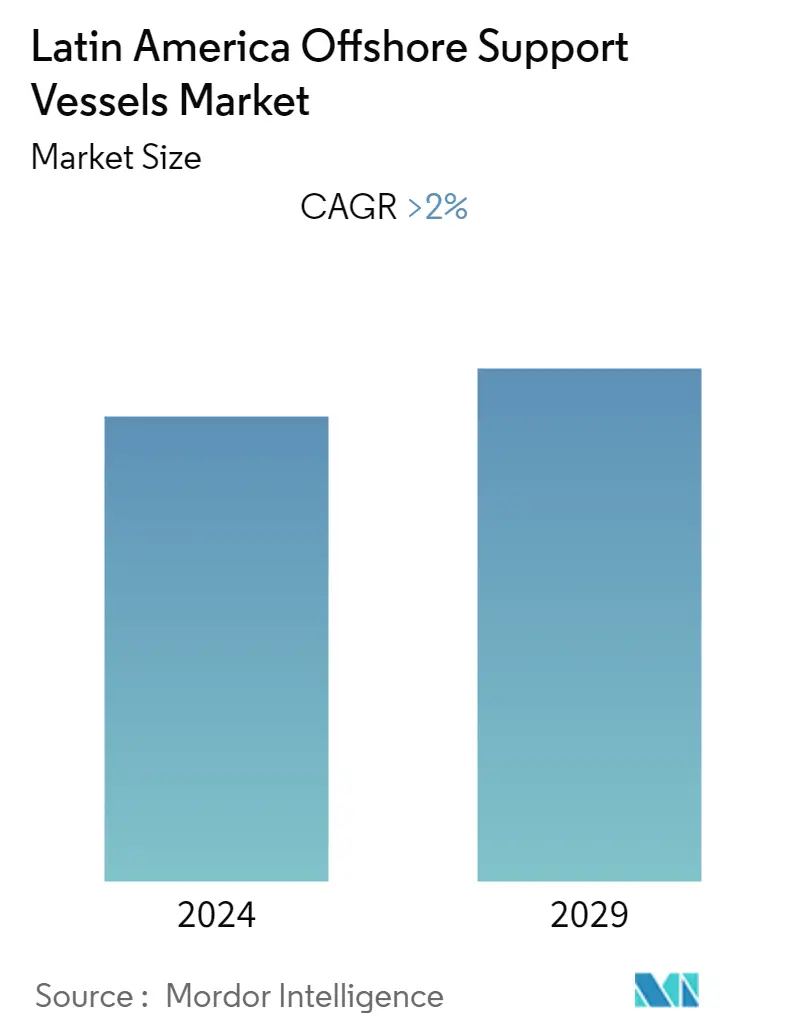

Latin America Offshore Support Vessels Market Size

| Study Period | 2021 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2021 - 2022 |

| CAGR | > 2.00 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Latin America Offshore Support Vessels Market Analysis

The Latin American offshore support vessels market is projected to register a CAGR of over 2% during the forecast period.

The market was negatively impacted by COVID-19. Presently the market has now reached pre-pandemic levels.

Over the medium term, factors like increased offshore oil and gas exploration and wind farm projects in the Atlantic Ocean are likely to drive the market.

On the other hand, stringent regulations by the governments and heavy fine for any issue related to the environment is likely to restrain market growth.

Nevertheless, increasing exploration and development activities in the recently found deep-water basins, such as Santos Basin and Campos Basin, are likely to create many opportunities for the Latin American offshore support market in the future.

Due to its highest number of deep-water activities in the Atlantic Ocean, Brazil is expected to see significant market growth during the forecast period.

Latin America Offshore Support Vessels Market Trends

This section covers the major market trends shaping the Latin America Offshore Support Vessels Market according to our research experts:

Platform Supply Vessels (PSVs) Segment to Dominate the Market

Latina America is home to some of the world's largest countries in terms of proven oil and gas reserves. The region also hosts one of the largest offshore oil and gas markets around the globe. Brazil, Venezuela, Mexico, Argentina, and Colombia are the major countries in the region's oil and gas industry.

Offshore oil and gas projects in Latina America have lower breakeven prices and competitive payback times compared to similar projects worldwide, making them more resilient in the current turbulent times. Around 30 offshore oil and gas projects are expected to start across the region by 2023, which requires a cumulative greenfield investment of around USD 50 billion. These projects are operated by a mix of national oil companies (NOCs) and major independent companies.

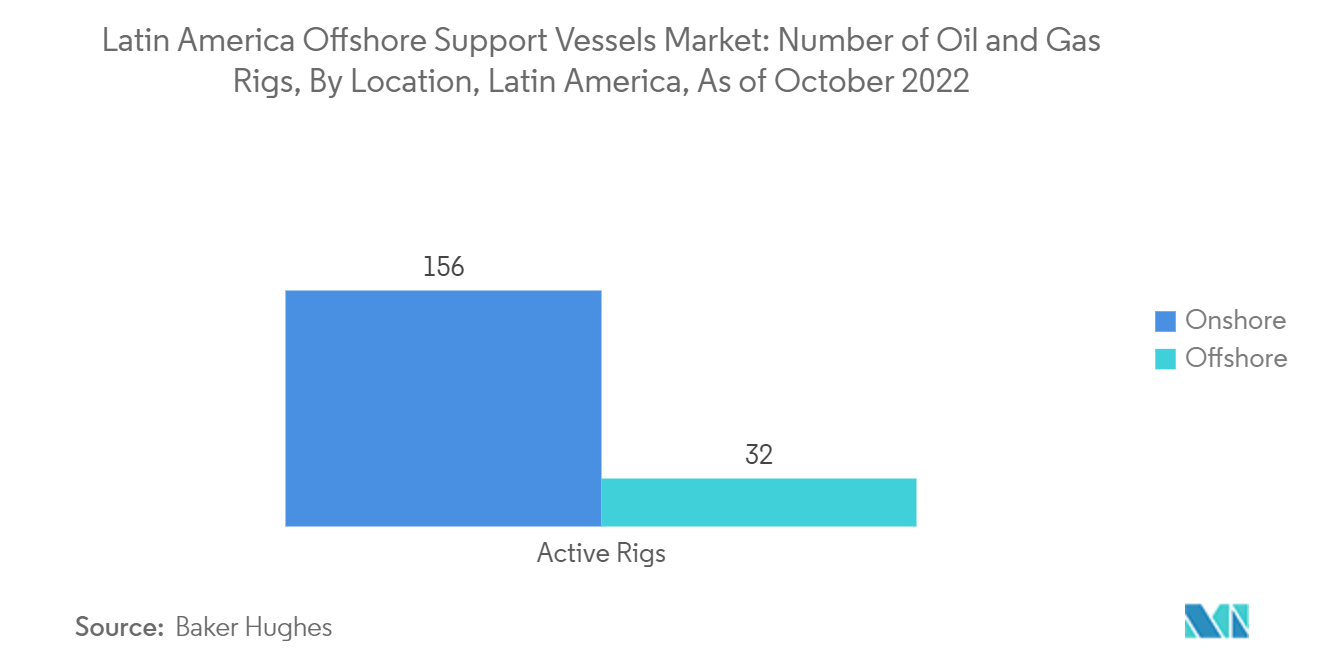

Platform Supply Vessels (PSVs) are the offshore vessels used for transferring equipment, crew, and other goods to the offshore drilling platform. In 2014, after a decrease in oil prices, the offshore support vessel market slowed down, but as the oil prices began to rise, the offshore support vessel market also gained its pace. As of October 2022, there were 156 onshore rigs in the region, with a further 32 rigs located offshore.

Guyana is expected to be a new entrant this decade in the list of major offshore producing regions due to the discovery of more than 8 billion BOE (barrel of oil equivalent) reserves in the ExxonMobil-operated Stabroek block. Close to 4 billion BOE of reserves are expected to be sanctioned by 2025, which will require investments in USD 30 billion and contribute more than 900,000 barrels of oil per day at peak production.

In July 2022, ExxonMobil and its partners announced two new oil discoveries in the Seabob-1 and Kiru-Kiru-1 wells, located in the Stabroek block offshore Guyana. As a result of these discoveries in the southeast of Liza and Payara developments, the previously discovered recoverable resources at the Stabroek block have been increased to approximately 11 billion barrel of oil equivalent.

In October 2022, Mexico's oil regulator approved the revamped plan presented by Pemex for developing the once-abandoned Lakach deepwater natural gas project.

The above-mentioned project's exploration and development phase will require huge amounts of equipment that can be delivered by platform supply vessels (PSVs).

Hence, the above points indicate that PSVs are expected to dominate the Latin American offshore support vessels market during the forecast period.

Brazil to Dominate the Market

The deepwater and ultra-deep-water activities directly influence the offshore support vessels market. After oil prices dropped in 2014, many countries shifted toward onshore projects. Still, it turned out that the return investment period of onshore projects is 10 to 15 years. So, Brazil started deepwater and ultra-deep-water explorations, which are more profitable and have a return investment period of 5 to 6 years.

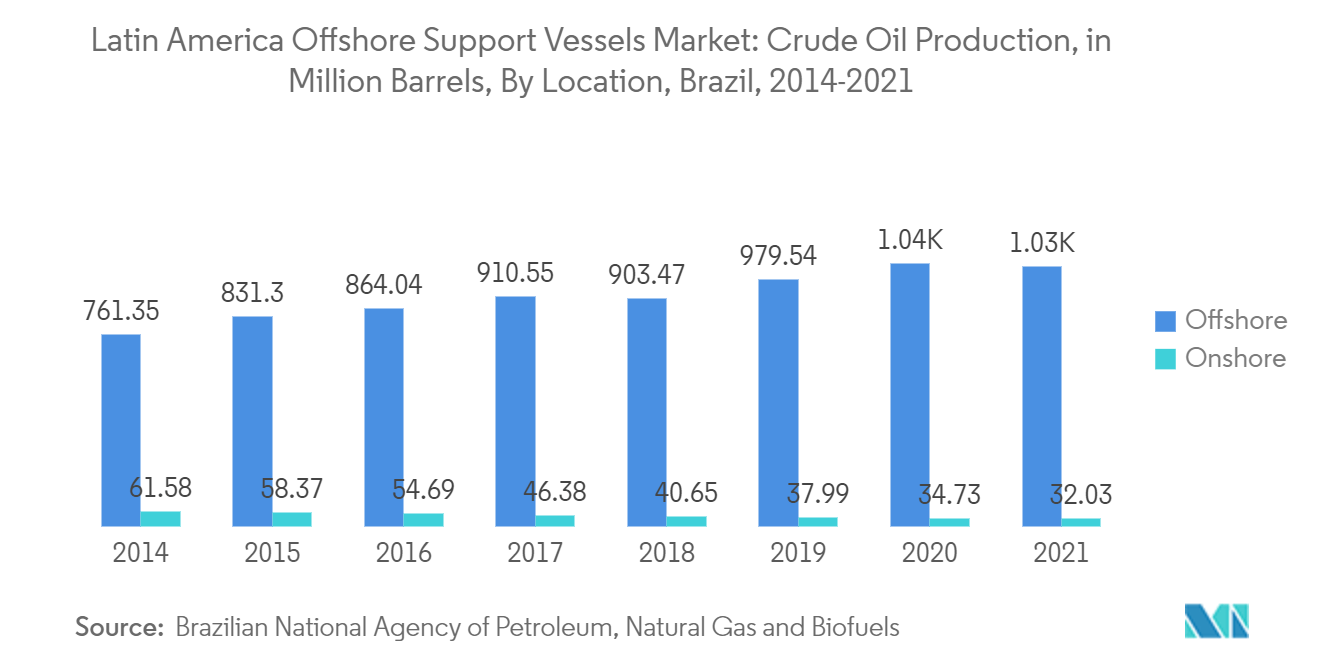

According to the National Agency of Petroleum, Natural Gas, and Biofuels (ANP), in 2021, out of the total crude oil production in the country, 97% came from offshore, and only 3 % came from onshore. The total crude oil production in the country was 1060.37 million barrel. Further upcoming projects in the deepwater are likely to increase Brazil's share in the Latin American offshore support vessels market.

In 2021, Brazil was the ninth-largest producer of oil and gas in the world, the largest producer in South America, and the eighth-largest oil product consumer in the world. Most of the oil and gas are produced offshore.

As of June 2022, around seven active rigs were operating in the offshore areas and three active rigs in the onshore areas of the country. As of 2021, floating assets such as floating production storage and offloading (FPSO), drillships, semi-submersibles, and Floating Storage and Offloading (FSO) accounted for more than 80% of the active offshore platforms in the country. This, in turn, indicates the dominance of offshore floating assets in Brazil's upstream oil and gas industry.

Brazil is expected to play a major role in the offshore oil and gas industry's recovery from a tumultuous 2020, especially in the floating production market. The country is expected to deploy around 18 FPSOs by 2025.

In May 2022, Singapore's Keppel Shipyard submitted the best bids in a Petrobras tender for the engineering, procurement, and construction (EPC) contracts for two FPSOs planned for Brazil's Buzios field. Keppel offered USD 2.98 billion each in lot A and lot B, beating the proposals of Sembcorp Marine, which offered USD 3.66 billion and USD 3.73 billion. Four other prospective bidders declined to submit proposals. Moreover, the FPSOs involved are P-80 and P-82, scheduled to begin operations in 2026 in the Santos basin pre-salt asset.

Petrobras plans to invest around USD 68 billion from 2022 to 2026. Of this total investment, 84% will be allocated to oil and natural gas exploration and production (E&P). Of the total E&P CAPEX (USD 57 billion), around 67% will be allocated to pre-salt assets. This indicates that the upstream oil and gas sector, especially Brazil's offshore oil and gas assets, is expected to witness significant investment during the forecast period. Therefore, factors such as plans to develop offshore oil and gas blocks, particularly in the presalt basins, are expected to drive the offshore support vessels market in Brazil during the forecast period.

Therefore, owing to the above points, Brazil, with most of the activities in the offshore deepwater, is likely to see significant growth in the Latin American offshore support vessels market during the forecast period.

Latin America Offshore Support Vessels Industry Overview

The Latin American offshore support vessels market is moderately consolidated. Some of the major players in the market include Edison Chouest Offshore, Tidewater Inc., GulfMark Offshore, Inc., SEACOR Marine Holdings Inc., and Bourbon Corp, among others.

Latin America Offshore Support Vessels Market Leaders

-

Edison Chouest Offshore

-

Tidewater Inc.

-

GulfMark Offshore, Inc

-

SEACOR Marine Holdings Inc

-

Bourbon Corp

*Disclaimer: Major Players sorted in no particular order

Latin America Offshore Support Vessels Market News

- October 2022: Brazil's Petrobras launched a public tender to procure up to 20 offshore support vessels, confirming its need for tonnage to support its ambitious growth plans.

- August 2022: Technology group Wärtsilä signed an agreement with Rio de Janeiro-based Companhia Brasileira de Offshore (CBO) on Decarbonisation Modelling. The objective is to support and accelerate CBO's journey towards decarbonized operations for its fleet of offshore support vessels, which is among the largest in Brazil in its segment. Wärtsilä's advanced platform utilizes a large amount of vessel data and machine learning algorithms, complemented by the company's extensive systems modeling experience. In this agreement, a detailed analysis will be conducted of the potential benefits to CBO of both short- and long-term solutions, including digitization, energy efficiency, and energy saving devices, hybridization, and alternative marine fuels in the future, with a specific focus on the viability of ethanol fuel in the future.

Latin America Offshore Support Vessels Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2027

4.3 Latin America Active Offshore Rig Count, till 2021

4.4 Recent Trends and Developments

4.5 Government Policies and Regulations

4.6 Market Dynamics

4.6.1 Drivers

4.6.2 Restraints

4.7 Supply Chain Analysis

4.8 Porter's Five Force Analysis

4.8.1 Bargaining Power of Suppliers

4.8.2 Bargaining Power of Consumers

4.8.3 Threat of New Entrants

4.8.4 Threat of Substitutes Products and Services

4.8.5 Intensity of Competitive Rivalry

5. MARKET SEGEMENTATION

5.1 Vessel Type

5.1.1 Anchor Handling Tug Vessel (AHTV)

5.1.2 Platform Supply Vessels (PSVs)

5.1.3 Other Vessel Types

5.2 Geography

5.2.1 Brazil

5.2.2 Argentina

5.2.3 Mexico

5.2.4 Guyana

5.2.5 Rest of Latin America

6. COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

6.2 Strategies Adopted by Key Players

6.3 Key Companies Profile

6.3.1 Edison Chouest Offshore

6.3.2 Tidewater Inc.

6.3.3 Bourbon Corp

6.3.4 Siem Offshore Inc.

6.3.5 GulfMark Offshore Inc.

6.3.6 AP Moeller Maersk A/S Class B

6.3.7 SEACOR Marine Holdings Inc.

6.3.8 Great Eastern Shipping Company Ltd

7. MARKET OPPORTUNITIES and FUTURE TRENDS

Latin America Offshore Support Vessels Industry Segmentation

Offshore support vessels, also known as offshore supply vessels, are ships designed specifically for operating on the ocean, serving multiple purposes. They may provide platform support, anchor handling, construction, maintenance, etc.

The Latin American offshore support vessels market is segmented by Vessel Type (Anchor Handling Tug Vessel (AHTV), Platform Supply Vessels (PSVs), and Other Vessel Types) and Geography (Brazil Argentina, Mexico, Guyana, and Rest of Latin America). The report also covers the market size and forecasts for the offshore support vessels market across major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue in USD billion.

Latin America Offshore Support Vessels Market Research FAQs

What is the current Latin America Offshore Support Vessels Market size?

The Latin America Offshore Support Vessels Market is projected to register a CAGR of greater than 2% during the forecast period (2024-2029)

Who are the key players in Latin America Offshore Support Vessels Market?

Edison Chouest Offshore, Tidewater Inc., GulfMark Offshore, Inc, SEACOR Marine Holdings Inc and Bourbon Corp are the major companies operating in the Latin America Offshore Support Vessels Market.

What years does this Latin America Offshore Support Vessels Market cover?

The report covers the Latin America Offshore Support Vessels Market historical market size for years: 2021, 2022 and 2023. The report also forecasts the Latin America Offshore Support Vessels Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Latin America Offshore Support Vessels Industry Report

Statistics for the 2024 Latin America Offshore Support Vessels market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Latin America Offshore Support Vessels analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.