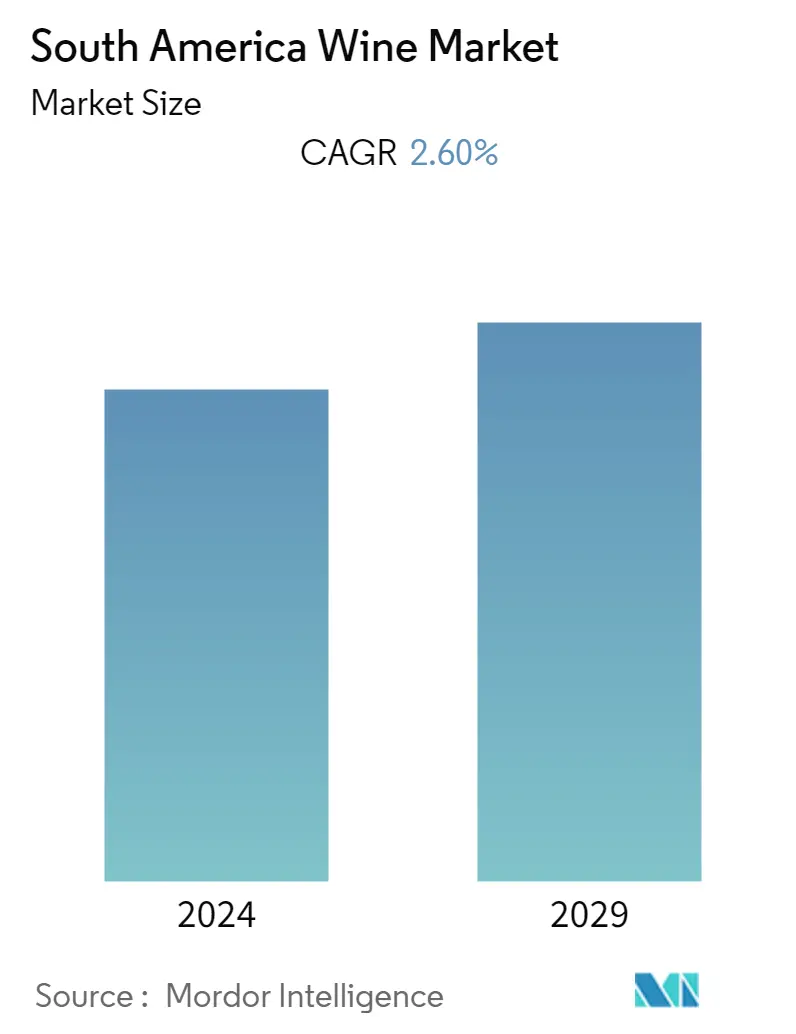

South America Wine Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | 2.60 % |

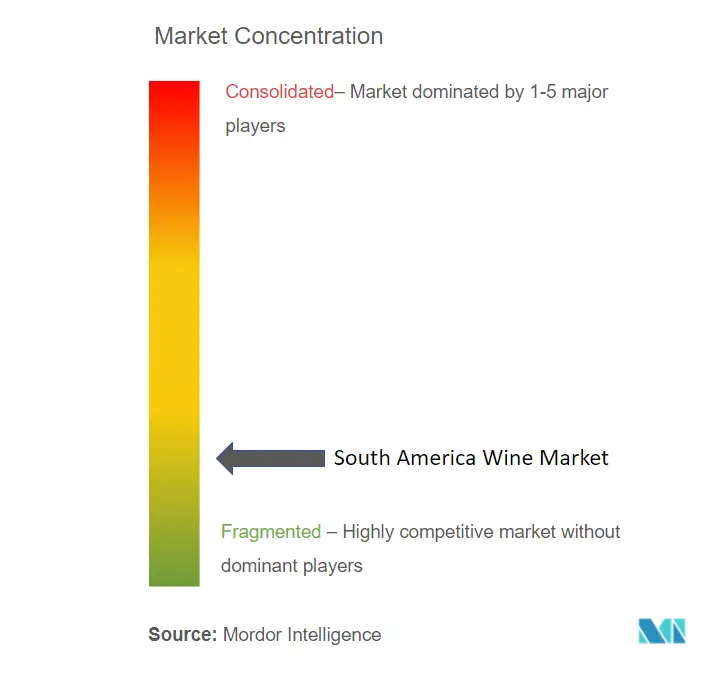

| Market Concentration | Medium |

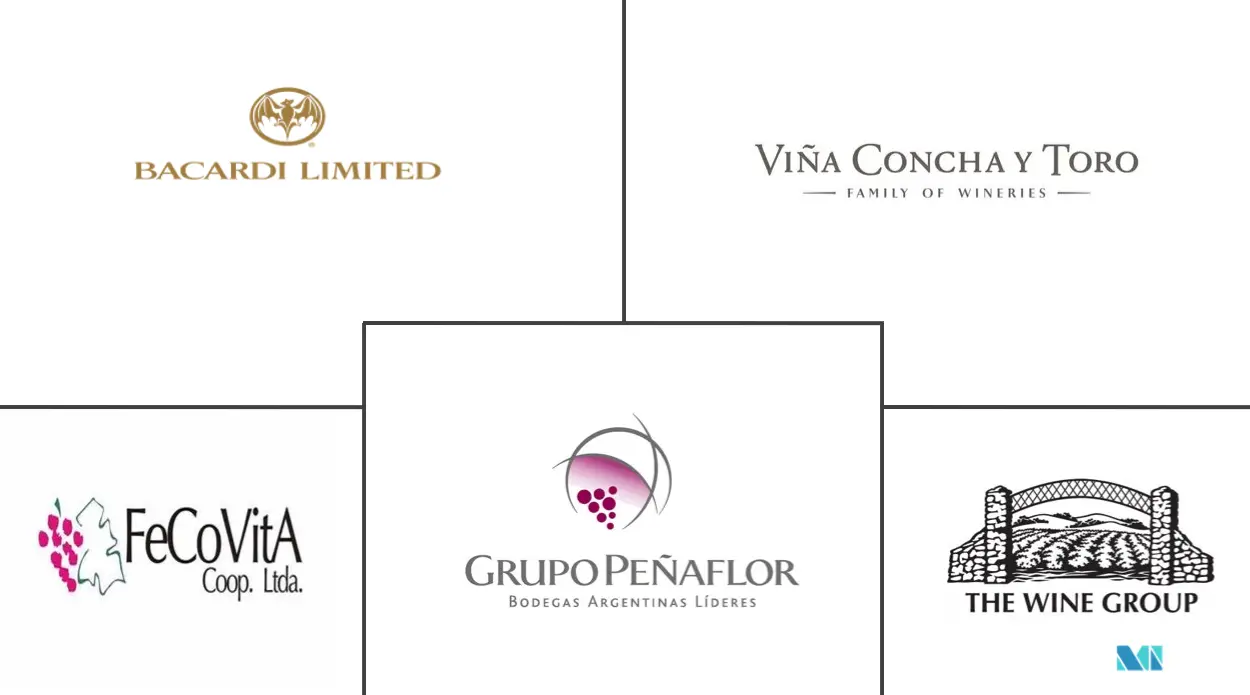

Major Players

*Disclaimer: Major Players sorted in no particular order |

South America Wine Market Analysis

The South America Wine market is projected to register a CAGR of 2.6% during the forecast period, 2022-2027.

The demand for wine in South America is anticipated to rise as a result of its health benefits, premiumization of wine goods, innovation in flavor, and more sophisticated distribution networks. The desire for fresh and unusual flavors like Riesling wine and other tropical fruit wines is predicted to increase, along with customer tastes and preferences changing.

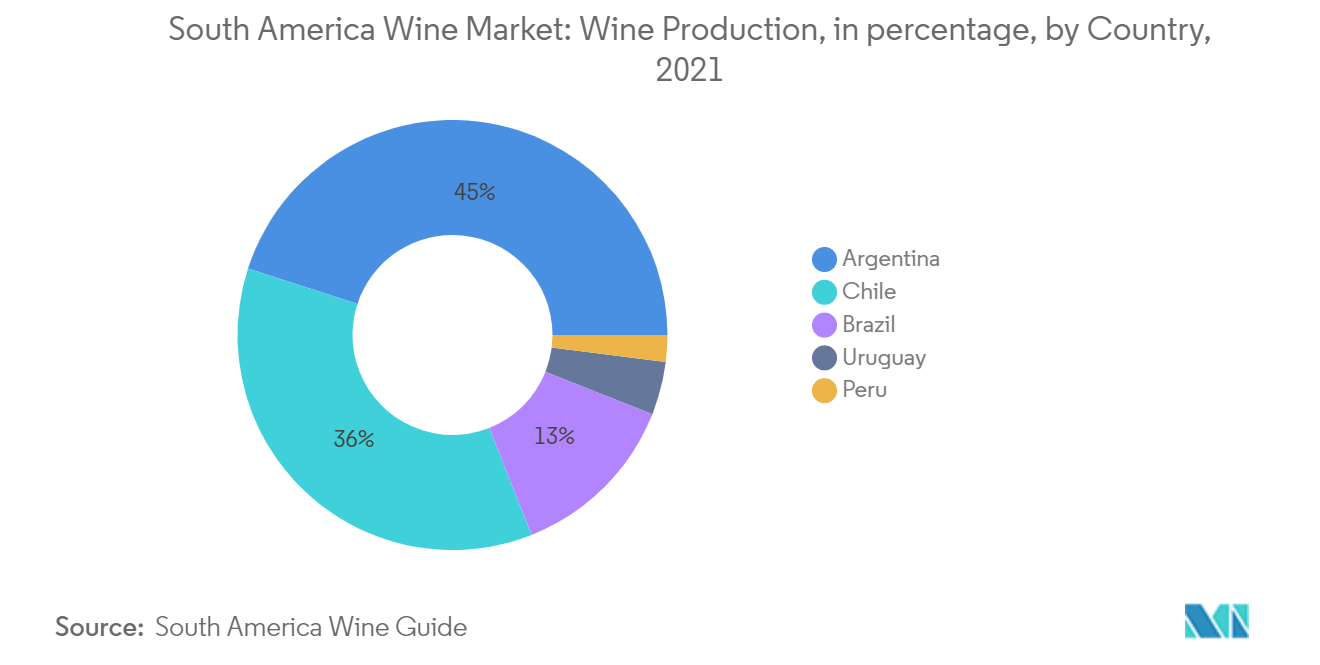

The South American wine industry is booming, and this is due to the region's special advantages. In terms of wine output, Chile is ninth in the world, only in front of Portugal, and Argentina is fifth. The use of more sophisticated production technologies was made possible by increased global trade and investment openness, which supported the alignment of countries like Chile and Argentina's wine industry with international standards.

Vineyards are protected from pests and diseases by the region's high altitude and low humidity. Due to this, Argentina's production costs are lower than those of other nations. Malbec, bonarda, and cabernet sauvignon are the primary red wine varieties produced in Argentina, whereas torrontes and chardonnay are the primary white wine varieties. Argentina's wine is more accessible, which is driving up import demand. For instance, in January 2022, Miami-based importer Origins Organic launched a new canned Argentine wine brand Le Petit Verre. The Malbec and Bubbly Rosé are Le Petit Verre's first offerings.

South America Wine Market Trends

This section covers the major market trends shaping the South America Wine Market according to our research experts:

Rising Number of Local Vineyards

The South American wine market is being driven by the rising number of vineyards. Local customers are drawn to these independently owned businesses because they place an emphasis on novel flavors and brewing techniques. As a result, there are now an increasing number of these vineyards spread out across the region. Every wine-producing location in South America has a distinctive microclimate, preferred wine grapes, and wine-making methods. Nearly all of South America's wines are produced in the continent's four largest wine-producing nations, Argentina, Brazil, Chile, and Uruguay, and there are many excellent wine varieties and bottles accessible. On the South American continent, Argentina is the nation that produces the highest wine. The Uco Valley's vineyards are the ones with the highest planting heights in the entire Mendoza region. Due to the climate created by the high altitude, wine grapes with a refined taste, high levels of acidity, and a distinctive crispness and finish can be produced. According to wine America, Argentina had about 15,451 vineyards, Chile had 12,361 vineyards, Brazil had 1,100 vineyards, and Colombia had 284 vineyards in 2020. The top 14 of the 50 Vineyards are in South America, there is a strong motivation to tour the area's vineyards in order to visit these14 wineries in South America.

Argentina holds a significant market share

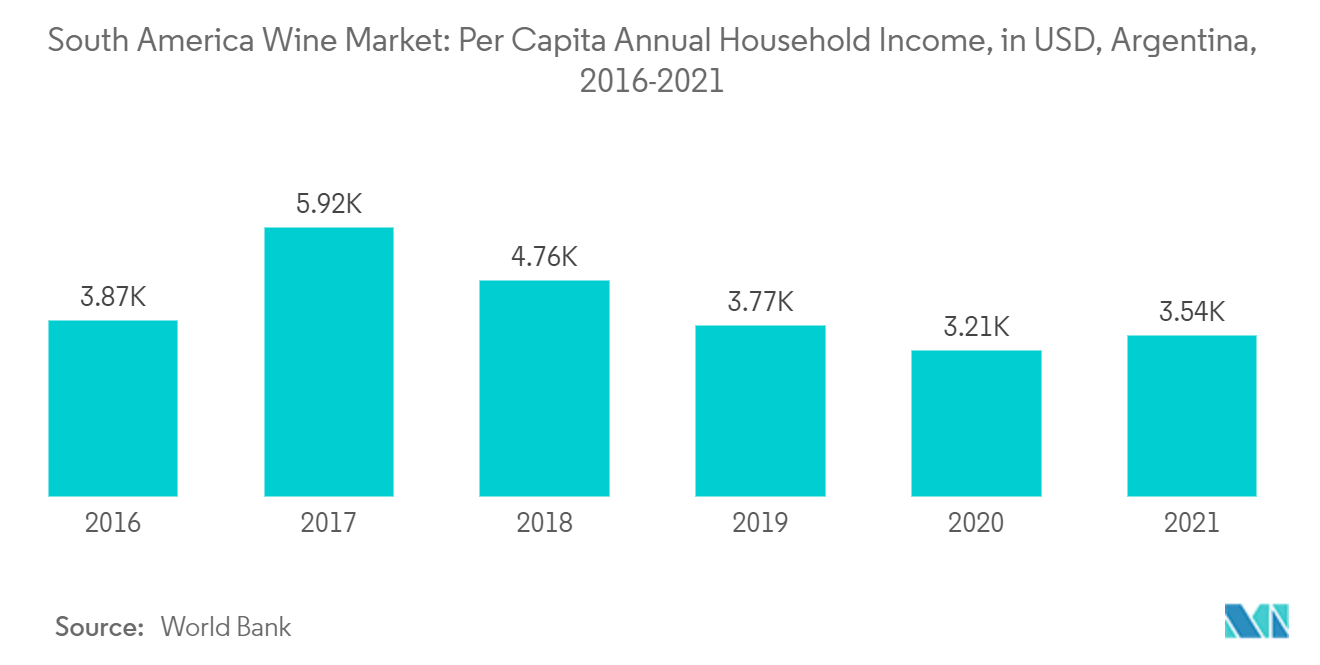

Argentina is one of the largest wine producers in the world. Mendoza is the most well-known and well-liked wine area in Argentina, there are several other areas including La Rioja, San Juan, and Salta. Argentina is known for a number of grape varietals, especially red ones like Malbec, owing to the ideal wine-growing environment. The rising disposable income among the young population coupled with the increasing trend of visiting pubs and bars in the country is primarily increasing consumer interest in spirits. There are about 2000 wineries located across the various wine regions of Argentina, many of which are open to tourists and provide wine tourism experiences. Argentina's wine tourism includes vineyard and winery tours, wine tastings, and accommodation. Argentina, which consumes 24 liters of wine per capita annually, is South America's top wine consumer in 2021, according to Land geist. As a result of the COVID-19 pandemic and subsequent lockdown, the alcohol consumption pattern has been drastically changed among consumers shifting from pubs and bars to their homes. With increasing at-home consumption, consumers in Argentina are more willing to pay a premium for high-quality wine. Therefore, the rising demand for diverse, innovative, and authentic high-end wine among millennials associated with changing consumer preference towards quality over quantity is increasing the demand for wine in Argentina and is expected to drive market growth in the forecast period.

South America Wine Industry Overview

The South American wine market is a highly competitive market due to many global and domestic companies operating in the region. The Wine Group, Vina Concha Y Toro, Fecovita Co-op, Grupo Penaflor, and Bacardi Limited are the market's leading companies. Due to their wide range of wine prices, these companies have a significant market share. A strong brand foundation is also greatly influenced by taste, type, and price. Due to their great brand awareness, well-known players are expanding their geographic reach, while other competitors are looking for mergers, acquisitions, and partnerships to take over regional market shares. For instance, in March 2021, Grupo Penaflor acquired Patritti winery, one of the major wineries in San Patricio del Chanar, Neuquen, Argentina. The Patritti winery, which produces wine on 110 hectares, has been added to the Grupo Penaflor portfolio along with Trapiche, Finca Las Moras, El Esteco, Mascota Vineyards, and Navarro Correas.

South America Wine Market Leaders

-

The Wine Group

-

Vina Concha Y Toro

-

Fecovita Co-op.

-

Grupo Penaflor

-

Bacardi Limited

*Disclaimer: Major Players sorted in no particular order

South America Wine Market News

- In May 2022, Concha Y Toro's brand Diablo launched its first White Wine. It is a seductive wine with notes of passion fruit and mango. This wine is versatile, especially recommended to pair with oily fish, seafood, and pasta with creamy sauces.

- In march 2021, Wines of Argentina, the parent company of the Vino Argentino brand started a new innovation program for Argentine wineries to enhance their online presence. The program consists of a series of online and in-person sessions where vineyards collaborate on significant tasks. These include non-traditional branding, the production and distribution of content, online networking, and the activation of events and channels.

- In February 2020, Fecovita launched a range of Argentinian wines made with British palates in consideration. A pair of "Reserve" wines, a group of more expensive Uco Valley Estate Malbec, Cabernet Sauvignon, and Cabernet Franc, and an expensive Uco Valley Single Vineyard Malbec make up the three tiers of the range.

South America Wine Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Drivers

4.2 Market Restraints

4.3 Porter's Five Force Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 By Type

5.1.1 Still Wine

5.1.2 Sparkling Wine

5.1.3 Fortified Wine

5.1.4 Vermouth

5.2 By Color

5.2.1 Red Wine

5.2.2 Rose Wine

5.2.3 White Wine

5.3 By Distriburtion Channel

5.3.1 On-Trade

5.3.2 Off-Trade

5.3.2.1 Supermarkets/Hypermarkets

5.3.2.2 Specialty Stores

5.3.2.3 Online Retailers

5.3.2.4 Other Distribution Channels

5.4 By Geography

5.4.1 Argentina

5.4.2 Brazil

5.4.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Most Adopted Strategies

6.2 Market Share Analysis

6.3 Company Profiles

6.3.1 The Wine group

6.3.2 Grupo Penaflor

6.3.3 Bacardi Limited

6.3.4 Cara Sur

6.3.5 Vina Concha Y Toro

6.3.6 Fecovita Co-op.

6.3.7 Bouchon Wine Limited

6.3.8 Bodegas Esmeralda

6.3.9 Casa Valduga

6.3.10 The Miolo Wine Group

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. IMPACT OF COVID-19 ON THE MARKET

9. DISCLAIMER

South America Wine Industry Segmentation

Wine is an alcoholic drink typically made from fermented grape juice. The South America Wine market is segmented by product type, color, distribution channel, and geography. Based on product type market is segmented into still wine, sparkling wine, fortified wine, and vermouth. Based on the color market is segmented into red wine, rose wine, and white wine, By distribution channel, the market is divided into on-trade and off-trade. Off-trade is further segmented into supermarkets/hypermarkets, specialty stores, online retailers, and other distribution channels. Based on geography market is segmented into Brazil, Argentina, and Rest of South America. For each segment, the market sizing and forecast have been done based on value (in USD million).

| By Type | |

| Still Wine | |

| Sparkling Wine | |

| Fortified Wine | |

| Vermouth |

| By Color | |

| Red Wine | |

| Rose Wine | |

| White Wine |

| By Distriburtion Channel | ||||||

| On-Trade | ||||||

|

| By Geography | |

| Argentina | |

| Brazil | |

| Rest of South America |

South America Wine Market Research FAQs

What is the current South America Wine Market size?

The South America Wine Market is projected to register a CAGR of 2.60% during the forecast period (2024-2029)

Who are the key players in South America Wine Market?

The Wine Group, Vina Concha Y Toro, Fecovita Co-op., Grupo Penaflor and Bacardi Limited are the major companies operating in the South America Wine Market.

What years does this South America Wine Market cover?

The report covers the South America Wine Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the South America Wine Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

South America Wine Industry Report

Statistics for the 2024 South America Wine market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. South America Wine analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.