Market Size of OBGYN EHR Industry

| Study Period | 2019 - 2029 |

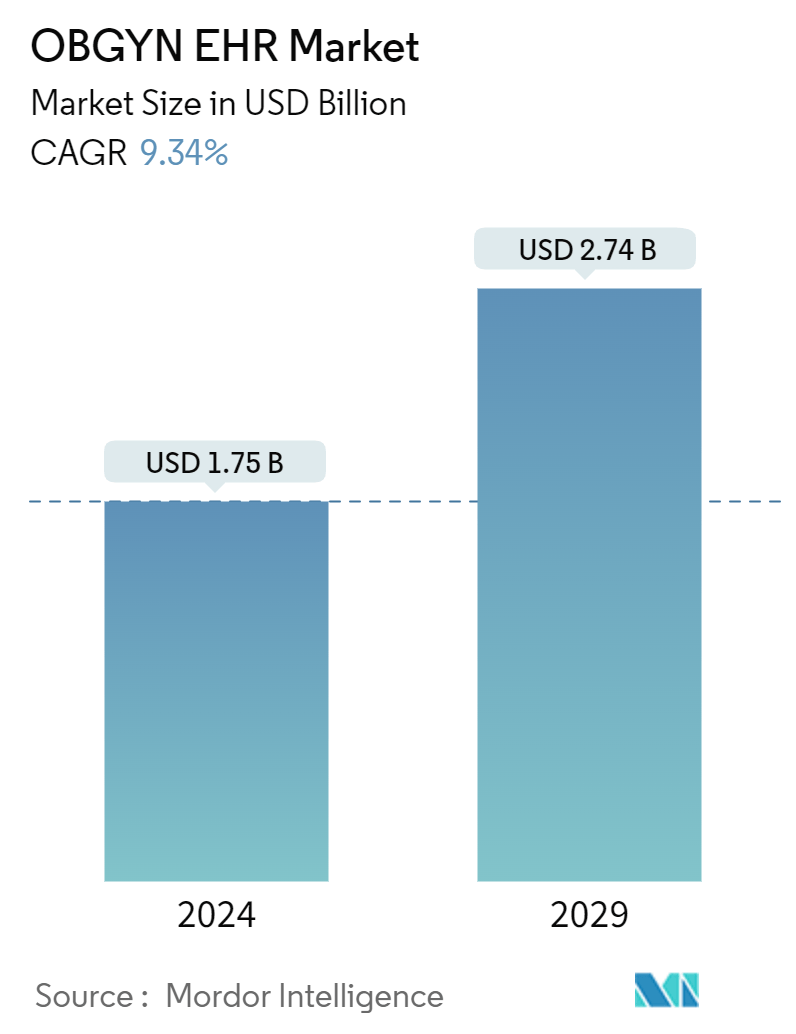

| Market Size (2024) | USD 1.75 Billion |

| Market Size (2029) | USD 2.74 Billion |

| CAGR (2024 - 2029) | 9.34 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

OBGYN EHR Market Analysis

The OBGYN EHR Market size is estimated at USD 1.75 billion in 2024, and is expected to reach USD 2.74 billion by 2029, at a CAGR of 9.34% during the forecast period (2024-2029).

The major factors driving the OBGYN electronic health records (EHR) market include the increasing digitalization of healthcare, growing adoption of electronic health records in gynecology practices, high childbirth rates, rising prevalence of gynecology diseases, and increase in strategic activities such as new solution launches and acquisitions. Increasing technological advancements in OBGYN EHR software boost the adoption of these technologies by gynecologists and obstetrician specialists to manage patient records with customizable workflows and increase hospital efficiency, which is ultimately expected to drive the market studied over the forecast period.

For instance, in May 2024, Athenahealth, a specialty EHR solutions provider, reported the launch of the athenaOne platform, an OBGYN electronic health solution that provides robust clinical, medical billing, and patient engagement support. Hence, the launch of such advanced OBGYN EHR software, which offers various applications for efficient management of obstetrics and gynecology clinics, is expected to increase their accessibility and affordability and ultimately drive the market over the forecast period. Furthermore, the increasing hospitalization of women for childbirth is expected to increase the utilization of OBGYN EHR software for effective management of women's health during the hospital stay of pregnant women and increase the efficiency of gynecology and obstetrics departments in hospitals, further driving the market studied over the forecast period.

According to the Canadian Institute for Health Information’s (CIHI) updated data from January 2024, the most common reason for hospitalization in Canada was giving birth in 2022. The most common inpatient surgery was a Caesarean section (C-section) in the same year, with the total C-section rate increasing gradually over the years and reaching 32.5% in 2022. Hence, the increasing inflow of patients to gynecology and obstetrics clinics is expected to increase the utilization of the OBGYN electronic health records for effective management of patients and optimize the clinic's operations, which is expected to ultimately drive the market studied over the forecast period.

Furthermore, the increasing prevalence of gynecological diseases in women increases the inflow of patients to OBGYN clinics, which accelerates the utilization of OBGYN EHR for the effective management of patients. This factor is expected to drive the market studied over the forecast period. For instance, according to the World Health Organization's updated data from March 2023, endometriosis affects roughly 10% (190 million) of reproductive-age women and girls globally. Hence, the significant prevalence of reproductive diseases in women is expected to increase the demand for OBGYN EHR solutions to improve women patients' outcomes, which will ultimately drive the market studied over the forecast period. Thus, increasing technological advancements in OBGYN EHR platforms, high birth rates, and the growing prevalence of gynecological diseases are expected to drive the market studied over the forecast period. However, the high implementation costs of OBGYN EHR, coupled with data privacy concerns, are expected to restrain the market studied over the forecast period.