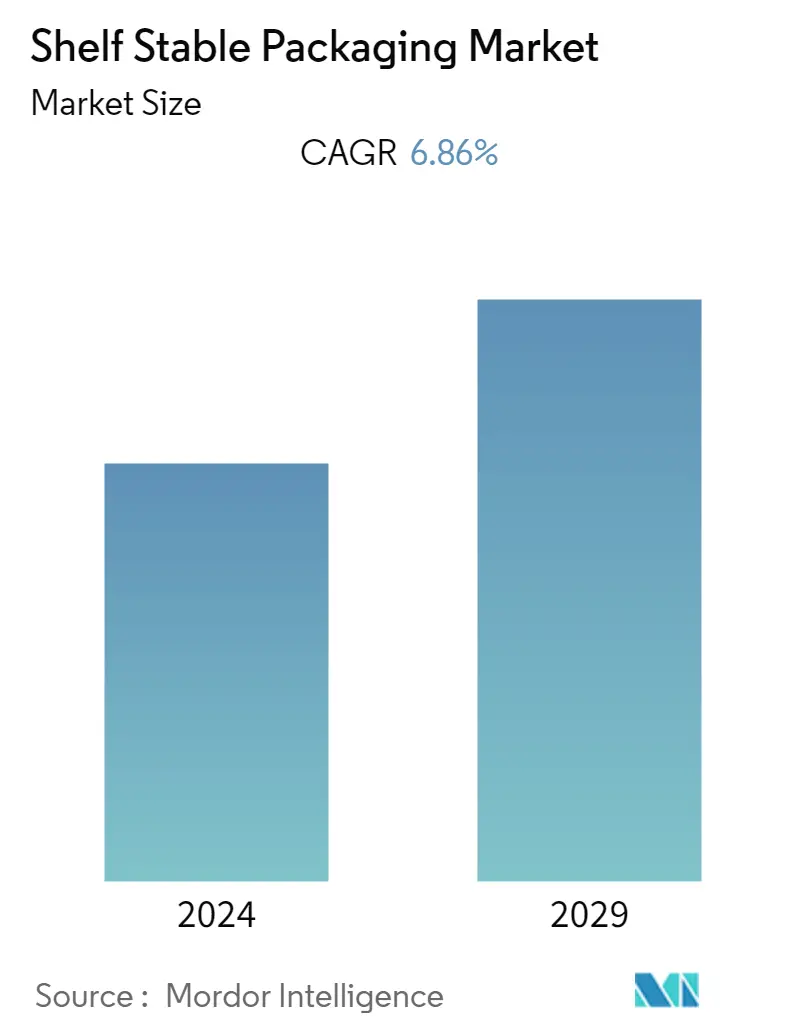

Shelf Stable Packaging Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 6.86 % |

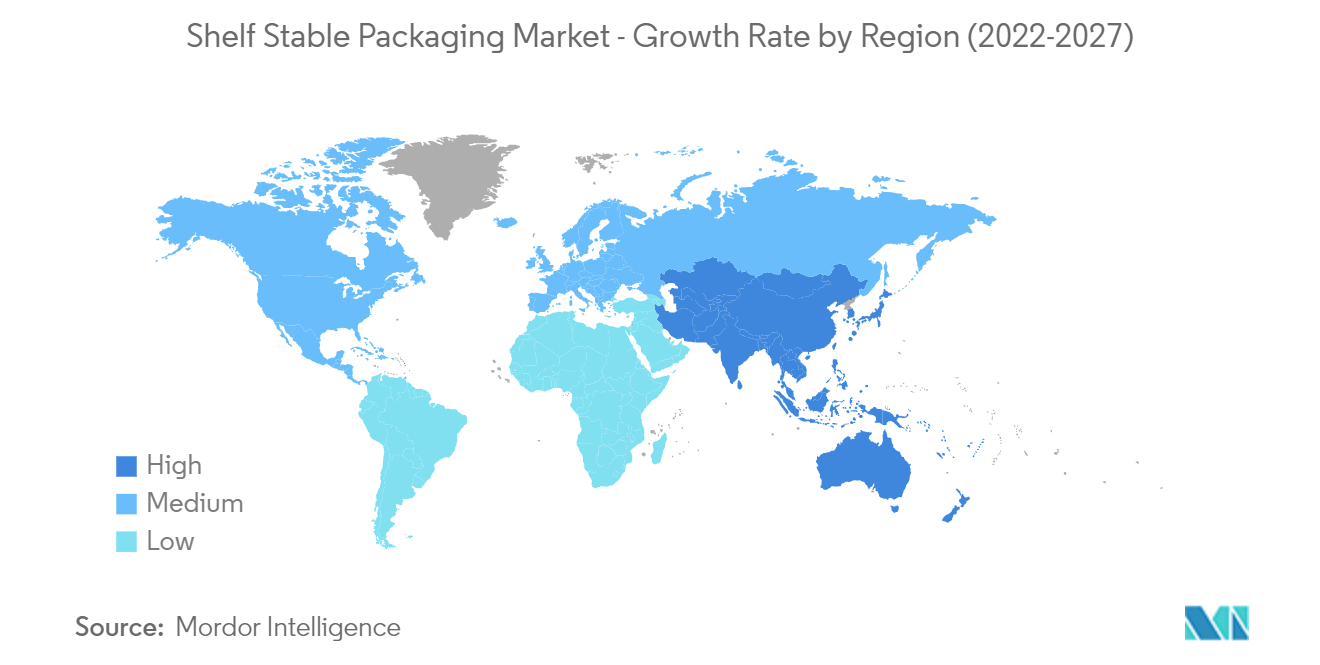

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

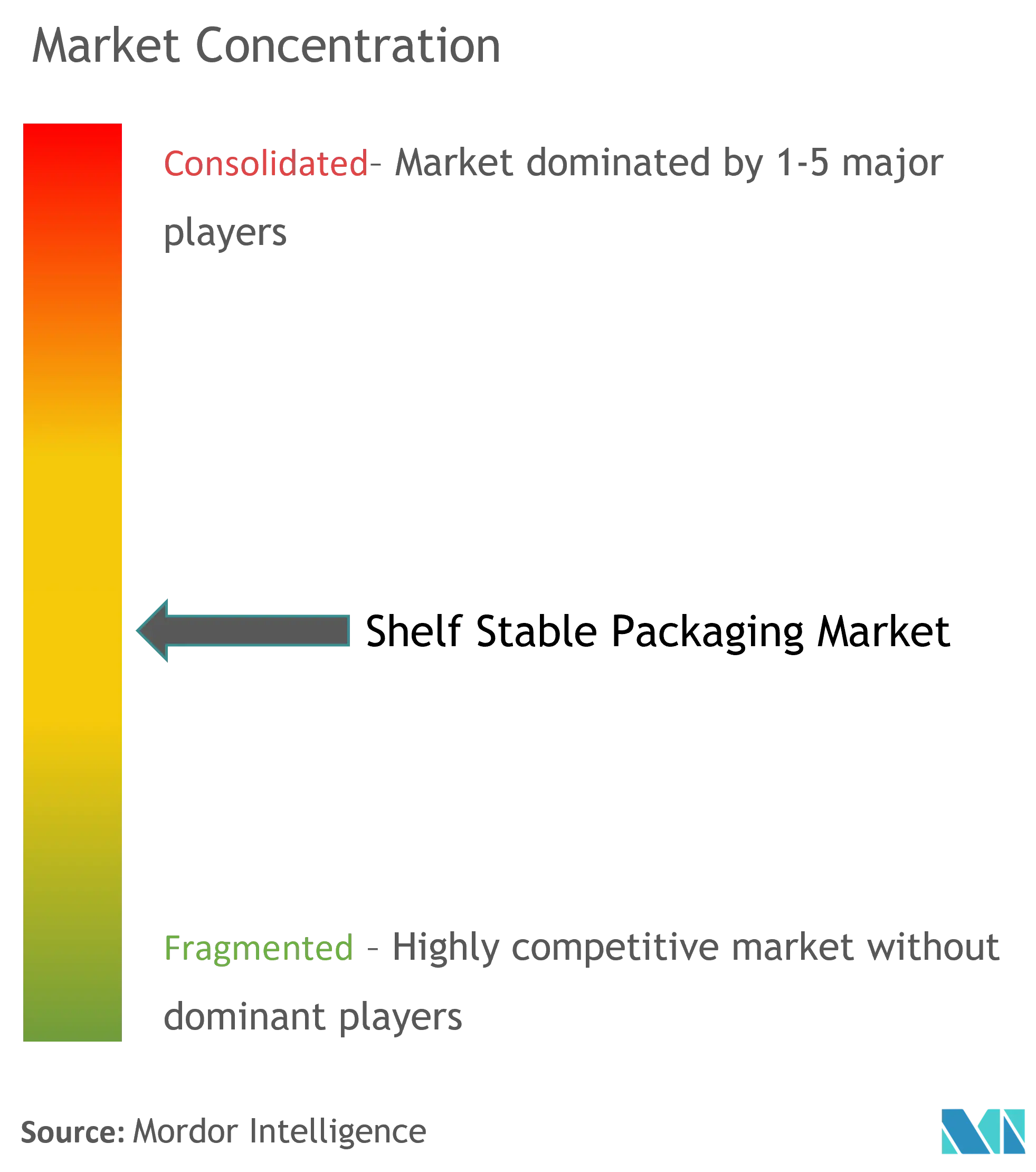

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Shelf Stable Packaging Market Analysis

The Shelf Stable Packaging Market is expected to record a CAGR of 6.86% during the forecast period. The perceptions of packaging among consumers have changed as a result of the COVID-19 pandemic. The number of consumers choosing packaged goods with a longer shelf life has increased. Additionally, COVID-19-related worries about food safety increased the demand for packaged foods, and it is anticipated that this trend will continue in the post-COVID market conditions as well.

- Rising demand for packaged food and beverages, increasing demand for Ready-to-Eat (RTE) food, the convenience of use, and increasing cost-effectiveness of shelf-stable packaging are primary factors supporting the market growth of the market worldwide.

- Climatic conditions and higher cost of refrigeration facilities are some of the major factors that are influencing packaging organizations to invest in packaging technologies that can improve the shelf life of products such as milk, value-added dairy products, food, and beverages.

- The novel food packaging techniques, viz. active packaging, intelligent packaging, and bioactive packaging, which involve intentional interaction with the food or its surroundings and influence on consumer's health, have been the major innovations in the field of packaging technology. These novel techniques act by prolonging the shelf life, enhancing or maintaining the quality, providing an indication, and regulating the freshness of food products.

- According to the 2022 PMMI State of the Industry, it has never been more crucial for packaging to be closed and sealed properly due to stricter health and safety regulations and producers looking to extend the shelf life of their products.

- All stakeholders benefit from increased shelf life. Processors frequently increase sales by expanding distribution to new markets. A sellable product can stay on store shelves for a longer period of time if it has a longer shelf life, which allows retailers to reduce the frequency of restocking and the losses caused by out-of-date products. Extended shelf life makes it simpler for consumers to keep a stocked pantry. Additionally, it lessens the quantity of food that is thrown away.

- COVID-19 has negatively impacted the market as the demand for food and beverage has witnessed growth, which has supported the market growth.

Shelf Stable Packaging Market Trends

This section covers the major market trends shaping the Shelf Stable Packaging Market according to our research experts:

Aseptic Packaging is the Fastest-growing Packaging Technology

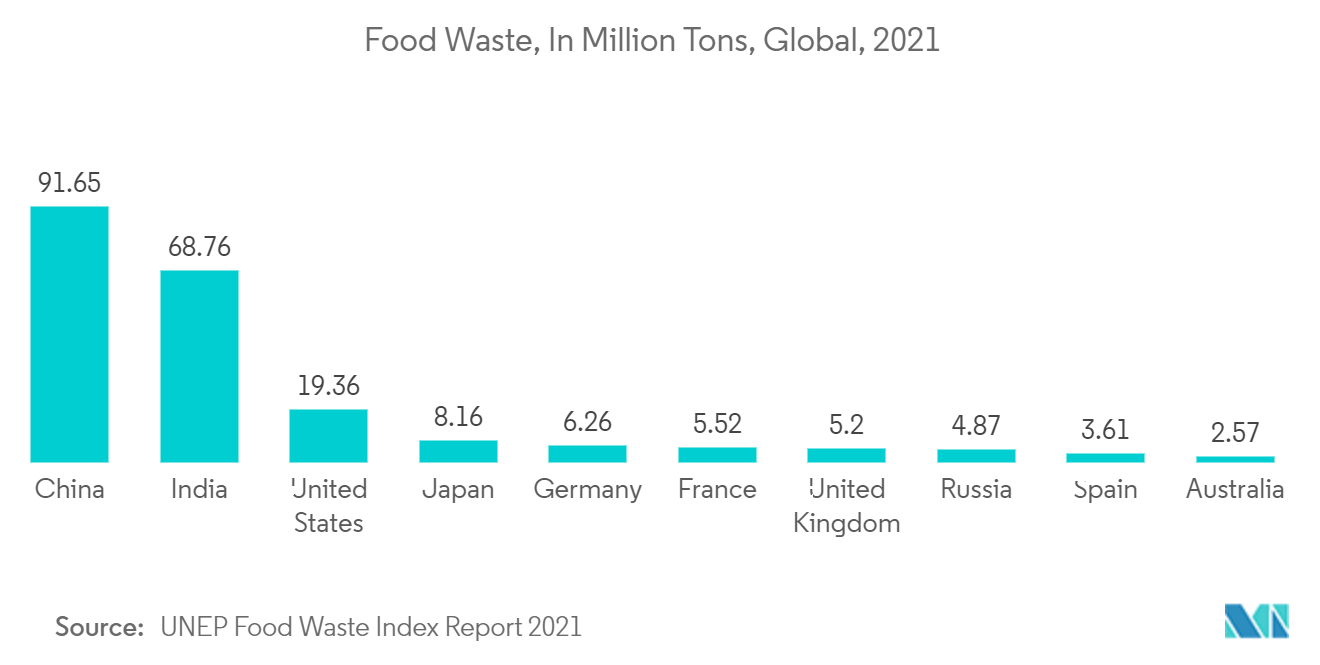

- Food waste is a crucial problem on the global level. Limited infrastructure, such as storage facilities, cold chains, connectivity, etc., results in a vast amount of food waste. The UNEP, FAO, and Project Drawdown estimated that 1.3 billion tons of food are wasted or lost annually (on a global scale), amounting to USD 2.6 trillion and 8-10% of greenhouse gas (GHG) emissions.

- The shelf life of food can be increased by using aseptic processing and packaging techniques which minimize food loss. Food is kept flavorful and safe using aseptic technology instead of refrigeration or preservatives. When food is packaged, aseptic technology ensures that both the food and the packaging materials are free of harmful bacteria, allowing food to retain more of its color, texture, flavor, and nutritional value.

- The pandemic has had a dramatic impact on the supply chain of the food and beverage industry in addition to its human cost. The supply chain has been hit hardest in the food and beverage sector. Globally, the pandemic also brought about a change in consumer behavior that resulted in high demand for food products with a longer shelf life.

- The food industry responded quickly to this demand, overcoming the challenging market conditions. As a result, the packaging industry reached new heights by integrating shelf stable packaging technologies, primarily aseptic food packaging.

- Food packaging has no longer just a passive role in protecting and marketing a food product. The emphasis on the decrease of the use of preservatives is also a driving factor for the use of aseptic packaging as aseptic food preservation methods enables processed food to be kept for longer period of time without preservatives, as long as they are not opened.

Asia-Pacific Expected to Record Highest CAGR

- Asia-Pacific region is expected to be one of the prominent markets for retort pouches owing to increasing consumer demand for greater convenience in food, beverage, packaging solutions.

- Furthermore, supermarkets and online stores are also increasingly becoming one of the important sources of ready-to-eat foods. They are gaining its space in developing countries, such as India and China, where the majority of the population is relying on the fast distribution channels to obtain ready-to-eat products at their own convenience, which has also been aiding the growth of the market.

- In Asia-Pacific, the market for retort pouch packaging in meat, poultry, and fish products is influenced by enduring qualities like sustainability, transparency, food safety, and reduction in food waste. According to Japan Canners Association, the retort food pouch product with the maximum production volume in Japan in 2021, at around 160 thousand tons, was curry. Sauces for dipping, at 51.58 thousand tons, followed next.

- Storage freezers and warehouses in the supermarket channel occasionally fall short in providing the conditions required to prevent product spoilage, leading to expensive product returns. The market for food and beverages faces challenges with shelf life due to improper handling and storage, a lack of modern facilities, and lengthy transportation times to remote locations in Asia-Pacific.

- Additionally, it can be challenging to satisfy client shelf-life requirements, particularly when there is fierce price competition. The degree to which processors navigate and get past these challenges related to shelf life can greatly influence how successful they are in the Asia-Pacific region. Therefore, end-user industries are increasingly using shelf stable packaging solutions to solve these challenges.

Shelf Stable Packaging Industry Overview

The Shelf Stable Packaging Market is competitive due to the presence of multiple vendors in the market. The market concentration of this market is medium, with the presence of some significant players adopting strategies such as product innovation, mergers, and acquisitions to gain some competitive advantage in this market.

- November 2022: The Bag-in-Box sustainable Fluids & Liquids packaging and dispensing solutions manufacturer Liquibox, a manufacturer of fresh food, beverage, consumer goods, and industrial end-markets, has signed a definitive agreement to be acquired by Sealed Air Corporation. Bag-in-Box is one the most efficient ways to package and dispense fluids & liquids. Due to its advantages in terms of sustainability and shelf life, this packaging format is becoming more prevalent even in mature industries.

- January 2022: In order to produce pharmaceutical-grade packaging, including shelf-stable bag in box, for its human milk-based nutrition products that cater to premature infants, global flexible packaging manufacturer Scholle IPN announced a partnership with LactaLogics.

Shelf Stable Packaging Market Leaders

-

Sealed Air Corporation

-

Spartech Corporation

-

Printpack

-

Silgan Holdings

-

DuPont

*Disclaimer: Major Players sorted in no particular order

Shelf Stable Packaging Market News

- July 2022: Aseptic Liqui-Sure and Aseptic Flip-N-Seal were launched by Liquibox. These aseptic-ready fitments give brands the option of bag-in-box dispensing. Both of the new products are aseptic-capable dispensing fittings that establish and maintain a hermetic seal to preserve the safety and freshness of liquids.

- March 2022: In order to cut down on waste and develop more sustainable supply chains, Mori, a food technology company, is focused on extending food's shelf life. The company announced that it raised USD 50 million in Series B1 financing. The Drawdown Fund, Blindspot, Acre Venture Partners, Refactor Capital, Closed Loop Partners, The Engine, Knollwood Investment Advisory, as well as new investors, Collaborative Fund and Thia Ventures, participated in the round, which was led by Prelude Ventures.

Shelf Stable Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Value Chain Analysis

4.3 Porters Five Force Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Demand to Reduce Cost of Cold Chain Logistics

5.1.2 Growing Demand for Ready-to-eat Food and Changing Consumer Lifestyle

5.2 Market Restraints

5.2.1 High Processing Requirements and Associated Costs

6. MARKET SEGMENTATION

6.1 By Packaging Format

6.1.1 Flexible

6.1.2 Rigid

6.2 By Packaging Material

6.2.1 Plastic

6.2.2 Metal

6.2.3 Glass

6.2.4 Paper and Paperboard

6.3 By Product Type

6.3.1 Metal Cans

6.3.2 Bottles

6.3.3 Jars

6.3.4 Cartons

6.3.5 Pouches

6.3.6 Other Product Type (Bag in Box, Cups, Trays, Bowls, etc)

6.4 By Packaging Technology

6.4.1 Asceptic Food Packaging

6.4.2 Retort Food Packaging

6.4.3 Hot Fill Food Packaging

6.4.4 Others

6.5 By End User Industry

6.5.1 Sauce & Condiment

6.5.2 Processed Fruit & Vegetable

6.5.3 Prepared Food

6.5.4 Juice

6.5.5 Dairy Food

6.5.6 Meat Poultry and Seafood

6.5.7 Others

6.6 Geography

6.6.1 North America

6.6.2 Europe

6.6.3 Asia Pacific

6.6.4 Latin America

6.6.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Mondi Group

7.1.2 Crown Holdings

7.1.3 Silgan Holdings

7.1.4 Reynolds Group

7.1.5 Ardagh Group

7.1.6 Tetra Pak

7.1.7 Berry Global

7.1.8 Printpack

7.1.9 DuPont

7.1.10 Sealed Air Corporation

7.1.11 Amcor PLC

7.1.12 PolyOne

7.1.13 APAK

7.1.14 Portland Pet Food Company

7.1.15 JHS Packaging

7.1.16 Bemis Company, Inc.

7.1.17 Spartech Corporation

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Shelf Stable Packaging Industry Segmentation

The market size reflects the value of shelf-stable packaging products packed with technologies such as aseptic food packaging, retort food packaging, hot fill food packaging, and more.

The shelf-stable packaging market is segmented by packaging format (flexible, rigid), packaging material (plastic, metal, glass, paper and paperboard), product type (metal cans, bottles, jars, cartons, pouches), packaging technology (sauce & condiment, processed fruit & vegetable, prepared food, juice, dairy food, meat poultry & seafood), and geography. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| By Packaging Format | |

| Flexible | |

| Rigid |

| By Packaging Material | |

| Plastic | |

| Metal | |

| Glass | |

| Paper and Paperboard |

| By Product Type | |

| Metal Cans | |

| Bottles | |

| Jars | |

| Cartons | |

| Pouches | |

| Other Product Type (Bag in Box, Cups, Trays, Bowls, etc) |

| By Packaging Technology | |

| Asceptic Food Packaging | |

| Retort Food Packaging | |

| Hot Fill Food Packaging | |

| Others |

| By End User Industry | |

| Sauce & Condiment | |

| Processed Fruit & Vegetable | |

| Prepared Food | |

| Juice | |

| Dairy Food | |

| Meat Poultry and Seafood | |

| Others |

| Geography | |

| North America | |

| Europe | |

| Asia Pacific | |

| Latin America | |

| Middle East and Africa |

Shelf Stable Packaging Market Research FAQs

What is the current Shelf Stable Packaging Market size?

The Shelf Stable Packaging Market is projected to register a CAGR of 6.86% during the forecast period (2024-2029)

Who are the key players in Shelf Stable Packaging Market?

Sealed Air Corporation, Spartech Corporation, Printpack, Silgan Holdings and DuPont are the major companies operating in the Shelf Stable Packaging Market.

Which is the fastest growing region in Shelf Stable Packaging Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Shelf Stable Packaging Market?

In 2024, the Asia-Pacific accounts for the largest market share in Shelf Stable Packaging Market.

What years does this Shelf Stable Packaging Market cover?

The report covers the Shelf Stable Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Shelf Stable Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Shelf Stable Packaging Industry Report

Statistics for the 2024 Shelf Stable Packaging market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Shelf Stable Packaging analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.