North America Insurance Telematics Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

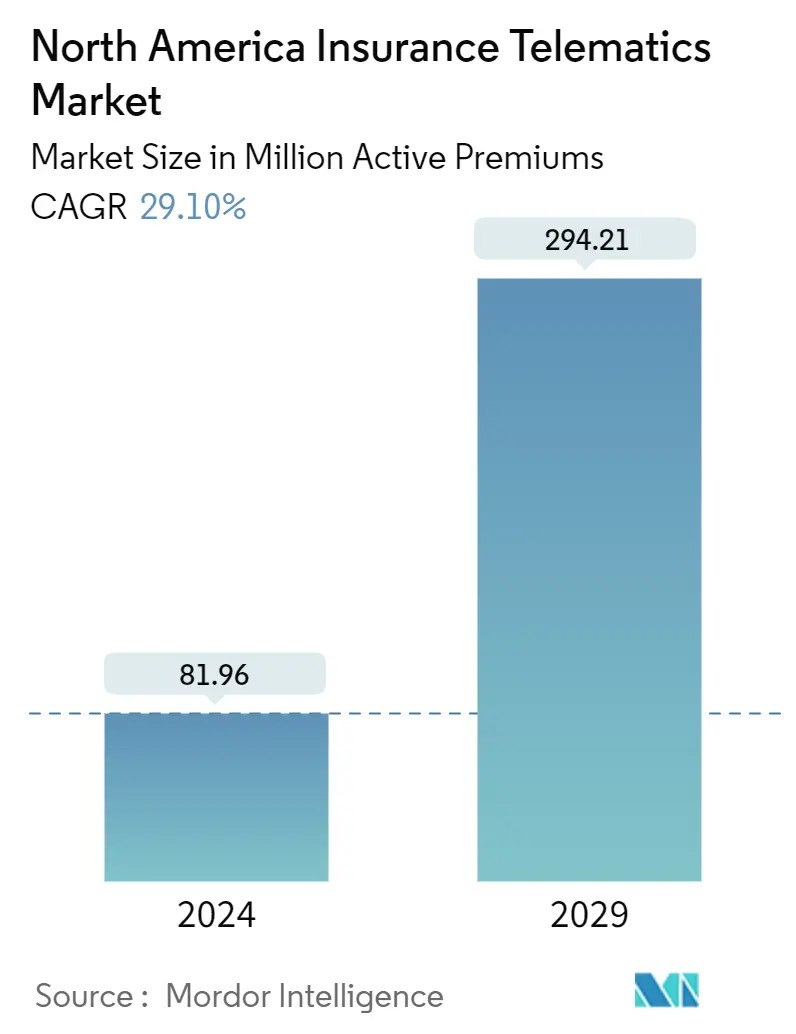

| Market Volume (2024) | 81.96 Million active premiums |

| Market Volume (2029) | 294.21 Million active premiums |

| CAGR (2024 - 2029) | 29.10 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

North America Insurance Telematics Market Analysis

The North America Insurance Telematics Market size is estimated at 81.96 Million active premiums in 2024, and is expected to reach 294.21 Million active premiums by 2029, growing at a CAGR of 29.10% during the forecast period (2024-2029).

The growing demand for telematic devices among the insurance and automotive sectors propels the market's growth. Many automotive companies invest in advanced telematics systems to gain a competitive edge. From application-specific telematics and computer imaging, fleet managers can access a wealth of information about the condition of their vehicles.

- Rising congestion and road traffic have made people's safety a top priority. Improving advanced vehicle features is a significant factor aiding the growth of the demand for vehicle insurance telematics. According to the National Safety Council, some 47,000 road traffic fatalities occurred in the United States in 2021, which was the most significant number of deaths recorded in the country since 2012. This fatality volume was slightly dipped in 2022, down to nearly 46,300. Motor vehicle crashes are a frequent cause of death in the United States.

- In addition, according to the official source, in 2023, there were 6,102,936 police-reported vehicle accidents in the United States. Of those, 39,508 were fatal. Such increases in road accidents may further create demand for insurance telematics in the region.

- Various governments are taking initiatives in road safety to avoid accidents or car crashes, which may create demand for insurance telematics in the region. Furthermore, Canada's fourth national road safety plan, the Road Safety Strategy (RSS) 2025, was launched by the Council of Ministers Responsible for Transportation and Highway Safety in early 2016. The goal remains to achieve downward trends in fatalities and severe injuries throughout a five-year duration, comparing multi-year rolling averages with the established baseline period.

- However, a lack of awareness of insurance telematics and privacy and security concerns somewhat hinder the market. On the other hand, increasing innovation in the automotive enterprise and untapped potential in emerging economies present new opportunities in the upcoming years.

- The COVID-19 pandemic had a positive impact on the insurance telematics industry. This is attributed to telematics directly addressing consumer needs to pay lower premiums when the vehicles had limited utilization during the lockdown.

- In addition, the pandemic changed insurers' demands from traditional actuarial and underwriting models to pay-as-you-drive (PAYD) models. In addition, increased acceptance of digital tools in the policy binding and claims process among consumers, combined with a need for insurers to design premium policies more precisely, are significant factors that notably contribute to the market's growth.

North America Insurance Telematics Market Trends

Increase in Innovation in the Automotive Industry Across the Region to Witness Growth

- Innovation in the automotive sector is a key driver of the growth of insurance telematics, creating opportunities for insurers to leverage technology to offer more personalized and data-driven insurance products. The proliferation of connected car technologies, including embedded telematics systems, onboard sensors, and in-vehicle communication networks, provide insurers with real-time data on vehicle performance, driver behavior, and environmental conditions. These data streams enable more accurate insurance policy risk assessments and pricing models.

- Moreover, developing autonomous and semi-autonomous vehicle technologies is reshaping the automotive industry and presenting new opportunities for insurance telematics. Insurers can leverage telematics data to assess the impact of ADAS and autonomous features on driving behavior, safety, and risk exposure. With the rise of connected and autonomous vehicles, telematics is even more important as these new systems need to monitor effectively and report data related to driving behavior. Telematics technology has become a crucial element in modern vehicles, enabling insurers to precisely determine premiums by assessing a driver's real-time behavior rather than relying on mere speculation.

- The United States is anticipated to be the significant market for connected cars due to the significant presence of automotive OEMs, higher technological awareness among the general car buyers, preference for infotainment and telematics in vehicles, widespread adoption of 4G/5G, and increasing sales of electric, connected and autonomous cars in the country.

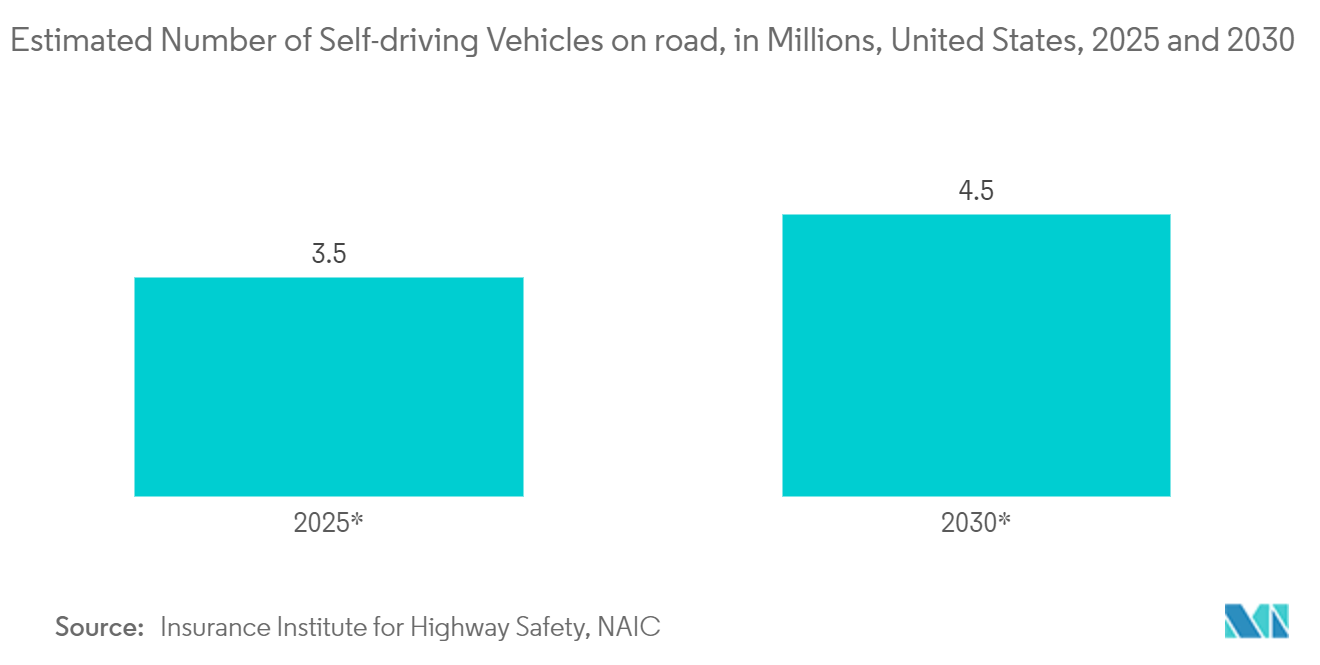

- According to the Insurance Institute for Highway Safety, it is anticipated that there will be around 3.5 million self-driving vehicles on US roads by 2025 and 4.5 million by 2030. However, the institute cautioned that these vehicles would not be fully autonomous but would operate autonomously under certain conditions. Recognizing the symbiotic relationship between insurers and autonomous vehicle manufacturers, insurers are actively engaging in collaborations. By working closely with manufacturers, insurers gain insights into the technology, safety features, and potential risks associated with autonomous vehicles.

- This collaborative approach helps insurers craft policies that align with the evolving landscape of self-driving cars. For instance, Connected Analytic Services, LLC (CAS), an affiliate of Toyota Insurance Management Solutions USA, expanded its partnership with Toyota Motor North America to add new product offerings to enhance the ownership experience for owners of enrolled Toyota vehicles. For Toyota customers who wish to use their driving data to obtain potential insurance savings, CAS is Toyota's exclusive data aggregation service, providing telematics and vehicle build data to insurance companies. Major players in the market are expanding their presence in digital mobility to cater to the increased demand for connected cars.

United States to Hold Major Market Share

- Decreasing the cost of development and technology, altering consumer behavior, and stringent government regulations drive the growth of the market studied in the United States. In the United States, consumers prefer usage-based insurance (UBI) snapshot programs. In other regions, motor insurance telematics policies are preferred.

- Introducing insurance telematics has several advantages for insurers and consumers, which are expected to fuel market growth. For consumers, it will promote safe driving, resulting in the mitigation of accident severity and frequency. Over the forecast period, the insurers' claim-handling expenses will likely decrease by at least half, contributing to the market's growth.

- Various US consumers are switching insurers because their premiums have increased despite driving less. Measures imposed during the lockdown during the pandemic led consumers to drive less and ultimately demanded policies that analyzed auto usage to provide personalized policies based on mileage.

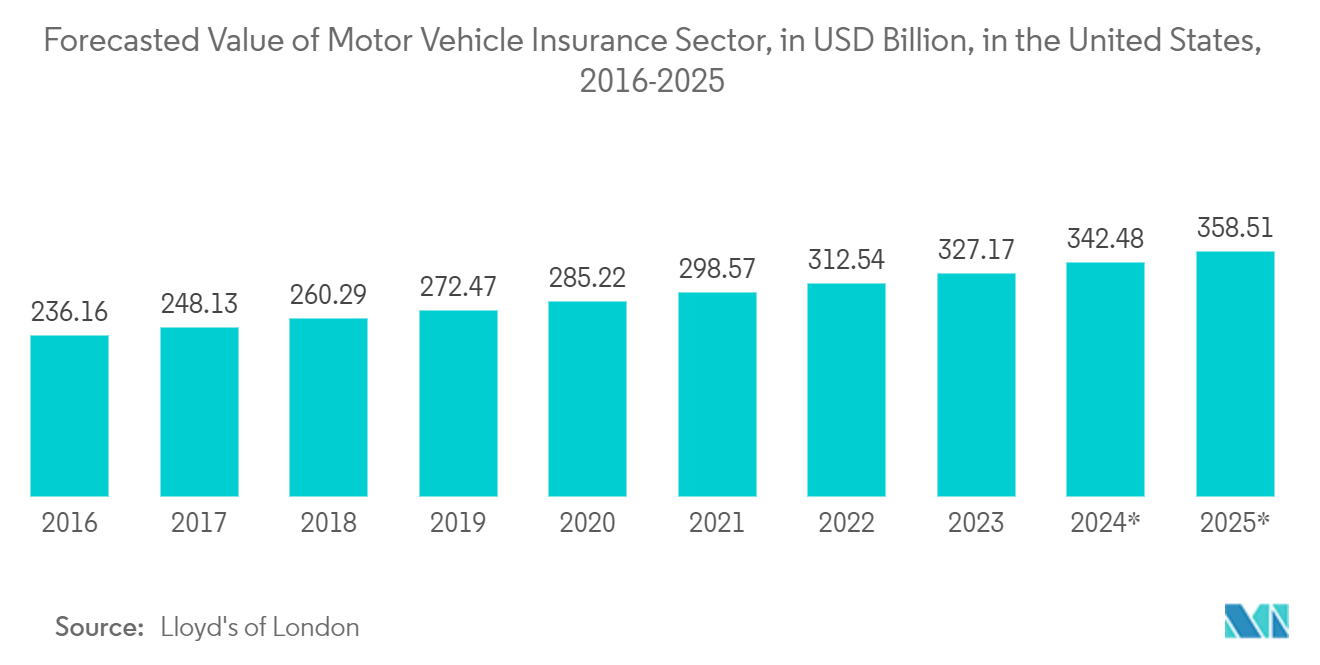

- According to Lloyd's of London, the value of the motor vehicle insurance sector in the United States is expected to amount to approximately USD 224.7 billion in 2015. It was projected to grow to about USD 358.51 billion by 2025.

- According to BEA, in May 2023, 1.07 million vehicles were sold in the United States, including light trucks, which remained the most significant United States auto market segment, contributing to sales of 1.06 million units.

- The United States is anticipated to be the significant market for connected cars in the country due to the substantial presence of automotive OEMs, high levels of technology awareness amongst the general car buyers, preference for infotainment and telematics in vehicles, widespread adoption of 4G/5G and increasing sales of electric, connected and autonomous cars in the country.

North America Insurance Telematics Industry Overview

The North American insurance telematics market is fragmented, with major players like Octo Telematics SpA, IMERTIK Global Inc., AXA SA, The Floow Limited, and LexisNexis Risks Solutions (RELX Group). Market participants employ partnerships and acquisitions to improve their product offerings and secure a lasting competitive edge.

- In October 2023 - OCTO Telematics announced a partnership with Flexcar, the smart alternative to car ownership, focused on adding OCTO’s connected vehicle capabilities to Flexcar’s fleet across the United States.

- In October 2023 - PowerFleet Inc. intends to merge with MiX Telematics Ltd, a fleet management tech firm based in South Africa, creating a single company with a combined subscriber base of some 1.7 million users. The deal is expected to close in the first quarter of 2024, and the combined business will be branded as PowerFleet. Its primary listing will be on Nasdaq, and its headquarters will be in Woodcliff Lake, New Jersey.

North America Insurance Telematics Market Leaders

-

Octo Telematics SpA

-

IMERTIK Global Inc.

-

AXA SA

-

The Floow Limited

-

LexisNexis Risks Solutions (RELX Group)

*Disclaimer: Major Players sorted in no particular order

North America Insurance Telematics Market News

- September 2023 - OCTO announced the launch of the Digital Driver, Try Before You Buy solution, available through an App dedicated to drivers and designed to encourage a more objective risk assessment based on driving style. The exclusive monitoring features of Try Before You Buy allow the insurance company to accurately define customer pricing through a more transparent relationship based on actual driving behavior data that goes far beyond the traditional use of demographic factors.

- September 2023 - The Floow Limited partnered with Definity and Munich Re, a provider of reinsurance solutions, to bring a new, innovative, usage-based auto insurance product to Canada. Definity’s new Sonnet Shift is the first ever UBI product in Canada to offer quarterly price adjustments based on recent driving scores. Powered by The Floow advanced telematics and Munich Re, Sonnet Shift uses individual driving behaviors and preferences as the main factors for pricing, including time of day, fatigue, smooth driving, speed, mobile distraction, and road risk.

North America Insurance Telematics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Degree of Competition

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Adoption of Usage-based Insurance by Insurance Companies

5.1.2 Increase in Innovation in the Automotive Industry Across the Region to Witness the Growth

5.2 Market Challenge

5.2.1 Data Quality and Compatibility Issues

6. USAGE BASED INSURANCE TELEMATICS - REVENUE MODELS

6.1 Pay-as-you-drive

6.2 Pay-how-you-drive

6.3 Manage-how-you-drive

7. COMPARATIVE ANALYSIS OF VARIOUS TYPES OF TELEMATICS HARDWARE-BASED INSURANCE SOLUTIONS

7.1 Portable

7.2 Embedded

7.3 Smartphone Based

8. MARKET SEGMENTATION

8.1 By Country

8.1.1 United States

8.1.2 Canada

9. COMPETITIVE LANDSCAPE

9.1 Company Profiles*

9.1.1 Octo Telematics SpA

9.1.2 IMERTIK Global Inc.

9.1.3 AXA SA

9.1.4 The Floow Limited

9.1.5 LexisNexis Risks Solutions (RELX Group)

9.1.6 PowerFleet Inc.

9.1.7 Cambridge Mobile Telematics

9.1.8 State Farm Mutual Automobile Insurance Company

9.1.9 GEICO (Berkshire Hathaway Inc.)

9.1.10 Nationwide Mutual Insurance Company

10. INVESTMENT ANALYSIS

11. FUTURE TRENDS

North America Insurance Telematics Industry Segmentation

Insurance telematics is used to track how people drive. It involves technology, such as GPS and sensors, to monitor and collect data on an individual's driving behavior. Insurance organizations use this data to assess risk and set personalized premiums accurately. Telematics devices installed in a vehicle help to track various parameters, such as speed, distance, and driving habits, which allows insurers to reward safe driving or adjust premiums based on actual usage patterns. Various telematics devices include cigarette-lighter plugs, smart tags, OBD (On-Board Diagnostic) devices, battery lines, windshield-mounted devices, black boxes, and smartphone apps.

The market for insurance telematics was analyzed considering the total number of active premiums filed by the various insurance providers across North America. The scope of the study includes different usage-based insurance telematics revenue models that are pay-as-you-drive, pay-how-you-drive, and manage-how-you-drive. The study also compares various types of telematics hardware insurance solutions across the United States and Canada, such as portable, embedded, and smartphone-based. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates during the forecast period. The study further analyzes the overall impact of COVID-19 and macroeconomic trends on the ecosystem. The report's scope encompasses market sizing and forecasts for the various market segments.

The North American insurance telematics market is segmented by country (United States, Canada). The market size and forecasts regarding the number of active premiums for all the above segments are provided.

| By Country | |

| United States | |

| Canada |

North America Insurance Telematics Market Research FAQs

How big is the North America Insurance Telematics Market?

The North America Insurance Telematics Market size is expected to reach 81.96 million active premiums in 2024 and grow at a CAGR of 29.10% to reach 294.21 million active premiums by 2029.

What is the current North America Insurance Telematics Market size?

In 2024, the North America Insurance Telematics Market size is expected to reach 81.96 million active premiums.

Who are the key players in North America Insurance Telematics Market?

Octo Telematics SpA, IMERTIK Global Inc., AXA SA, The Floow Limited and LexisNexis Risks Solutions (RELX Group) are the major companies operating in the North America Insurance Telematics Market.

What years does this North America Insurance Telematics Market cover, and what was the market size in 2023?

In 2023, the North America Insurance Telematics Market size was estimated at 58.11 million active premiums. The report covers the North America Insurance Telematics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the North America Insurance Telematics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

North America Insurance Telematics Industry Report

The North American Insurance Telematics Market Report provides a comprehensive market overview, focusing on the segmentation by country, specifically the United States and Canada. The market size is evaluated in terms of the number of active premiums within these regions. This industry report includes a detailed market analysis and industry trends, offering an industry outlook that spans from the current period to the forecasted future.

The report highlights the market growth and market forecast, providing insights into the industry size and industry growth rate. It includes industry statistics and market data that are crucial for understanding the market value and market segmentation. The industry information presented in the report is based on extensive industry research and market research, ensuring accurate industry analysis and market predictions.

This market report also examines the market leaders and their influence on the market dynamics. The market review includes a thorough analysis of market trends and market outlook, offering valuable insights for stakeholders. The industry reports and industry sales figures are supported by detailed market predictions and industry research.

A sample of this industry analysis is available as a report pdf download, providing a report example for those interested in deeper insights. The report also covers the market forecast and market growth, ensuring that readers are well-informed about the future prospects of the North American Insurance Telematics market. The research companies involved have meticulously compiled the data to offer a reliable and comprehensive industry overview.