Market Size of Singapore Payments Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

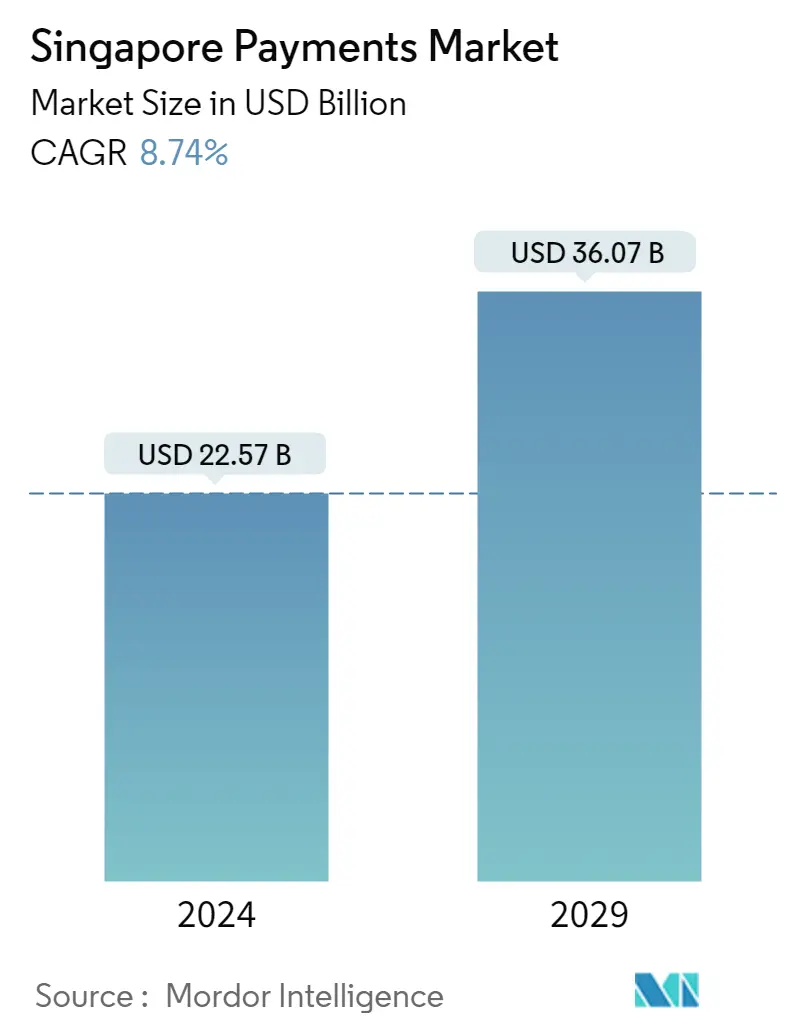

| Market Size (2024) | USD 22.57 Billion |

| Market Size (2029) | USD 36.07 Billion |

| CAGR (2024 - 2029) | 8.74 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Singapore Payments Market Analysis

The Singapore Payments Market size is estimated at USD 22.57 billion in 2024, and is expected to reach USD 36.07 billion by 2029, growing at a CAGR of 8.74% during the forecast period (2024-2029).

- The ongoing growth of real-time payments and the government's efforts to encourage digitalization are expected to drive market growth. With the government now allowing non-bank financial institutions (NFIs) to access banking retail payment infrastructure, instant payments in Singapore are set to increase even more. NFIs that have been granted a major payment institution licensed under the Payment Services Act are now permitted to link directly to FAST and PayNow.

- One of the primary goals of the Singapore government's Smart Nation vision is to build an e-payments society, which is one of the key goals. The payments sector in Singapore is now modern and open to new players. This industry is available to non-bank financial institutions (NFIs), promoting competition and interoperability among e-wallets. For instance, Grab, a ride-hailing firm, introduced GrabPay, and Singtel, a telecommunications company, introduced DashPay.

- Mobile phones (notably smartphones) have become an integral aspect of an individual's life as the global economy has grown rapidly. Furthermore, for most individuals worldwide, the internet has become an indispensable element of their daily lives. As a result, the number of cell phones and internet users has surged worldwide, resulting in a major expansion in the payments sector.

- Further, the latest Back to Business study by Visa revealed that the majority (94%) of small and micro businesses (SMBs) in the country were seeking to adopt new payment methods in 2022, with 89% saying doing so would be fundamental to their growth. Amongst the methods that SMBs were considering using are e-wallet apps (59%), mobile contactless payments (58%), contactless cards (43%), Buy Now Pay Later solutions (35%), and digital currencies (33%).

- As per the latest figures from the Singapore Police Force (SPF), the number of scam and cybercrime cases in the country hit an all-time high of 33,669 in 2022, with a 25.2% YoY increase. E-commerce was among the top five types of scams reported in Singapore. Scammers often use emails, text messages, or phone calls to deceive their targets. For instance, they pretend to be officials or trusted entities to convince victims to reveal their personal information, like bank accounts or credit card details. Scammers then use the data to carry out unauthorized transactions. Such trends may hinder market growth.

Singapore Payments Industry Segmentation

The payments market is segmented by two modes of payment - POS and e-commerce. E-Acommerce payments include online purchases of goods and services, such as purchases made on e-commerce websites and online booking of travel and accommodation. However, it does not include online purchases of motor vehicles, real estate, utility bill payments (such as water, heating, and electricity), mortgage payments, loans, credit card bills, or purchases of shares and bonds. As for POS, all transactions that occur at the physical point of sale are included in the market scope. It includes traditional in-store transactions and all face-to-face transactions, regardless of where they take place. Cash is also considered for both cases (cash-on-delivery for e-commerce sales).

Singapore's payments market is segmented by mode of payment (point of sale and online sale) and by end-user industry (retail, entertainment, healthcare, hospitality, and other end-user industries). The Market Sizes and Value (USD) Forecasts for all Segments are Provided.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Mode of Payment | ||||||

| ||||||

|

| By End-user Industry | |

| Retail | |

| Entertainment | |

| Healthcare | |

| Hospitality | |

| Other End-user Industries |

Singapore Payments Market Size Summary

The Singapore payments market is experiencing significant growth, driven by the increasing adoption of real-time payments and the government's push towards digitalization. The inclusion of non-bank financial institutions in the banking retail payment infrastructure has further accelerated this trend, allowing for greater competition and interoperability among digital payment platforms. The government's Smart Nation initiative aims to create an e-payments society, fostering an environment where new players like Grab and Singtel can introduce innovative payment solutions such as GrabPay and DashPay. The widespread use of smartphones and the internet has also contributed to the expansion of the payments sector, with a growing number of individuals relying on mobile and online payment methods.

The retail industry in Singapore is rapidly evolving, presenting numerous opportunities for payment providers to enhance their platforms and meet the increasing demand for digital payment solutions. The introduction of digital payment tokens and crypto payment solutions by companies like FOMO Pay highlights the region's commitment to embracing new technologies. The market is moderately competitive, with key players such as DBS PayLah, GrabPay, and PayPal actively expanding their presence. Government initiatives and partnerships, like DBS's collaboration with IATA and the trial of Purpose Bound Money by StraitsX and Grab, are expected to further intensify competition and drive innovation in the payments landscape.

Singapore Payments Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Stakeholder Analysis

-

1.3 Industry Attractiveness-Porter's Five Forces Analysis

-

1.3.1 Bargaining Power of Suppliers

-

1.3.2 Bargaining Power of Buyers/Consumers

-

1.3.3 Threat of New Entrants

-

1.3.4 Threat of Substitute Products

-

1.3.5 Intensity of Competitive Rivalry

-

-

1.4 Evolution of the payments landscape in the country

-

1.5 Key market trends pertaining to the growth of cashless transaction in the country

-

1.6 Impact of COVID-19 on the payments market in the country

-

-

2. Market Segmentation

-

2.1 By Mode of Payment

-

2.1.1 Point of Sale

-

2.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

-

2.1.1.2 Digital Wallet (includes Mobile Wallets)

-

2.1.1.3 Cash

-

2.1.1.4 Other Point of Sales

-

-

2.1.2 Online Sale

-

2.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

-

2.1.2.2 Digital Wallet (includes Mobile Wallets)

-

2.1.2.3 Other Online Sales (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

-

-

-

2.2 By End-user Industry

-

2.2.1 Retail

-

2.2.2 Entertainment

-

2.2.3 Healthcare

-

2.2.4 Hospitality

-

2.2.5 Other End-user Industries

-

-

Singapore Payments Market Size FAQs

How big is the Singapore Payments Market?

The Singapore Payments Market size is expected to reach USD 22.57 billion in 2024 and grow at a CAGR of 8.74% to reach USD 36.07 billion by 2029.

What is the current Singapore Payments Market size?

In 2024, the Singapore Payments Market size is expected to reach USD 22.57 billion.