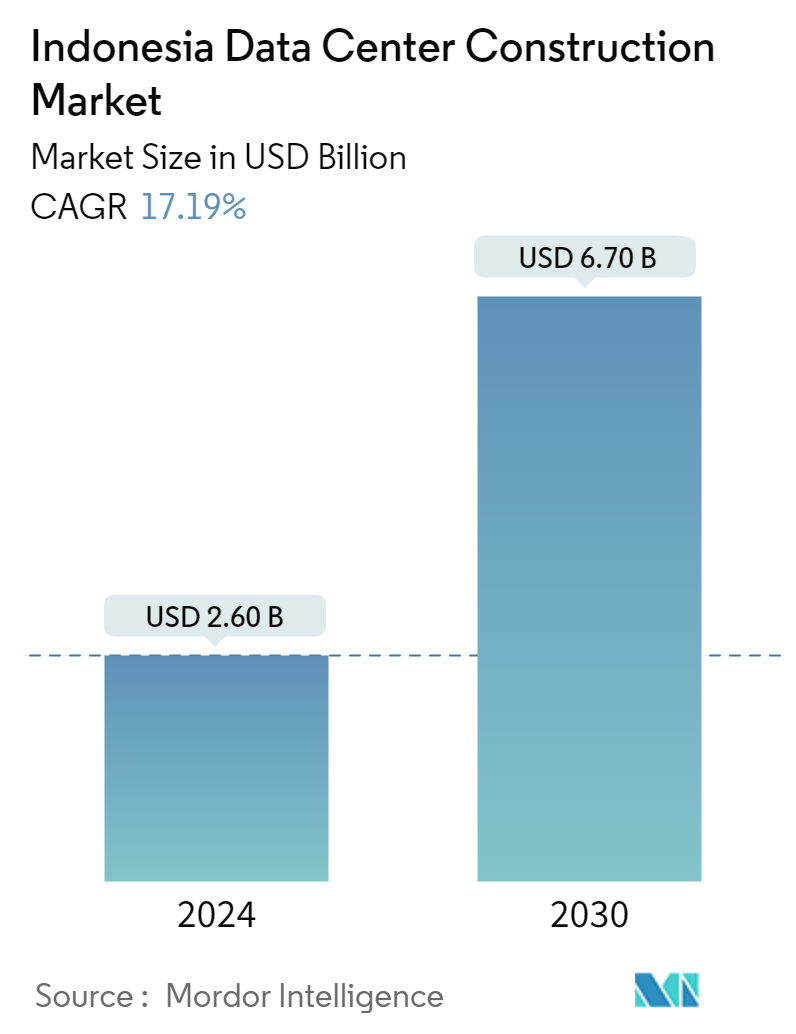

Indonesia Data Center Construction Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 2.60 Billion |

| Market Size (2029) | USD 6.70 Billion |

| CAGR (2024 - 2030) | 17.19 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Indonesia Data Center Construction Market Analysis

The Indonesia Data Center Construction Market size is estimated at USD 2.60 billion in 2024, and is expected to reach USD 6.70 billion by 2029, growing at a CAGR of 17.19% during the forecast period (2024-2029).

- The Indonesian data center construction market is experiencing notable growth, propelled by the surge in digitalization, increasing connectivity, and other market-driving factors.

- Under Construction IT Load Capacity: The upcoming IT load capacity of the Indonesian data center construction market is expected to reach 1,490 MW by 2030.

- Under Construction Raised Floor Space: The country's construction of raised floor area is expected to increase by 5.3 million sq. ft by 2030.

- Planned Racks: The country's total number of racks to be installed is expected to reach 267 thousand units by 2030.

- Planned Submarine Cables: Close to 50 submarine cable systems connect Indonesia, and many are under construction. One such submarine cable, estimated to be built by the end of 2026, is Apricot, which stretches over 11,972 km with landing points in Batam, Indonesia and Tanjung Pakis, Indonesia.

Indonesia Data Center Construction Market Trends

IT and Telecom to Register a Significant Market Share

- The Indonesian government, acknowledging the significance of cloud computing, has initiated programs to bolster its uptake. Specifically, it aims to digitally onboard over 64 million MSMEs, urging them to 'Go Digital and Go Global.' By 2024, the government aims to have 30 million MSMEs transitioned into the digital realm.

- Furthermore, the Indonesian government is actively encouraging tech giants to invest in the nation, bolstering its tech economy. For instance, during his visit in April 2024, Microsoft's CEO, Satya Nadella, unveiled plans for a substantial USD 1.7 billion investment in Indonesia. This investment is earmarked to enhance Indonesia's tech landscape, particularly in the realms of advanced cloud services and artificial intelligence. Central to this initiative is the establishment of data centers. Microsoft focuses on expanding Indonesia's data center infrastructure and cloud computing capabilities. Nadella stressed that this move is pivotal in bringing cutting-edge AI infrastructure to Indonesia, positioning Microsoft as a leader in this technological frontier.

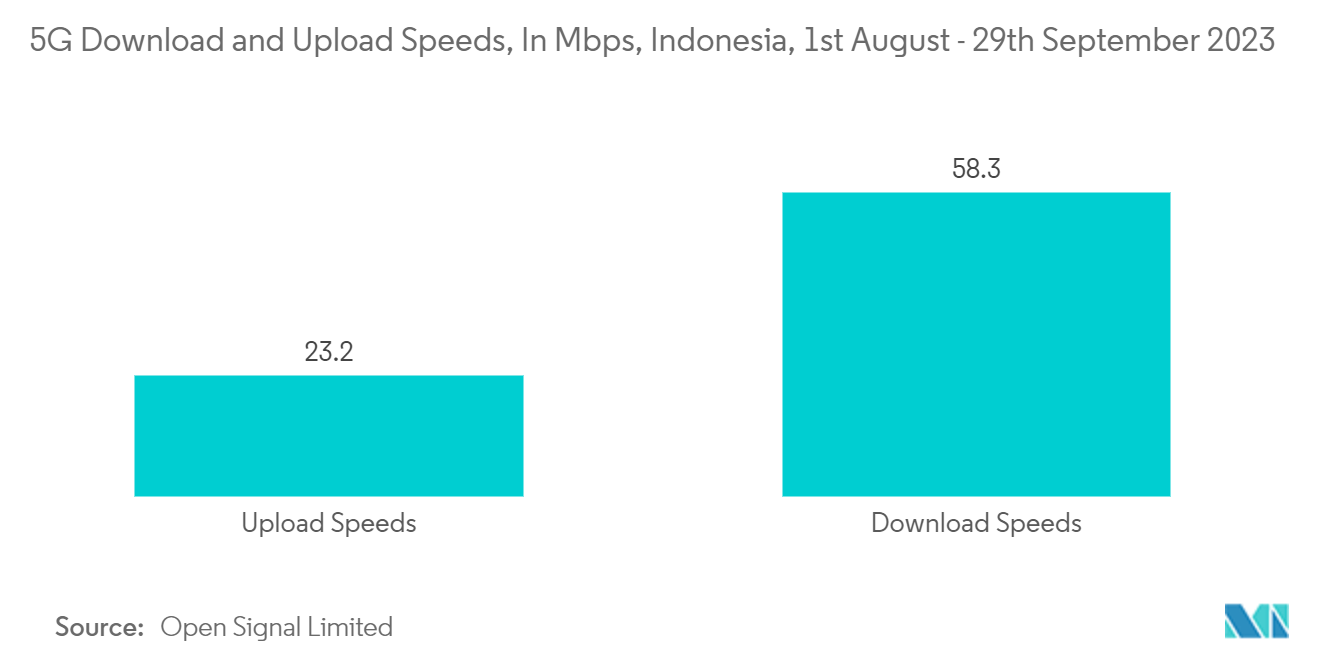

- Even in the telecom industry, the government is prioritizing technological collaborations and investments. In September 2023, the Indonesian government highlighted its openness to investment partnerships, particularly in advancing 5G digital connectivity to bolster the nation's digital infrastructure. Notably, by early September 2023, 5G networks were operational in just 49 Indonesian cities, leaving significant room for further expansion, as emphasized by the Communication and Information Minister.

- In September 2023, Telkomsel (PT Telekomunikasi Selular) and Ericsson unveiled their reinvigorated collaboration, aimed at bolstering and expanding their 4G and 5G networks across Indonesia. Ericsson, known for its connectivity solutions, rolled out its energy-efficient 5G Radio Access Network (RAN) products. These were deployed across strategic regions, including Aceh, North, Central, and West Sumatra, and the eastern part of Kalimantan, which encompasses the new capital city, Nusantara.

- This surge in data storage demand is poised to elevate the need for data centers in the region, thereby bolstering the prospects of data center construction firms in the coming years.

Tier 3 is Expected to Hold a Major Share of the Market Studied

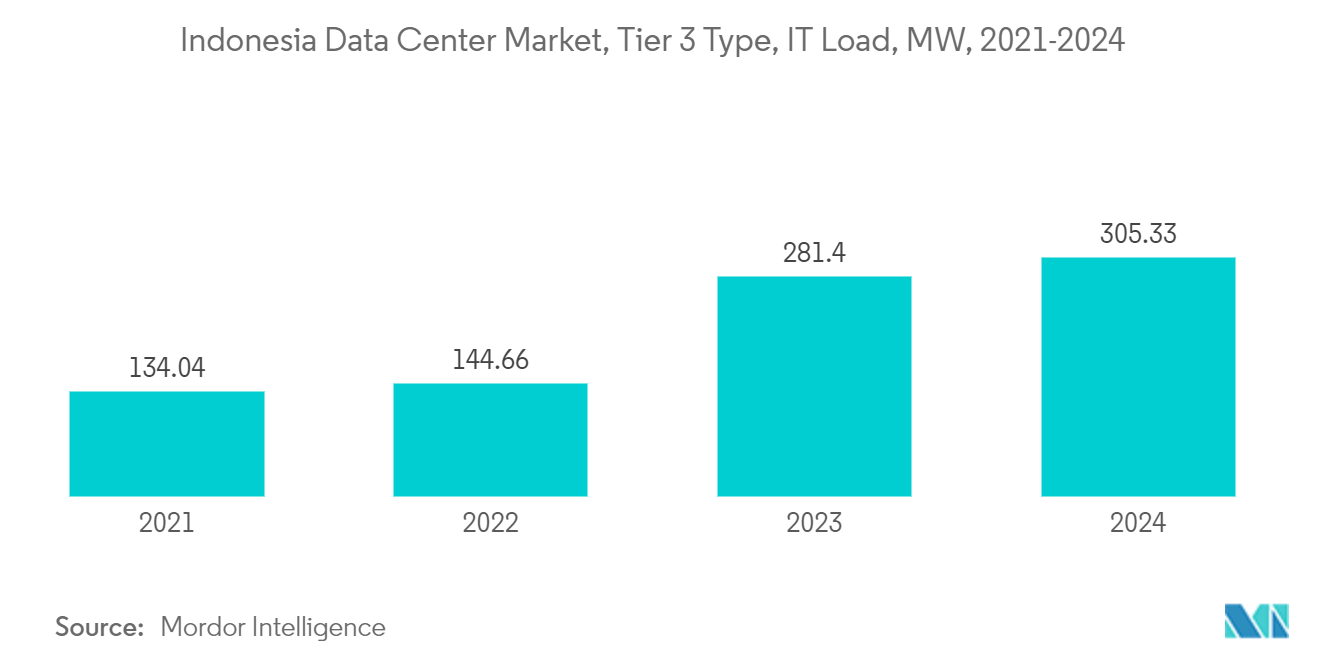

- The tier 3 segment had a share of over 54% in the Indonesian data center construction market in 2023. It is further projected to register a CAGR of 14% to reach an IT load capacity of 672 MW by 2030. Reliability and affordability are the major factors driving the demand for tier 3 data centers in the country.

- Furthermore, in 2023, Indonesia boasted over 22 tier 3-certified data centers, with approximately 18 concentrated in Greater Jakarta.

- In 2023, Space DC Pte Ltd led with a tier 3 certification, offering a maximum IT load capacity of 48 MW. XL Axiata Tbk PT (Princeton Digital Group) followed closely with 45.9 MW, trailed by Nusantara Data Center at 19.84 MW and Indosat Tbk PT (Big Data Exchange (BDx)) at 13.5 MW. Other players in the market also contributed.

- Considering IT load capacity, the tier 3 data centers in the region focus on accommodating large and massive loads. Massive centers take the lead at 48.5%, closely trailed by large centers at 42.4%. Although less prevalent, medium and small loads still hold notable shares at 5.7% and 3.5%, respectively.

- Over 8 data center facilities are currently under construction in the country, all adhering to tier 3 standards. Key players leading the tier 3 data center construction landscape include GTN Data Center (Edge Connex), GDS Holdings, and Indosat Tbk PT (Big Data Exchange (BDx)). A majority of these facilities are from Jakarta and Batam, with a smaller number in other regions.

- Such instances in the market studied are expected to drive demand for tier 3-certified facilities. This surge in demand, specifically from the tier 3 segment, will, in turn, bolster the need for data center construction services in the years ahead.

Indonesia Data Center Construction Industry Overview

The Indonesian data center construction market is moderately consolidated. Some significant players in the market include Aurecon Group Pty Ltd, PT AECOM Indonesia, Arup, Jacobs Engineering Group, and Turner & Townsend.

- June 2024: NTT announced the commencement of construction for its third data center in Indonesia, the Jakarta 2 Annex Data Center. Commercial operations are slated to begin in early 2026. Initially revealed in May, the seven-story Jakarta 2 Annex Data Center (JKT2A) is set to provide 12 MW of power across 5,800 sq. m (62,430 sq. ft) of IT space. The facility is specifically engineered to accommodate high-density racks, supporting loads of up to 40 kW.

- September 2023: Princeton Digital Group (PDG) inaugurated a state-of-the-art data center in Indonesia. The firm unveiled its latest 22 MW hyperscale data center, JC2, in Citibung, Greater Jakarta. This marks PDG's sixth establishment in Indonesia. Situated alongside JC1, the new facility spans 23,850 sq. m, elevating the Citibung campus's total capacity to 35 MW.

Indonesia Data Center Construction Market Leaders

-

Aurecon Group Pty Ltd.

-

PT AECOM Indonesia

-

Arup

-

Jacobs Engineering Group

-

Turner & Townsend

*Disclaimer: Major Players sorted in no particular order

Indonesia Data Center Construction Market News

- May 2024: Edgnex, a UAE-based data center company, announced plans to construct a 15 MW data center in Jakarta, Indonesia. The facility will be situated along MT Haryono, with the first phase of construction set for completion in the fourth quarter of 2025.

- June 2023: DCI Indonesia, a data center firm, unveiled its second building, H2-02, at its campus located outside Jakarta. The new 12 MW addition brings the total power capacity of the H2 campus to 27 MW, spanning two buildings. Situated on a sprawling 791-ha site in Karawang, east of Jakarta, the company's H2 campus boasts a massive capacity of up to 600 MW.

Indonesia Data Center Construction Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions And Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Research Framework

2.2 Secondary Research

2.3 Primary Research

2.4 Data Triangulation and Insight Generation

3. EXECUTIVE SUMMARY

4. MARKET INSIGHT

4.1 Market Overview

4.2 Market Dynamics

4.2.1 Market Drivers

4.2.1.1 The Rising Investments in Indonesia, Aimed at Bolstering its Cloud Services and Artificial Intelligence Capabilities, are Fueling the Demand for Data Centers

4.2.1.2 The Indonesia Government's Digital Initiatives Have Fueled a Surge in the Demand for Data Centers

4.2.2 Market Restraints

4.2.2.1 High Power Consumption and Emission Contribution of Data Centers

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitutes

4.3.5 Intensity of Competitive Rivalry

4.4 Key Indonesia Data Center Construction Statistics

4.4.1 Number of Data Centers in Indonesia, 2022 and 2023

4.4.2 Data Center Under Construction in Indonesia, in MW, 2024 - 2029

4.4.3 Average CapEx and Opex for the Indonesian Data Center Construction Market

4.4.4 Data Center Power Capacity Absorption in MW, Selected Cities, Indonesia, 2022 and 2023

4.4.5 The top CapEx spenders on Data center infrastructure in Indonesia.

5. MARKET SEGMENTATION

5.1 Market Segmentation - By Infrastructure

5.1.1 Market Segmentation - By Electrical Infrastructure

5.1.1.1 Power Distribution Solution

5.1.1.1.1 PDUs - Basic and Smart - Metered and Switched Solutions

5.1.1.1.2 Transfer Switches

5.1.1.1.2.1 Static

5.1.1.1.2.2 Automatic (ATS)

5.1.1.1.3 Switchgear

5.1.1.1.3.1 Low-voltage

5.1.1.1.3.2 Medium-voltage

5.1.1.1.4 Power Panels and Components

5.1.1.1.5 Others

5.1.1.2 Power Backup Solutions

5.1.1.2.1 UPS

5.1.1.2.2 Generators

5.1.1.3 Service (Design and Consulting, Integration, and Support and Maintenance)

5.1.2 Market Segmentation - By Mechanical Infrastructure

5.1.2.1 Cooling Systems

5.1.2.1.1 Immersion Cooling

5.1.2.1.2 Direct-to-chip Cooling

5.1.2.1.3 Rear Door Heat Exchanger

5.1.2.1.4 In-row and In-rack Cooling

5.1.2.2 Racks

5.1.2.3 Other Mechanical Infrastructures

5.1.3 General Construction

5.2 Market Segmentation - By Tier Type

5.2.1 Tier-I and-II

5.2.2 Tier-III

5.2.3 Tier-IV

5.3 Market Segmentation - By End User

5.3.1 Banking, Financial Services, and Insurance

5.3.2 IT and Telecommunications

5.3.3 Government and Defense

5.3.4 Healthcare

5.3.5 Other End Users

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Aurecon Group Pty Ltd

6.1.2 PT AECOM Indonesia

6.1.3 Arup

6.1.4 Jacobs Engineering Group

6.1.5 Turner & Townsend

6.1.6 AWP Architects

6.1.7 Aesler Group International

6.1.8 ARKONIN

6.1.9 DSCO Group Pte Ltd

6.1.10 Larsen & Toubro Limited

- *List Not Exhaustive

7. INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

9. ABOUT US

9.1 Industries Covered

9.2 Illustrative List of Clients in the Industry

9.3 Our Customized Research Capabilities

Indonesia Data Center Construction Industry Segmentation

Data center construction combines physical processes used to construct a data center facility. It chains construction standards with data center operational environment requirements.

The Indonesian data center construction market is segmented by infrastructure (electrical infrastructure [power distribution solutions (PDUs, transfer switches, switchgear, power panels and components, and other power distribution solutions), power backup solutions (UPS and generators), and services (design and consulting, integration, and support and maintenance)], mechanical infrastructure [cooling systems (immersion cooling, direct-to-chip cooling, rear door heat exchanger, and in-row and in-rack cooling), racks, and other mechanical infrastructures], and general construction), tier type (tier 1 and 2, tier 3, and tier 4), and end user (banking, financial services, and insurance, IT and telecommunications, government and defense, healthcare, and other end users). The market sizes and forecasts are provided in terms of value (USD) for the above segments.

| Market Segmentation - By Infrastructure | ||||||||||||||||||||

| ||||||||||||||||||||

| ||||||||||||||||||||

| General Construction |

| Market Segmentation - By Tier Type | |

| Tier-I and-II | |

| Tier-III | |

| Tier-IV |

| Market Segmentation - By End User | |

| Banking, Financial Services, and Insurance | |

| IT and Telecommunications | |

| Government and Defense | |

| Healthcare | |

| Other End Users |

Indonesia Data Center Construction Market Research Faqs

How big is the Indonesia Data Center Construction Market?

The Indonesia Data Center Construction Market size is expected to reach USD 2.60 billion in 2024 and grow at a CAGR of 17.19% to reach USD 6.70 billion by 2029.

What is the current Indonesia Data Center Construction Market size?

In 2024, the Indonesia Data Center Construction Market size is expected to reach USD 2.60 billion.

Who are the key players in Indonesia Data Center Construction Market?

Aurecon Group Pty Ltd., PT AECOM Indonesia, Arup, Jacobs Engineering Group and Turner & Townsend are the major companies operating in the Indonesia Data Center Construction Market.

What years does this Indonesia Data Center Construction Market cover, and what was the market size in 2023?

In 2023, the Indonesia Data Center Construction Market size was estimated at USD 2.15 billion. The report covers the Indonesia Data Center Construction Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Indonesia Data Center Construction Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Indonesia Data Center Construction Industry Report

Statistics for the 2024 Indonesia Data Center Construction market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Indonesia Data Center Construction analysis includes a market forecast outlook to for 2024 to 2030 and historical overview. Get a sample of this industry analysis as a free report PDF download.