Simulation Software Market Size

| Study Period | 2019 - 2029 |

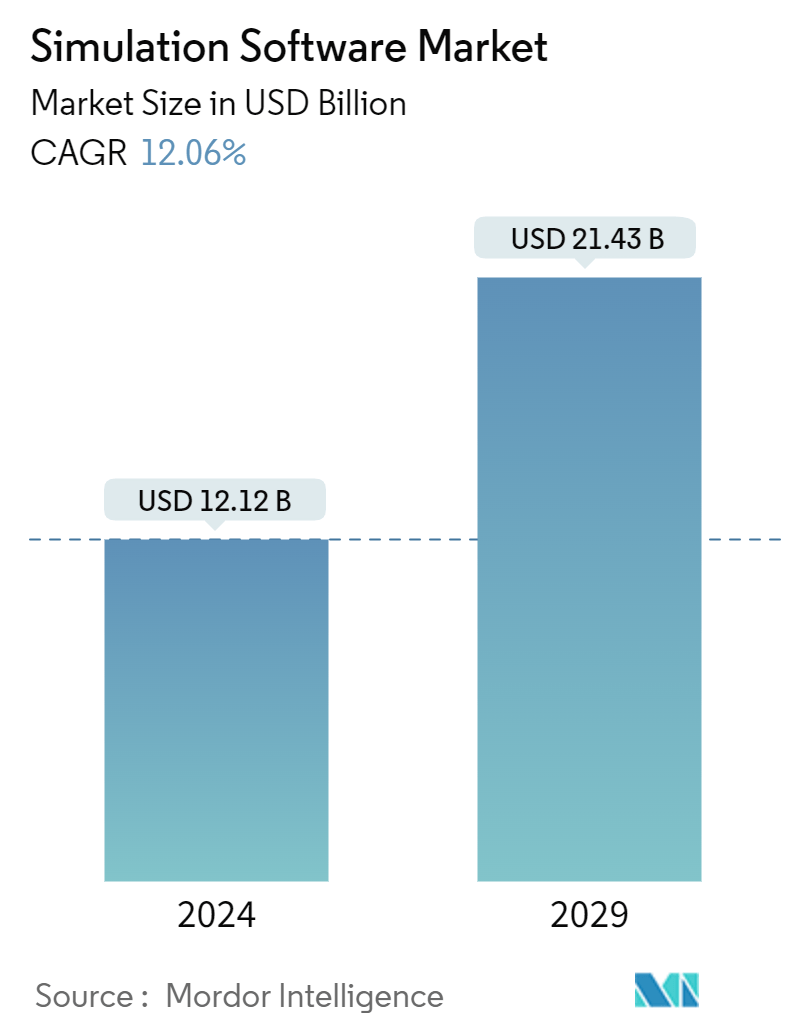

| Market Size (2024) | USD 12.12 Billion |

| Market Size (2029) | USD 21.43 Billion |

| CAGR (2024 - 2029) | 12.06 % |

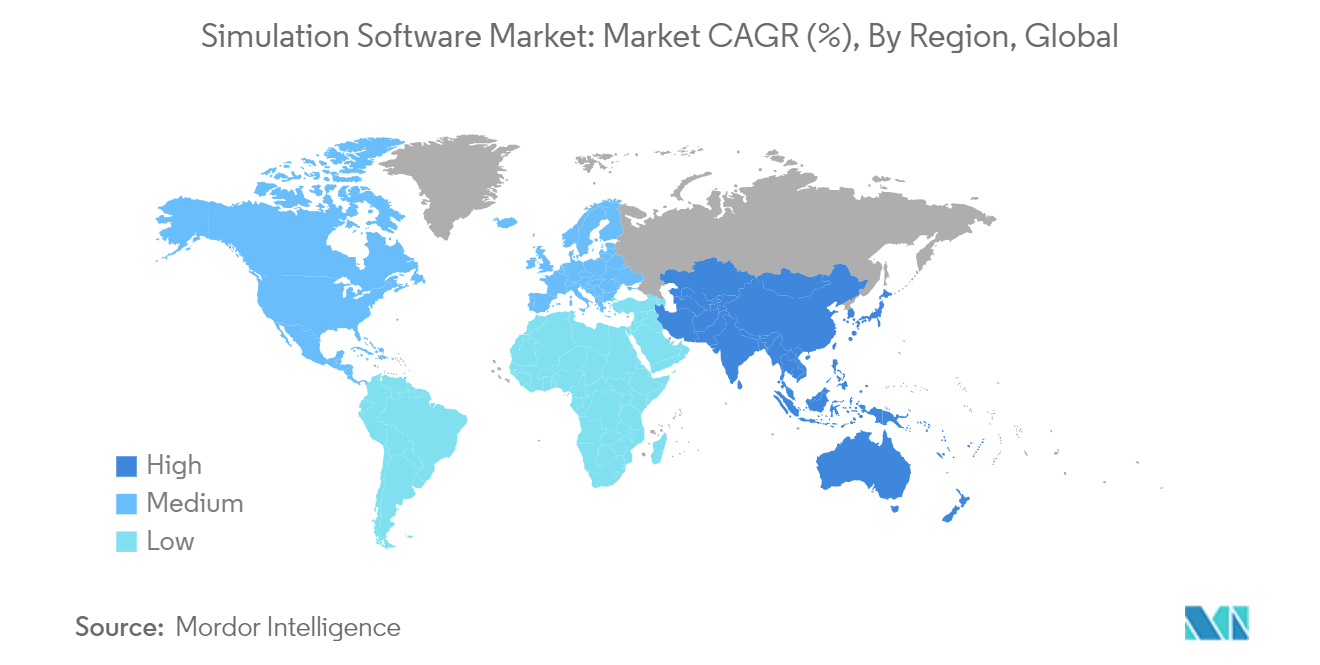

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

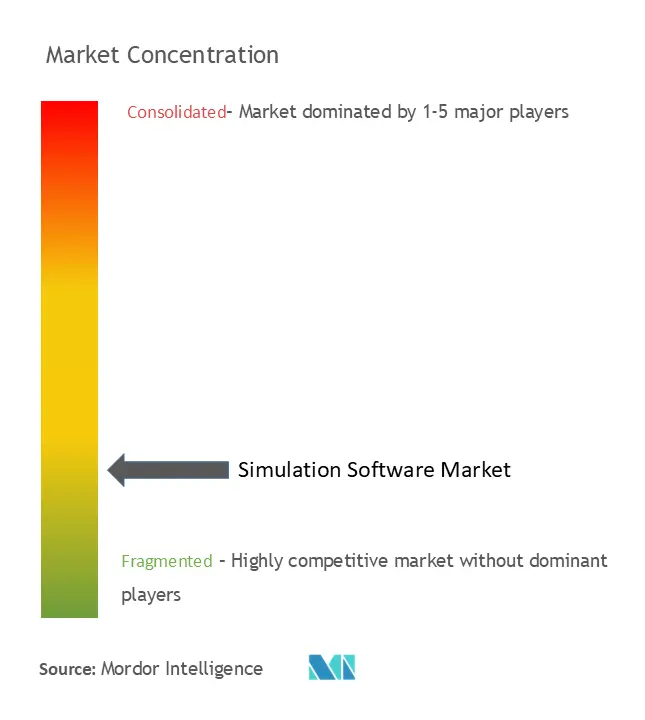

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Simulation Software Market Analysis

The Simulation Software Market size is estimated at USD 12.12 billion in 2024, and is expected to reach USD 21.43 billion by 2029, growing at a CAGR of 12.06% during the forecast period (2024-2029).

Simulation software is integral to industries that depend on advanced design, testing, and modeling environments. This technology is widely utilized across key sectors such as automotive, aerospace, defense, energy, telecommunications, and education. The software enables users to create digital prototypes, simulate real-world applications, and test complex systems without the need for physical experimentation. This leads to cost reduction, increased efficiency, and faster innovation cycles.

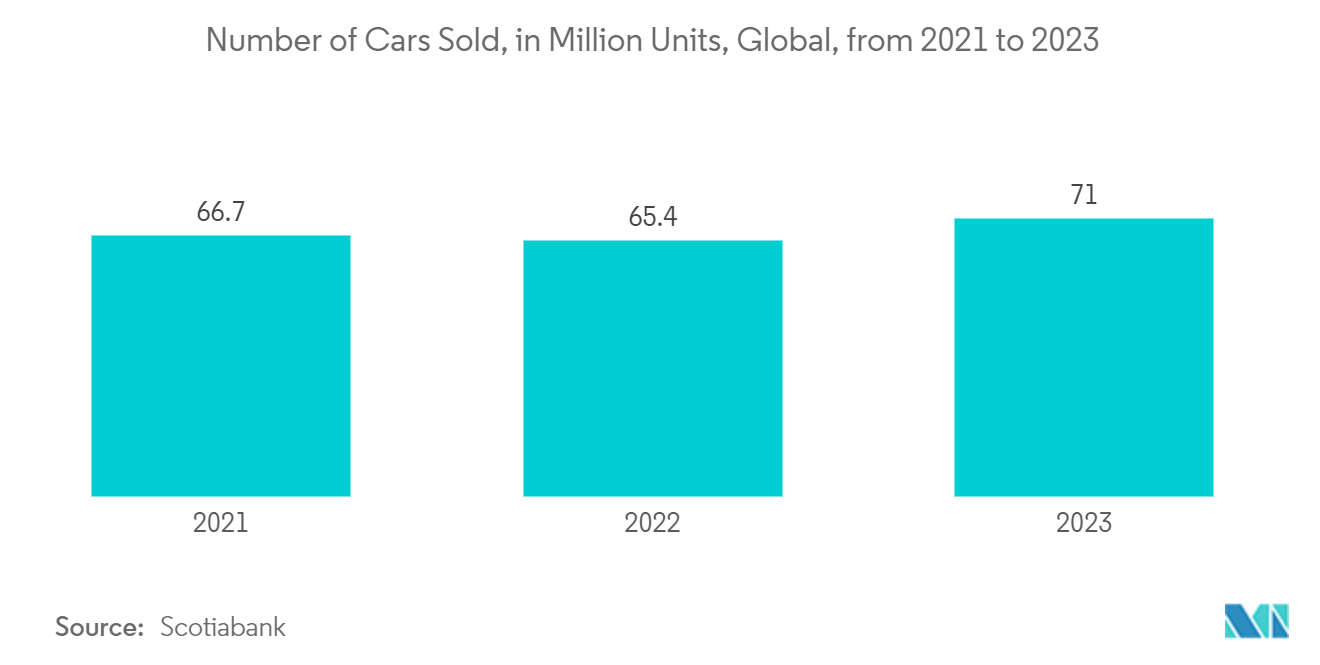

- Key Drivers: Automotive Industry's Impact on Growth The automotive sector is a significant contributor to the expansion of the simulation software market. The rising demand for electric vehicles (EVs) and autonomous driving technologies necessitates sophisticated simulation tools to design, test, and refine complex vehicle systems. These tools are essential for developing and optimizing powertrains, battery systems, and in-vehicle infotainment technologies. Similarly, in the aerospace and defense industries, simulation software is critical for modeling high-risk environments, improving safety and performance in aircraft design, and enhancing defense systems and mission-critical operations. In the energy sector, simulation software is increasingly adopted to optimize renewable energy systems such as wind and solar power, mitigating variability and unpredictability.

- Cloud-Based Simulation Software: A Growing Trend The market for cloud-based simulation software has experienced notable growth. Cloud platforms offer scalability, flexibility, and cost advantages over traditional on-premise solutions. With cloud-based systems, users can access powerful simulation tools over the internet, fostering collaboration and reducing the need for significant upfront infrastructure investments. This trend aligns with the broader industry shift toward digital transformation. Cloud-based solutions also support artificial intelligence (AI) and machine learning (ML) integration, enabling more efficient simulations and optimized workflows.

Rising Demand from the Automotive Sector

- Increased Need for EV Simulation: The surge in electric vehicle (EV) development has amplified the need for advanced simulation tools. Automakers leverage simulation software to design and test EV components, such as battery systems and charging infrastructure. By simulating real-world performance, manufacturers can identify potential issues during the early stages of development, reducing costs and time-to-market.

- Simulation for Autonomous Driving Technologies: Autonomous vehicles require extensive testing under various conditions, which can be difficult to replicate in the real world. Simulation software allows for the virtual testing of autonomous driving systems across multiple road and weather conditions, ensuring their safe operation in complex environments. Major automakers and technology firms have embraced these tools to accelerate the development of autonomous vehicles.

- Digital Twins Enhance Vehicle Development: Digital twins—virtual replicas of physical products—are increasingly used in automotive simulation to model in-vehicle technologies, from infotainment systems to safety features. By using digital twins, automakers can simulate performance under diverse conditions, improving user experience and vehicle safety.

The Growing Shift to Cloud-Based Simulation Solutions

- Flexibility and Scalability of Cloud Platforms: Cloud-based simulation software is gaining traction due to its inherent flexibility and scalability. These solutions allow companies of all sizes to access advanced simulation tools without heavy infrastructure investments. Cloud platforms support global collaboration, enabling engineers and designers to access and analyze simulation data in real-time.

- Cost-Effectiveness for SMEs: The subscription model of cloud-based simulation solutions reduces capital expenditure, making advanced tools accessible to small and medium enterprises (SMEs). This scalability allows users to adjust computational resources according to project needs, enhancing cost efficiency.

- AI and Machine Learning Integration: AI-driven simulation workflows can optimize design processes by running multiple scenarios in parallel, identifying the most efficient configurations. This capability is particularly valuable in manufacturing, where even minor gains in efficiency can result in significant cost savings.

Simulation Software Market Trends

Automotive Segment is Expected to Grow at a Faster Pace

- Automotive Segment Growth Accelerates:The automotive sector's reliance on simulation software continues to grow, driven by the need for virtual prototyping, crash testing, and system op mization. These tools help manufacturers improve vehicle safety and performance without the need for physical prototypes. Automotive suppliers are also adopting simulation technologies to reduce research and development (R&D) costs.

- Digital Twins in Automotive Performance Monitoring: The integration of digital twins in the automotive industry allows manufacturers to simulate real-time vehicle performance data, helping detect maintenance issues before they escalate. This proactive approach improves vehicle reliability while aligning with regulatory standards on emissions and safety. Simulation tools are vital in the development of EV batteries and testing, further expanding market opportunities.

- Real-Time Simulation Tools Gain Popularity: Real-time simulation software is becoming a pivotal tool for automotive manufacturers. Engineers use these systems to continuously test vehicle components, optimizing performance under various driving conditions. For instance, companies like BMW are developing simulation centers for autonomous driving technologies, helping accelerate the innovation of electric and autonomous vehicles.

- Cloud Platforms Enhance Market Efficiency: Cloud-based simulation platforms are providing cost-effective, scalable solutions for automotive companies. The ability to reduce testing times, enhance collaboration, and improve product quality is driving adoption among SMEs, further contributing to the sector's growth within the simulation software market.

North America Leads the Simulation Software Market

- Market Leadership in Technological Innovation: North America holds the largest share in the global simulation software market, underpinned by strong technological advancements and substantial R&D investments. The aerospace, automotive, and healthcare sectors are at the forefront of simulation software adoption. Major players, including Ansys, Dassault Systèmes, and Siemens, are driving innovation, helping industries optimize operations, reduce costs, and improve safety.

- Government Initiatives Fuel Market Growth: Regulatory pressures regarding sustainability and efficiency are spurring the adoption of simulation software across industries. For example, automotive manufacturers are investing in simulation tools to meet stringent emissions standards, aligning with governmental green economy goals. In the defense sector, government-backed projects depend on simulation software for mission planning and system development.

- Healthcare Sector Embraces Simulation Tools: In North America, the healthcare sector is increasingly utilizing simulation software for medical training, surgical planning, and medical device development. The complexity of these applications demands sophisticated simulation technologies, further driving market expansion beyond traditional engineering fields.

- Scalability with Cloud Platforms: The adoption of cloud-based simulation software continues to grow in North America, providing significant cost savings and enabling remote, real-time simulations. The ability to scale across organizations, from SMEs to large enterprises, is broadening the market share of simulation software in the region, cementing its leadership in the global industry outlook.

Simulation Software Industry Overview

Fragmented Market with Global Players: The simulation software market is highly fragmented, with a mix of multinational corporations and niche solution providers. Companies like Siemens AG, Autodesk Inc., and Rockwell Automation Inc. maintain dominant positions, while smaller entities contribute to innovation in specific industry applications. This competition fosters diverse advancements across sectors ranging from automotive to academic research.

Leading Companies Drive Innovation: Global players such as Siemens, Rockwell Automation, Schneider Electric, Autodesk, and Ansys are pushing technological boundaries in industries like aerospace, automotive, and manufacturing. Their strong R&D capabilities and market reach enable them to meet evolving customer needs while driving global growth in the simulation software market.

Key Trends: Cloud, AI, and Digital Twins: The integration of cloud-based solutions, AI, and digital twins is transforming the market. Companies that embrace these technologies are poised for success. To remain competitive, firms must prioritize software usability, cross-platform functionality, and cost-effective solutions, particularly for SMEs.

Simulation Software Market Leaders

-

Siemens AG

-

Rockwell Automation Inc.

-

Schneider Electric SE

-

Autodesk Inc.

-

Ansys Inc.

*Disclaimer: Major Players sorted in no particular order

Simulation Software Market News

- March 2023 - Simulations Plus, Inc., which offers modeling and simulation software for pharmaceutical development, revealed a partnership with the Institute of Medical Biology of the Polish Academy of Sciences to create novel compounds for RORγ/RORγT nuclear receptors using artificial intelligence in the ADMET Predictor software.

- January 2023 - Real-Time Innovations (RTI), the software framework organization for autonomous systems, reported its association with Ansys, a player in simulation software. This partnership accelerates developing, testing, and deploying high-performance and high-reliability distributed procedures by authorizing them to be simulated without their underlying hardware, which may have restricted availability or be cost-prohibitive.

Simulation Software Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Threat of New Entrants

4.2.2 Bargaining Power of Buyers/Consumers

4.2.3 Bargaining Power of Suppliers

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Impact of the COVID-19 on the Market

4.4 Market Drivers

4.4.1 Rising Demand from the Automotive Sector

4.4.2 The Growing Shift to Cloud-Based Simulation Solutions

4.5 Market Restraints

5. MARKET SEGMENTATION

5.1 Deployment Type

5.1.1 On-premise

5.1.2 Cloud

5.2 End-user Industry

5.2.1 Automotive

5.2.2 IT and Telecommunication

5.2.3 Aerospace and Defense

5.2.4 Energy and Mining

5.2.5 Education and Research

5.2.6 Electrical and Electronics

5.2.7 Other End-user Industries

5.3 Geography

5.3.1 North America

5.3.2 Europe

5.3.3 Asia

5.3.4 Australia and New Zealand

5.3.5 Latin America

5.3.6 Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles*

6.2.1 Altair Engineering Inc.

6.2.2 The MathWorks Inc.

6.2.3 Autodesk Inc.

6.2.4 Cybernet Systems Corp.

6.2.5 Bentley Systems Incorporated

6.2.6 PTC Inc.

6.2.7 CPFD Software LLC

6.2.8 Design Simulation Technologies Inc.

6.2.9 Synopsys Inc.

6.2.10 Siemens AG

6.2.11 Ansys Inc.

6.2.12 Dassault Systèmes SE

6.2.13 Simio LLC

6.2.14 Lanner Group Ltd

6.2.15 SIMUL8 Corporation

6.2.16 CONSELF Srl

6.2.17 SolidWorks Corporation

6.2.18 Rockwell Automation Inc.

6.2.19 The COMSOL Group

6.2.20 Schneider Electric SE

7. MARKET INVESTMENT ANALYSIS

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

Simulation Software Industry Segmentation

Simulation is the imitation of the operation of a real-world process or system. The act of simulating something first requires a mathematical model to be developed. This replicated model represents the key characteristics of the physical process. The model basically represents the system itself, whereas the simulation software runs the operation of the system over time.

The simulation software market is segmented by deployment (on-premise, cloud), end-user industry (automotive, IT and telecommunication, aerospace and defense, energy and mining, education and research), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Deployment Type | |

| On-premise | |

| Cloud |

| End-user Industry | |

| Automotive | |

| IT and Telecommunication | |

| Aerospace and Defense | |

| Energy and Mining | |

| Education and Research | |

| Electrical and Electronics | |

| Other End-user Industries |

| Geography | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Simulation Software Market Research FAQs

How big is the Simulation Software Market?

The Simulation Software Market size is expected to reach USD 12.12 billion in 2024 and grow at a CAGR of 12.06% to reach USD 21.43 billion by 2029.

What is the current Simulation Software Market size?

In 2024, the Simulation Software Market size is expected to reach USD 12.12 billion.

Who are the key players in Simulation Software Market?

Siemens AG, Rockwell Automation Inc., Schneider Electric SE, Autodesk Inc. and Ansys Inc. are the major companies operating in the Simulation Software Market.

Which is the fastest growing region in Simulation Software Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Simulation Software Market?

In 2024, the North America accounts for the largest market share in Simulation Software Market.

What years does this Simulation Software Market cover, and what was the market size in 2023?

In 2023, the Simulation Software Market size was estimated at USD 10.66 billion. The report covers the Simulation Software Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Simulation Software Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the major factors driving the Simulation Software Industry?

The major factors driving the Simulation Software Industry are a) Increased product development complexity b) Growing emphasis on product quality and innovation

What are the major factors driving the Simulation Software Industry?

The major factors driving the Simulation Software Industry are a) Increased product development complexity b) Growing emphasis on product quality and innovation

Simulation Software Industry Report

Simulation Software Market Research

Our industry research in the simulation software market delivers comprehensive insights into emerging trends, technological advancements, and sector-specific applications. The report covers a detailed analysis of key growth drivers, such as the increasing demand from the automotive sector for electric vehicle (EV) and autonomous driving simulations, along with the rising adoption of cloud-based solutions. Additionally, the report delves into how AI and digital twins are revolutionizing simulation processes across industries like aerospace, defense, energy, and manufacturing, providing stakeholders with actionable intelligence for strategic decision-making.

This market research report is designed to benefit a range of stakeholders, from SMEs to multinational corporations, by offering critical data on market segmentation, industry trends, and technology adoption rates. The report pdf format provides easy access to insights, helping companies optimize operational efficiency, reduce costs, and improve product quality through cutting-edge simulation tools. With a focus on cloud scalability, the integration of AI, and the expansion of digital twins, the report offers a forward-looking industry outlook crucial for maintaining a competitive edge in the global simulation software landscape.