Japan Bunker Fuel Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

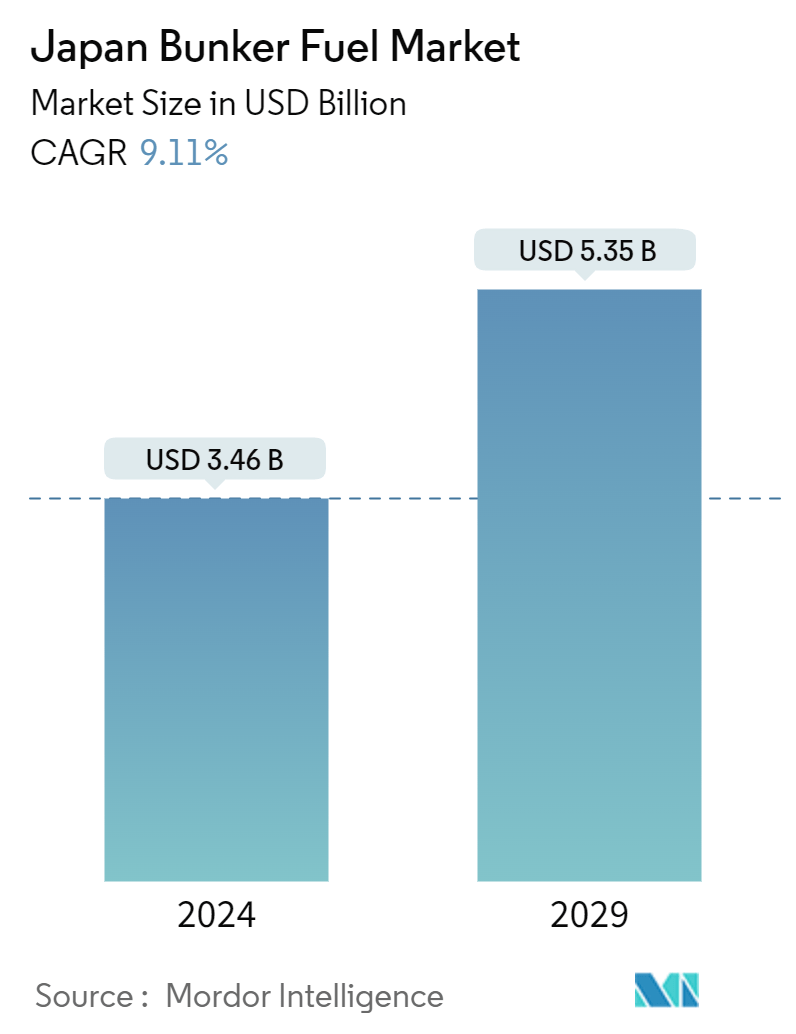

| Market Size (2024) | USD 3.46 Billion |

| Market Size (2029) | USD 5.35 Billion |

| CAGR (2024 - 2029) | 9.11 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Japan Bunker Fuel Market Analysis

The Japan Bunker Fuel Market size is estimated at USD 3.46 billion in 2024, and is expected to reach USD 5.35 billion by 2029, growing at a CAGR of 9.11% during the forecast period (2024-2029).

- In the medium period, factors such as rising demand for cleaner bunker fuels due to implementing more restrictive environmental regulations and the growing trade of LNG for the power sector in the regions are expected to drive the market between 2024 and 2029.

- On the other hand, changes in the cost of bunker fuel and crude oil are expected to hinder the market's growth.

- Nevertheless, the number of ships in service and the demand for maritime transportation are expected to create several future market opportunities from 2024 to 2029.

Japan Bunker Fuel Market Trends

Very Low Sulfur Fuel Oil (VLSFO) is Expected to Witness Significant Growth

- Bunker fuels have a high sulfur content and may emit harmful fumes. Different methods can be employed to lower sulfur concentration. Ultra-low-sulfur fuel oil is one of the varieties of this kind of fuel. With an IMO regulation going into effect in January 2020, there is a growing need for very low sulfur fuel oil (VLSFO) with a sulfur concentration of less than 0.5%.

- The majority of the market for high-sulfur fuel oil (HSFO) bunker fuel is anticipated to be replaced soon by low-sulfur substitutes. The majority of VLSFO sold on the market is made up of residual and distillate components combined with different cutters with different viscosities and sulfur contents to produce a product that meets specifications.

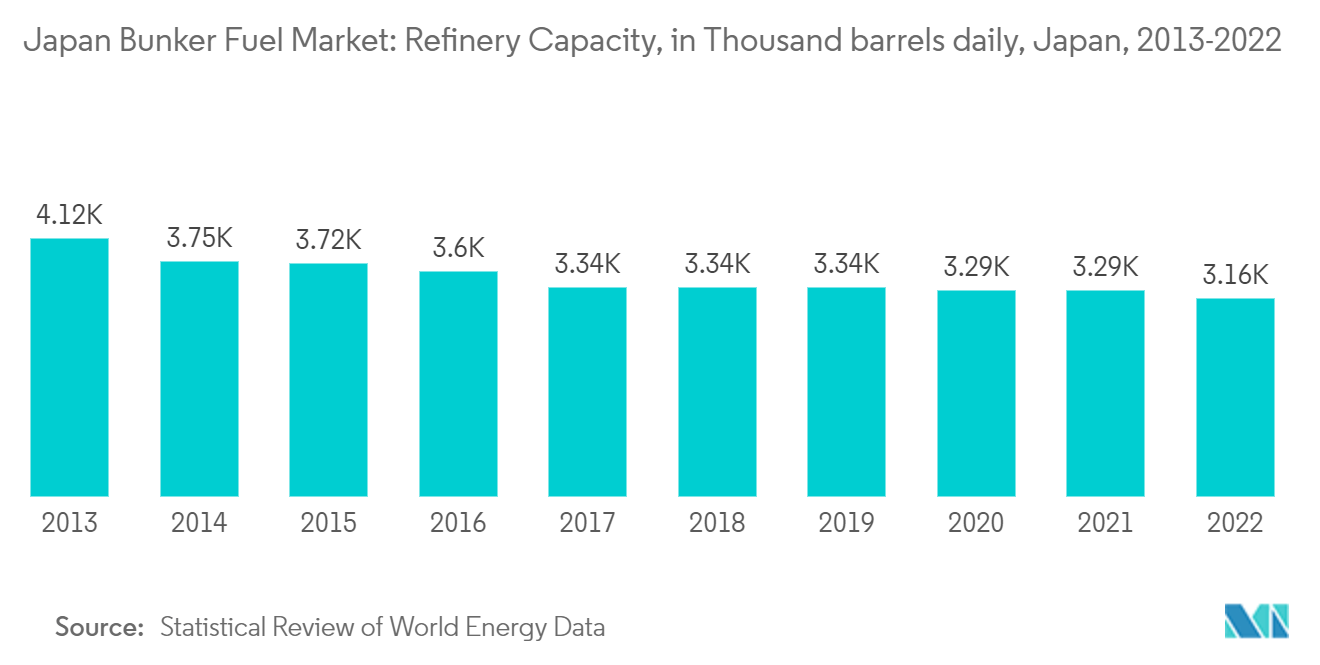

- The nation is focusing on increasing the number of refineries to overcome the increased demand for VLSFO. As of January 2024, Japan had 20 refineries. The country's refining capacity is 3.23 million b/d, compared to 6 million b/d in the early 1980s. The country is making strategies to increase the number of refineries to fulfill the demand for VLSFO and reach the previous numbers again. All these strategies are likely to fulfill the increased demand between 2024 and 2029.

- As of 2023, Japan's total bunker demand involved 70% of low-sulfur fuel oil (VLSFO) for deliveries of ocean-going vessels. This is more dependent on the refinery's capacity. The government is making plans to increase the refinery's capacity with several organizations. In February 2024, Cosmos announced that the refinery capacity is likely to be above 90% during FY2024-25 compared to 87.5 % in FY23-24.

- Moreover, in August 2023, Pemex announced that it had inked a deal with the Japan International Cooperation Agency (JICA) and the sustainable solutions company Adaptex to implement a plan for innovative technology to operate with greater energy efficiency in the refinery involving very low-sulfur fuel oil (VLSFO). All these types of agreements increase the demand for VLSFO between 2024 and 2029 and create future opportunities for the organization.

- Hence, driven by high domestic demand, recent developments, and upcoming oil refinery projects, the region is expected to drive the demand for the market from 2024 to 2029.

LNG as a Bunker Fuel is Likely to Witness Significant Growth

- The Japan LNG bunkering industry has developed over the last decade, driven by increased global LNG usage, clean energy demand, and the opportunity to minimize greenhouse gas emissions. LNG-powered vessels are becoming progressively higher in demand, and lower natural gas prices signaled the start of an expansion in the market for these kinds of vessels.

- The cost of converting the current operational vessels to LNG-powered vessels is significant. It is, therefore, not feasible economically. After the new pollution restrictions take effect, LNG-based vessels are anticipated to have the lowest operating costs of all the fuel options. Furthermore, a gradual transition from conventional ship fueling methods, such as heavy fuel oil, marine gas oil, and marine diesel oil, to LNG propulsion is more advantageous. The ship's operational efficiency has increased, and its carbon footprint is significantly reduced with LNG-based propulsion.

- Countries are now focusing on using LNG power carriers owing to the new environmental regulations. In February 2024, the first-ever capsized bulk carrier powered by LNG was to be delivered to Japan. The ship is the first Capesize LNG-fueled bulk carrier ever constructed at a Japanese shipyard, according to an NYK investigation. Expanding its fleet of LNG-fueled ships, NYK is taking on the issue of decarbonizing a complete supply chain while meeting the NYK Group's target of a 45% reduction in GHG emissions from FY2021 to FY2030. These developments increase the demand for LNG as a bunker fuel between 2024 and 2029.

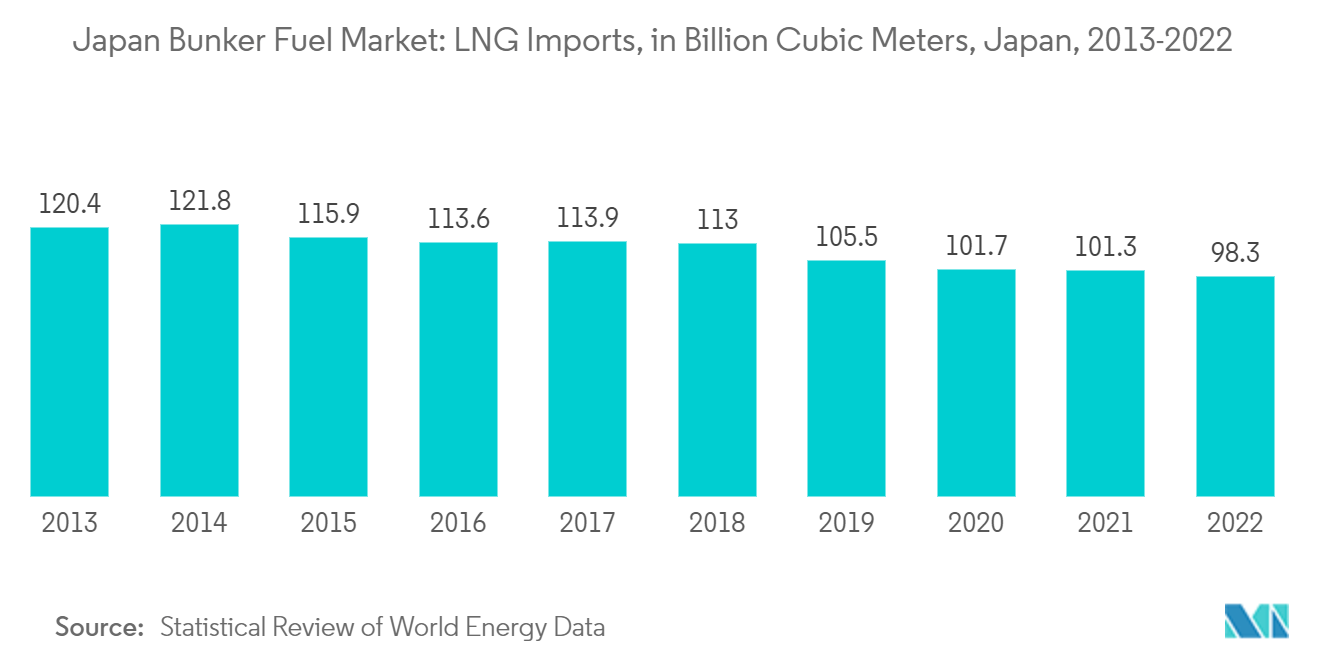

- According to the Statistical Review of World Energy Data, LNG imports were reported to be 98.3 billion cubic meters in 2022, which was reduced by 2.96% compared to 2021. The imports are likely to increase in the coming years as the government focuses on increasing the refinery capacity by signing multiple deals.

- Furthermore, in August 2023, LNG Japan Corp. agreed to pay up to USD 880 million for a stake in a massive natural gas project off the coast of Australia. The Scarborough project will see Woodside Energy Group give up 10% of its ownership to the joint venture, which Sumitomo Corp. and Sojitz Corp hold. Furthermore, a deal was reached to deliver 12 cargoes, or roughly 900,000 tons, of liquefied natural gas (LNG) annually for ten years starting in 2026 from the project. All these types of agreements increase the capacity of LNG between 2024 and 2029 and create future opportunities for the organization.

- Hence, driven by high domestic demand, recent developments, and upcoming projects, the region is expected to drive the demand for the market from 2024 to 2029.

Japan Bunker Fuel Industry Overview

The Japanese bunker fuel market is semi-consolidated. Some of the major players in this market are PetroChina Company Limited, Ocean Bunkering Services (Pte) Ltd, Shell Eastern Trading (Pte) Ltd, Equatorial Marine Fuel Management Services Pte Ltd, and Sentek Marine & Trading Pte Ltd.

Japan Bunker Fuel Market Leaders

-

PetroChina Company Limited

-

Ocean Bunkering Services (Pte) Ltd

-

Shell Eastern Trading (Pte) Ltd

-

Equatorial Marine Fuel Management Services Pte. Ltd.

-

Sentek Marine & Trading Pte Ltd

*Disclaimer: Major Players sorted in no particular order

Japan Bunker Fuel Market News

- July 2023: Asahi Tanker completed bunkering with marine biofuel (B24) and liquefied natural gas (LNG) for the oceangoing LPG tanker Buena Reina. Marine biofuel comprises roughly 24% of biofuel and conventional bunker fuel oil (VLSFO). The most significant port in Japan, Tokyo Bay, hosted the operation of Buena Reina, which Marubeni Corporation chartered.

- May 2023: The very large gas carrier (VLGC) in the United Arab Emirates (UAE) will receive a B24 biofuel bunker from Japanese LPG trader and importer Astomos Energy Corporation and compatriot energy business Inpex Corporation. According to the deal, Inpex will use a bunker ship run by the oil and shipping business Monjasa at the Khor Fakkan port in the UAE emirate of Sharjah to provide B2 biofuel to the VLGC that Astomos has rented.

Japan Bunker Fuel Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of Study

1.2 Market Definition

1.3 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Increasing LNG Trade

4.5.1.2 Rising Marine Transportation

4.5.2 Restraints

4.5.2.1 Fluctuations in Crude Oil Prices

4.6 Supply Chain Analysis

4.7 PESTLE Analysis

5. MARKET SEGMENTATION

5.1 By Fuel Type

5.1.1 High Sulfur Fuel Oil (HSFO)

5.1.2 Very-low Sulfur Fuel Oil (VLSFO)

5.1.3 Marine Gas Oil (MGO)

5.1.4 Other Fuel Types

5.2 By Vessel Type

5.2.1 Containers

5.2.2 Tankers

5.2.3 General Cargo

5.2.4 Bulk Carrier

5.2.5 Other Vessel Types

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Fuel Suppliers

6.3.1.1 PetroChina Company Limited

6.3.1.2 Ocean Bunkering Services (Pte) Ltd

6.3.1.3 Sentek Marine & Trading Pte Ltd

6.3.1.4 Equatorial Marine Fuel Management Services

6.3.1.5 Shell Eastern Trading (Pte) Ltd

6.3.2 Ship Owners

6.3.2.1 Cosco Shipping Lines Co Ltd

6.3.2.2 Orient Overseas Container Line (OOCL)

6.3.2.3 Parakou Group

6.3.2.4 Nan Fung Group

6.3.2.5 Mediterranean Shipping Company

6.3.2.6 The Great Eastern Shipping Co. Ltd

- *List Not Exhaustive

6.4 Market Ranking/Share Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Demand for Marine Transportation

Japan Bunker Fuel Industry Segmentation

Bunker fuel refers to any fuel pumped into a ship's bunkers to power its combustion engines. Deep-sea cargo ships often burn the heavy, residual oil that remains after gasoline, diesel, and other light hydrocarbons are removed from crude oil during the refining process.

The Japanese bunker fuel market is segmented by capacity and vessel type. By type, the market is segmented into high sulfur fuel oil (HSFO), very low sulfur fuel oil (VLSFO), marine gas oil (MGO), liquefied natural gas (LNG), and other fuel types. By vessel type, the market is segmented into containers, tankers, general cargo, bulk carriers, and other vessel types. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| By Fuel Type | |

| High Sulfur Fuel Oil (HSFO) | |

| Very-low Sulfur Fuel Oil (VLSFO) | |

| Marine Gas Oil (MGO) | |

| Other Fuel Types |

| By Vessel Type | |

| Containers | |

| Tankers | |

| General Cargo | |

| Bulk Carrier | |

| Other Vessel Types |

Japan Bunker Fuel Market Research FAQs

How big is the Japan Bunker Fuel Market?

The Japan Bunker Fuel Market size is expected to reach USD 3.46 billion in 2024 and grow at a CAGR of 9.11% to reach USD 5.35 billion by 2029.

What is the current Japan Bunker Fuel Market size?

In 2024, the Japan Bunker Fuel Market size is expected to reach USD 3.46 billion.

Who are the key players in Japan Bunker Fuel Market?

PetroChina Company Limited, Ocean Bunkering Services (Pte) Ltd, Shell Eastern Trading (Pte) Ltd, Equatorial Marine Fuel Management Services Pte. Ltd. and Sentek Marine & Trading Pte Ltd are the major companies operating in the Japan Bunker Fuel Market.

What years does this Japan Bunker Fuel Market cover, and what was the market size in 2023?

In 2023, the Japan Bunker Fuel Market size was estimated at USD 3.14 billion. The report covers the Japan Bunker Fuel Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Japan Bunker Fuel Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Japan Bunker Fuel Industry Report

Statistics for the 2024 Japan Bunker Fuel market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Japan Bunker Fuel analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.