UK Construction Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 398.68 Billion |

| Market Size (2029) | USD 466.57 Billion |

| CAGR (2024 - 2029) | 3.19 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

UK Construction Market Analysis

The UK Construction Market size is estimated at USD 398.68 billion in 2024, and is expected to reach USD 466.57 billion by 2029, growing at a CAGR of 3.19% during the forecast period (2024-2029).

The increasing building activities across the United Kingdom are driving the market. Furthermore, the market is being propelled by growing commercial activities. Even though the general trends point to significant expansion, the UK construction industry has recently faced numerous difficulties. Inflation and Russia's invasion of Ukraine have disrupted the supply chain and pushed up the price of building materials.

There has been a significant recovery, with favorable growth rates in the United Kingdom’s construction output. According to the Office for National Statistics UK, the value of new construction works in current prices in Great Britain reached a record high of GBP 132,989 million (USD 168,027 million) in 2022, which was mainly due to an increase in both domestic and public sector work amounting to GBP 14,093 million and GBP 4,068 million (USD 5,138 million), respectively.

In addition, new construction orders increased by 11.4% to GBP 80,837 million (USD 102,116 million) in 2022, driven by private infrastructure, private businesses, and other public non-housing, with industrial being the only sector that registered a decline.

In Great Britain, construction-related employees (excluding self-employment) totaled 1.4 million in 2022, an increase of 3.3% compared to 2021. England had the most significant increase in construction-related employees, amounting to 3.5%, followed by Wales and Scotland registering a 2.0% increase each.

UK Construction Market Trends

Increase in GVA of Construction Industry Driving the Market

The United Kingdom has a solid competitive edge in the construction market. The United Kingdom has world-class expertise in architecture, design, and engineering, and British companies lead the way in sustainability solutions for buildings.

The changes in the global economy create new opportunities for Britain. The government supports the growth of British companies and their aspirations, trust, and drive to compete on a global scale to promote recovery. This agenda includes reforming the planning system, ensuring that vital infrastructure projects are financed, and supporting the housing market through critical initiatives like the Funding for Lending Scheme and the Help-to-Buy Equity Loan Scheme.

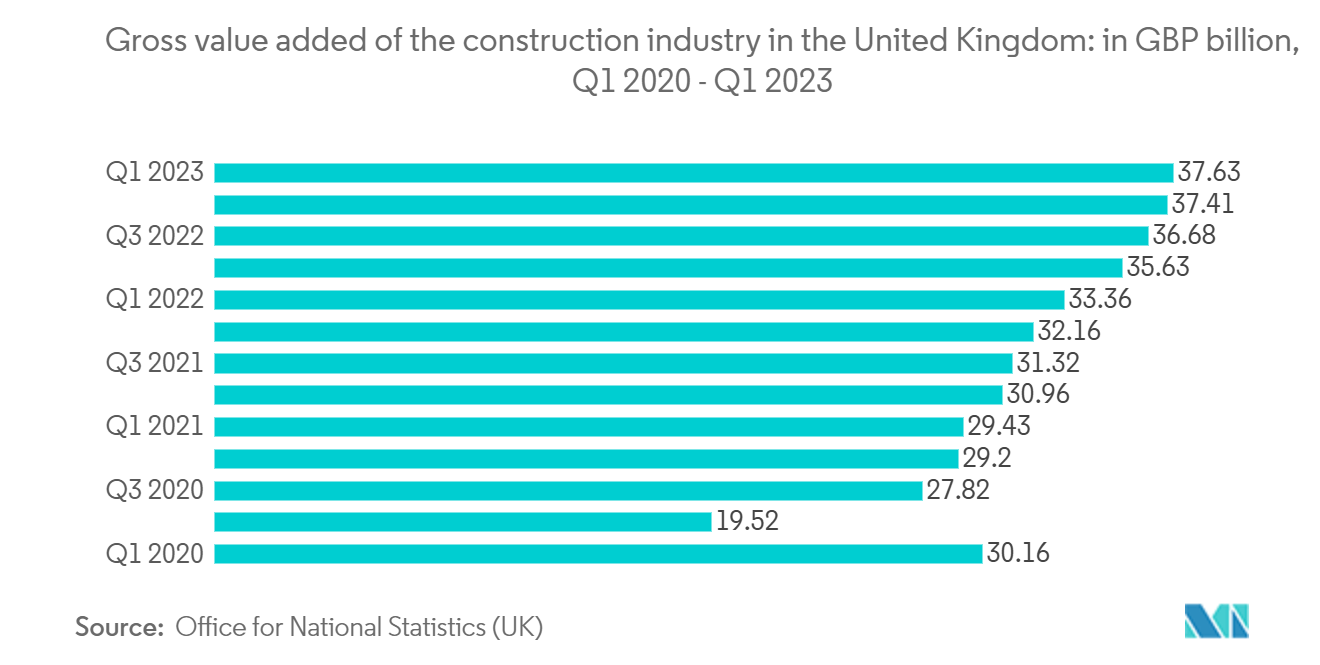

The gross value added (GVA) by the construction sector in the United Kingdom in the first quarter of 2023 was GBP 37.63 billion (USD 47.55 billion), according to its Office for National Statistics. The GVA of this sector dropped to GBP 20 billion (USD 25.6 billion) in Q2 of 2020 due to the COVID-19 pandemic, marking the sector's lowest point in a decade. Out of all the industries in the UK construction sector, private housing was the one that made the most money.

Private Housing Holds the Largest Share in the UK Construction Market

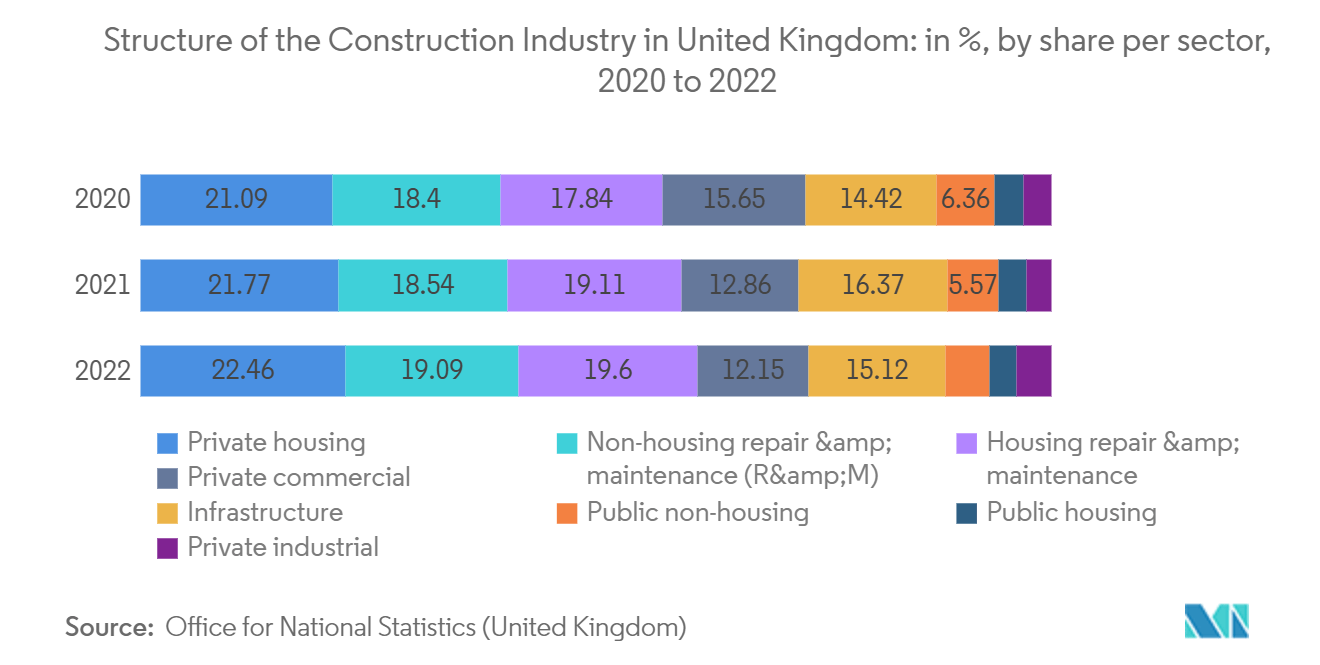

Private housing was the segment that held the most significant share of the UK construction market. Nevertheless, housing and non-housing repair and maintenance together amounted to almost 39% of the construction output in 2022, according to data from the UK Office for National Statistics. The output volume of infrastructure grew during the past years, surpassing the construction of commercial buildings.

There has been a gradual increase in the number of households occupied by private renters in England. According to industry experts, the share of households occupied by private renters in 2023 was estimated to be 18.8%, with around 4.6 million households being privately rented. There has also been a marked increase in the average price of homes in the United Kingdom.

In the United Kingdom, private rental prices increased in the 12 months to January 2023 by 4.4%, up from 4.2% in the 12 months to December 2022, according to the Office of National Statistics. From 12 months to January 2023, the annual private rental price increased by 3.9% in Wales, 4.3% in England, and 4.5% in Scotland. In England, the East Midlands had the highest annual percentage change over 12 months to January 2023 in private rental prices of 5.0%, while the West Midlands recorded the lowest change at 3.9%. Also, in the 12 months until January 2023, London's yearly percentage change in private renting prices was 4.3%.

UK Construction Industry Overview

The UK construction market is partially fragmented, with the presence of many regional and local players and a few global companies. In addition, there is a vast potential for growth in the residential and transport construction segments during the forecast period, stimulating opportunities for market players. Key players are Kier Group PLC, Morgan Sindall Group PLC, Mace Limited, Winvic Ltd, and ISG PLC. In addition, due to the increasing investments in construction and future large projects in the United Kingdom, the market is projected to grow during the forecast period.

UK Construction Market Leaders

-

Kier Group plc

-

Morgan Sindall Group plc

-

Mace Ltd

-

Winvic Group

-

ISG plc

*Disclaimer: Major Players sorted in no particular order

UK Construction Market News

- August 2023: McAleer and Rushe announced that they had begun constructing the last phase of Southbank Place in London. The GBP 138 million (USD 174.34 million) Southbank Place Building 5 development is situated 100 m from the London Eye. This development is part of the master plan for the Shell Tower in London's South Bank.

- March 2023: The UK Department of Transport announced over GBP 40 billion (USD 50.54 billion) of capital investment in transport across the next two financial years, which will drive significant improvements for rail and roads across the market.

UK Construction Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Drivers

4.2.1 Investments in Transport Infrastructure

4.3 Restraints

4.3.1 Shortage of Skilled Labor

4.4 Opportunities

4.4.1 The Birmingham Big City Plan

4.5 Value Chain/Supply Chain Analysis

4.6 Industry Attractiveness - Porter's Five Forces Analysis

4.6.1 Bargaining Power of Suppliers

4.6.2 Bargaining Power of Buyers/Consumers

4.6.3 Threat of New Entrants

4.6.4 Threat of Substitute Products

4.6.5 Intensity of Competitive Rivalry

5. MARKET INSIGHTS

5.1 Current Economic and Construction Market Scenario

5.2 Technological Innovations in the Construction Sector

5.3 Impact of Government Regulations and Initiatives on the Industry

5.4 Insights into Upcoming and Ongoing Infrastructure Projects in the United Kingdom

5.5 Impact of COVID-19 on the Market

6. MARKET SEGMENTATION

6.1 By Sector

6.1.1 Residential

6.1.2 Commercial

6.1.3 Industrial

6.1.4 Infrastructure

6.1.5 Energy and Utilities

6.2 By Key Regions

6.2.1 England

6.2.2 Northern Ireland

6.2.3 Scotland

6.2.4 Wales

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Kier Group PLC

7.1.2 Morgan Sindall Group PLC

7.1.3 Mace Ltd

7.1.4 Winvic Group

7.1.5 ISG PLC

7.1.6 Bouygues UK

7.1.7 Balfour Beatty PLC

7.1.8 Galliford Try PLC

7.1.9 Keller Group PLC

7.1.10 Laing O'Rourke PLC*

- *List Not Exhaustive

7.2 Other Companies

8. FUTURE OF THE MARKET

9. APPENDIX

UK Construction Industry Segmentation

Construction is the installation, maintenance, and repair of buildings and other stationary structures, as well as the construction of roadways and service facilities that form fundamental components of structures and are required for their operation. Construction encompasses the processes involved in constructing buildings, infrastructure, industrial facilities, and related operations from start to finish. A complete background analysis of the UK construction market, including an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and the COVID-19 pandemic’s impact, is covered in the report.

The UK construction market is segmented by sector (residential, commercial, industrial, infrastructure, and energy and utilities) and key regions (England, Northern Ireland, Scotland, and Wales). The report offers market sizes and forecasts for all the above segments in value (USD).

| By Sector | |

| Residential | |

| Commercial | |

| Industrial | |

| Infrastructure | |

| Energy and Utilities |

| By Key Regions | |

| England | |

| Northern Ireland | |

| Scotland | |

| Wales |

UK Construction Market Research Faqs

How big is the UK Construction Market?

The UK Construction Market size is expected to reach USD 398.68 billion in 2024 and grow at a CAGR of 3.19% to reach USD 466.57 billion by 2029.

What is the current UK Construction Market size?

In 2024, the UK Construction Market size is expected to reach USD 398.68 billion.

Who are the key players in UK Construction Market?

Kier Group plc, Morgan Sindall Group plc, Mace Ltd, Winvic Group and ISG plc are the major companies operating in the UK Construction Market.

What years does this UK Construction Market cover, and what was the market size in 2023?

In 2023, the UK Construction Market size was estimated at USD 385.96 billion. The report covers the UK Construction Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the UK Construction Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the future growth prospects for the UK Construction Market?

The future growth prospects for the UK Construction Market are a) Increasing emphasis on sustainability and integration of green building practices b) Growing focus on private sector sustainability initiatives and advancements in construction technology c) Surging focus on energy-efficient and sustainable construction

UK Construction Industry Report

The UK construction industry is on a trajectory of significant growth and transformation, fueled by a steadfast commitment to sustainability, cutting-edge technological advancements, and a surging demand for both residential and commercial infrastructure. In sync with global movements towards energy efficiency and the adoption of smart building technologies, the UK construction market is experiencing an uptick in investments directed towards green building practices, Building Information Modeling (BIM), and the Internet of Things (IoT) applications. Spanning a diverse range of construction types, including residential, commercial, and industrial projects, the market is distinctly focused on sustainable and energy-efficient development. UK construction companies are increasingly gravitating towards eco-friendly materials and renewable energy systems, underscoring their commitment to environmental preservation. The market growth is propelled by the strategic leverage of technological innovations to boost efficiency and sustainability. With construction industry UK statistics projecting a promising future, the sector's advancement is well-documented in ����vlog��ý™ Industry Reports, offering a comprehensive market forecast outlook and historical overview. For a deeper dive into this burgeoning market, a free report PDF download is available, providing valuable insights into the UK Construction market share, size, and revenue growth rate.