Middle East & Africa Defense Market Size

| Study Period | 2019 - 2029 |

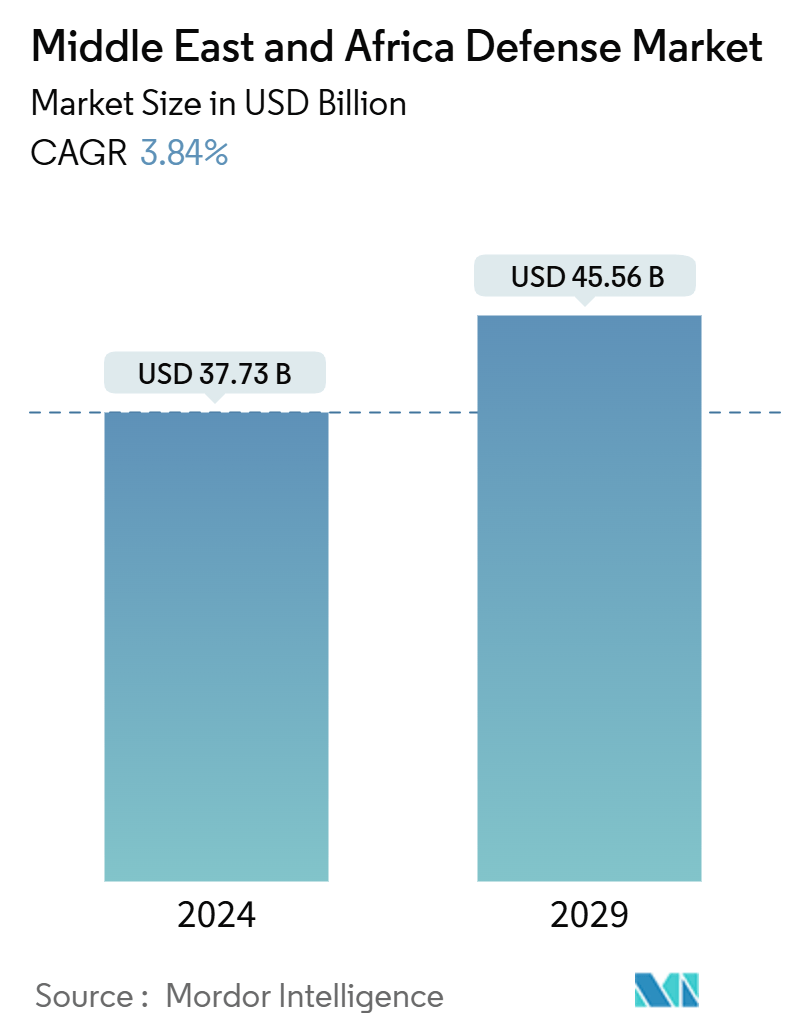

| Market Size (2024) | USD 37.73 Billion |

| Market Size (2029) | USD 45.56 Billion |

| CAGR (2024 - 2029) | 3.84 % |

| Fastest Growing Market | Middle East |

| Largest Market | Middle East |

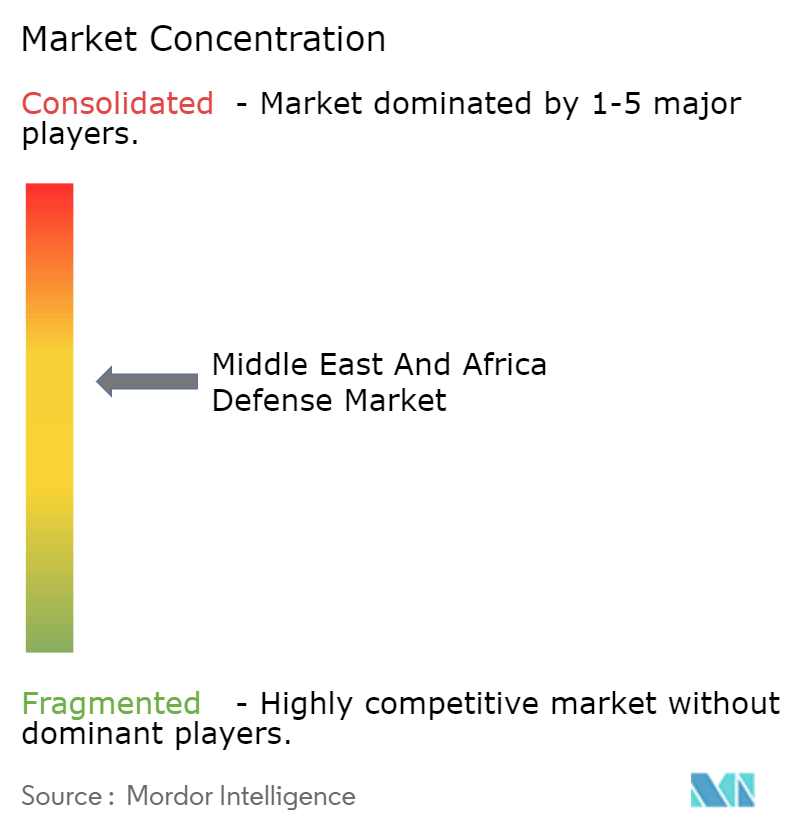

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East And Africa Defense Market Analysis

The Middle East And Africa Defense Market size is estimated at USD 37.73 billion in 2024, and is expected to reach USD 45.56 billion by 2029, at a CAGR of 3.84% during the forecast period (2024-2029).

The Middle East and Africa defense market is on the upswing, driven by rising geopolitical tensions, regional conflicts, and heightened military investments. Leading the charge are countries like Saudi Arabia, the United Arab Emirates, Israel, and Egypt, which are channeling billions into modernizing their military assets.

The MEA defense market is pursuing cutting-edge technologies, emphasizing artificial intelligence, cyber warfare, and electronic warfare systems. Furthermore, there's a noticeable trend of collaboration with global defense giants, focusing on technology transfers and local production.

Geopolitical instability and regional conflicts are primary catalysts for the MEA defense market's growth. Nations in the Middle East and Africa, often caught in border disputes and counter-terrorism operations, are ramping up investments to modernize and expand their defense capabilities. Ongoing tensions, such as those between Iran and certain GCC nations, alongside conflicts in Yemen, Libya, and Syria, have driven countries like Saudi Arabia, the UAE, and Israel to bolster their defense budgets. These nations procure advanced military assets, from missile defense systems to UAVs, to enhance their strategic deterrence and operational readiness. This push for advanced defense technology not only aims to bolster national security but also seeks to promote regional stability.

However, the MEA defense market grapples with a significant challenge: balancing the drive for advanced defense capabilities with fiscal constraints, especially amid economic uncertainties. Oil-dependent economies in the region find their defense budgets swayed by fluctuating oil prices, often influenced by geopolitical tensions and global economic shifts. Recent international economic slowdowns and changing energy policies have led to oil market volatility, straining defense budgets. As they modernize their defense, nations like Saudi Arabia and the UAE are also navigating the challenge of maintaining robust defense spending while pursuing economic diversification and infrastructure investments under their Vision 2030 initiatives.

The region's dependence on foreign defense suppliers and the intricacies of international defense trade—like sanctions and export controls—complicates procurement. The ever-shifting geopolitical landscape, marked by changing alliances and rivalries, further complicates defense acquisitions and strategic planning. For instance, sanctions on Iran and the looming threat of new sanctions on other regional entities can disrupt supply chains and stall vital defense initiatives. Navigating these fiscal and geopolitical waters is crucial to ensuring that defense modernization doesn't come at the expense of broader economic stability and growth aspirations.

Middle East And Africa Defense Market Trends

The Vehicles Segment to Experience the Highest Growth During the Forecast Period

The vehicle segment is expected to be a fast-growing segment in the Middle East and African defense market during the forecast period, mainly due to the growing threats to regional security, modernization programs, and technological advancements. The ongoing geopolitical tensions, as manifested through the conflicts in Yemen and Libya and counter-terrorism operations across the region, have brought about hefty investments in modern armored vehicles, given their enhanced protection, mobility, and firepower characteristics against advanced enemy threats in contemporary warfare and peacekeeping missions.

Countries such as Saudi Arabia and the United Arab Emirates are at the forefront, where the latter has ordered the most significant number of procurements to date, such as Oshkosh Defense's JLTVs and the modernization of existing fleets with state-of-the-art systems like Patria's AMV XP. The integration of advanced technologies like Active Protection Systems, C4ISR, and hybrid-electric propulsion systems is increasing demand for this segment even more. Other factors, like strategic cooperation and joint ventures between regional nations and significant defense firms, drive local production capacity. Such collaboration is best manifested in the deal between UAE's EDGE Group and Turkey's FNSS to produce Rabdan 8x8 vehicles.

Emphasis on indigenization and self-reliance in defense manufacturing under broader initiatives, such as Saudi Arabia's Vision 2030, is significantly driving the development of the domestic defense industrial base for the growth of this segment. Moreover, the versatility of armored vehicles for various military operations, from conventional wars to counter-insurgency, coupled with an increasing focus on homeland security and law enforcement functions, significantly contributes to the market expansion.

While there has been a rise in geopolitical tensions, regional conflicts, and counter-terrorism operations, the versatility, operational efficiency, and less risk to personnel are making the defense forces adopt UAVs. Countries such as Saudi Arabia, the United Arab Emirates, and Israel are at the front end of making their defense arsenals saturated with UAVs, either with an indigenization program or through international cooperation. For example, the local production of the CH-4 and Wing Loong II UAVs by Saudi Arabia in collaboration with China and the extensive deployment of Heron and Hermes UAVs by Israel are examples of the current trend.

Rapid technological change, especially in UAVs, such as increased payload capacities, extended flight endurance, and advanced sensor systems, is remarkably expanding their operational scope. UAVs fitted with state-of-the-art electro-optical/infrared (EO/IR) sensors, synthetic aperture radar (SAR), and electronic warfare (EW) systems provide unmatched situational awareness and precision strike capabilities. Moreover, the integration of AI and ML algorithms enables autonomous operations and real-time data processing, further enriching mission effectiveness.

In June 2023, Israel's Ministry of Defense took delivery of its inaugural Namer 1500 armored personnel carrier (APC). The Namer 1500, part of Israel’s flagship Merkava and Armored Vehicle Directorate project, is set to succeed the nation's aging M113 APCs.

Saudi Arabia to Dominate Market Share During the Forecast Period

Saudi Arabia's dominant market share in the Middle East and Africa is driven by significant infrastructural investments, technological developments, and strategic initiatives envisaged in Vision 2030. Saudi Arabia has used large inflows of its oil revenues to diversify the economy in areas like defense, aerospace, and renewable energy. Growing factors include the creation of NEOM, a USD 500 billion smart city project, and substantial military procurement programs to enhance the capacity to protect itself. Moreover, Saudi Arabia's geography as a logistics hub allows for colossal trade and investment inflows. Other market growth drivers include the country's strategy for developing indigenous manufacturing capabilities and forging public-private partnerships.

Collaborations with international technology companies and defense contractors position Saudi Arabia's commitment to becoming a regional leader in innovation and economic diversification. The government's policy to transform the digital economy and invest in emerging technologies like AI and UAS should remain a leading factor in sustaining its market lead. In February 2024, Munitions India secured a USD 225 million contract from Saudi Arabia for 155mm artillery shells. Weighing around 45 kilograms and measuring about 60 centimeters, these 155mm rounds are predominantly utilized in howitzer systems—massive cannons that adjust their barrels at varying angles for the desired range.

Additionally, in February 2024, the Ministry of Defense of Saudi Arabia signed numerous strategic contracts and MoUs at the World Defense Show in Riyadh to reinforce military readiness and combat efficiency through manufacturing localization in line with the directions of Vision 2030. These include contracts with PrivatAir Saudi Arabia, LIG Nex1, Raytheon Saudi Arabia, Middle East Propulsion Co., SAAB Saudi Arabia, SAMI Aerospace and Maintenance Services, SAMI LAND Systems, Haji Husein Ali Reza & Co., Modern Technology Co., Saudi Arabian Thales International, Big Blue Pearl Co., and Saudi Information Technology Co. These signed contracts and MoUs reflect a big step toward enhancing the military readiness and capabilities of the Saudi Armed Forces while fostering local industry growth and technological advancement in line with national strategic objectives.

Middle East And Africa Defense Industry Overview

The Middle East and Africa defense market is semi-consolidated, and market share is divided among regional and international players who provide their products and solutions to their respective domestic armed and security forces. Some prominent market players are The Boeing Company, Lockheed Martin Corporation, Saudi Arabian Military Industries, Israel Aerospace Industries Ltd, and BAE Systems PLC.

Elbit Systems Ltd, ASELSAN AS, Israel Aerospace Industries Ltd, and Denel SOC are some of the domestic players with an international presence that provides a wide range of military products, from portable military equipment for land forces to radars and other equipment onboard aircraft. SAMI spearheads the pivotal role of Saudi Arabia's Vision 2030 in localizing defense manufacturing, reducing dependence on foreign suppliers, and committing to substantial investment and strategic partnerships. IAI has robust aerospace and defense solutions in the form of UAVs, missile systems, international collaborations, and export activities.

Boeing and Lockheed Martin are regional international giants, supplying a wide range of military aircraft and defense systems. Boeing's growth can be fueled by its extensive portfolio and ongoing contracts with regional governments, while strategic regional partnerships drive Lockheed Martin's market presence. Denel SOC Ltd, South Africa's largest defense company, produces diverse military equipment and has formed strategic alliances with global defense companies to enhance its technological capabilities.

Government initiatives, like Saudi Arabia's Vision 2030, have been made toward enhancing the manufacturing of defense equipment locally, as this would encourage local industry growth and reduce foreign dependence. Continuous technological advancements and innovations, like the development of drones and missile defense systems, push the defense capabilities of the region even further.

For instance, in March 2024, SAMI Navantia signed the agreement to support Saudi Vision 2030, which includes improving operational capabilities through integrating state-of-the-art technologies to satisfy the needs of the Royal Saudi Naval Forces. SAMI's state-of-the-art computer equipment and software investment is a mark of commitment to excellence and leadership in the naval systems industries. This center focuses on integrating and developing naval systems via high-performance software, with key focuses on artificial intelligence, cybersecurity, and unmanned vehicle integration to assure local capability and independence of operation.

Middle East And Africa Defense Market Leaders

-

The Boeing Company

-

Lockheed Martin Corporation

-

BAE Systems plc

-

Israel Aerospace Industries Ltd.

-

Saudi Arabian Military Industries (SAMI)

*Disclaimer: Major Players sorted in no particular order

Middle East And Africa Defense Market News

- September 2024: EDGE Group inked a strategic partnership with the Brazilian Navy, aiming to finalize the development of the Navy's National Anti-Ship Missile (MANSUP) by the close of 2025. As part of the agreement, EDGE Group, in collaboration with SIATT - Brazil's foremost expert in smart weaponry would allocate essential resources to ensure timely delivery of the MANSUP. This is crucial for its integration into the Navy's upcoming Tamandaré class stealth frigates. The contract establishes a framework allowing EDGE Group to leverage MANSUP technology and data to advance the MANSUP-ER (Extended Range) variant.

- May 2024: IAI introduced the Compact ADA, a cutting-edge solution to shield avionic systems from GNSS jamming. The Compact ADA boasts a reduced Size, Weight, and Power (SWaP) profile, making it a jam-resistant GNSS system tailored for airborne tactical platforms.

- January 2024: Saab AB and the UAE Ministry of Defence signed a three-year contract worth USD 190 million for in-service support for the GlobalEye AEW&C. Saab will provide full-spectrum maintenance and operational support to the GlobalEye AEW&C, an imperative part of the UAE's state-of-the-art surveillance and reconnaissance capabilities.

Middle East And Africa Defense Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Buyers/Consumers

4.4.2 Bargaining Power of Suppliers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Procurement

5.1.1 Personnel Training and Protection

5.1.2 Communication Systems

5.1.3 Weapons and Ammunition

5.1.4 Vehicles

5.1.4.1 Land-based Vehicles

5.1.4.2 Sea-based Vehicles

5.1.4.3 Air-based Vehicles

5.2 MRO

5.2.1 Communication Systems

5.2.2 Weapons and Ammunition

5.2.3 Vehicles

5.3 Geography

5.3.1 Saudi Arabia

5.3.2 Turkey

5.3.3 Israel

5.3.4 Egypt

5.3.5 Algeria

5.3.6 South Africa

5.3.7 Morocco

5.3.8 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles

6.2.1 Saudi Arabian Military Industries (SAMI)

6.2.2 EDGE PJSC Group

6.2.3 Lockheed Martin Corporation

6.2.4 The Boeing Company

6.2.5 Elbit Systems Ltd.

6.2.6 Israel Aerospace Industries Ltd

6.2.7 RTX Corporation

6.2.8 Rheinmetall AG

6.2.9 ASELSAN A.S.

6.2.10 Rafael Advanced Defense Systems Ltd

6.2.11 Rheinmetall AG

6.2.12 Northrop Grumman Corporation

6.2.13 BAE Systems plc

6.2.14 Denel SOC Ltd.

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Middle East And Africa Defense Industry Segmentation

The Middle East and African defense market analyzes different defense equipment used to maintain the region's military strength. The study covers all aspects and is expected to provide insights into budget allocation and spending in the Middle East and African defense market during the forecast period.

The Middle East and Africa defense market is segmented into procurement, MRO, and geography. By procurement, the market is segmented into personnel training and protection, communication systems, weapons and ammunition, and vehicles. Vehicles include land, air, and sea-based vehicles. MRO segments the market into communication systems, weapons, ammunition, and vehicles. The report also covers the market sizes and forecasts for the major countries across the region. The market sizing and forecasts have been provided in value (USD).

| Procurement | |||||

| Personnel Training and Protection | |||||

| Communication Systems | |||||

| Weapons and Ammunition | |||||

|

| MRO | |

| Communication Systems | |

| Weapons and Ammunition | |

| Vehicles |

| Geography | |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Egypt | |

| Algeria | |

| South Africa | |

| Morocco | |

| Rest of Middle East and Africa |

Middle East And Africa Defense Market Research Faqs

How big is the Middle East And Africa Defense Market?

The Middle East And Africa Defense Market size is expected to reach USD 37.73 billion in 2024 and grow at a CAGR of 3.84% to reach USD 45.56 billion by 2029.

What is the current Middle East And Africa Defense Market size?

In 2024, the Middle East And Africa Defense Market size is expected to reach USD 37.73 billion.

Who are the key players in Middle East And Africa Defense Market?

The Boeing Company, Lockheed Martin Corporation, BAE Systems plc, Israel Aerospace Industries Ltd. and Saudi Arabian Military Industries (SAMI) are the major companies operating in the Middle East And Africa Defense Market.

Which is the fastest growing region in Middle East And Africa Defense Market?

Middle East is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Middle East And Africa Defense Market?

In 2024, the Middle East accounts for the largest market share in Middle East And Africa Defense Market.

What years does this Middle East And Africa Defense Market cover, and what was the market size in 2023?

In 2023, the Middle East And Africa Defense Market size was estimated at USD 36.28 billion. The report covers the Middle East And Africa Defense Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Middle East And Africa Defense Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Middle East And Africa Defense Industry Report

Statistics for the 2024 Middle East & Africa Defense market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Middle East & Africa Defense analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.