North America Insulin Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

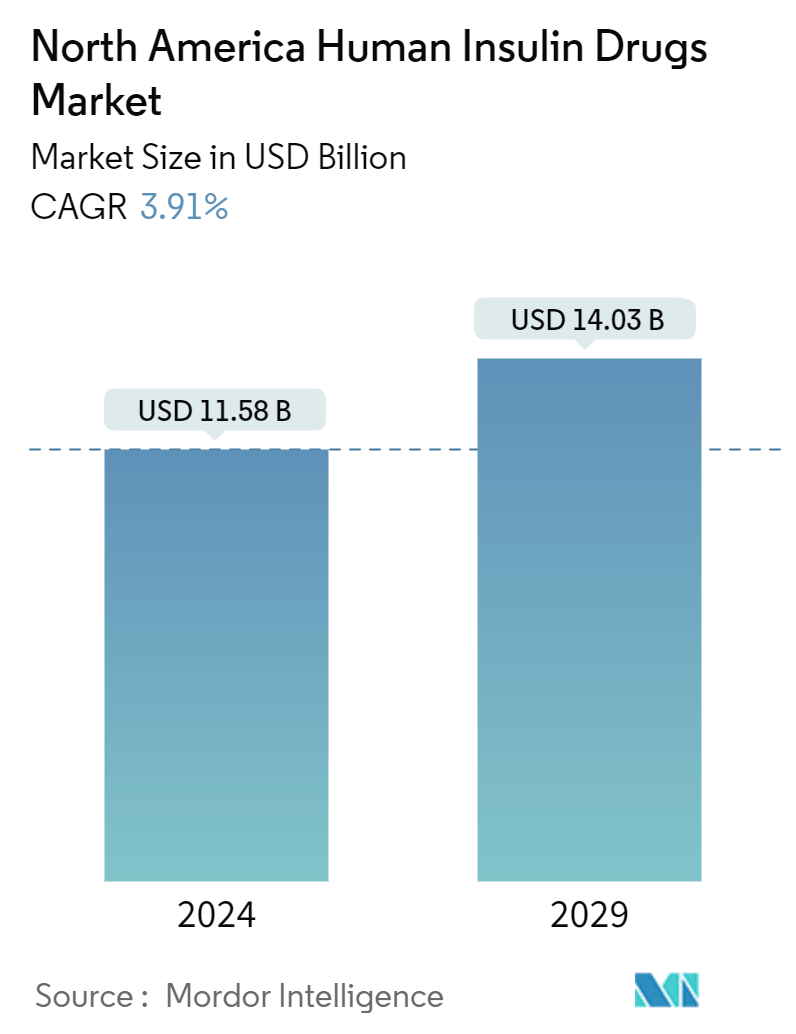

| Market Size (2024) | USD 11.58 Billion |

| Market Size (2029) | USD 14.03 Billion |

| CAGR (2024 - 2029) | 3.91 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

North America Insulin Market Analysis

The North America Human Insulin Drugs Market size is estimated at USD 11.58 billion in 2024, and is expected to reach USD 14.03 billion by 2029, growing at a CAGR of 3.91% during the forecast period (2024-2029).

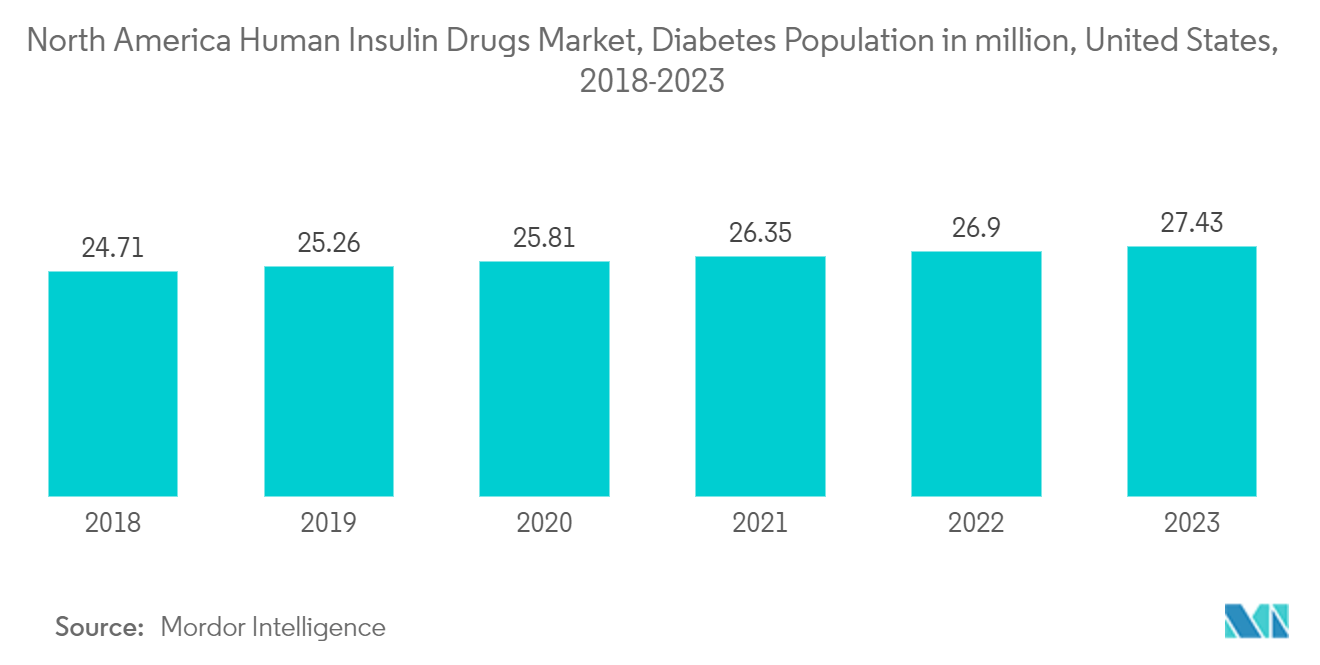

In North America, the prevalence of diabetes has been steadily increasing, in line with global trends. Sedentary lifestyles, poor dietary choices, and obesity are contributing factors to the rise in both type 1 and type 2 diabetes cases in the region. Consequently, there is a growing need for effective management strategies to tackle this public health issue.

A key element in managing diabetes in North America is the rising utilization of insulin medications. Insulin therapy remains crucial for individuals with type 1 diabetes and many patients with type 2 diabetes who require insulin to maintain optimal blood sugar levels. As the diabetes population continues to grow, the demand for insulin medications is expected to rise in the coming years.

Several factors are propelling the increased use of insulin medications in North America. Advances in insulin formulations and delivery methods have enhanced the effectiveness, safety, and convenience of insulin treatment, making it more attractive to patients. Newer insulin analogs provide quicker onset and longer-lasting effects, allowing for more flexible dosing schedules that closely resemble the body's natural insulin production.

Additionally, the growing awareness of the importance of early intervention and intensive glycemic control in preventing diabetes-related complications has led to more aggressive treatment approaches, including the initiation of insulin therapy at earlier stages of the disease. Healthcare providers are increasingly recognizing the benefits of early insulin initiation in preserving beta-cell function and improving long-term outcomes for patients with diabetes.

Furthermore, initiatives aimed at improving access to insulin, such as patient assistance programs and advocacy efforts to reduce insulin prices, are helping to ensure that individuals with diabetes can afford and access the medication they need. However, challenges such as insulin affordability and healthcare disparities continue to exist and require ongoing attention and action from policymakers, healthcare providers, and stakeholders across North America.

Overall, the increasing diabetes population in North America is driving greater usage of insulin drugs as a crucial component of diabetes management. With continued efforts to improve access, affordability, and innovation in insulin therapy, the region can work towards better outcomes for individuals living with diabetes.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

North America Insulin Market Trends

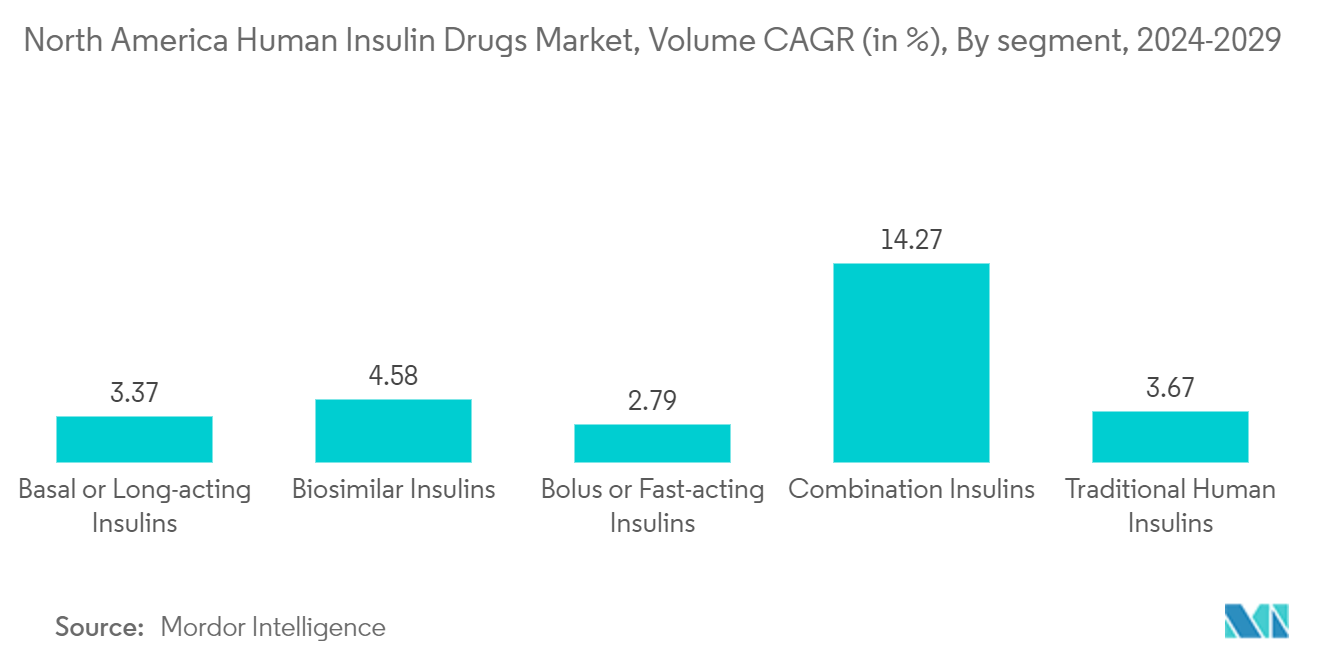

Basal/Long Acting Insulins Holds The Highest Market Share in Current Year

The US Food and Drug Administration (FDA) approved Lantus in April 2000. Lantus is a man-made form of the hormone insulin that is produced in the body. Insulin is a hormone that works by lowering levels of glucose (sugar) in the blood. Insulin glargine is a long-acting insulin that starts to work several hours after injection and keeps working evenly for 24 hours.

Lantus is for use in adults with type-1 or type-2 diabetes and in children at least 6 years old with type-1 diabetes. For type-1 diabetes, Lantus is used together with short-acting insulin given before meals. Lantus and Januvia, two treatments for diabetes, are some of the highest-selling drugs of all time and represent some of the greatest breakthroughs in diabetes control.

In current year, the United States was the largest market for Lantus, accounting for more than 58% of market revenues. However, the biosimilars for Lantus may not present it with competitive challenges currently. The loss of exclusivity for Lantus may not result in a near-term disruption of the market for it. However, there will be additional pricing pressure and some loss of market share that will continue and may increase over time.

United States Holds Highest Market Share in Current Year

Among North American countries, the United States dominates around 94% of the total North American human insulin drug market. This is mainly due to the high diabetes prevalence in the country. The United States records the highest healthcare expenditure globally, and it also has a higher adoption of advanced therapeutics.

The United States accounts for the highest sales of long-acting insulin, Lantus, across the North American region. Most diabetic drug manufacturing companies consider the country a critical market for improving overall global sales.

Lantus is the most commonly administered basal insulin across the world, accounting for a dominant share in the United States market. Together, Eli Lilly and Boehringer Ingelheim are working to develop and market Basaglar (Insulin Glargine). Insulin Tregopil, an oral prandial insulin tablet, is being developed by Biocon to treat type-1 and type-2 diabetes mellitus. Fast-acting oral insulin holds the potential to revolutionize T1D care by enhancing post-prandial glucose control with fewer side effects and higher adherence.

To provide a more practical, efficient, and secure way to administer insulin therapy, Oramed Pharmaceuticals Inc., a clinical-stage pharmaceutical company focused on the development of oral drug delivery systems, is attempting to bring the first oral insulin product to market.

The United States accounts for the highest sales of Humalog across the world, with over 56% of the market share. The majority of diabetes drug manufacturing companies consider the country a critical market for improving overall global sales. In the United States, Humalog is available in different varieties under names like Humalog Mix 75/25, Humalog U-100, Humalog U-200, and Humalog Mix 50/50 for the treatment of diabetes.

Therefore, owing to the aforesaid factors, the growth of the studied market is anticipated in the North American region.

North America Insulin Industry Overview

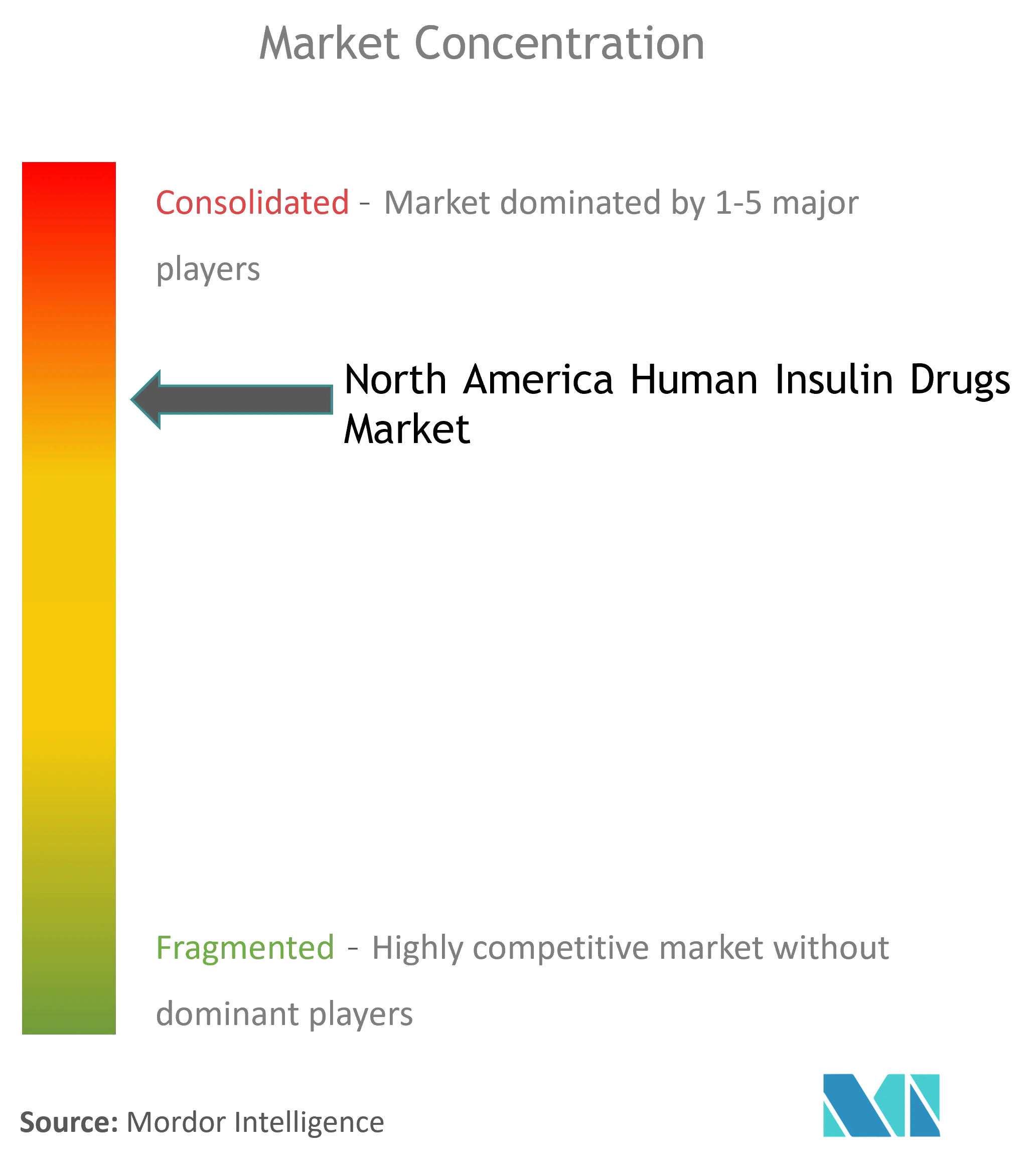

The North American human insulin market is highly fragmented, with three major manufacturers having a large market share. In the United States, there are no other players except Novo Nordisk, Sanofi, and Eli Lilly. In the remaining countries, the manufacturers confine themselves to other local or region-specific manufacturers. Mergers and acquisitions that happened between the players in the recent past helped the companies strengthen their market presence. Eli Lilly and Boehringer Ingelheim have an alliance to develop and commercialize Basaglar (insulin glargine).

North America Insulin Market Leaders

-

Sanofi S.A.

-

Novo Nordisk A/S

-

Eli Lilly and Company

-

Pfizer Inc

-

Biocon Limited

*Disclaimer: Major Players sorted in no particular order

North America Insulin Market News

- June 2023: The initial allogeneic (donor) pancreatic islet cellular therapy, Lantidra, has been sanctioned by the U.S. Food and Drug Administration. This treatment is derived from pancreatic cells of deceased donors and is intended for individuals with type 1 diabetes. Lantidra is specifically authorized for adults who struggle to achieve target glycated hemoglobin levels due to frequent severe hypoglycemia episodes, despite undergoing intensive diabetes management and education.

- November 2022: The FDA approved the second interchangeable insulin glargine biosimilar, Rezvoglar, to improve glycemic control in adults and pediatric patients with diabetes, according to a drug information update from the agency.

North America Insulin Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Drivers

4.3 Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Drug

5.1.1 Basal or Long-acting Insulin

5.1.1.1 Lantus (Insulin Glargine)

5.1.1.2 Levemir (Insulin Detemir)

5.1.1.3 Toujeo (Insulin Glargine)

5.1.1.4 Tresiba (Insulin Degludec)

5.1.1.5 Basaglar (Insulin Glargine)

5.1.2 Bolus or Fast-acting Insulin

5.1.2.1 NovoRapid/Novolog (Insulin Aspart)

5.1.2.2 Humalog (Insulin Lispro)

5.1.2.3 Apidra (Insulin Glulisine)

5.1.2.4 FIASP (Insulin aspart)

5.1.2.5 Admelog (Insulin lispro)

5.1.3 Traditional Human Insulin

5.1.3.1 Novolin/Actrapid/Insulatard

5.1.3.2 Humulin

5.1.3.3 Insuman

5.1.4 Combination Insulin

5.1.4.1 NovoMix (Biphasic Insulin Aspart)

5.1.4.2 Ryzodeg (Insulin Degludec and Insulin Aspart)

5.1.4.3 Xultophy (Insulin Degludec and Liraglutide)

5.1.4.4 Soliqua/Suliqua (Insulin glargine/Lixisenatide)

5.1.5 Biosimilar Insulin

5.1.5.1 Insulin Glargine Biosimilars

5.1.5.2 Human Insulin Biosimilars

5.2 Geography

5.2.1 United States

5.2.2 Canada

5.2.3 Rest of North America

6. MARKET INDICATORS

6.1 Type 1 Diabetes Population

6.2 Type 2 Diabetes Population

7. COMPETITIVE LANDSCAPE

7.1 COMPANY PROFILES

7.1.1 Novo Nordisk A/S

7.1.2 Sanofi S.A.

7.1.3 Eli Lilly and Company

7.1.4 Biocon Limited

7.1.5 Pfizer Inc.

7.1.6 Wockhardt

7.1.7 Julphar

7.1.8 Exir

7.1.9 Sedico

- *List Not Exhaustive

7.2 COMPANY SHARE ANALYSIS

7.2.1 Novo Nordisk AS

7.2.2 Sanofi S.A.

7.2.3 Eli Lilly and Company

7.2.4 Other Companies

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

North America Insulin Industry Segmentation

Human insulin, such as Myxredlin, Humulin R U-100, and Novolin R, can also be administered intravenously by healthcare professionals in a medical environment. During this process, doctors or nurses will diligently observe any potential side effects. It is important to note that while human insulin effectively manages elevated blood sugar levels, it does not provide a cure for diabetes. The North American human insulin drug market is segmented by drug and geography. The report offers the value (in USD) and volume (in units) for the above segments.

| Drug | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

| Geography | |

| United States | |

| Canada | |

| Rest of North America |

North America Insulin Market Research FAQs

How big is the North America Human Insulin Drugs Market?

The North America Human Insulin Drugs Market size is expected to reach USD 11.58 billion in 2024 and grow at a CAGR of 3.91% to reach USD 14.03 billion by 2029.

What is the current North America Human Insulin Drugs Market size?

In 2024, the North America Human Insulin Drugs Market size is expected to reach USD 11.58 billion.

Who are the key players in North America Human Insulin Drugs Market?

Sanofi S.A., Novo Nordisk A/S, Eli Lilly and Company, Pfizer Inc and Biocon Limited are the major companies operating in the North America Human Insulin Drugs Market.

What years does this North America Human Insulin Drugs Market cover, and what was the market size in 2023?

In 2023, the North America Human Insulin Drugs Market size was estimated at USD 11.13 billion. The report covers the North America Human Insulin Drugs Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the North America Human Insulin Drugs Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

North America Insulin Industry Report

Statistics for the 2024 North America Insulin market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. North America Insulin analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.