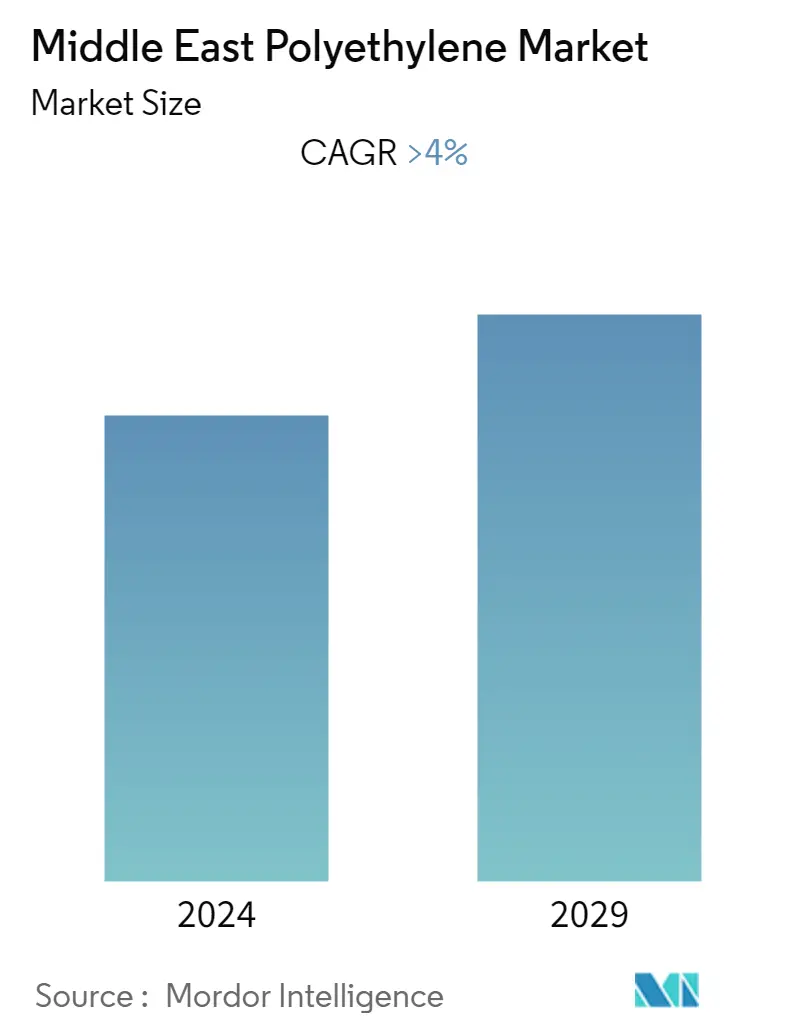

Middle East Polyethylene Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | > 4.00 % |

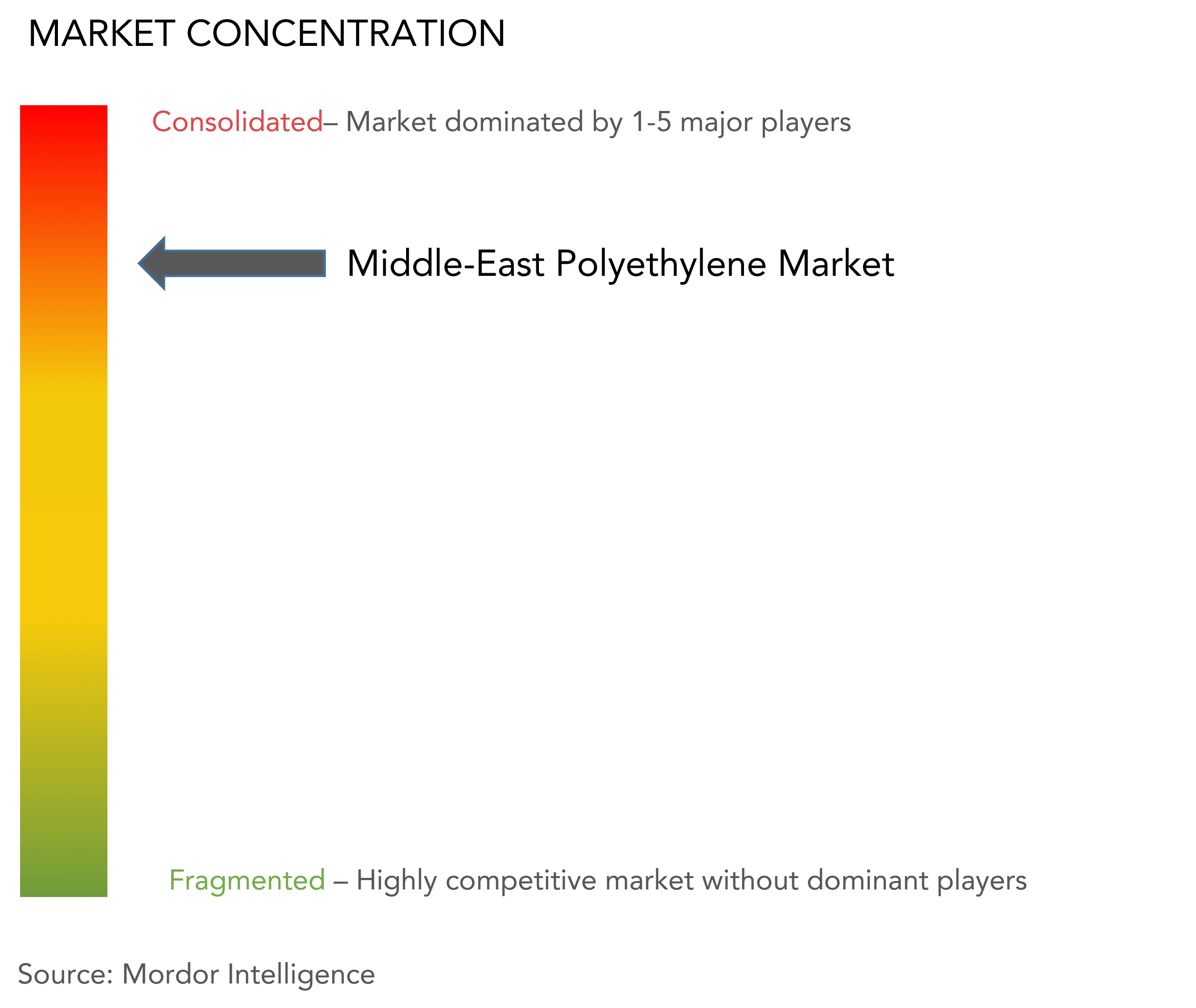

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Middle East Polyethylene Market Analysis

The Middle Eastern polyethene market is anticipated to register a CAGR of greater than 4% during the forecast period. The COVID-19 pandemic had a negative impact on the market studied as demand from industries like automotive, electrical and electronics, and consumer goods witnessed a downfall. Crude oil prices fell due to a drop in demand and excess supply. Polyethene, on the other hand, is expected to be in high demand from the healthcare and packaging industries. Despite environmental worries about plastics, the market will continue to develop because these materials are used practically in all everyday items. Currently, the Middle Eastern polyethene market is recovered from the pandemic and is growing significantly.

- Over the short term, the increasing demand for polyethene from a diverse range of end-use industries, including automotive, electrical, electronics, food and beverage, and consumer goods, has driven the market's growth.

- However, the availability of substitutes such as polypropylene and polyethene terephthalate products is limiting product adoption and is expected to hamper market growth over the forecast period.

- Nevertheless, the enhanced properties of polyethylene are promoting its applications in fashion clothes, sports goods, toys, and others.

Middle East Polyethylene Market Trends

This section covers the major market trends shaping the Middle East Polyethylene Market according to our research experts:

Increasing Demand in the Building and Construction Industry

- Polyethylene is used in building and construction for pipe-in-pipe, entryways, rooftop sheets, and slabs. The characteristics of polyethylene, such as strong thermal insulation, frost resistance, and flexibility, promote its usage in a variety of construction applications.

- Furthermore, polyethylene is employed in the building industry as window films, flooring, countertop protection, and even roofing. Polyethylene sheet is also used to seal rooms and cover construction components.

- The Middle Eastern construction industry is expanding. For economic diversification, the Saudi government is focusing on boosting the education, healthcare, infrastructure, and industrial sectors. As a result, demand for institutional, residential, industrial, and commercial buildings is likely to rise.

- From 2010 to 2025, Saudi Arabia's first-phase projects have a combined budget of USD 16.8 billion, including the construction and upgrade of 5500 kilometers. The Saudi Railway Master Plan's (SRMP) second-phase projects will build 3000 km of track for USD 55.7 billion, while the third-phase plans will build 1400 km of track for USD 24.8 billion between 2034 and 2040. It was also intended to gradually privatize services while independently maintaining the regulatory and operational sectors of the railway firm.

- Qatar pursued a wide range of infrastructural and industrial projects as part of its commitment to hosting the 2022 FIFA World Cup, its commitment to its National Vision 2030, and its objective of hosting the Asian Games in 2030. In the run-up to the 2022 FIFA World Cup, a few high-value road and rail transportation projects will be built over the following two years to improve connectivity and alleviate the problem of excessive congestion around Doha.

- The UAE is also working toward a brighter and more environmentally friendly future. Masdar Metropolis is the world's first zero-carbon, zero-waste, car-free city in Abu Dhabi. The United Arab Emirates effectively changed it from a future science notion to an organic, metropolitan organism. When completed in 2025, Masdar City will serve as a model for the rest of the region. The UAE construction industry is ready to enter a new period of growth, spurred by the country's lofty aspirations for the next 50 years and newer, more progressive legislation.

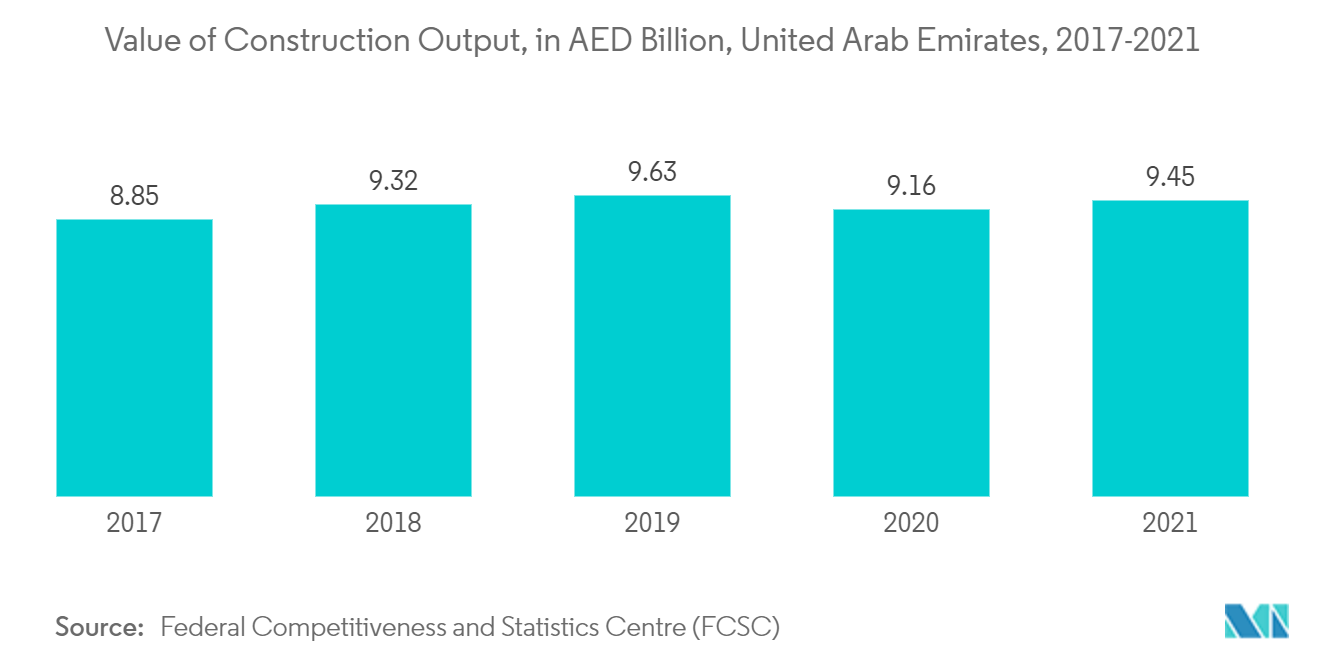

- According to Federal Competitiveness and Statistics Centre (FCSC), the value of construction output in the United Arab Emirates was AED 9.45 billion (USD 2.57 billion) as compared to AED 9.16 billion (USD 2.49 billion) in 2020.

- The Egyptian government is a significant player in the building business. A high-profile example is the Egyptian government's development of a massive "New Administrative Capital" 30 miles east of Cairo. The project's first phase, which includes all cabinet departments and authorities, is virtually complete, and the government will relocate to the new capital by the end of 2021.

- All the aforementioned factors are expected to drive construction activity in the Middle Eastern region, which also impacts the demand for polyethylene during the forecast period.

Saudi Arabia is Anticipated to Hold a Major Share in Middle East

- Saudi Arabia dominates the polyethylene market in terms of market share and market size. The country is likely to maintain its dominance over the forecast period.

- The Saudi economy is reliant on oil exports. Furthermore, the government has tight control over all key economic operations.

- The construction industry accounts for roughly 6%-7% of the country's total GDP. For economic diversification, the Saudi government is focusing on boosting the education, healthcare, infrastructure, and industrial sectors. As a result, demand for institutional, residential, industrial, and commercial buildings is likely to rise.

- The country is looking for qualified builders to shape its most ambitious projects, which have a USD 1.1 trillion project backlog. Saudi Arabia is amid Vision 2030, a major transformation agenda underpinned by megaprojects such as the Neom super-city tourist destination, the 334 km2 entertainment city of Qiddiya, the development at the UNESCO World Heritage site of Al-Ula, and the luxury and sustainable tourism-focused Red Sea Project.

- Furthermore, the Saudi Ministry of Housing stated announced its plan to build around 100,000 additional housing units in collaboration with real estate companies for a total cost of SAR 65 billion. Nineteen projects have already been announced in nine regions of the country, with an additional 40 private projects expected to offer 14,000 "villa" housing units in the country.

- Saudi Arabia is embarking on several residential and commercial projects, which are projected to boost the country's construction activity. The Neom Metropolis Project is a projected cross-border city in Tabuk Province, northwestern Saudi Arabia. Its goal is to have smart city technology while simultaneously serving as a tourism destination. The region is located in the northern Red Sea, south of Jordan and Israel, and east of Egypt across the Tiran Strait. It will cover an estimated 26,500 km2 and stretch 460 kilometers along the Red Sea coast.

- According to General Authority for Statistics (Saudi Arabia), the revenue from building construction in Saudi Arabia is expected to be roughly USD 28,7 billion by 2024. Polyethylene is employed in many transportation applications, such as glazing, interior wall panels, dividers, headliners, and light diffusers. According to the Central Department of Statistics and Information, the transportation sub-index of the Consumer Price Index (CPI) basket grew to 118.83 points in October 2022, up from 118.77 points in September 2022.

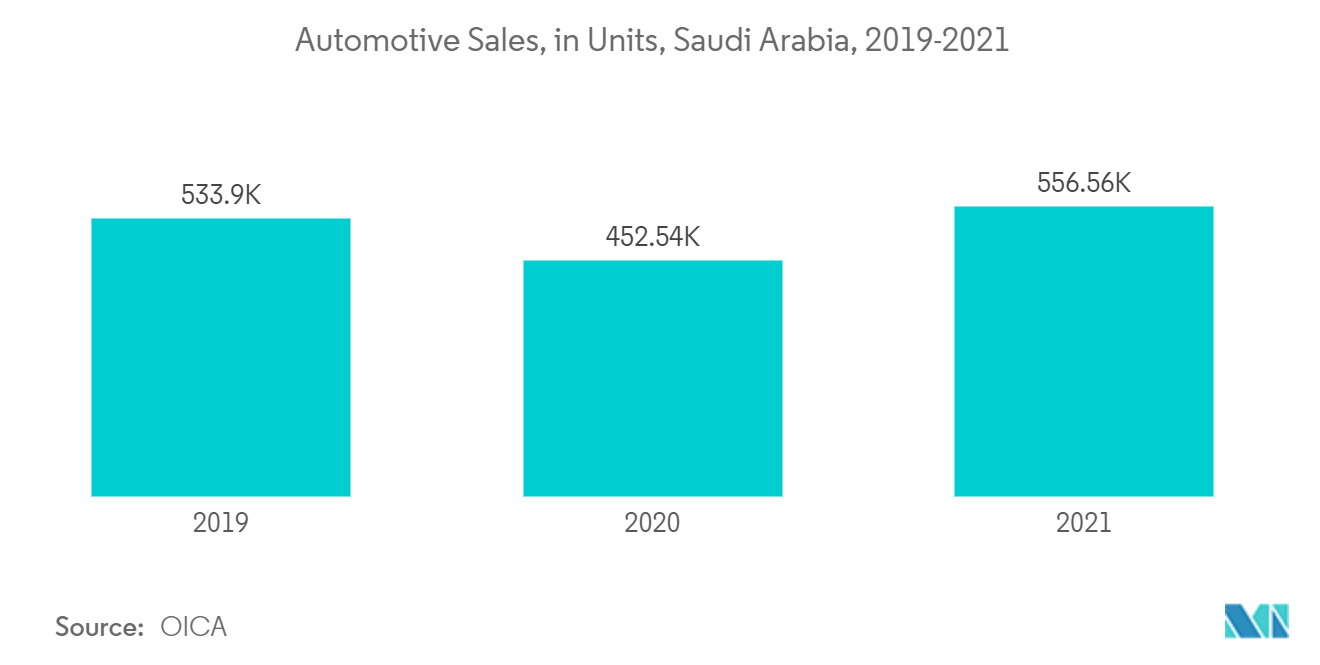

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), automotive sales in Saudi Arabia accounted for 556,559 units in 2021, compared to 452,544 units in the previous year.

- Thus, all the above-mentioned factors are likely to provide growth opportunities for the Middle Eastern polyethylene market during the forecast period.

Middle East Polyethylene Industry Overview

The Middle Eastern polyethylene market is consolidated in nature. Some of the major manufacturers in the market include Dow, Exxon Mobil Corporation, LyondellBasell Industries Holdings BV, Saudi Ethylene and Polyethylene Co. (Tasnee), and SABIC among others (in no particular order).

Middle East Polyethylene Market Leaders

-

Dow

-

Exxon Mobil Corporation

-

LyondellBasell Industries Holdings BV

-

Saudi Ethylene and Polyethylene Co. (Tasnee)

-

SABIC

*Disclaimer: Major Players sorted in no particular order

Middle East Polyethylene Market News

- November 2022: SABIC partnered with Guangdong Jinming Machinery Co. Ltd, a plastic packaging equipment manufacturer, and Bolsas de los Altos, a leading plastic film and packaging converter. The agreement will allow SABIC polyolefin resin products, as well as polyethylene resin offers from Gulf Coast Growth Ventures (GCGV) and TRUCIRCLETM, to be tested and validated.

- September 2021: SABIC announced the development of a new technology and range of dedicated polyethylene (PE) and polypropylene (PP) resins that represent a substantial advancement in the performance profile of polyolefin pressure pipes. The technique is being developed from concept to reality in collaboration with Tecnomatic and aquatherm, two key specialists in pipe manufacture.

Middle East Polyethylene Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from a Diverse Range of End-user Industries

4.1.2 Growth in Industrial Applications such as Primarily Packing Automotive and Electrical Replacement Part

4.2 Restraints

4.2.1 Availability of Substitutes such as Polypropylene and Polyethylene Terephthalate Products

4.2.2 Other Restraints

4.3 Industry Value-Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION

5.1 By Product Type

5.1.1 HDPE

5.1.2 LDPE

5.1.3 LLDPE

5.1.4 Other Product Types

5.2 By Application

5.2.1 Blow Molding

5.2.2 Films and Sheets

5.2.3 Injection Molding

5.2.4 Pipes and Conduit

5.2.5 Wires and Cables

5.2.6 Other Applications

5.3 By End-user Industry

5.3.1 Packaging

5.3.2 Transportation

5.3.3 Electrical and Electronics

5.3.4 Building and Construction

5.3.5 Agriculture

5.3.6 Other End-user Industries

5.4 By Country

5.4.1 Saudi Arabia

5.4.2 UAE

5.4.3 Qatar

5.4.4 Kuwait

5.4.5 Oman

5.4.6 Iran

5.4.7 Rest of the Middle East

6. COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Rank Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Amir Kabir Petrochemical Co. (AKPC)

6.4.2 Dow

6.4.3 Exxon Mobil Corporation

6.4.4 Ilam Petrochemical

6.4.5 Jam Petrochemical Co.

6.4.6 LyondellBasell Industries Holdings BV

6.4.7 Marun Petrochemical Co.

6.4.8 SABIC

6.4.9 Saudi Ethylene and Polyethylene Co. (Tasnee)

6.4.10 Saudi Polymers Company (Chevron & SABIC)

6.4.11 Sharq - Eastern Petrochemical Co. (SDPC)

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 The Simplicity of Product Molding in Polyethylene is Expanding its Application Range

Middle East Polyethylene Industry Segmentation

Polyethylene (PE) is a light, flexible synthetic resin created by polymerizing ethylene. Polyethylene is a member of the essential polyolefin resin family. It is the most commonly used plastic in the world, found in everything from clear food wraps and shopping bags to detergent bottles and automotive fuel tanks. It can also be split or spun into synthetic fibers or made to have rubber-like elastic characteristics.

The Middle Eastern polyethylene market is segmented into product type, application, end-user industry, and geography. By product type, the market is segmented into HDPE, LDPE, LLDPE, and other product types. By application, the market is segmented into blow molding, films and sheets, injection molding, pipes and conduits, wires and cables, and other applications. By end-user industry, the market is segmented into packaging, transportation, electrical and electronics, building and construction, agriculture, and other end-user industries. The report covers the market size and forecast for the Middle Eastern polyethylene market in 6 countries across the Middle East. For each segment, the market sizing and forecasts have been done based on volume in tons.

| By Product Type | |

| HDPE | |

| LDPE | |

| LLDPE | |

| Other Product Types |

| By Application | |

| Blow Molding | |

| Films and Sheets | |

| Injection Molding | |

| Pipes and Conduit | |

| Wires and Cables | |

| Other Applications |

| By End-user Industry | |

| Packaging | |

| Transportation | |

| Electrical and Electronics | |

| Building and Construction | |

| Agriculture | |

| Other End-user Industries |

| By Country | |

| Saudi Arabia | |

| UAE | |

| Qatar | |

| Kuwait | |

| Oman | |

| Iran | |

| Rest of the Middle East |

Middle East Polyethylene Market Research FAQs

What is the current Middle East Polyethylene Market size?

The Middle East Polyethylene Market is projected to register a CAGR of greater than 4% during the forecast period (2024-2029)

Who are the key players in Middle East Polyethylene Market?

Dow, Exxon Mobil Corporation, LyondellBasell Industries Holdings BV, Saudi Ethylene and Polyethylene Co. (Tasnee) and SABIC are the major companies operating in the Middle East Polyethylene Market.

What years does this Middle East Polyethylene Market cover?

The report covers the Middle East Polyethylene Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Middle East Polyethylene Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Middle East Polyethylene Industry Report

Statistics for the 2024 Middle East Polyethylene market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Middle East Polyethylene analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.