Market Size of Military Radars Industry

| Study Period | 2019 - 2029 |

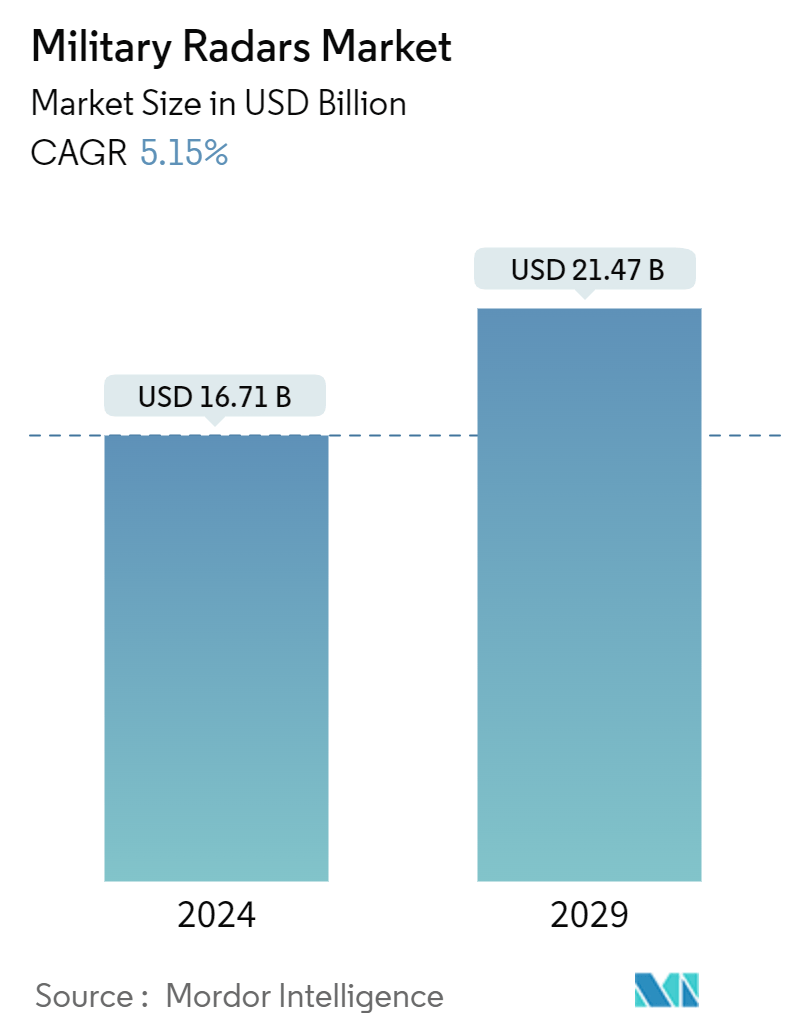

| Market Size (2024) | USD 16.71 Billion |

| Market Size (2029) | USD 21.47 Billion |

| CAGR (2024 - 2029) | 5.15 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Military Radars Market Analysis

The Military Radars Market size is estimated at USD 16.71 billion in 2024, and is expected to reach USD 21.47 billion by 2029, growing at a CAGR of 5.15% during the forecast period (2024-2029).

Radars are widely used in military applications for surveillance, navigation, weapon guidance, airspace monitoring, and other purposes. The demand for coherent radar in the military is expected to grow in the coming years due to the rise in terrorism and geopolitical tensions in certain geographies, such as the Middle East and Asia-Pacific.

A constant pursuit of technological superiority for defense and surveillance purposes characterizes radars for the military. The need for advanced threat detection, tracking, and target identification capabilities drives demand in this segment. With their rapid beam steering and high accuracy, phased array radars are increasingly prevalent in military applications. Trends in the military radar market include the integration of artificial intelligence (AI) for real-time threat analysis and decision-making. Stealth technology influences radar development, emphasizing reducing radar cross-sections to evade enemy detection.

However, the military radar systems market also faces some challenges, such as the high cost and complexity of radar systems, regulatory and environmental issues, vulnerability to jamming and spoofing, and competition from alternative technologies, such as lidar and sonar. Therefore, the market players must invest in research and development, innovation, and collaboration to overcome these challenges and gain a competitive edge.

Military Radars Industry Segmentation

Armed forces use military radars for surveillance, locating targets, tracking their movements, and directing other weapons or countermeasures against them. Military radars are also used for navigation and tracking weather changes. The study includes radars used by the navy (coastal radars and ship-based radars), air force (weather navigation radar, airborne radar, and precision approach radar), and army (perimeter surveillance radars, long-range surveillance radars, and fixed and movable land radars), as well as in space applications. The other applications include IED detection, airspace monitoring, traffic management, and weather monitoring.

The military radar systems market is segmented by platform, application, components, and geography. By platform, it is segmented into ground-based, naval, airborne, and space. By application, the market is classified into air and missile defense, intelligence, surveillance, and reconnaissance (ISR), navigation and weapon guidance, space situational awareness, and other applications. Based on components, the market is segmented into antennas, transmitters, receivers, power amplifiers, duplexers, digital signal processors, stabilization systems, and graphical user interfaces. The report also covers the market sizes and forecasts for the military radar systems market in major countries across different regions. For each segment, the market size and forecast are provided in terms of value (USD).

| Platform | |

| Ground-based | |

| Naval | |

| Airborne | |

| Space |

| Application | |

| Air and Missile Defense | |

| Intelligence, Surveillance, and Reconnaissance (ISR) | |

| Navigation and Weapon Guidance | |

| Space Situational Awareness | |

| Other Applications |

| Component | |

| Antennas | |

| Transmitters | |

| Receivers | |

| Power Amplifiers | |

| Duplexers | |

| Digital Signal Processors | |

| Stabilization Systems | |

| Graphical User Interfaces |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Military Radars Market Size Summary

The military radar systems market is poised for significant growth, driven by the increasing demand for advanced surveillance, navigation, and threat detection capabilities. This demand is fueled by rising geopolitical tensions and the need for technological superiority in defense applications. Phased array radars, known for their rapid beam steering and high accuracy, are becoming more prevalent. The integration of artificial intelligence for real-time threat analysis and decision-making is a notable trend, alongside the development of stealth technologies aimed at reducing radar cross-sections. However, the market faces challenges such as high costs, regulatory issues, and competition from alternative technologies like lidar and sonar. To maintain a competitive edge, market players are focusing on research, innovation, and collaboration.

The market is characterized by substantial investments from countries like the United States, China, India, and Russia, which are modernizing their air fleets and enhancing defense capabilities. Collaborative efforts in Europe, such as the Future Combat Air System program, highlight the focus on developing next-generation stealth fighter jets. North America, particularly the United States, is a key player due to its significant military spending and active procurement of advanced radar systems. Leading defense technology firms are investing in sophisticated radar systems, including AESA and 3D radars, to meet the evolving demands of modern warfare. The market's competitive landscape is shaped by major players like Lockheed Martin, Northrop Grumman, and RTX Corporation, who are focusing on developing radar systems capable of detecting stealthy targets.

Military Radars Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.3 Market Restraints

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Buyers/Consumers

-

1.4.2 Bargaining Power of Suppliers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Platform

-

2.1.1 Ground-based

-

2.1.2 Naval

-

2.1.3 Airborne

-

2.1.4 Space

-

-

2.2 Application

-

2.2.1 Air and Missile Defense

-

2.2.2 Intelligence, Surveillance, and Reconnaissance (ISR)

-

2.2.3 Navigation and Weapon Guidance

-

2.2.4 Space Situational Awareness

-

2.2.5 Other Applications

-

-

2.3 Component

-

2.3.1 Antennas

-

2.3.2 Transmitters

-

2.3.3 Receivers

-

2.3.4 Power Amplifiers

-

2.3.5 Duplexers

-

2.3.6 Digital Signal Processors

-

2.3.7 Stabilization Systems

-

2.3.8 Graphical User Interfaces

-

-

2.4 Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

-

2.4.2 Europe

-

2.4.2.1 United Kingdom

-

2.4.2.2 Germany

-

2.4.2.3 France

-

2.4.2.4 Russia

-

2.4.2.5 Rest of Europe

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 India

-

2.4.3.3 Japan

-

2.4.3.4 South Korea

-

2.4.3.5 Rest of Asia-Pacific

-

-

2.4.4 Latin America

-

2.4.4.1 Brazil

-

2.4.4.2 Rest of Latin America

-

-

2.4.5 Middle East and Africa

-

2.4.5.1 United Arab Emirates

-

2.4.5.2 Saudi Arabia

-

2.4.5.3 Egypt

-

2.4.5.4 Rest of Middle East and Africa

-

-

-

Military Radars Market Size FAQs

How big is the Military Radars Market?

The Military Radars Market size is expected to reach USD 16.71 billion in 2024 and grow at a CAGR of 5.15% to reach USD 21.47 billion by 2029.

What is the current Military Radars Market size?

In 2024, the Military Radars Market size is expected to reach USD 16.71 billion.