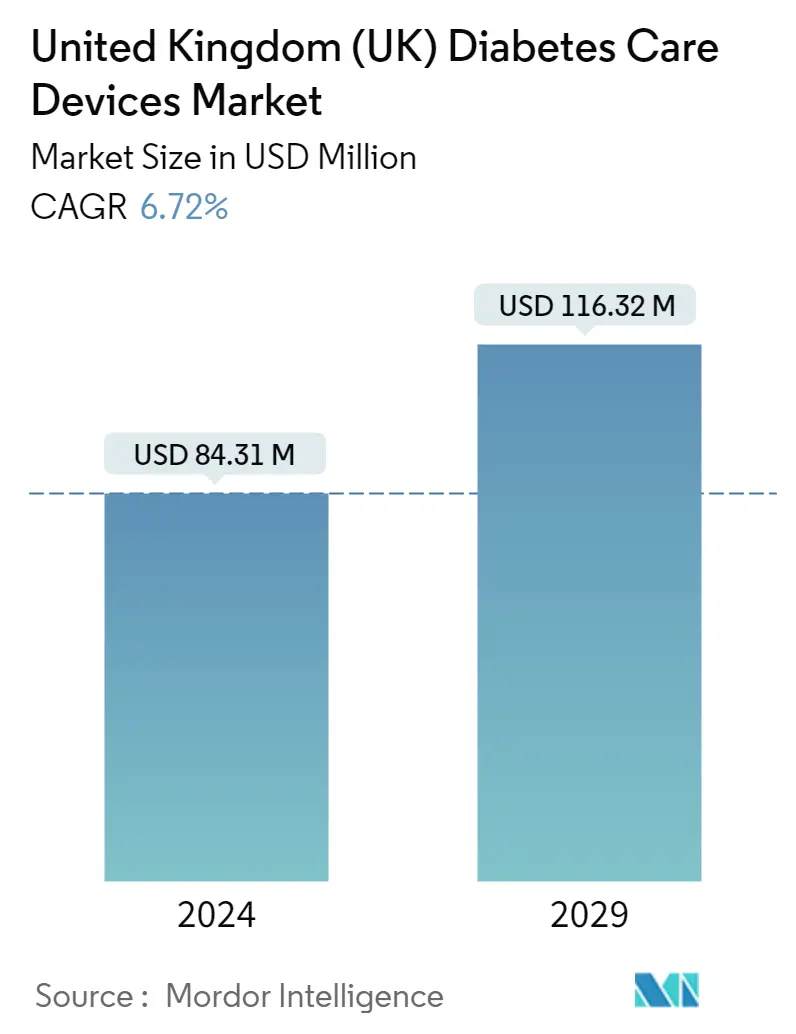

UK Diabetes Devices Market Size

| Study Period | 2018 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Market Size (2024) | USD 84.31 Million |

| Market Size (2029) | USD 116.32 Million |

| CAGR (2024 - 2029) | 6.72 % |

Major Players

*Disclaimer: Major Players sorted in no particular order |

UK Diabetes Devices Market Analysis

The United Kingdom Diabetes Care Devices Market size is estimated at USD 84.31 million in 2024, and is expected to reach USD 116.32 million by 2029, growing at a CAGR of 6.72% during the forecast period (2024-2029).

The COVID-19 pandemic had a substantial impact on the United Kingdom's diabetes care devices. According to The British Diabetic Association, 'The pandemic has had, and continues to have, a huge impact on our society. However research and data have shown that people with diabetes have been disproportionately affected by COVID-19, particularly in terms of poorer outcomes when contracting the virus. That's why preventing or delaying cases of type 2 diabetes is more important than ever before.'

The pandemic also highlighted opportunities for continuing and expanding innovations in the delivery of diabetes care, through virtual consultations between healthcare providers and people with diabetes, and the use of diabetes technology. Crisis management has created unprecedented interest in remote care from both patients and providers and removed many long-standing regulatory barriers. Thus, the COVID-19 outbreak increased the diabetes care device market's growth.

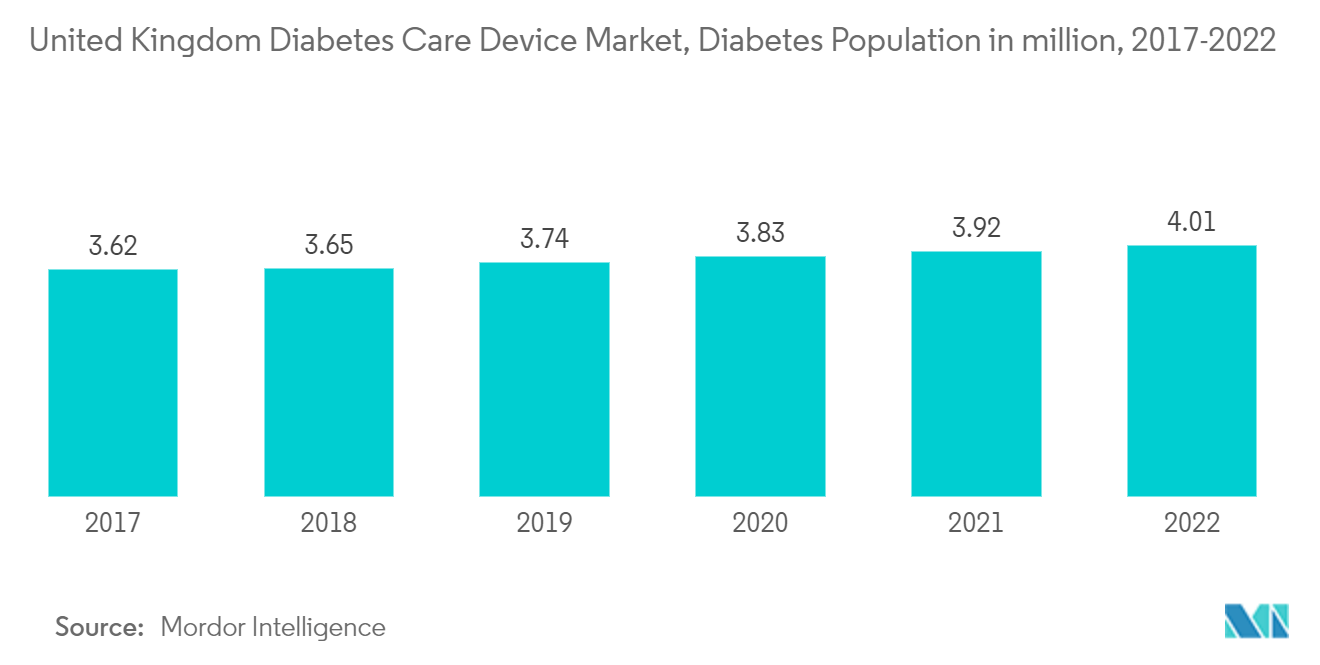

The rate of newly diagnosed cases of Type 1 and Type 2 diabetes is seen to increase, mainly due to obesity, unhealthy diet, and physical inactivity. The rapidly increasing incidence and prevalence of diabetic patients and healthcare expenditure are indications of the increasing usage of diabetic care products. According to The British Diabetic Association, Diabetes prevalence 2021 data shows an increase in the number of people living with a diabetes diagnosis in the UK: an increase of more than 150,000 from 2020. It is estimated that more than 13.6 million people are at increased risk of type 2 diabetes in the UK. At this rate, the number of people with diabetes, including the undiagnosed population, is expected to rise to 5.5 million by 2030.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

UK Diabetes Devices Market Trends

Continuous Glucose Monitoring Segment is Expected to Witness a Healthy Growth Rate Over the Forecast Period

The continuous Glucose Monitoring Segment recorded more than USD 1.8 billion in revenue in the current year, which is expected to register further with a CAGR of more than 11.3% during the forecast period.

To use a CGM, a small sensor is inserted into the abdomen or arm with a tiny plastic tube known as a cannula penetrating the top layer of skin. An adhesive patch holds the sensor in place, allowing it to take glucose readings in interstitial fluid throughout the day and night. Generally, the sensors must be replaced every 7 to 14 days. A small, reusable transmitter connected to the sensor allows the system to send real-time readings wirelessly to a monitor device that displays blood glucose data. Some systems contain a dedicated monitor, and some display the information via a smartphone app.

Continuous glucose monitoring sensors use glucose oxidase to detect blood sugar levels. Glucose oxidase converts glucose to hydrogen peroxidase, which reacts with the platinum inside the sensor, producing an electrical signal to be communicated to the transmitter. Sensors are the most important part of continuous glucose monitoring devices. Researchers are trying to find and develop alternatives to electrochemical-based glucose sensors and create more affordable, minimally invasive, and user-friendly CGM sensors. Optical measurement is a promising platform for glucose sensing. Some technologies with high potential in continuous glucose sensing are reported, including spectroscopy, fluorescence, holographic technology, etc. Eversense, a CGM sensor based on fluorescence sensing developed by Senseonics Company, presents a much longer lifespan than electrochemical sensors. Technological advancements to improve the accuracy of the sensors are expected to drive segment growth during the forecast period.

The frequency of monitoring glucose levels depends on the type of diabetes, which varies from patient to patient. Type-1 diabetic patients need to check their blood glucose levels regularly to monitor their blood glucose levels and adjust the insulin dosing accordingly. The current CGM devices show a detailed representation of blood glucose patterns and tendencies compared to a routine check of glucose levels at set intervals. Furthermore, the current continuous glucose monitoring devices can either retrospectively display the trends in blood glucose levels by downloading the data or give a real-time picture of glucose levels through receiver displays. Continuous glucose monitoring devices are becoming cheaper with the advent of new technologies, like cell phone integration, which is likely to drive the segment growth during the forecast period.

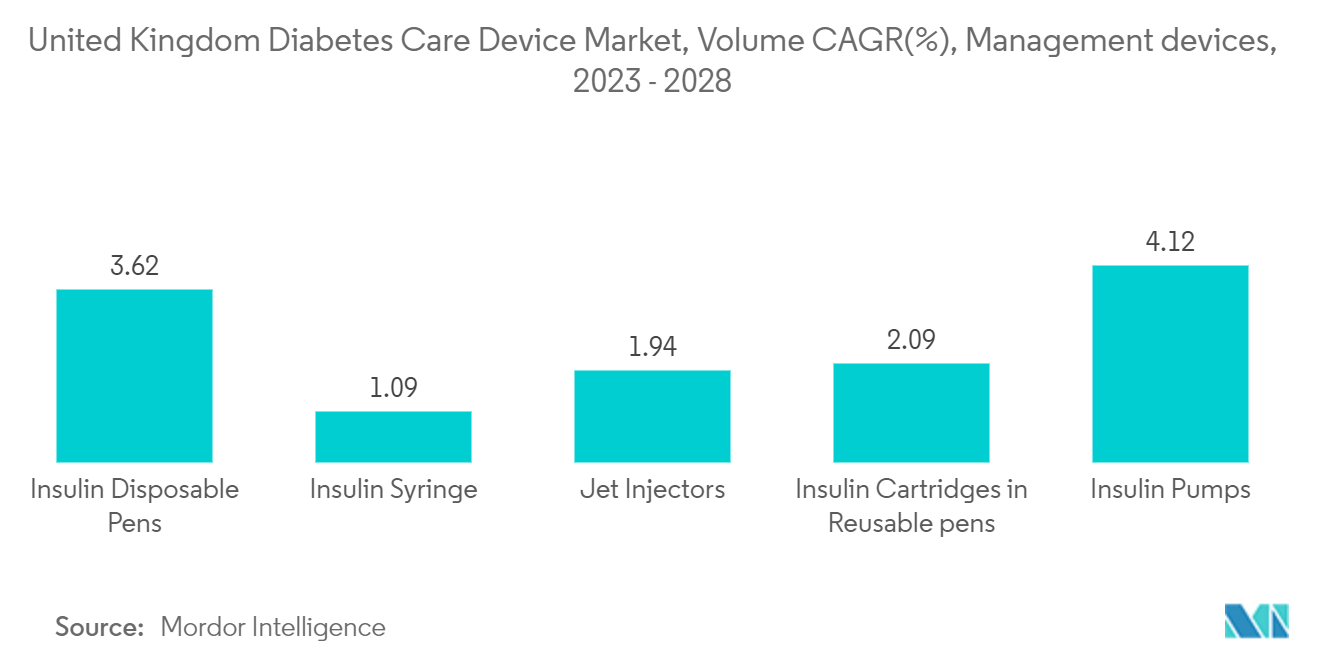

Insulin cartridges in reusable pens occupied the highest share in the management devices segment in the current year

Insulin cartridges in reusable pens occupied the highest market share of about 51% in the management devices segment in the current year.

Insulin cartridges in reusable pens are an upgraded version of insulin vials. Most types of insulins are manufactured in the form of cartridges, making them easily accessible. These devices comprise the functional benefits of reusable pens and are cost-effective, as these cartridges are less expensive compared to disposable insulin pens in the long run. Due to the increasing demand for insulin cartridges, most insulin device manufacturers produce reusable insulin pens compatible with various manufacturers' cartridges.

These insulin cartridges are considered more consumer-friendly, as they are smaller and less noticeable than the classic vial-and-syringe. These devices are also more portable for consumers on the go. Open cartridges do not need to be refrigerated, making storage easy for consumers. Thus, cartridges are the most cost-effective insulin use, as reusable pens are a one-time investment, unlike disposable pens.

The National Service Framework (NSF) program is improving services by setting national standards to drive service quality and tackle variations in care. The Association of British HealthTech Industries (ABHI) launched a diabetes section, enabling diabetes technology companies to work together in the first forum of its kind. The ABHI group is for any health technology company interested in diabetes care, from CGM and insulin pumps to apps. Such advantages helped adopt these products in the United Kingdom market.

UK Diabetes Devices Industry Overview

The United Kingdom diabetes care devices market is semi-consolidated, with few significant and generic players. Manufacturers drove constant innovations to compete in the market. The major players, such as Abbott and Medtronic, underwent many mergers, acquisitions, and partnerships to establish market dominance while also adhering to organic growth strategies, which is evident from the R&D spending of these companies. The manufacturers of insulin delivery devices are spending a massive amount on the R&D of the devices.

UK Diabetes Devices Market Leaders

-

Insulet Corporation

-

Roche Diabetes Care

-

Abbott Diabetes Care

-

Dexcom Inc.

-

Medtronic PLC

*Disclaimer: Major Players sorted in no particular order

UK Diabetes Devices Market News

- May 2023: The National Institute of Clinical Excellence (NICE) made a significant advancement by revising its guidelines to incorporate CGMs and flash glucose monitors, which are automated glucose monitoring devices, for children diagnosed with type 2 diabetes. This development marks a significant milestone for the United Kingdom, as it eliminates the sole reliance on fingerstick testing to monitor blood sugar levels in children. Although fingersticks have been valuable, they can induce stress and discomfort, particularly for children and their families who need to perform numerous tests daily.

- April 2022: Abbott, CamDiab, and Ypsomed announced they are partnering to develop and commercialize an integrated automated insulin delivery (AID) system. The initial focus of the partnership will be on European countries. The connected, smart wearable solution is designed to continuously monitor a person's glucose levels and automatically adjust and deliver the right amount of insulin at the right time, removing the guesswork of insulin dosing.

UK Diabetes Devices Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Management Devices

5.1.1 Insulin Pump

5.1.1.1 Technology

5.1.1.1.1 Tethered Insulin Pump

5.1.1.1.2 Tubeless Insulin Pump

5.1.1.2 Component

5.1.1.2.1 Insulin Pump Device

5.1.1.2.2 Insulin Pump Reservoir

5.1.1.2.3 Infusion Set

5.1.2 Insulin pens

5.1.2.1 Cartridges in Reusable Pens

5.1.2.2 Insulin Disposable Pens

5.1.3 Insulin Syringes

5.1.4 Jet Injectors

5.2 Monitoring Devices

5.2.1 Self-monitoring Blood Glucose

5.2.1.1 Glucometer Devices

5.2.1.2 Blood Glucose Test Strips

5.2.1.3 Lancets

5.2.2 Continuous Glucose Monitoring

5.2.2.1 Sensors

5.2.2.2 Durables (Receivers and Transmitters)

5.3 End User

5.3.1 Hospital/Clinics

5.3.2 Home/Personal

6. MARKET INDICATORS

6.1 Type 1 Diabetes Population

6.2 Type 2 Diabetes Population

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Abbott Diabetes Care

7.1.2 Roche Diabetes Care

7.1.3 LifeScan (Johnson & Johnson)

7.1.4 Sanofi

7.1.5 Medtronic

7.1.6 Novo Nordisk A/S

7.1.7 Terumo

7.1.8 Eli Lilly

7.1.9 Arkray

7.1.10 Becton Dickinson

7.1.11 Dexcom

- *List Not Exhaustive

7.2 Company Share Analysis

7.2.1 Self-monitoring Blood Glucose Devices

7.2.1.1 Abbott Diabetes Care

7.2.1.2 LifeScan

7.2.1.3 Others

7.2.2 Continuous Glucose Monitoring Devices

7.2.2.1 Dexcom

7.2.2.2 Abbott Diabetes Care

7.2.2.3 Others

7.2.3 Insulin Devices

7.2.3.1 Medtronic

7.2.3.2 Novo Nordisk A/S

7.2.3.3 Others

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

UK Diabetes Devices Industry Segmentation

Diabetes care devices are the hardware, equipment, and software used by diabetes patients to regulate blood glucose levels, prevent diabetes complications, lessen the burden of diabetes, and enhance the quality of life. The United Kingdom diabetes care devices market is segmented into management devices (insulin pumps (technology and components (insulin pump devices, insulin pump reservoirs, and infusion sets)), insulin syringes, insulin pens (cartridges in reusable pens, disposable insulin pens), and jet injectors), and monitoring devices (self-monitoring blood glucose (glucometer devices, blood glucose test strips, and lancets) and continuous glucose monitoring (sensors and durables)) and End User ( Hospital/clinics, and Home/Personal). The report offers the value (in USD) and volume (in units) for the above segments.

| Management Devices | |||||||||||

| |||||||||||

| |||||||||||

| Insulin Syringes | |||||||||||

| Jet Injectors |

| Monitoring Devices | |||||

| |||||

|

| End User | |

| Hospital/Clinics | |

| Home/Personal |

UK Diabetes Devices Market Research FAQs

How big is the United Kingdom Diabetes Care Devices Market?

The United Kingdom Diabetes Care Devices Market size is expected to reach USD 84.31 million in 2024 and grow at a CAGR of 6.72% to reach USD 116.32 million by 2029.

What is the current United Kingdom Diabetes Care Devices Market size?

In 2024, the United Kingdom Diabetes Care Devices Market size is expected to reach USD 84.31 million.

Who are the key players in United Kingdom Diabetes Care Devices Market?

Insulet Corporation, Roche Diabetes Care, Abbott Diabetes Care, Dexcom Inc. and Medtronic PLC are the major companies operating in the United Kingdom Diabetes Care Devices Market.

What years does this United Kingdom Diabetes Care Devices Market cover, and what was the market size in 2023?

In 2023, the United Kingdom Diabetes Care Devices Market size was estimated at USD 79 million. The report covers the United Kingdom Diabetes Care Devices Market historical market size for years: 2018, 2019, 2020, 2021, 2022 and 2023. The report also forecasts the United Kingdom Diabetes Care Devices Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

UK Diabetes Devices Industry Report

Statistics for the 2024 United Kingdom (UK) Diabetes Care Devices market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. United Kingdom (UK) Diabetes Care Devices analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.