Market Size of Turkey Property And Casualty Insurance Industry

| Study Period | 2024 - 2029 |

| Base Year For Estimation | 2023 |

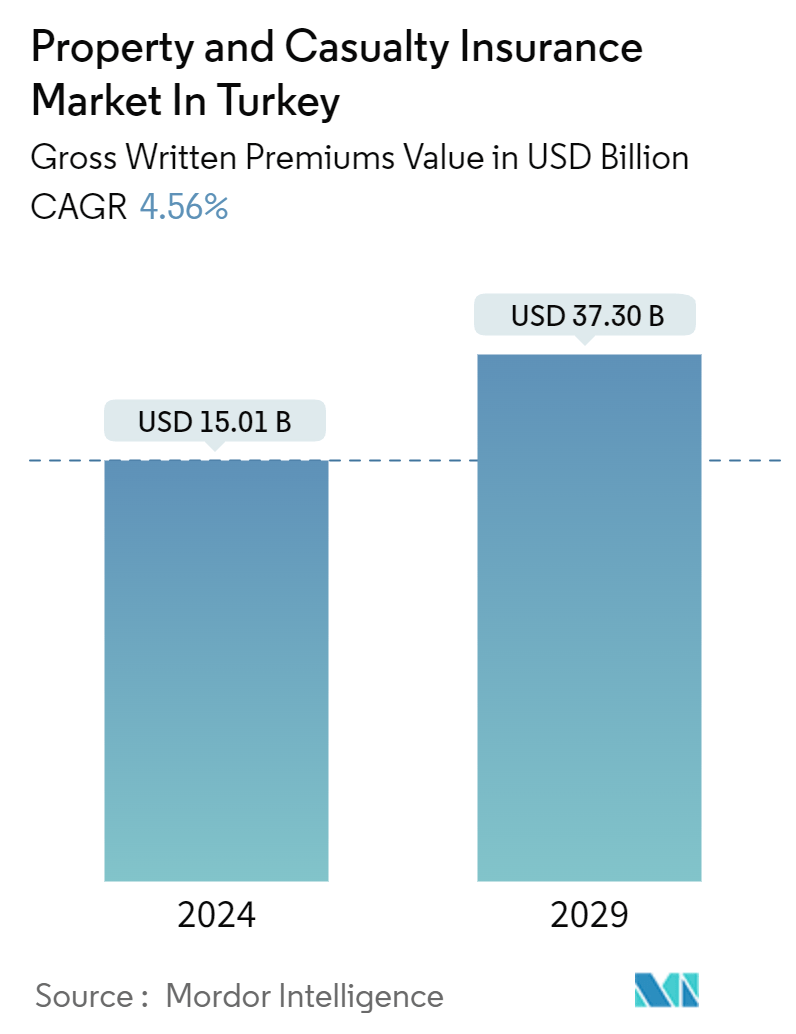

| Market Size (2024) | USD 15.01 Billion |

| Market Size (2029) | USD 37.30 Billion |

| CAGR (2024 - 2029) | 4.56 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Turkey Property and Casualty Insurance Market Analysis

The Property And Casualty Insurance Market In Turkey Market size in terms of gross written premiums value is expected to grow from USD 15.01 billion in 2024 to USD 37.30 billion by 2029, at a CAGR of 4.56% during the forecast period (2024-2029).

The Property and Casualty (P&C) insurance market represents a crucial segment of the broader insurance industry, offering indispensable protection against risks related to property damage and liability. This market includes various types of insurance, such as homeowners insurance, auto insurance, and commercial insurance, all of which are vital for individuals and businesses alike. As the P&C insurance sector adapts to emerging risks, technological advancements, and evolving consumer expectations, it remains a cornerstone of financial security and resilience.

The Rise of Digital Distribution Channels

Transformation through Technology: The increasing adoption of digital technologies in the P&C insurance industry is fundamentally altering the distribution landscape. Traditional agency-based models are now supplemented by direct and online channels, offering consumers enhanced convenience and flexibility. The proliferation of insurtech platforms has played a pivotal role in this transformation, utilizing data analytics and artificial intelligence to streamline underwriting processes and improve customer experience. This shift is enabling insurers to reach a broader audience, particularly tech-savvy consumers who prefer online transactions.

Impact on Market Competition: The growing preference for digital channels is intensifying competition within the P&C insurance market. Companies that invest in digital infrastructure and user-friendly platforms are gaining a competitive advantage by delivering personalized products and faster services. The integration of mobile apps and online portals for policy management and claims processing has become a standard expectation, pushing traditional insurers to innovate. This trend is driving efficiency, cost savings, and enhanced customer engagement across the industry.

Shifting Risk Landscape and Product Innovation

Emerging Risks and Insurance Solutions: The evolving risk landscape, influenced by factors such as climate change, cyber threats, and the complexities of global supply chains, is prompting insurers to innovate. The increasing frequency and severity of natural disasters have led to heightened demand for specialized property insurance products that address climate-related risks. Similarly, the rise in cyberattacks has spurred the development of cyber liability insurance, offering businesses protection against data breaches and other digital threats.

Adaptation through New Offerings: Insurers are expanding their product portfolios to address emerging risks, ensuring they remain relevant in a rapidly changing environment. The integration of advanced technologies, such as the Internet of Things (IoT) and blockchain, is enabling more accurate risk assessments and dynamic pricing models. These innovations are critical in helping the industry meet the evolving needs of consumers and businesses, driving growth in the P&C insurance market.

Turkey Property and Casualty Insurance Industry Segmentation

Property and casualty insurance encompasses a range of insurance policies designed to safeguard individuals and their belongings. Property insurance specifically safeguards possessions such as homes, vehicles, and more. This report aims to offer an extensive examination of the market under study. It delves into the market dynamics, identifies emerging trends within different segments and regional markets, and provides insights into various product and application types. Additionally, it evaluates the key players in the market and analyzes the competitive landscape. Turkey's property and casualty insurance market is segmented by insurance type and distribution channel. The market is segmented by insurance type into home, motor, and other insurance types. The market is segmented by direct, agency, bank, broker, and other distribution channels. The report offers market size and forecasts for Turkey's property and casualty insurance market in value (USD) for all the above segments.

| Insurance type | |

| Home | |

| Motor | |

| Other Insurance Types |

| Distribution Channels | |

| Direct | |

| Agency | |

| Bank | |

| Other Distribution Channels |

Turkey Property And Casualty Insurance Market Size Summary

The property and casualty insurance market in Turkey is experiencing a steady growth trajectory, driven by various factors including regulatory changes and the increasing demand for non-life insurance products. The market, which is predominantly consolidated with a few major players holding significant market shares, has shown resilience in the face of challenges posed by the COVID-19 pandemic. The pandemic has necessitated shifts in operational processes across the insurance value chain, prompting a greater reliance on digital solutions and remote assessments. Despite the initial negative impact on gross written premiums, the market has rebounded, with expectations of continued growth during the forecast period. The preference for purchasing insurance through banks, particularly for home building and contents insurance, highlights the evolving distribution channels in the market.

The Turkish property and casualty insurance sector is characterized by a strong focus on motor insurance, which dominates the non-life premiums, while other segments such as marine, aviation, and transit insurance are anticipated to grow significantly. The market's potential for further expansion is underscored by the low penetration of non-life insurance relative to GDP, attracting foreign investment and partnerships. The presence of the Turkish Catastrophe Insurance Pool mitigates some of the risks associated with natural disasters, allowing insurers to concentrate on motor business underwriting. The market's growth is supported by the involvement of both local and international companies, with key players like Allianz Sigorta A≈û and Axa Sigorta A≈û actively participating in the competitive landscape.

Turkey Property And Casualty Insurance Market Size - Table of Contents

-

1. MARKET DYNAMICS AND INSIGHTS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Growing Demand for Customized Insurance Policies

-

-

1.3 Market Restraints

-

1.3.1 Low Penetration Rate of Insurance in the Country

-

-

1.4 Market Opportunities

-

1.4.1 Demand for Innovative Insurance Products

-

-

1.5 Porter's Five Forces Analysis

-

1.5.1 Threat of New Entrants

-

1.5.2 Bargaining Power of Buyers/Consumers

-

1.5.3 Bargaining Power of Suppliers

-

1.5.4 Threat of Substitute Products

-

1.5.5 Intensity of Competitive Rivalry

-

-

1.6 Insights on Various Regulatory Trends Shaping Property and Casualty Insurance Market

-

1.7 Insights on Impact of Technology and Innovation in Operation in Property and Casualty Insurance Market

-

1.8 Impact of COVID-19 on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 Insurance type

-

2.1.1 Home

-

2.1.2 Motor

-

2.1.3 Other Insurance Types

-

-

2.2 Distribution Channels

-

2.2.1 Direct

-

2.2.2 Agency

-

2.2.3 Bank

-

2.2.4 Other Distribution Channels

-

-

Turkey Property And Casualty Insurance Market Size FAQs

How big is the Turkey Property And Casualty Insurance Market?

The Turkey Property And Casualty Insurance Market size is expected to reach USD 15.01 billion in 2024 and grow at a CAGR of 4.56% to reach USD 37.30 billion by 2029.

What is the current Turkey Property And Casualty Insurance Market size?

In 2024, the Turkey Property And Casualty Insurance Market size is expected to reach USD 15.01 billion.