Military Truck Market Size

| Study Period | 2019-2029 |

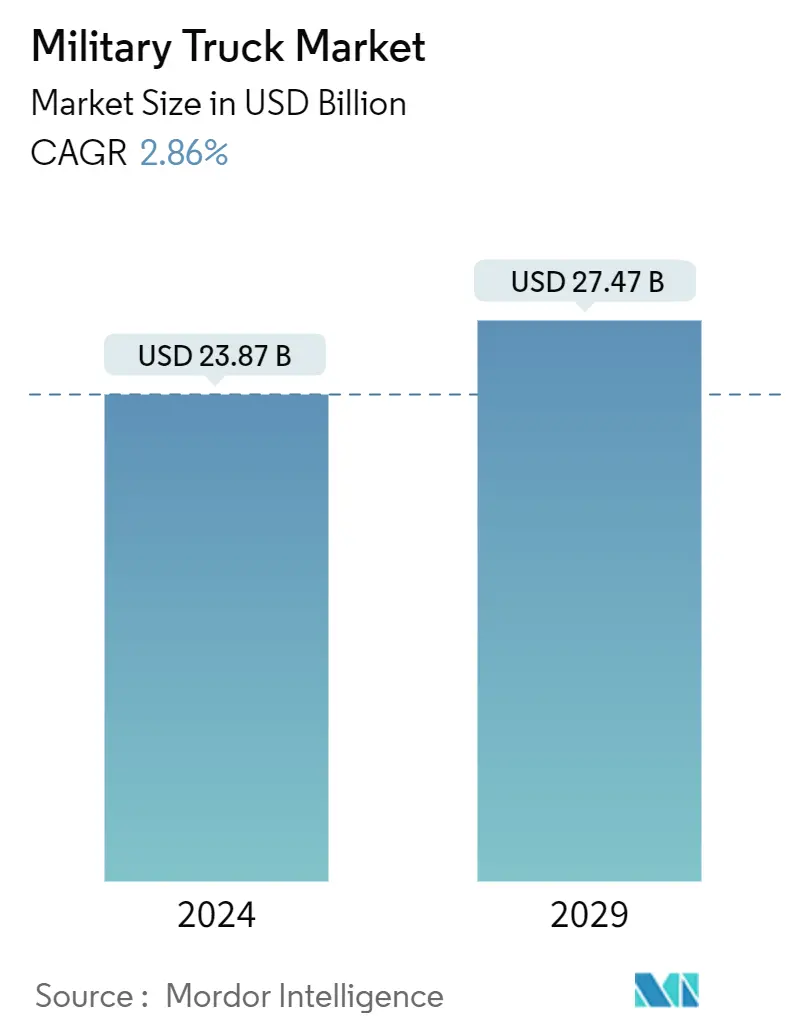

| Market Size (2024) | USD 23.87 Billion |

| Market Size (2029) | USD 27.47 Billion |

| CAGR (2024 - 2029) | 2.86 % |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Military Truck Market Analysis

The Military Truck Market size is estimated at USD 23.87 billion in 2024, and is expected to reach USD 27.47 billion by 2029, growing at a CAGR of 2.86% during the forecast period (2024-2029).

The increasing deployment of military units in different locations and growing military missions are increasing the demand for moving troops and supplies, hauling equipment to those areas, and recovering vehicles and weapon systems during such missions, which is driving the growth of the market.

Growing military budgets have aided the growth of the market. Several emerging countries have increased their budget spending towards military transportation and logistics which is expected to drive the growth of the military truck market during the forecast period.

The military truck market faces several challenges. One of the major challenges is the ability to maintain performance, payload, and mobility while dealing with the increasing weight associated with armor and sophisticated systems. Additionally, manufacturers must address the need for increased fuel efficiency, which can be difficult to achieve with heavy-duty vehicles. Budgetary restrictions and the long procurement periods associated with military procurement can create uncertainty for manufacturers and customers. These challenges require continuous adaptation and innovation within the industry.

Military Truck Market Trends

Heavy Military Trucks Accounted For the Largest Share of the Market

The most important characteristics of military logistics trucks are dependability, high transport efficiency, tactical mobility, and protection. Heavy trucks are capable of traversing virtually any terrain, including deep snow off-road and soft wet terrain. With a maximum payload capacity of approximately 1 ton, these trucks are capable of tow weight of approximately 3 tons.

The growing military budgets globally have led to the acquisition of various types of military hardware. In this context, the heavy military trucks, play a crucial role as the main carrier for several types of weapons, sensors and communication platforms which has aided their procurement. For instance, in May 2023 the Defense Resources Agency of Lithuania forged an agreement with the German truck manufacturer Daimler Trucks for the purchase of 230 vehicles, including Arocs, and 141 vehicles, including Zetros. The total value of the contract is estimated to be around EUR 216 million (USD 236 million). The new contract is intended to strengthen the defense forces of the armed forces of Lithuania. The service procured specialised Arocs vehicles with all the required parts and Zetros vehicles with cranes. The delivery of the trucks is planned to take place in the years 2023 to 2030. Thus, growing spending on defense sector and rising procurement of military trucks drive the market growth in coming years.

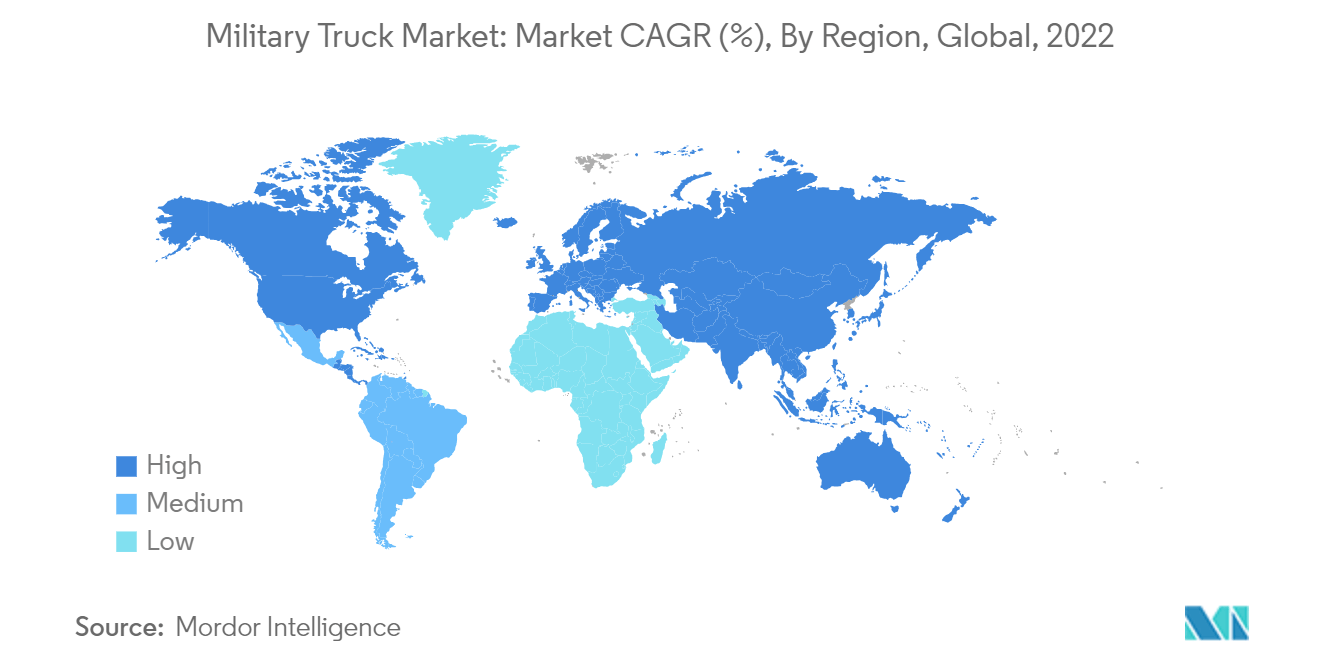

North America is Anticipated to Dominate the Market During the Forecast Period

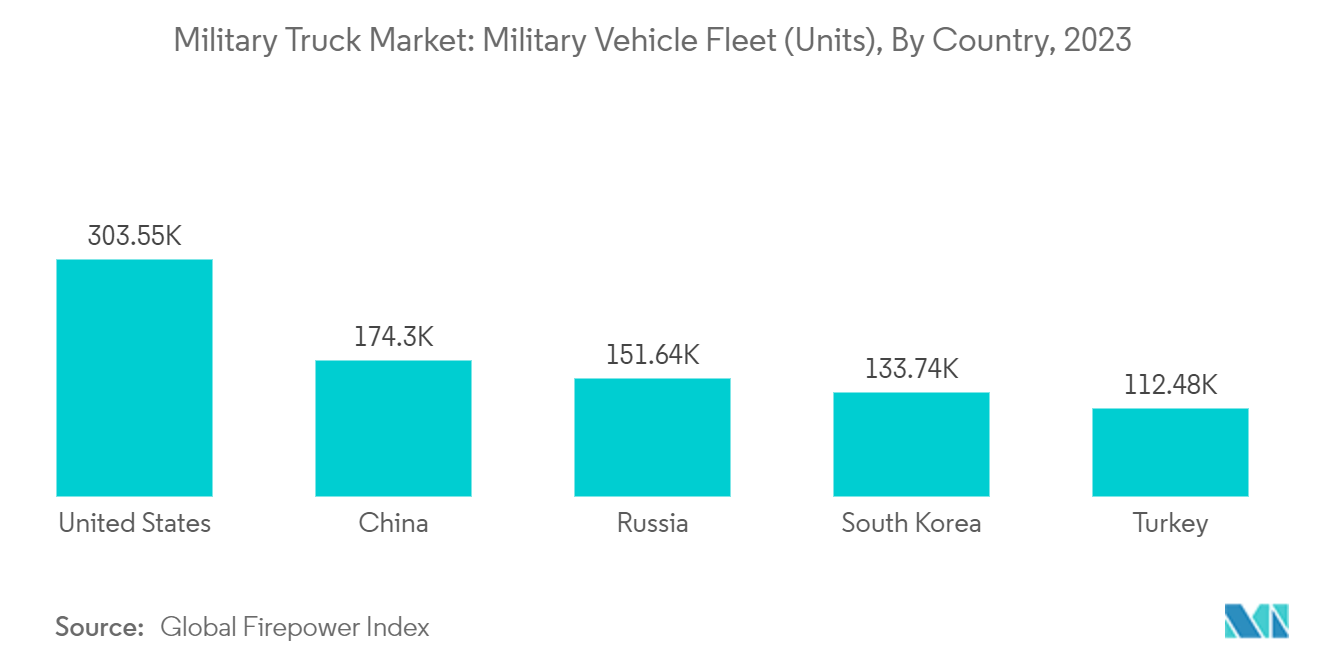

North America held the largest share in the military truck market and continue its domination during the forecast period. The main reason for the higher revenue share of the region is the high demand for military transportation systems from the US. In 2022, the US Army maintained both its regular and reserve personnel strength at approximately the same level as in 2021. The Army’s 2022 staffing targets were 485,000 for the regular Army 336,000 for the National Guard and 189,500 for the Army Reserve. Additonally, the deployment of US troops in various regions of the world, due to the US engaging in various global conflicts, is one of the major factors driving the growth of revenues from the region. These military camps and command units demand continuous land-based logistics and unit resupply missions, due to which the country is procuring military trucks on a large scale. Since February 2022, the US Department of Defense (DoD) has deployed or redeployed more than 20,000 additional troops to Europe in the wake of the Ukraine crisis.

Innovation is also a prime driver of market growth as manufacturers are consistently investing towards the R&D of advanced military trucks to enhance the level of safety and capabilities of the current generation. For instance, in January 2023, the US Army selected four companies to build new tactical truck prototypes. Mack Defense, Navistar Defense, Oshkosh Defense, and a team made up of American Rheinmetall Vehicles and GM Defense will build prototypes for a Common Tactical Truck after the US Army awarded them deals worth a cumulative USD 24.3 million. Such contracts are envisioned to bolster the market prospects for the region during the forecast period.

Military Truck Industry Overview

The military trucks market is semi-consolidated in nature with a presence of few local and global players holding significant shares in the market. Oshkosh Corporation, Rheinmetall AG, Mercedes-Benz Group AG, Tata Motors Ltd., and Krauss-Maffei Wegmann GmbH & Co. KG. are prominent players in the market. The manufacturers of military trucks are continually looking for ways to develop newer generation trucks keeping in mind the rules and regulations set by the various defense authorities worldwide. Players are focusing on enhancing the protection of their trucks, using newer designs and advancements in material technologies, which will help them gain new contracts from the militaries and expand their market share during the forecast period.

Military Truck Market Leaders

-

Rheinmetall AG

-

Oshkosh Corporation

-

Krauss-Maffei Wegmann GmbH & Co. KG.

-

Tata Motors Ltd

-

Mercedes-Benz Group AG

*Disclaimer: Major Players sorted in no particular order

Military Truck Market News

In October 2023, Estonia and Latvia signed a framework agreement for USD 730.5 million for the supply of military vehicles to three mobility developers. As per the agreement, the companies will supply up to 3.000 vehicles, over seven years. Veho will supply vehicles up to 5 tons, while systems of more than 5 tons will be delivered by Volvo Eesti and Scania Eesti.

In May 2023, the German military placed an order for a further 57 HX81 (unprotected heavy-duty truck) heavy military trucks, valued at USD 534 million. The order is the latest in a series of 7-year framework agreements signed with the German military in 2018 for a total of up to 137 new HX81 trucks.

Military Truck Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Application

5.1.1 Cargo Logistics

5.1.2 Troop Transport

5.1.3 Other Applications

5.2 Weight Class

5.2.1 Light

5.2.2 Medium

5.2.3 Heavy

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.2 Europe

5.3.2.1 United Kingdom

5.3.2.2 Germany

5.3.2.3 France

5.3.2.4 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Rest of Asia-Pacific

5.3.4 Rest of the World

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles

6.2.1 Oshkosh Corporation

6.2.2 Rheinmetall AG

6.2.3 Mercedes-Benz Group AG

6.2.4 Volkswagen AG

6.2.5 Krauss-Maffei Wegmann GmbH & Co. KG.

6.2.6 IVECO S.p.A.

6.2.7 Renault Trucks

6.2.8 Ashok Leyland

6.2.9 Tata Motors Ltd

6.2.10 Scania

6.2.11 Arquus

6.2.12 KAMAZ PTC

6.2.13 KrAZ

6.2.14 MITSUBISHI HEAVY INDUSTRIES, LTD.

6.2.15 Dongfeng Motor Corporation

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Military Truck Industry Segmentation

Military trucks are designed to carry personnel, equipment and supplies to support operations. Operations in difficult and hazardous environments necessitate the integration of cutting-edge capabilities and technologies in vehicles.

The military truck market is segmented based on application, weight class, and geography. By application, the market is segmented into cargo logistics, troop transport and other applications. The other applications includes utility, and search and rescue, etc.. By weight class, the market is divided into light, medium and heavy trucks. The report also covers the market sizes and forecasts for the military truck market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Application | |

| Cargo Logistics | |

| Troop Transport | |

| Other Applications |

| Weight Class | |

| Light | |

| Medium | |

| Heavy |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| Rest of the World |

Military Truck Market Research FAQs

How big is the Military Truck Market?

The Military Truck Market size is expected to reach USD 23.87 billion in 2024 and grow at a CAGR of 2.86% to reach USD 27.47 billion by 2029.

What is the current Military Truck Market size?

In 2024, the Military Truck Market size is expected to reach USD 23.87 billion.

Who are the key players in Military Truck Market?

Rheinmetall AG, Oshkosh Corporation, Krauss-Maffei Wegmann GmbH & Co. KG., Tata Motors Ltd and Mercedes-Benz Group AG are the major companies operating in the Military Truck Market.

Which is the fastest growing region in Military Truck Market?

North America is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Military Truck Market?

In 2024, the North America accounts for the largest market share in Military Truck Market.

What years does this Military Truck Market cover, and what was the market size in 2023?

In 2023, the Military Truck Market size was estimated at USD 23.19 billion. The report covers the Military Truck Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Military Truck Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Military Truck Industry Report

Statistics for the 2024 Military Truck market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Military Truck analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.