5 Rest of Asia Pacific

5.4.4 LAMEA

5.4.4.1 Latin America

5.4.4.2 Middle East

5.4.4.3 Africa

6. COMPETITIVE LANDSCAPE

6.1 Market Concentration Overview

6.2 Company Profiles

6.2.1 United Parcel Service

6.2.2 AI Futtaim Logistics

6.2.3 Bollore Logistics

6.2.4 Bowling Green Logistics

6.2.5 GEODIS

6.2.6 Yusen Logistics Co., Ltd

6.2.7 DHL International GmbH

6.2.8 Mahindra Logistics Ltd

6.2.9 XPO Logistics

6.2.10 Agility Public Warehousing Company K.S.C.P.

6.2.11 CEVA Logistics*

- *List Not Exhaustive

6.3 Other Companies

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. APPENDIX

Green Logistics Industry Segmentation

Green logistics refers to applying sustainable practices within supply chain management to reduce the negative environmental impact of logistics activities. It incorporates eco-friendly transport solutions, optimized route planning, energy-efficient warehousing, and waste management techniques.

A complete background analysis of the green logistics market, which includes an assessment of the sector and the contribution of the industry to the economy, market overview, market size estimation for critical segments, key regions, and emerging trends in the market segments, market dynamics, and essential production and consumption statistics are covered in the report.

The green logistics market is segmented by end-user (healthcare, manufacturing, automotive, banking and financial services, retail and e-commerce, and others), by business type (warehousing, distribution, and value-added services), by mode of operation (storage, roadways distribution, seaways distribution, and others) and by region (North America, Europe, Asia-Pacific, and LAMEA). The report offers market size and forecasts for the green logistics market in value (USD) for all the above segments.

| By End User | |

| Healthcare | |

| Manufacturing | |

| Automotive | |

| Banking and Financial services | |

| Retail and E-commerce | |

| Others |

| By Business Type | |

| Warehousing | |

| Distribution | |

| Value-Added Services |

| By Mode of Operation | |

| Storage | |

| Roadways Distribution | |

| Seaways Distribution | |

| Others |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Green Logistics Market Research FAQs

How big is the Green Logistics Market?

The Green Logistics Market size is expected to reach USD 1.28 trillion in 2024 and grow at a CAGR of 8.29% to reach USD 1.91 trillion by 2029.

What is the current Green Logistics Market size?

In 2024, the Green Logistics Market size is expected to reach USD 1.28 trillion.

Who are the key players in Green Logistics Market?

United Parcel Service, AI Futtaim Logistics, Bollore Logistics, Yusen Logistics Co., Ltd and DHL International GmbH are the major companies operating in the Green Logistics Market.

Which region has the biggest share in Green Logistics Market?

In 2024, the Asia Pacific accounts for the largest market share in Green Logistics Market.

What years does this Green Logistics Market cover, and what was the market size in 2023?

In 2023, the Green Logistics Market size was estimated at USD 1.17 trillion. The report covers the Green Logistics Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Green Logistics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Green Logistics Industry Report

Statistics for the 2024 Green Logistics market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Green Logistics analysis includes a market forecast outlook for 2024 to (2024to2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.