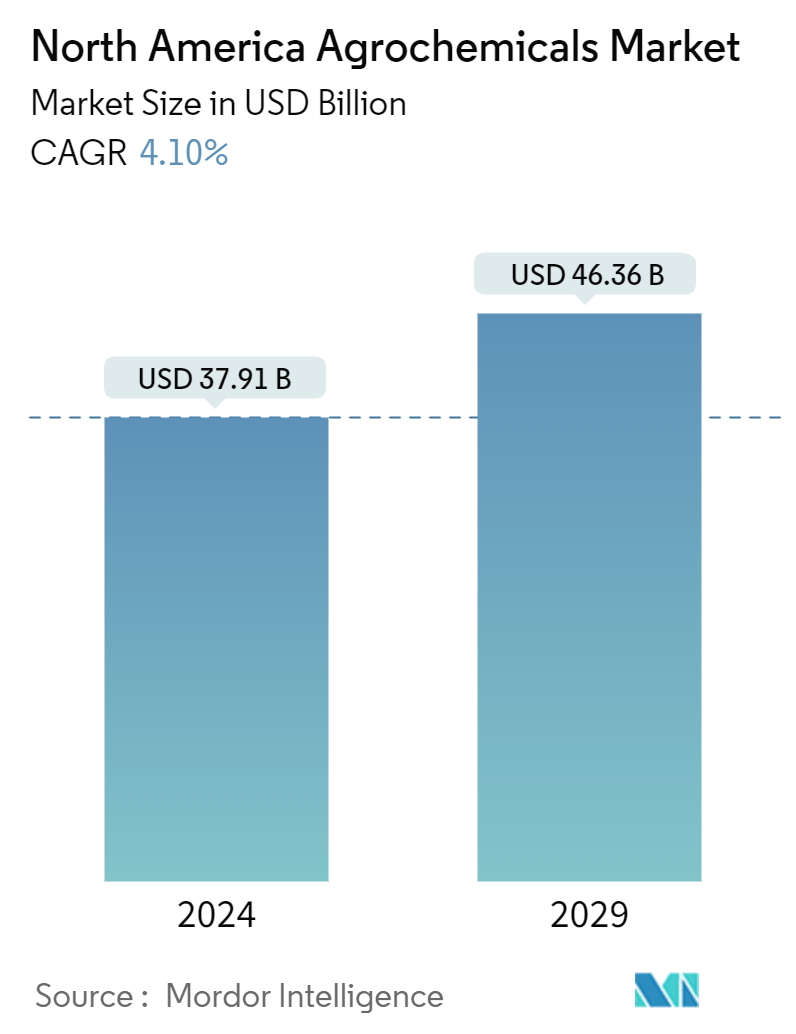

North America Agrochemicals Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 37.91 Billion |

| Market Size (2029) | USD 46.36 Billion |

| CAGR (2024 - 2029) | 4.10 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Agrochemicals Market Analysis

The North America Agrochemicals Market size is estimated at USD 37.91 billion in 2024, and is expected to reach USD 46.36 billion by 2029, growing at a CAGR of 4.10% during the forecast period (2024-2029).

- Over the years, the agrochemical market in North America has undergone significant transformations, marked by robust growth, evolving crop mix trends, and stringent environmental regulations. As a result, there is a heightened emphasis on judiciously utilizing optimal chemicals while minimizing their environmental impact. Regulations are pivotal in shaping this market. The agrochemical market is witnessing a steady emergence of price premiums and innovative, eco-friendly production methods.

- The main focus of the agriculture sector is to increase productivity and food security in the region. However, the region’s agricultural area has seen significant fluctuations over the years compared to neighboring regional economies. The growing population in the United States is leading to a decline in the proportion of arable land, which is primarily used to produce food. This is pushing crop cultivation under poor soil profiles. As per FAOSTAT data, the area under cereals decreased from 54,729,333 hectares in 2021 to 50,911,502 hectares in 2022. Therefore, the use of agrochemicals is the highest for cereals and grains as soil nutrient deficiencies can lead to decreased yield and less bio-available nutrients in crops such as rice.

- The US fertilizer market is mature in terms of N, P, and K fertilizer consumption. The demand for nitrogen fertilizers is the highest among inorganic fertilizers. The demand for potassic and phosphatic fertilizers is increasing at a steady pace, owing to the shift of farmers toward maize cultivation rather than soybeans. Several initiatives have been taken by the US government to encourage farmers to use fertilizers. For instance, in 2022, the US Department of Agriculture (USDA) announced USD 500 million in grants to increase American fertilizer production to spur competition and combat price hikes on US farmers caused by the Russia-Ukraine War.

North America Agrochemicals Market Trends

Fertilizers Constitute the Most Significant Sub-segment Under Type

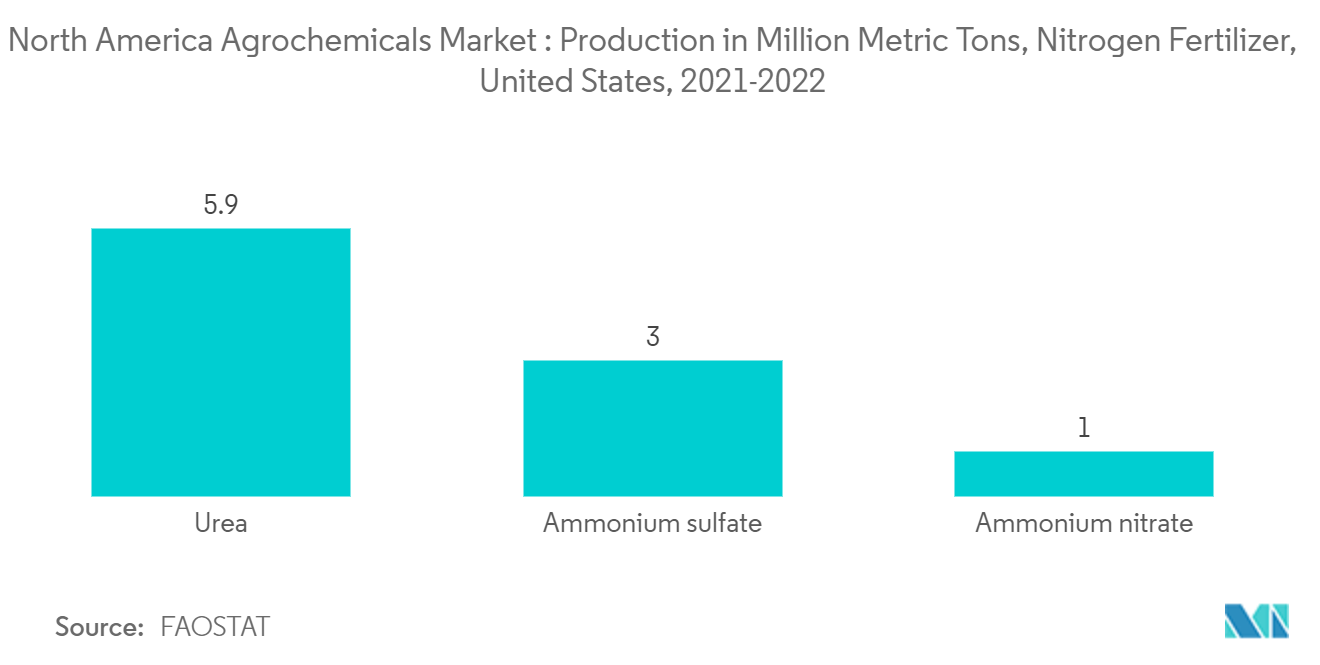

North America is one of the leading regions in the manufacturing and marketing of almost all types of fertilizers worldwide. The United States and Canada are the largest producers in the region. Technical and scientific advancements have made the application of fertilizers more efficient in recent years and helped farmers maximize fertilizers’ benefits while reducing risks. Nitrogenous fertilizers are the most important fertilizers in agricultural production in the United States. According to the Fertilizer Institute report, the United States is one of the world’s fourth-largest producers of nitrogen fertilizers. As per FAO statistics, the United States produced 5.9 million metric tons of urea, 1.0 million metric tons of ammonium nitrate (AN), and 3.0 million metric tons of ammonium sulfate in 2022.

Canada is the third-largest producer of primary fertilizers (N, P, and K) globally, supported by the country's potash and nitrogen production capacities. As per the Canadian government’s statistics, Canada’s 10 active mines in Saskatchewan produced an estimated 24.6 million metric tons of potash in 2022, an increase of 1.3 million metric tons from 2021. Moreover, Canada is also the world’s largest exporter of potash. In 2022, Canada exported 21.2 million metric tons of potash, accounting for 39% of the world’s total exports. Canadian fertilizer is traded with over 75 countries, representing 2% of total Canadian exports.

The US Department of Agriculture reported that wheat, corn, soybean, and cotton accounted for approximately 60% of nitrogen, phosphate, and potash fertilizers in the previous year. Corn and wheat stood out as the primary cereals, receiving a significant share of NPK fertilizers. ITC Trade Map statistics revealed that North America's corn exports surged from USD 51,910.3 million in 2021 to USD 53,068.5 million in 2023. This uptick in corn exports increased the use of fertilizers, owing to the need to boost yields from the same area.

The United States Dominates the Market

The United States is one of the most dominant players in the agrochemicals market. According to a study conducted by the US Department of Agriculture and Environmental Protection Agency (EPA), chlorpyrifos and acephate are the most commonly used pesticide active ingredients in the country's agriculture sector. Currently, corn, soybeans, wheat, and cotton account for the most use of agrochemicals in the market. As reported by FAO, soybean yield increased from 31.88 thousand hectares in 2019 to 33.31 thousand hectares in 2022. This increase in yield indicates the rise in the country's use of agrochemicals.

According to statistics from the World Bank, the agricultural land in the United States remained constant at 44.4% from 2019 to 2021. Urbanization and industrialization are the major reasons for restricting the expansion of agricultural land in the United States. There is little scope for arable land expansion in the coming years. According to the American Farmland Trust (AFT), in the past 20 years, the United States has converted around 31 million acres of agricultural land into commercial, residential, and industrial areas. However, farmers in the region are applying fertilizers to increase their crop yield and feed the growing population.

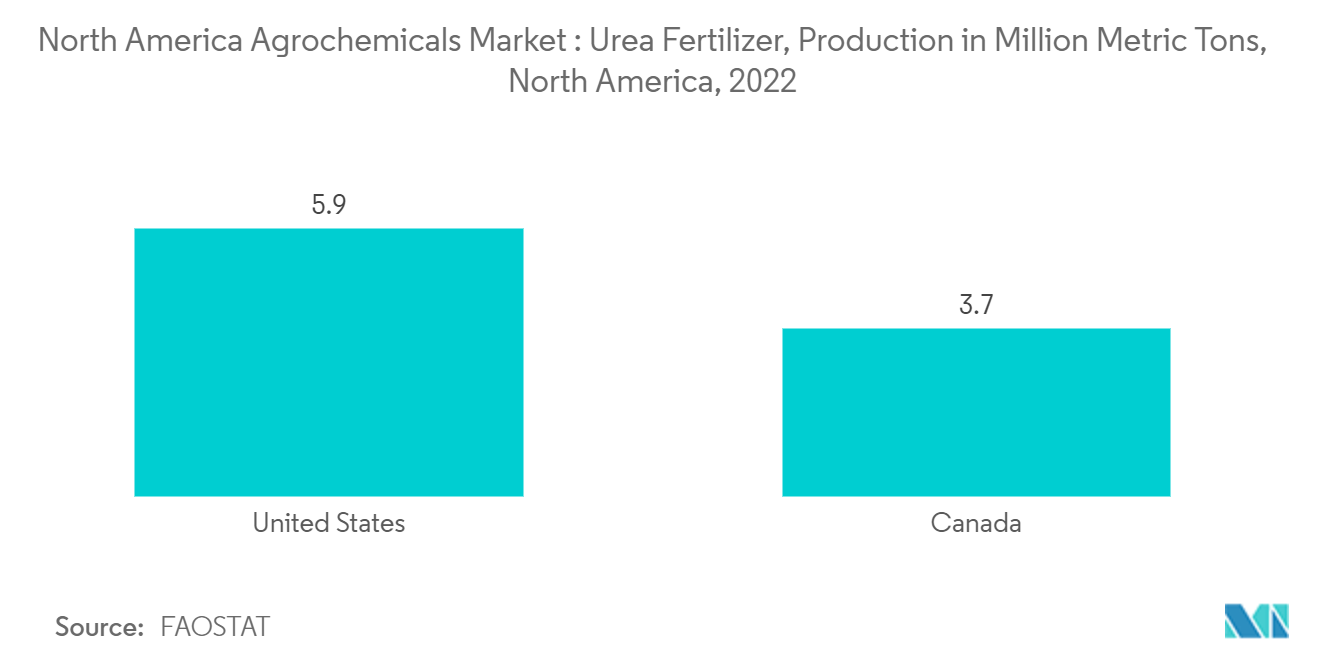

The United States is one of the largest exporters of nitrogen fertilizers, which makes it an attractive investment destination. Urea, calcium ammonium nitrate (CAN), ammonium nitrate, and ammonium sulfate are the major nitrogen fertilizers in the country; urea is the most significant among them. For instance, as per FAO statistics, the United States produced 5.2 million metric tons of urea fertilizer in 2021, which increased by 5.9 million metric tons in 2022.

Major players in the country are undergoing strategic product launches to expand their product portfolio. For instance, in 2021, Corteva AgriScience launched the DuraCor herbicide for pastures and rangeland in the United States. DuraCor is expected to control more than 140 broadleaf weed species, as well as offer several anticipated features, such as low use rate and low odor formation.

North America Agrochemicals Industry Overview

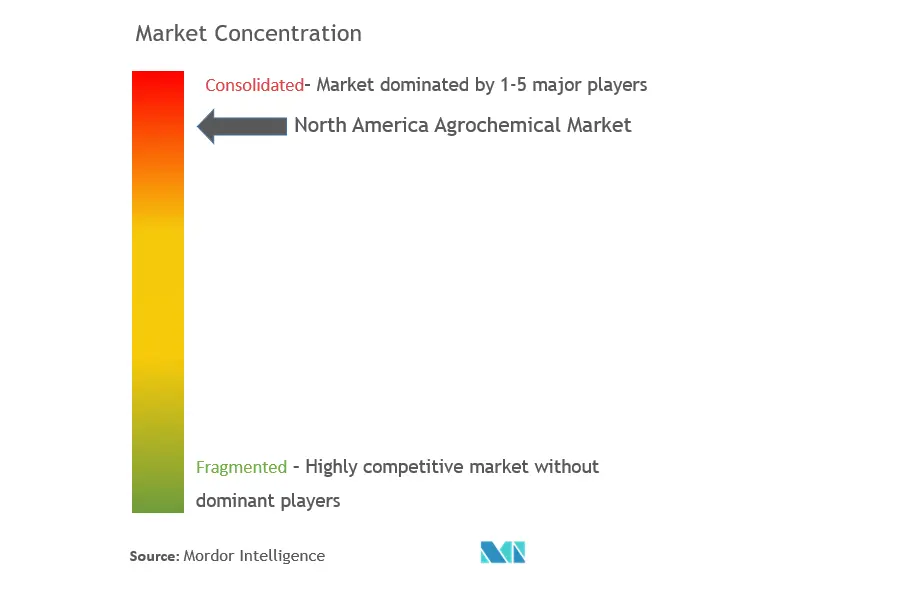

The North American agrochemical market is highly consolidated, with the major players accounting for major shares in 2023. Companies such as Archer Daniels Midland Company (ADM), BASF SE, Bayer CropScience AG, Syngenta AG, Yara International ASA, Corteva Agriscience, and FMC Corporation are the major players in the market. These players compete to maintain a consistent share of the market through various strategies such as mergers and acquisitions, partnerships, expansions, and product launches.

North America Agrochemicals Market Leaders

-

Bayer AG

-

Corteva Agriscience

-

BASF SE

-

Archer Daniels Midland Company (ADM)

-

Yara International ASA

*Disclaimer: Major Players sorted in no particular order

North America Agrochemicals Market News

- July 2023: ADAMA introduced Davai A Plus and Clearfield Broad-Spectrum Herbicide Solutions for imidazolinone-tolerant legumes like lentils, peas, and soybeans.

- April 2023: Nufarm launched a new liquid formulation fungicide, Tourney EZ, exclusively for turf and ornamental crops based on customer demand, which strengthened the company's role in turf and ornamental crop protection.

- January 2023: ICL entered into a strategic partnership agreement with General Mills to be the supplier of strategic specialty phosphate solutions to General Mills. The long-term agreement focuses on international expansion.

North America Agrochemicals Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rapid Adoption of Bio-Based Agrochemicals

4.2.2 Adoption of Sustainable Farming Technologies

4.2.3 Need for Increased Land Productivity

4.3 Market Restraints

4.3.1 Stringent Regulations on Agrochemical Usage

4.3.2 High Costs Associated and Difficulty with New Molecule Development

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Threat of Substitute Products

4.4.4 Threat of New Entrants

4.4.5 Intensity Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Type

5.1.1 Fertilizers

5.1.2 Pesticides

5.1.3 Adjuvants

5.1.4 Plant Growth Regulators

5.2 Application

5.2.1 Grains and Cereals

5.2.2 Pulses and Oilseeds

5.2.3 Fruits and Vegetables

5.2.4 Turf and Ornamentals

5.2.5 Other Applications

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.1.4 Rest of North America

6. COMPETITIVE LANDSCAPE

6.1 Most Adopted Strategies

6.2 Market Share Analysis

6.3 Company Profiles

6.3.1 UPL Limited

6.3.2 Bayer Cropscience AG

6.3.3 BASF SE

6.3.4 Corteva Agriscience

6.3.5 Archer Daniels Midland Company (ADM)

6.3.6 FMC Corporation

6.3.7 Adama Agricultural Solutions

6.3.8 Gowan Company

6.3.9 Nufarm Ltd

6.3.10 Syngenta AG

6.3.11 Yara International ASA

7. MARKET OPPORTUNITIES AND FUTURE TREND

North America Agrochemicals Industry Segmentation

According to the OECD, agrochemicals are commercially produced, usually chemical, bio-based compounds used in farming, such as fertilizers, pesticides, or soil conditioners.

The North American agrochemicals market is segmented by type (fertilizers, pesticides, adjuvants, and plant growth regulators), application (grains and cereals, pulses and oilseeds, fruits and vegetables, turfs and ornamentals, and other applications), and geography (United States, Canada, Mexico, and Rest of North America). The report offers market estimation and forecasts in value (USD) for all the above-mentioned segments.

| Type | |

| Fertilizers | |

| Pesticides | |

| Adjuvants | |

| Plant Growth Regulators |

| Application | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Fruits and Vegetables | |

| Turf and Ornamentals | |

| Other Applications |

| Geography | ||||||

|

North America Agrochemicals Market Research FAQs

How big is the North America Agrochemicals Market?

The North America Agrochemicals Market size is expected to reach USD 37.91 billion in 2024 and grow at a CAGR of 4.10% to reach USD 46.36 billion by 2029.

What is the current North America Agrochemicals Market size?

In 2024, the North America Agrochemicals Market size is expected to reach USD 37.91 billion.

Who are the key players in North America Agrochemicals Market?

Bayer AG, Corteva Agriscience, BASF SE, Archer Daniels Midland Company (ADM) and Yara International ASA are the major companies operating in the North America Agrochemicals Market.

What years does this North America Agrochemicals Market cover, and what was the market size in 2023?

In 2023, the North America Agrochemicals Market size was estimated at USD 36.36 billion. The report covers the North America Agrochemicals Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the North America Agrochemicals Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

North America Agrochemical Industry Report

Statistics for the 2024 North America Agrochemical market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. North America Agrochemical analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.