North America Flexible Plastic Packaging Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

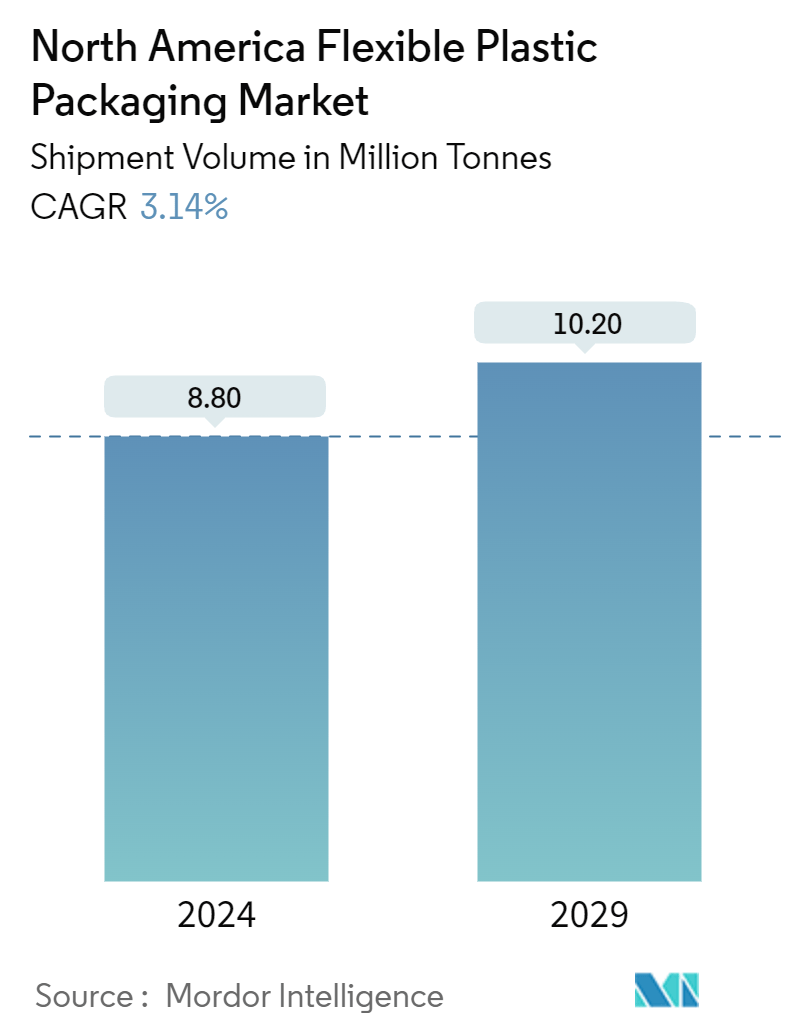

| Market Volume (2024) | 8.80 Million tonnes |

| Market Volume (2029) | 10.20 Million tonnes |

| CAGR (2024 - 2029) | 3.14 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Flexible Plastic Packaging Market Analysis

The North America Flexible Plastic Packaging Market size in terms of shipment volume is expected to grow from 8.80 Million tonnes in 2024 to 10.20 Million tonnes by 2029, at a CAGR of 3.14% during the forecast period (2024-2029).

- The demand for flexible plastic packaging is rising, driven by a surge in consumer products like food, beverages, and cosmetics. This uptick is mainly due to the convenience and portability offered by modern packaging solutions. As urban lifestyles evolve, consumers increasingly favor packaging that's not just lightweight but also easy to use. In response, vendors are innovating, ensuring their packaging remains competitive in the shifting landscape of organized retail.

- There's a growing push to infuse technology into packaging, spurred by the need for better barrier qualities, product innovation, and the digitization of supply chains. The region's food ingredients market is flourishing, propelled by a booming food and beverage industry, a rising appetite for dairy products, and a heightened demand for processed and packaged foods. Flexible plastic packaging emerges as the go-to choice, especially as the need for portable and convenient food packaging escalates across industries.

- Highlighting the trend, the US Census Bureau reported that between April and June 2023, retail e-commerce sales in the United States reached nearly USD 277.6 billion, a significant uptick from the previous quarter. This surge in e-commerce sales is nudging regional players in flexible plastic packaging to innovate and expand their market reach to meet diverse customer needs.

- As the consumption of confectionaries and sweets rises, flexible plastic packaging firms are tailoring their products to this niche, boosting sales. For instance, data from the United States Census Bureau projects that the confectionery industry's revenue in the United States could hit USD 10.89 billion by FY 2023.

- Industry players actively invest in new product development to meet customer demands. For instance, in August 2023, TC Transcontinental Packaging announced a hefty USD 60 million investment. This funding is earmarked for cutting-edge mono-material recyclable flexible plastic packaging solutions featuring high-performance polyethylene films with enhanced heat resistance. The investment also includes a groundbreaking film line that will produce biaxially oriented polyethylene (BOPE), a first in North America, and a significant expansion of TC Transcontinental Packaging's Spartanburg, South Carolina facility.

- As sustainability takes center stage, manufacturers in the flexible plastic packaging and consumer packaged goods (CPG) sectors are pivoting toward eco-friendly options. These include incorporating post-consumer recycled (PCR) content, utilizing biodegradable materials, transitioning from multi-layer to mono-material structures, and substituting plastic with paper. While these changes are laudable, they pose operational challenges, especially in transitioning between different flexible materials.

North America Flexible Plastic Packaging Market Trends

Innovative Packaging Solutions are Driving the Market’s Growth due to the Demand from Frozen-Food Categories

- High demand from frozen food categories is spurring innovation in packaging design. This innovation aims to meet specific requirements, including maintaining product freshness, enhancing shelf appeal, and ensuring ease of use. Manufacturers are increasingly investing in developing new types of flexible plastic packaging tailored to the unique needs of these food categories, thereby further fueling the growth of the flexible plastic packaging market.

- With its lightweight nature and resistance to chemicals and moisture, the polyethylene (PE) segment dominates the market in terms of volume. Polyethylene's versatility shines through in its ability to effectively package various items, from fruits and vegetables to meat and seafood. Notably, the United States stands out as one of the largest consumers of frozen foods, a trend set to boost North America's films and wraps segment significantly.

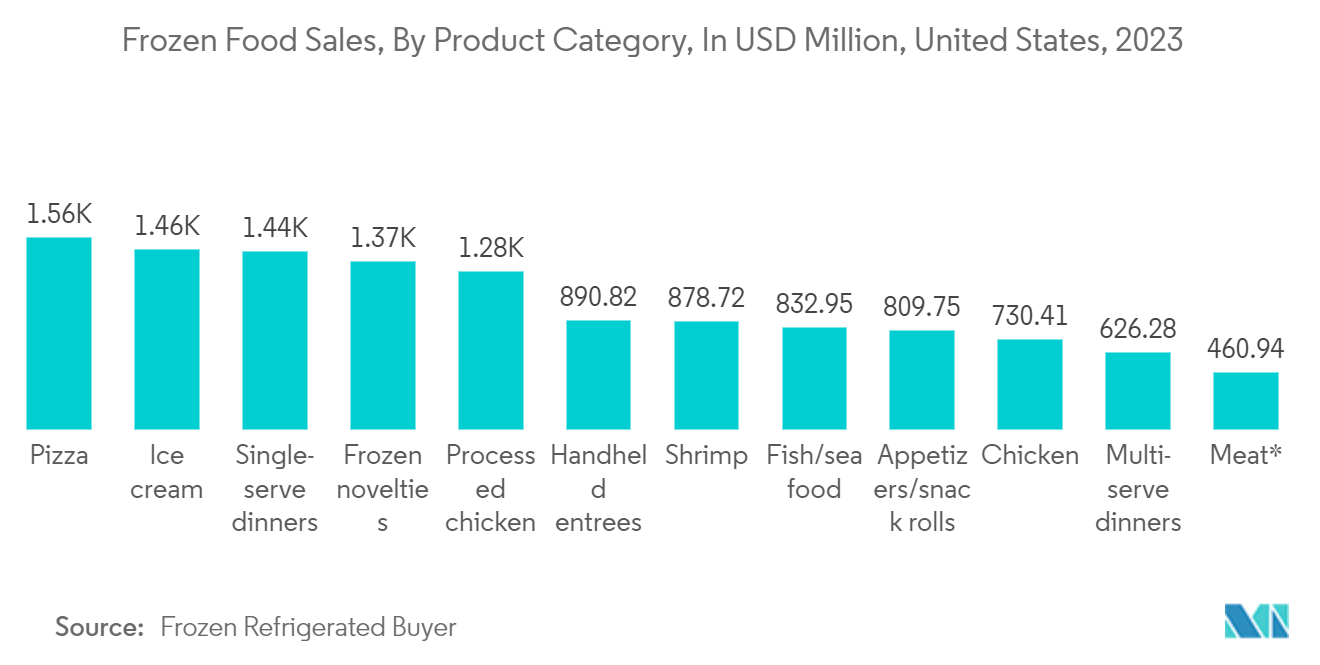

- Recent Frozen and Refrigerated Buyer data highlights the market's demand for frozen foods. In 2023, frozen appetizers and snack rolls accounted for USD 809.75 million, with pizza leading the pack at over USD 1.5 billion in sales. As these categories maintain their popularity, manufacturers are increasingly turning to flexible plastic packaging to meet the rising consumer demand. This surge in packaging needs is a crucial driver behind the flexible plastic packaging market's growth.

- For the 12 weeks that ended on January 1, 2023, private label sales of frozen meat in the United States hit approximately USD 211.74 million. During the same period, the Cooked Perfect frozen meat brand saw sales of around USD 31 million. With private labels and branded products vying for market share, manufacturers are pressured to differentiate their offerings. This push for differentiation is fueling the development of innovative packaging solutions tailored to frozen meat's unique demands, like enhanced freshness preservation and added consumer convenience features.

- Amid mounting environmental concerns and a rising demand for sustainability, manufacturers in the frozen food industry are pivoting toward recyclable packaging solutions. A case in point is the American Packaging Corporation, in February 2024, unveiled its RE Design for Recycle flexible packaging technology. This eco-friendly innovation specifically targets frozen food products, including fruits and vegetables. By adopting this technology, the company aims to replace its current non-recyclable multi-material laminate, aligning with its broader sustainability objectives.

Changing Consumer Preferences in Canada Aids the Market's Growth

- Consumer preferences are shifting toward user-friendly and compact packaging solutions, driving the Canadian flexible plastic packaging market. The country has witnessed a notable uptick in consuming single-serve snacks and convenience foods. Additionally, there's been a noteworthy increase in spending on ready-to-eat meals and beverages, particularly coffee and hot chocolate, often packaged in pouches.

- The convenience and portability of pouch packaging have propelled its popularity. Many consumers now favor flexible stand-up pouches for various products, including snacks, baby foods, sauces, and drinks. Companies in the region are increasingly turning to innovative packaging solutions, often through partnerships, to expand their product offerings nationwide. Notably, there's a rising demand for dehydrated foods, snacks, nuts, and bakery products, which heavily rely on flexible plastic packaging.

- According to StatCan's data from June 2023, Ontario led the pack with 81 frozen food manufacturing establishments, followed by Quebec, British Columbia, and Alberta, with 50, 33, and 25 establishments, respectively. Flexible plastic packaging has emerged as the go-to choice for frozen food manufacturers when shipping large quantities. Its lightweight nature and compact design, compared to rigid alternatives, not only make transportation easier but also contribute to cost savings and environmental benefits.

- With the continuous expansion of e-commerce platforms, the demand for plastic packaging in e-commerce supply chains has become paramount due to its durability and protective attributes. As e-commerce booms, investments are pouring into tailored packaging solutions that address the unique challenges of online retail. This surge in e-commerce is reshaping Canada's packaging landscape. With its reduced material usage and enhanced shipping efficiency, flexible plastic packaging is increasingly becoming the preferred option for e-commerce businesses aiming to streamline their logistics.

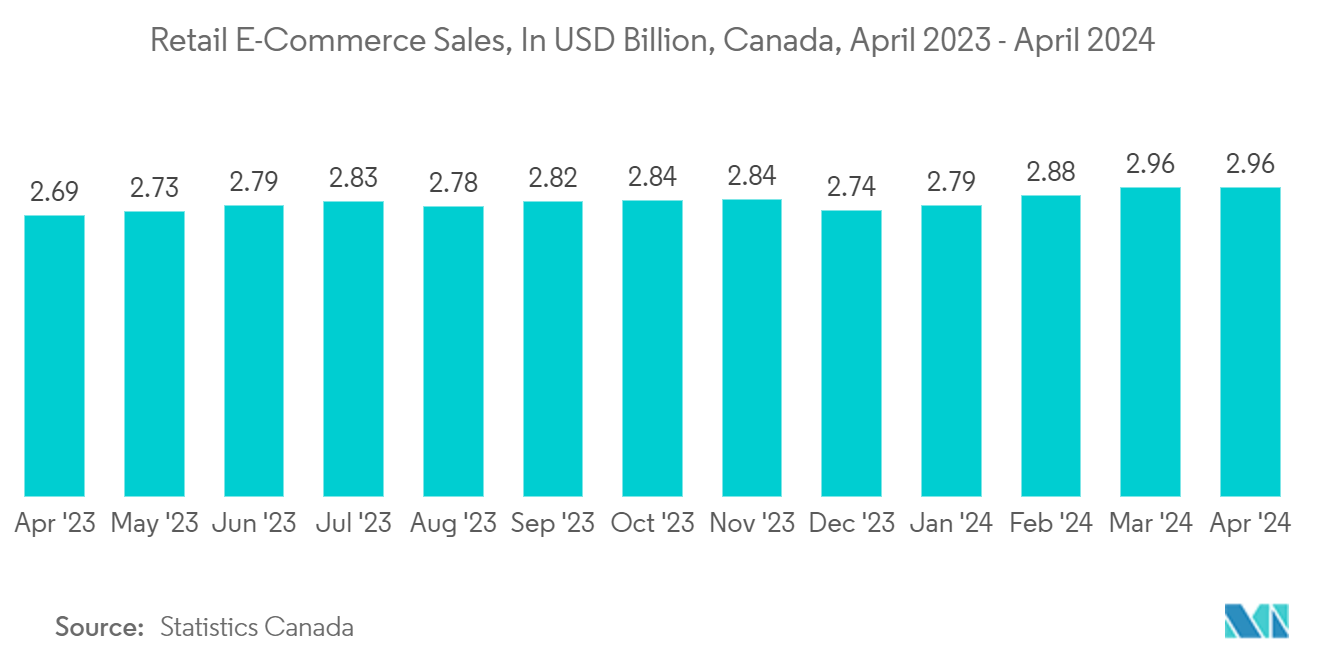

- Statistics Canada reported that Canada's retail e-commerce sales, which stood at CAD 3.78 billion (USD 2.88 billion) in August 2022, surged to CAD 3.99 billion (USD 2.959 billion) by April 2024, showcasing significant growth. Such a substantial uptick in e-commerce sales propels players in the flexible plastic packaging sector to innovate, introducing new products like pouches, bags, and films. It aims to meet diverse customer demands and expand its market presence.

- Several factors, including heightened consumer awareness of environmental concerns, evolving regulatory standards, and a growing emphasis on sustainability, propel packaging-waste recycling initiatives in Canada. The market is witnessing a surge in innovative recycling technologies, particularly in flexible packaging. Advances like enhanced sorting systems, chemical recovery processes, and efficient recycling methods significantly impact flexible packaging, reducing its environmental footprint and leading to a notable uptick in overall recycling rates.

- Highlighting the industry's commitment, in September 2023, the Canada Plastics Pact (CPP) unveiled a comprehensive five-year action plan to bolster the circular economy for flexible plastic packaging nationwide. This initiative, termed the 'flexible plastic packaging roadmap,' underscores an unprecedented collaboration across Canada's value chain. It emphasizes the collective effort required from all industry stakeholders to accelerate and scale solutions and achieve a circular economy by 2027.

North America Flexible Plastic Packaging Industry Overview

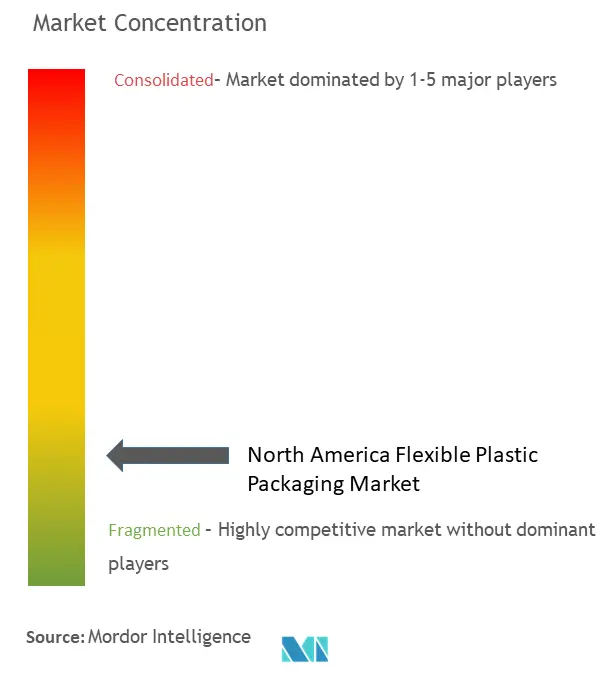

The North American flexible plastic packaging market is fragmented. Key players in the market are Berry Global Group, Proampac LLC, Novolex Holdings Inc., Sealed Air Corporation, Sonoco Products Company, American Packaging Corporation, Winpak Co. Limited, and Amcor Group GmbH. The players in the market are focusing on expanding their presence and addressing sustainability.

- February 2024: Berry Global Group announced the opening of a circular innovation and training center in Tulsa, Oklahoma, which will help the company accelerate the development of highly innovative products driven by superior materials science and engineering. This would help the company help its customers unpack complexities and understand the possibility of the flexible packaging market.

- October 2023: Winpak Films, Inc., a division of Winpak Co. Ltd, announced the expansion of the existing facility in Senoia to cater to the increasing demand in the country. With the growth strategy, the company focuses on providing the best packaging solutions for people and the planet.

North America Flexible Plastic Packaging Market Leaders

-

Berry Global Group

-

Novolex Holdings Inc.

-

Sonoco Products Company

-

Amcor Group GmbH

-

ProAmpac LLC

*Disclaimer: Major Players sorted in no particular order

North America Flexible Plastic Packaging Market News

- January 2024: ProAmpac LLC announced the collaboration with Aptar CSP Technologies to launch ProActive Intelligence Moisture Protect (MP-1000), which will eliminate the need for desiccant packets. It will help the company lower the moisture level in the packaging headspace, making it ideal for applications for products that require optimal moisture control.

- November 2023: NOVA Chemicals Corporation, a Canadian petrochemical company, notified the ink of a partnership with a key global packaging firm, Amcor Group GmbH, to supply mechanically recycled polyethylene resin (rPE) for manufacture in flexible packaging films by the latter. Increasing the use of recycled polyester (rPE) in flexible packaging is a key component of Amcor's circularity strategy. Such constant developments toward sustainability across the country would drive the demand for flexible plastic packaging across the region.

North America Flexible Plastic Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumption and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Expansion of the E-commerce Sector in the Region

5.1.2 Rising Demand for Barrier Packaging Solutions from the Food Industry

5.2 Market Restraints

5.2.1 Environmental Concerns over Plastic Waste and Regulatory Restrictions

6. TRADE SCENARIO

6.1 EXIM Data Based on Product Type and Plastic Resins

6.2 Trade Analysis (Top 5 Import-Export Countries, Price Analysis, and Key Ports, among others)

7. PRICING TREND ANALYSIS

7.1 Plastic Resins (Current Pricing and Historic Trends)

7.2 Product Type (Key Packaging Formats)

8. PACKAGING COST ANALYSIS

9. MARKET SEGMENTATION

9.1 By Material Type

9.1.1 Polyethene (PE)

9.1.2 Bi-oriented Polypropylene (BOPP)

9.1.3 Cast Polypropylene (CPP)

9.1.4 Polyvinyl Chloride (PVC)

9.1.5 Ethylene Vinyl Alcohol (EVOH)

9.1.6 Other Material Types (Polycarbonate, PHA, PLA, Acrylic, and ABS)

9.2 By Product Type

9.2.1 Pouches

9.2.2 Bags

9.2.3 Films and Wraps

9.2.4 Other Product Types (Blister Packs, Liners, etc.)

9.3 By End-user Industry

9.3.1 Food

9.3.1.1 Frozen Foods

9.3.1.2 Dry Foods

9.3.1.3 Meat, Poultry, and Sea Food

9.3.1.4 Candy & Confectionery

9.3.1.5 Pet Food

9.3.1.6 Fresh Produce

9.3.1.7 Dairy Products

9.3.1.8 Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)

9.3.2 Beverage

9.3.3 Personal Care and Household Care

9.3.4 Medical and Pharmaceutical

9.3.5 Other End user Industries ( Automotive, Chemical, Agriculture)

9.4 By Country

9.4.1 United States

9.4.2 Canada

10. COMPETITIVE LANDSCAPE

10.1 Company Profiles*

10.1.1 Berry Global Group

10.1.2 ProAmpac LLC

10.1.3 Novolex Holdings Inc.

10.1.4 Sealed Air Corporation

10.1.5 Sonoco Products Company

10.1.6 American Packaging Corporation

10.1.7 Printpack Inc.

10.1.8 Sigma Plastics Group Inc.

10.1.9 Amcor Group GmbH

10.1.10 Constantia Flexibles Group GmbH

10.1.11 Winpak Co. Limited

10.1.12 Mondi PLC

10.1.13 Uflex Limited

10.1.14 Transcontinental Inc.

10.1.15 PPC Flex Company Inc.

10.1.16 C-P Flexible Packaging

10.1.17 ePac Holdings LLC

11. HEAT MAP ANALYSIS

12. COMPETITOR ANALYSIS - EMERGING VS. ESTABLISHED PLAYERS

13. RECYCLING & SUSTAINABILITY LANDSCAPE

14. FUTURE OUTLOOK

North America Flexible Plastic Packaging Industry Segmentation

Flexible plastic packaging allows more economical and customizable options for packaging products. Flexible plastic packaging products are particularly useful in industries requiring versatile packaging, such as the food and beverage, personal care, and pharmaceutical industries. It has gained popularity due to its high efficiency and cost-effectiveness. Flexible plastic packaging combines the advantages of plastic materials such as PE and PP without compromising the product's printability, barrier protection, freshness, or ease of use. Consumers are looking for easy-to-use and lightweight packaging, and vendors are designing innovative packaging solutions to remain competitive in the growing organized retail market with the changing demands of customers. Shifting to an alternative lighter material, such as flexible pouches, provides more significant energy-saving benefits.

The North America Flexible Plastic Packaging Market Report is Segmented by Material (Polyethene [PE], Bi-Oriented Polypropylene [BOPP], Cast Polypropylene [CPP], Polyvinyl Chloride [PVC], Ethylene Vinyl Alcohol [EVOH], and Other Material Types [Polycarbonate, PHA, PLA, Acrylic, and ABS]), Product Type (Pouches, Bags, Films and Wraps, and Other Product Types), End-User Industry (Food [Frozen Food, Dry Food, Meat, Poultry, and Sea Food, Candy & Confectionery, Pet Food, Dairy Products, Fresh Produce and Other Food (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)], Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End User Industry [Automotive, Chemical, Agriculture ]), and Country (United States and Canada). The report offers market forecasts and size in volume (tonnes) for all the above segments.

| By Material Type | |

| Polyethene (PE) | |

| Bi-oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Polyvinyl Chloride (PVC) | |

| Ethylene Vinyl Alcohol (EVOH) | |

| Other Material Types (Polycarbonate, PHA, PLA, Acrylic, and ABS) |

| By Product Type | |

| Pouches | |

| Bags | |

| Films and Wraps | |

| Other Product Types (Blister Packs, Liners, etc.) |

| By End-user Industry | ||||||||||

| ||||||||||

| Beverage | ||||||||||

| Personal Care and Household Care | ||||||||||

| Medical and Pharmaceutical | ||||||||||

| Other End user Industries ( Automotive, Chemical, Agriculture) |

| By Country | |

| United States | |

| Canada |

North America Flexible Plastic Packaging Market Research FAQs

How big is the North America Flexible Plastic Packaging Market?

The North America Flexible Plastic Packaging Market size is expected to reach 8.80 million tonnes in 2024 and grow at a CAGR of 3.14% to reach 10.20 million tonnes by 2029.

What is the current North America Flexible Plastic Packaging Market size?

In 2024, the North America Flexible Plastic Packaging Market size is expected to reach 8.80 million tonnes.

Who are the key players in North America Flexible Plastic Packaging Market?

Berry Global Group, Novolex Holdings Inc., Sonoco Products Company, Amcor Group GmbH and ProAmpac LLC are the major companies operating in the North America Flexible Plastic Packaging Market.

What years does this North America Flexible Plastic Packaging Market cover, and what was the market size in 2023?

In 2023, the North America Flexible Plastic Packaging Market size was estimated at 8.52 million tonnes. The report covers the North America Flexible Plastic Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the North America Flexible Plastic Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

North America Flexible Plastic Packaging Industry Report

Statistics for the 2024 North America Flexible Plastic Packaging market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. North America Flexible Plastic Packaging analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.