Ophthalmic Devices Market Size

| Study Period | 2019 - 2029 |

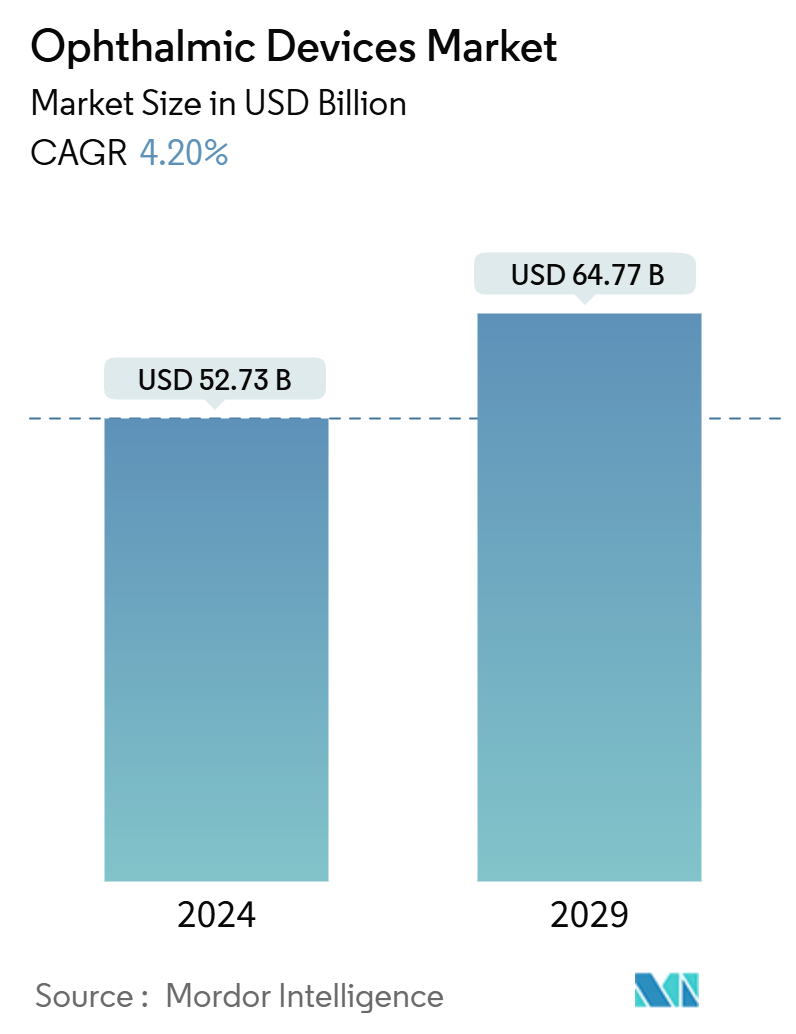

| Market Size (2024) | USD 52.73 Billion |

| Market Size (2029) | USD 64.77 Billion |

| CAGR (2024 - 2029) | 4.20 % |

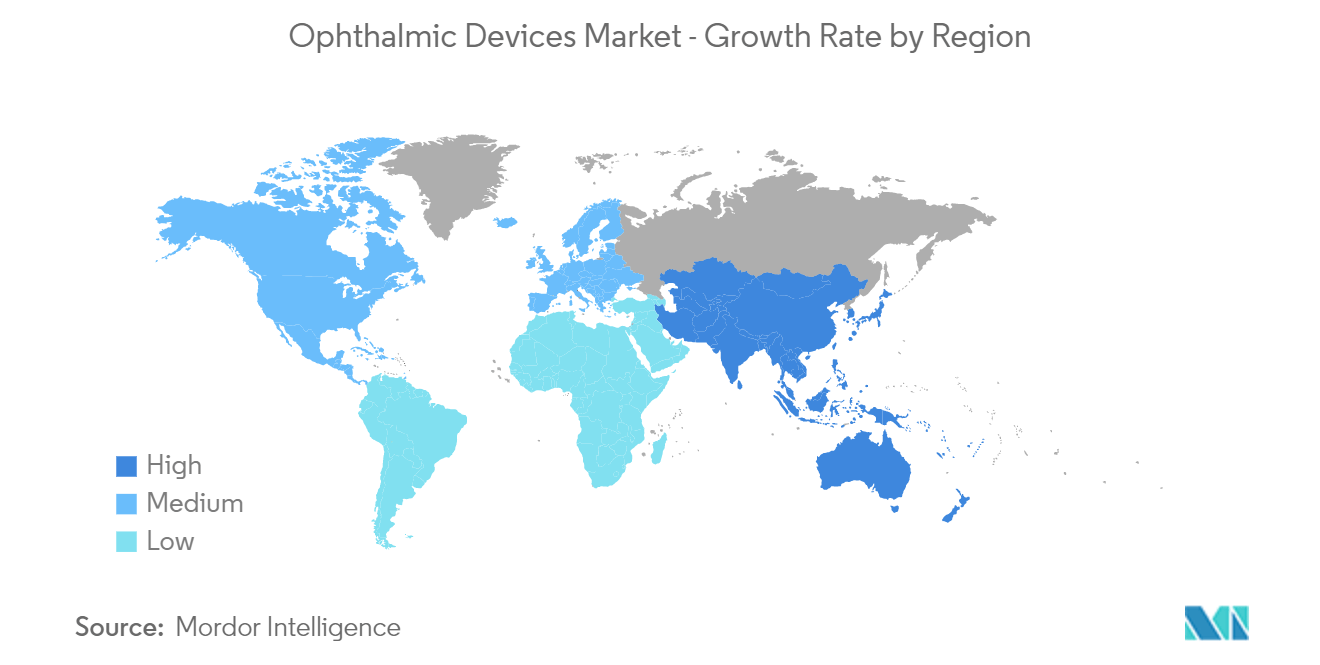

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

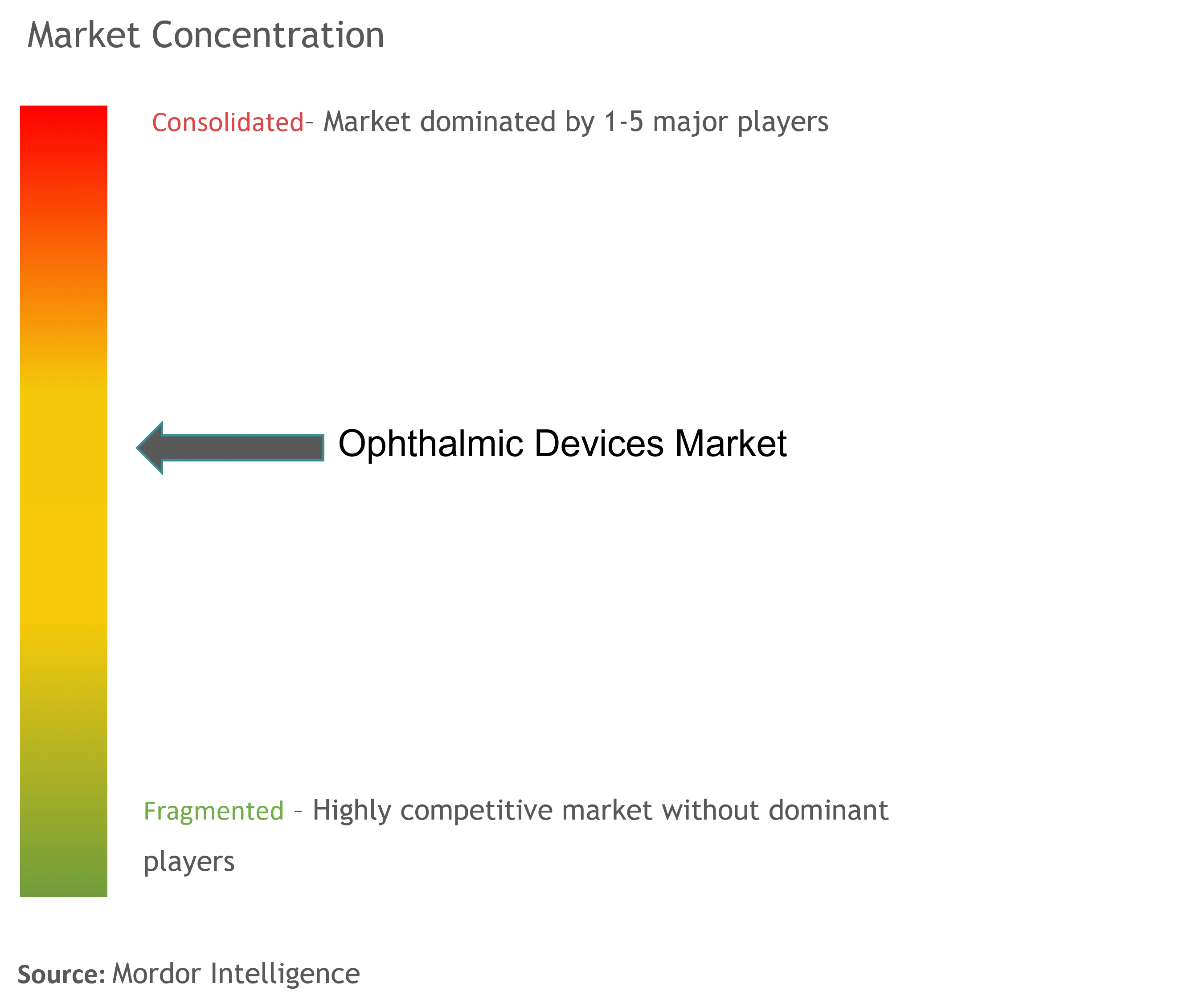

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Ophthalmic Devices Market Analysis

The Ophthalmic Devices Market size is estimated at USD 52.73 billion in 2024, and is expected to reach USD 64.77 billion by 2029, at a CAGR of 4.20% during the forecast period (2024-2029).

The COVID-19 epidemic has resulted in considerable service reductions throughout the NHS, with ophthalmology being one of the most severely impacted specialties. According to a study published in March 2021 in the British and Irish Orthopaedic Journal, outpatient clinic appointments were reduced by 87.2%, ophthalmic surgery by 90.9%, outpatient referrals to ophthalmology by 50.2%, and ward reviews by 50% during the first peak of the pandemic. There were 1,377 canceled appointments, with 6.8% of them deemed appropriate for teleophthalmology. Another study published in BMC Ophthalmology in May 2022 found that during the COVID-19 health emergency, retina clinic volume fell by 62%. The average time from check-in to technician has decreased by 79%, total visit length has decreased by 46%, and time spent in the provider phase of care has decreased by 53%. Thus, the COVID-19 pandemic severely curtailed ophthalmology services initially, but currently, as the pandemic has subsided, the market has gained some traction, and thus the market is expected to have stable growth during the forecast period of the study.

Furthermore, ophthalmic devices are medical equipment designed for diagnosis, surgical, and vision correction purposes. These devices have gained substantial importance due to the high prevalence of various ophthalmic diseases such as glaucoma, cataracts, and other vision-related issues across the globe. According to the World Health Organisation's March 2022 update, trachoma is a public health problem in 44 countries and is responsible for the blindness or visual impairment of about 1.9 million people globally. Such a high burden of disease and the need for surgical treatment are thus driving the growth of the market.

Moreover, technological advancements in the ophthalmology field have boosted the adoption rate of these devices globally. Portable medical devices are increasingly being used for home-based diagnosis and treatment of eye disorders, allowing for the diagnosis and monitoring of eye illnesses. For instance, in August 2022, Swaraashi Netralya announced the debut of ophthalmic instruments, including an ophthalmoscope, to diagnose eye problems in adults and children in India. The Mirante SLO/OCT, a scanning laser ophthalmoscope used to acquire high-quality color pictures, was introduced in India. Similarly, in February 2023, NIDEK CO., LTD. Japan introduced the Cube Ophthalmic Surgical System, which includes revolutionary ultrasound technology to provide more powerful and effective phacoemulsification. Thus, the introduction of ophthalmic devices in the market may increase accessibility to the end user, likely boosting market growth.

Thus, the aforesaid factors are likely to have a positive impact on the growth of the market. However, poor primary healthcare infrastructure in developing and underdeveloped countries and the risk associated with ophthalmic procedures may hinder the market's growth.

Ophthalmic Devices Market Trends

Vision Correction Devices Segment is Expected to Register a High CAGR Over the Forecast Period

Vision correction devices, or corrective lenses, are used to aid and improve vision for those with common refractive errors like myopia, hypermetropia, astigmatism, and presbyopia. These visual impairments result in low vision. Moreover, the prevalence of these conditions is expected to grow shortly, owing to increased screen time, a rising geriatric population, and other chronic conditions leading to vision loss. For instance, according to World Health Organisation (WHO) statistics from 2022, at least 2.2 billion individuals worldwide have near- or farsighted vision impairment. Vision impairment may have been avoided or managed in at least 1 billion cases, or nearly half of these cases. The majority of those who have vision impairments or blindness are over 50 years old. Thus, such statistics suggest an increasing need for vision correction devices and are expected to drive the growth of the segment.

Additionally, the launch of new products in the market is also contributing to the growth of the market segment. For instance, in July 2022, Bausch + Lomb Corporation launched Revive custom soft contact lenses, a new family of customizable soft contact lenses, in the United States. Revive custom soft lenses are designed to meet the vision needs of patients, especially those with high or unique prescriptions. Such launches are propelling the growth of the market segment. Additionally, in June 2022, Johnson & Johnson Vision reported that its latest contact lens innovation, Acuvue Oasys Max 1-Day, and Acuvue Oasys Max 1-Day Multifocal, had obtained FDA clearance, Health Canada certification, and CE Mark validation. The new contact lenses are comfortable and clear all day. Thus, the introduction of corrective lenses and regulatory approval is expected to boost the market growth.

Hence, the high number of eye disorder cases is likely to create demand for advanced vision correction devices, thereby boosting the growth of the market segment.

North America is Expected to Hold a Significant Share in the Market and Expected to do Same Over the Forecast Period

North America is expected to hold a significant share of the market owing to factors such as high disposable income, growing awareness, a rising geriatric population, and the increasing prevalence of eye diseases coupled with the launch of newer products and devices.

The growing incidence of ophthalmic diseases is anticipated to contribute to market growth. For instance, according to the CDC Report in November 2022, glaucoma cases are expected to rise to 6.3 million by 2050 in the United States. Further, the Statistics Canada report published in March 2023, estimated that glaucoma impacted more than 728,000 Canadians in 2022. Thus, the growing burden of glaucoma is expected to increase demand for glaucoma surgery and likely boost the market for ophthalmic devices over the forecast period.

Additionally, the increasing focus of market players on innovation and the launch of new products in the market is also expected to propel the growth of the market in the region. For instance, in March 2022, Alcon Inc. launched the Clareon portfolio of intraocular lenses (IOLs) in the United States, including the Clareon Monofocal, PanOptix, and Vivity IOLs. Furthermore, in April 2023, Canadian eye health company Bausch + Lomb has launched the StableVisc cohesive ophthalmic viscosurgical device (OVD) and the TotalVisc Viscoelastic System in the United States.

Thus, owing to the abovementioned factors, such as the growing burden of ophthalmic diseases and product launches, the market in the North American region is expected to project growth over the forecast period.

Ophthalmic Devices Industry Overview

The ophthalmic devices market is moderately competitive. Also, the new technological advancements and launch of new products and initiatives are expected to make the market more competitive. Some of the players operating in the market are Alcon Inc., Bausch Health Companies Inc., Carl Zeiss Meditec AG, EssilorLuxottica SA, HAAG-Streit Group, Hoya Corporation, Johnson & Johnson, and others.

Ophthalmic Devices Market Leaders

-

Alcon Inc.

-

Bausch Health Companies Inc.

-

Johnson and Johnson

-

Carl Zeiss Meditec AG

-

Ziemer Ophthalmic Systems AG

*Disclaimer: Major Players sorted in no particular order

Ophthalmic Devices Market News

- March 2023: the Bausch + Lomb Corporation announced the debut of the StableVisc cohesive ophthalmic viscosurgical device (OVD) and TotalVisc Viscoelastic System in the United States. StableVisc and TotalVisc give eye surgeons new choices for dual-action protection during cataract surgery.

- August 2022: Glaukos Corporation received 510(k) clearance from the United States Food and Drug Administration (FDA) for the iStent infinite. It is a trabecular micro-bypass system indicated for use in a standalone procedure to reduce elevated intraocular pressure (IOP) in patients with primary open-angle glaucoma uncontrolled by prior medical and surgical therapy.

Ophthalmic Devices Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Demographic Shift and Increasing Prevalence of Eye Diseases

4.2.2 Rising Geriatric Population

4.2.3 Technological Advancements in Ophthalmic Devices

4.3 Market Restraints

4.3.1 Risk Associated with Ophthalmic Procedures

4.3.2 Poor Primary Healthcare Infrastructure in Developing and Under-Developed Countries

4.4 Porter's Five Force Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value – USD million)

5.1 By Devices

5.1.1 Surgical Devices

5.1.1.1 Glaucoma Drainage Devices

5.1.1.2 Glaucoma Stents and Implants

5.1.1.3 Intraocular Lenses

5.1.1.4 Lasers

5.1.1.5 Other Surgical Devices

5.1.2 Diagnostic and Monitoring Devices

5.1.2.1 Autorefractors and Keratometers

5.1.2.2 Corneal Topography Systems

5.1.2.3 Ophthalmic Ultrasound Imaging Systems

5.1.2.4 Ophthalmoscopes

5.1.2.5 Optical Coherence Tomography Scanners

5.1.2.6 Other Diagnostic and Monitoring Devices

5.1.3 Vision Correction Devices

5.1.3.1 Spectacles

5.1.3.2 Contact Lenses

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Mexico

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 United Kingdom

5.2.2.3 France

5.2.2.4 Italy

5.2.2.5 Spain

5.2.2.6 Rest of Europe

5.2.3 Asia- Pacific

5.2.3.1 China

5.2.3.2 Japan

5.2.3.3 India

5.2.3.4 Australia

5.2.3.5 South Korea

5.2.3.6 Rest of Asia-Pacific

5.2.4 Middle East and Africa

5.2.4.1 GCC

5.2.4.2 South Africa

5.2.4.3 Rest of Middle East and Africa

5.2.5 South America

5.2.5.1 Brazil

5.2.5.2 Argentina

5.2.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Alcon Inc.

6.1.2 Bausch Health Companies Inc.

6.1.3 Carl Zeiss Meditec AG

6.1.4 EssilorLuxottica SA

6.1.5 HAAG-Streit Group

6.1.6 Hoya Corporation

6.1.7 Johnson and Johnson

6.1.8 Nidek Co. Ltd

6.1.9 Topcon Corporation

6.1.10 Ziemer Ophthalmic Systems AG

6.1.11 Volk Optical, Inc.

6.1.12 Leica Microsystems

6.1.13 Optovue, Incorporated

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Ophthalmic Devices Industry Segmentation

As per the scope of the report, ophthalmology is a branch of medical science that deals with structure, function, and various diseases related to the eye. Ophthalmic devices are medical equipment designed for diagnosis, surgical, and vision correction purposes. The Ophthalmic Devices Market is Segmented by Devices (Surgical Devices (Glaucoma Drainage Devices, Glaucoma Stents and Implants, Intraocular Lenses, Lasers, and Other Surgical Devices), Diagnostic and Monitoring Devices (Autorefractors and Keratometers, Corneal Topography Systems, Ophthalmic Ultrasound Imaging Systems, Ophthalmoscopes, Optical Coherence Tomography Scanners, Other Diagnostic and Monitoring Devices), Vision Correction Devices (Spectacles, Contact Lenses) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| By Devices | ||||||||

| ||||||||

| ||||||||

|

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Ophthalmic Devices Market Research Faqs

How big is the Ophthalmic Devices Market?

The Ophthalmic Devices Market size is expected to reach USD 52.73 billion in 2024 and grow at a CAGR of 4.20% to reach USD 64.77 billion by 2029.

What is the current Ophthalmic Devices Market size?

In 2024, the Ophthalmic Devices Market size is expected to reach USD 52.73 billion.

Who are the key players in Ophthalmic Devices Market?

Alcon Inc., Bausch Health Companies Inc., Johnson and Johnson, Carl Zeiss Meditec AG and Ziemer Ophthalmic Systems AG are the major companies operating in the Ophthalmic Devices Market.

Which is the fastest growing region in Ophthalmic Devices Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Ophthalmic Devices Market?

In 2024, the North America accounts for the largest market share in Ophthalmic Devices Market.

What years does this Ophthalmic Devices Market cover, and what was the market size in 2023?

In 2023, the Ophthalmic Devices Market size was estimated at USD 50.52 billion. The report covers the Ophthalmic Devices Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Ophthalmic Devices Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

How are emerging markets influencing the growth of the Ophthalmic Devices Market?

The emerging markets are influencing the growth of the Ophthalmic Devices Market through a) Increasing demand in developing countries b) Investment opportunities

Ophthalmic Devices Industry Report

The global ophthalmic devices market is on an upward trajectory, fueled by the rising prevalence of vision disorders and an increasing demand for quality eye care. Technological advancements and the introduction of innovative products like micro-invasive glaucoma surgical implants and new contact lens technologies are driving significant growth. Ophthalmic companies are at the forefront, investing in R&D to meet the diverse needs of patients and healthcare providers. Despite challenges such as high device costs and low treatment rates in emerging nations, the market is expanding, especially in developing regions where there's a strategic focus on raising awareness of advanced corrective vision treatments. The market's growth is also supported by a detailed analysis provided by ����vlog��ý™ Industry Reports, which includes statistics on market share, size, revenue growth rate, and a forecast outlook. This comprehensive overview highlights the opportunities for ophthalmic companies to innovate and expand their customer base in a market set to continue its significant growth. Get a free report PDF download for a sample of this industry analysis.