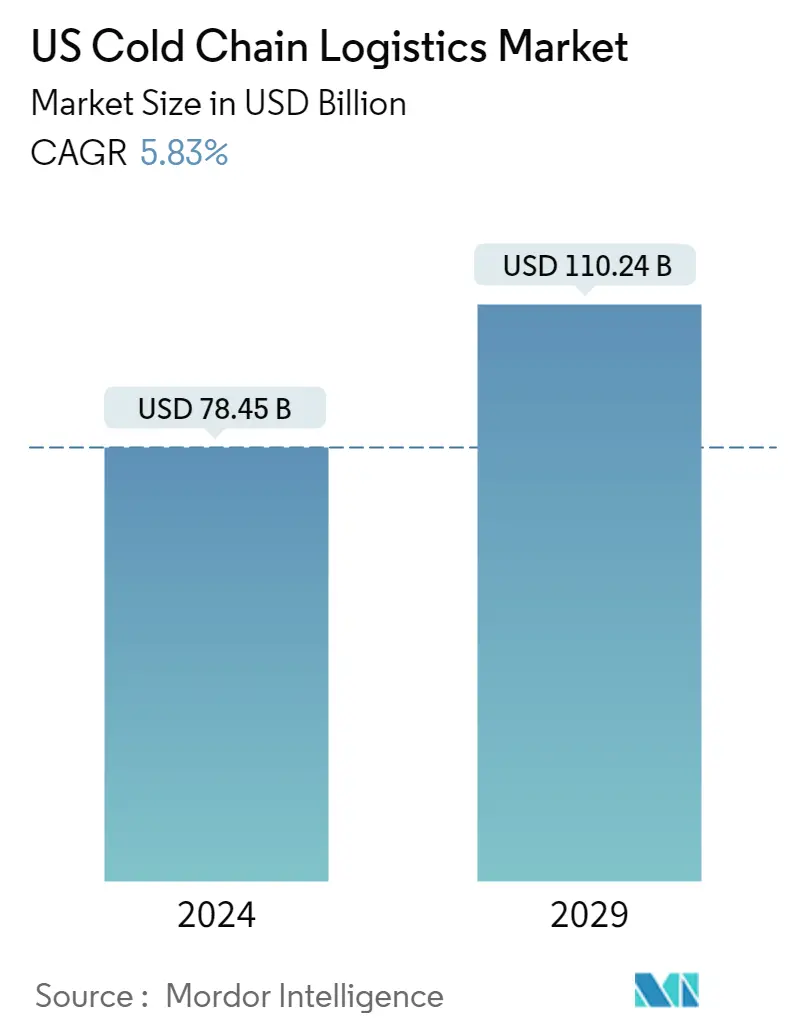

US Cold Chain Logistics Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 78.45 Billion |

| Market Size (2029) | USD 110.24 Billion |

| CAGR (2024 - 2029) | 5.83 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

US Cold Chain Logistics Market Analysis

The US Cold Chain Logistics Market size is estimated at USD 78.45 billion in 2024, and is expected to reach USD 110.24 billion by 2029, growing at a CAGR of 5.83% during the forecast period (2024-2029).

- The COVID-19 pandemic significantly boosted the domestic e-retailing sector and the consumption of processed foods and beverages, pushing the demand for refrigerated storage spaces and logistics. The rise of online groceries, with a significant share of orders for perishables and frozen foods, is also supporting the market demand. The market has also benefitted significantly from the stringent government regulation toward the production and supply of temperature-sensitive products.

- However, the labor shortages in the transportation and warehousing sector, high energy requirements, and the negative environmental impact of the cold chain logistics operations are some of the challenges that may limit the market growth. To tackle the challenges regarding the high energy requirements and negative environmental impact, some companies are introducing solutions that increase the energy required to run the cold chain infrastructure.

- Technologies like Artificial Intelligence (AI), Machine Learning, Internet of Things (IoT), Robotics, Ware, and distribution center automation are being incorporated by players to increase the efficiency of their operations, reduce operational costs, and provide better customer experience.

- More outsourcing is occurring throughout the broader industrial logistics market, with third-party logistics (3PL) providers accounting for 34% of total leasing activity in 2022 through May, up from 30% in the same period of 2021. This trend is particularly common in the cold storage industry due to costs and more complex technology systems.

- According to the US Department of Agriculture (USDA), 72% of the refrigerated storage capacity in the US is outsourced to public refrigerated warehouse (PRW) companies, down from 75% five years ago. The remaining 28% includes in-house cold chain operators, up from 25% five years ago.

- The perishables imports, pharmaceutical industry growth, including the biologics sector, increasing consumption of frozen foods, pharmaceutical temperature monitoring regulations, etc., are the demand drivers for the cold chain logistics market in the United States.

US Cold Chain Logistics Market Trends

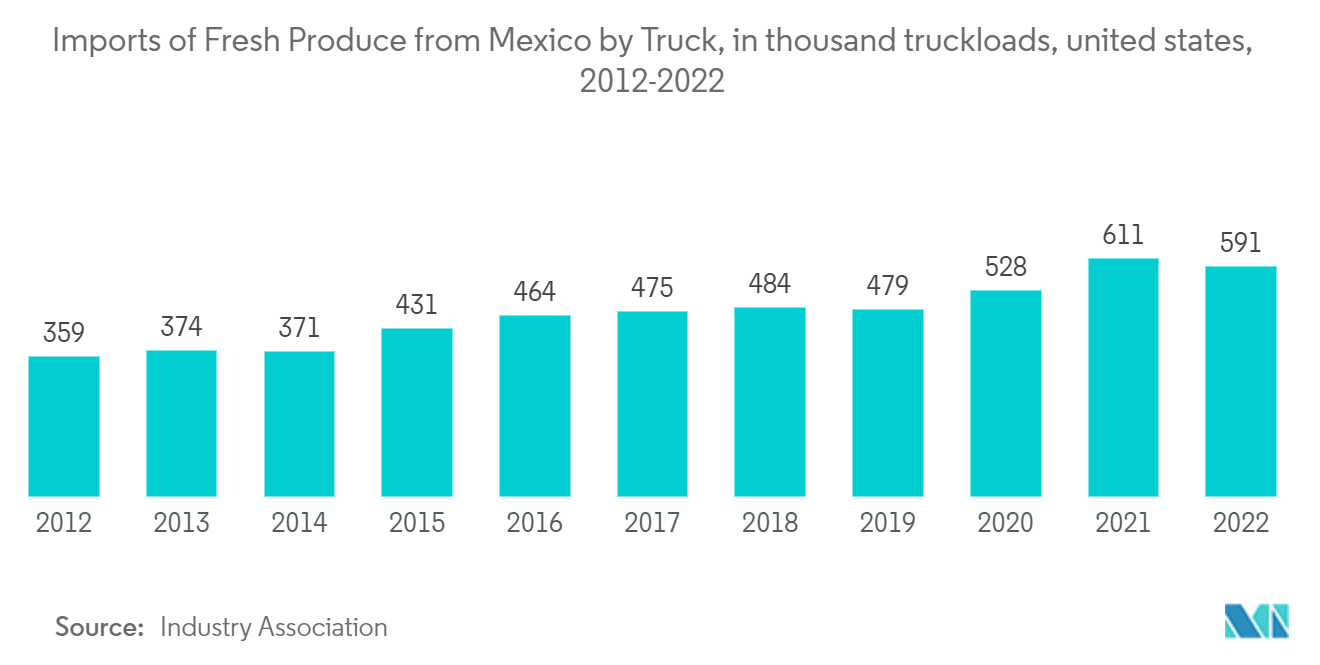

Rising fresh produce imports from Mexico

- The United States imports over USD 22 billion worth of fresh produce annually from all over the globe and receives fresh produce from over 125 countries. Thirty-two percent of the country’s fresh vegetables and fifty-five percent of its fresh fruit are imported from other countries.

- Almost 70% of all goods shipped via air freight between Latin America and North America consist of perishable products. Seventy-seven percent of the fresh fruits and vegetables imported by the United S come from Mexico, with an additional 11% from Canada.

- Mexico is the largest agricultural trading partner for the United States, totaling USD 71.9 billion (imports plus exports) in 2022. US agricultural exports to Mexico totaled USD 28.5 billion, while imports from Mexico totaled USD 43.4 billion. The main agricultural products imported from Mexico are fruits and vegetables; in fact, 44% of the fruits and 48% of the vegetables imported by the US are from Mexico.

- In 2022, 83.6% of US agricultural imports from Mexico consisted of vegetables, fruit, beverages, or distilled spirits, according to the US Department of Agriculture (USDA).

- The United States imported USD 18.7 billion of produce from Mexico in 2022, including fresh, frozen, and processed fruits, vegetables, and nuts. Just over 98% of these imports entered the United States through land ports between Mexico and Texas, New Mexico, Arizona, and California. When considering only fresh fruits and vegetables, which constitute nearly 89% of the total produce, imports totaled USD 16.6 billion.

- These imports were shipped in 590,906 forty-thousand-pound truckloads. Approximately 55% of the US fresh fruit and vegetable imports from Mexico entered through Texas land ports, arriving in 325,467 truckloads worth USD 11.6 billion.

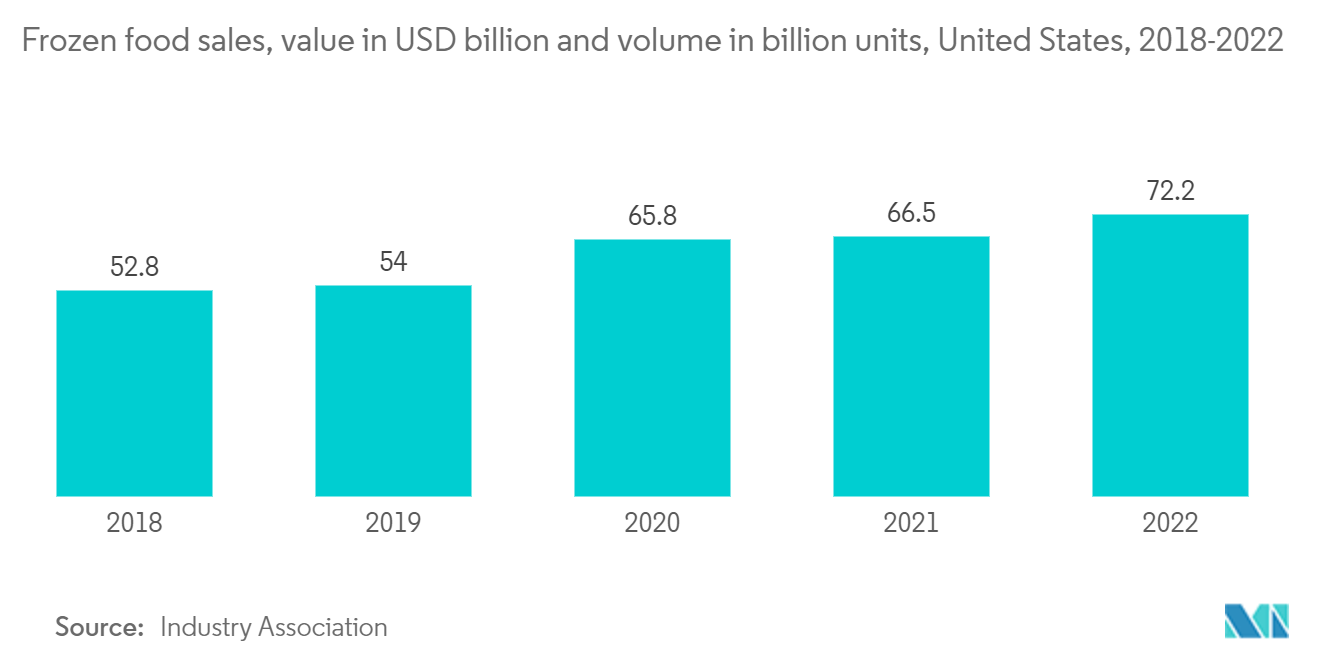

Increasing popularity of frozen foods

- The American Frozen Food Institute (AFFI) reported that frozen food sales increased 8.6% to USD 72.2 billion in 2022. Unit sales decreased during that time but remained 5% above pre-pandemic levels.

- Between 2018 and 2022, frozen food dollar sales increased a whopping USD 19.4 billion, underlining the impact of the pandemic on the category’s growth. While frozen food dollar sales have consistently climbed since 2018, unit sales decreased in both 2021 and 2022 by 3.2% and 5.1%, respectively, highlighting the potential impact of inflation on frozen food costs.

- Despite the decreases, unit sales remain elevated compared to pre-pandemic levels, indicating continued demand for frozen foods. This is particularly true for frozen processed meat, frozen snacks, and seafood, which have seen double-digit increases in unit sales compared to pre-pandemic levels.

- A new survey from AFFI finds that more than a quarter of shoppers are buying more frozen fruits and vegetables than three years ago and identify many benefits with these foods. Frozen fruits and vegetables help make it easier for households and demographic groups to increase their produce consumption and reduce food waste. Overall, penetration in the United States is high, with 94% of American households buying frozen fruits and vegetables.

- The sales of frozen fruits and vegetables in the United States reached USD 7.1 billion over the 52 weeks ending June 26, 2022, and product volume were 271 million pounds above pre-pandemic levels at 3.9 billion pounds. The top products within the segment were plain vegetables, potatoes, onions, and fruit, with sales of USD 2.9 billion, USD 2.3 billion, and USD 1.5 billion, respectively.

US Cold Chain Logistics Industry Overview

The cold chain logistics market of the United States is highly fragmented, aiding the domestic as well as international transportation of temperature-sensitive goods. It is undergoing developments with the introduction of solar-powered refrigerated units, multi-temperature trucks, and freight optimization software. International and local players like FedEx, XPO Logistics, Total Quality Logistics, Americold Logistics and many such companies are operational in the market.

US Cold Chain Logistics Market Leaders

-

FedEx Logistics

-

XPO Logistics

-

CH Robinson Worldwide

-

JB Hunt

-

Expeditors

*Disclaimer: Major Players sorted in no particular order

US Cold Chain Logistics Market News

- June 2023: Honor Foods, the Burris Logistics food service redistribution company, purchased Sunny Morning Foods, a food service redistributor with dairy expertise located in Fort Lauderdale, FL. Sunny Morning Foods strengthens the company’s portfolio and broadens its position as a preferred food service redistributor in the Mid-Atlantic, New England, and now Southeast regions.

- May 2023: Americold Logistics, a global leader in temperature-controlled warehouses and logistics for the food industry, announced the grand opening of its facility expansion in Santa Perpetua, Barcelona, Spain. The expansion adds 11 loading bays and 12,000 pallet positions, bringing greater capacity for temperature-controlled products and services to customers in the region.

- May 2023: Americold Logistics, the world’s largest publicly traded REIT focused on the ownership, operation, acquisition, and development of temperature-controlled warehouses, announced a strategic investment into RSA Cold Chain in Dubai. At close, Americold’s investment is USD 3.9 million for the company’s share (49%) of RSA Cold Chain equity.

US Cold Chain Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Deliverables

1.2 Study Assumptions

1.3 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS AND INSIGHTS

4.1 Current Market Scenario

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 PHARMACEUTICAL INDUSTRY GROWTH

4.2.1.2 RISING FRESH PRODUCE IMPORTS FROM MEXICO

4.2.1.3 INCREASING POPULARITY OF FROZEN FOODS

4.2.2 Restraints

4.2.2.1 EMISSIONS FROM COLD CHAIN OPERATIONS

4.2.2.2 LABOUR SHORTAGES

4.2.3 Opportunities

4.2.3.1 Adopting energy-efficient solutions

4.2.3.2 rise of online grocery business

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Buyers/Consumers

4.3.2 Bargaining Power of Suppliers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Insights on Technological Trends and Automation

4.5 Insights on Government Regulations and Initiatives

4.6 Industry Value Chain/Supply Chain Analysis

4.7 Spotlight on Ambient/Temperature-controlled Storage

4.8 Impact of Emission Standards and Regulations on Cold Chain Industry

4.9 Impact of Covid-19 on the Market

5. MARKET SEGMENTATION

5.1 By Services

5.1.1 Storage

5.1.2 Transportation

5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

5.2 By Temperature Type

5.2.1 Chilled

5.2.2 Frozen

5.2.3 Ambient

5.3 By Application

5.3.1 Fruits and Vegetables

5.3.2 Dairy Products (Milk, Butter, Cheese, Ice Cream, Etc.)

5.3.3 Fish, Meat, and Seafood

5.3.4 Processed Food

5.3.5 Healthcare & Pharmaceuticals

5.3.6 Bakery and Confectionary

5.3.7 Other Applications

6. COMPETITIVE LANDSCAPE

6.1 Market Concentration Overview

6.2 Company Profiles

6.2.1 FedEx

6.2.2 XPO Logistics

6.2.3 CH Robinson Worldwide

6.2.4 JB Hunt

6.2.5 Expeditors

6.2.6 Total Quality Logistics

6.2.7 Americold Logistics

6.2.8 Burris Logistics

6.2.9 Prime Inc.

6.2.10 Lineage Logistics

6.2.11 Arc Best

6.2.12 Stevens Transport

6.2.13 DHL Supply Chain

6.2.14 United States Cold Storage

6.2.15 DB Schenker

6.2.16 Covenant Transportation Services*

- *List Not Exhaustive

7. FUTURE OF THE MARKET

8. APPENDIX

US Cold Chain Logistics Industry Segmentation

Cold chain logistics involves the careful management of temperature-sensitive products throughout their storage and transportation. It ensures the integrity and quality of goods like food, pharmaceuticals, and chemicals by maintaining specific temperature conditions, such as chilled or frozen, to prevent spoilage, degradation, or loss of efficacy.

The United States cold chain logistics market is segmented by service (storage, transportation, and value-added services), by temperature type (chilled and frozen), and by application (horticulture (fresh fruits & vegetables), meats, fish, and poultry, processed food products, pharma, life sciences, and chemicals, and other applications).

The report also covers the impact of COVID-19 on the market. The report offers market size and forecast for the United States cold chain logistics market in value (USD) for all the above segments.

| By Services | |

| Storage | |

| Transportation | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| By Temperature Type | |

| Chilled | |

| Frozen | |

| Ambient |

| By Application | |

| Fruits and Vegetables | |

| Dairy Products (Milk, Butter, Cheese, Ice Cream, Etc.) | |

| Fish, Meat, and Seafood | |

| Processed Food | |

| Healthcare & Pharmaceuticals | |

| Bakery and Confectionary | |

| Other Applications |

US Cold Chain Logistics Market Research FAQs

How big is the US Cold Chain Logistics Market?

The US Cold Chain Logistics Market size is expected to reach USD 78.45 billion in 2024 and grow at a CAGR of 5.83% to reach USD 110.24 billion by 2029.

What is the current US Cold Chain Logistics Market size?

In 2024, the US Cold Chain Logistics Market size is expected to reach USD 78.45 billion.

Who are the key players in US Cold Chain Logistics Market?

FedEx Logistics, XPO Logistics, CH Robinson Worldwide, JB Hunt and Expeditors are the major companies operating in the US Cold Chain Logistics Market.

What years does this US Cold Chain Logistics Market cover, and what was the market size in 2023?

In 2023, the US Cold Chain Logistics Market size was estimated at USD 74.13 billion. The report covers the US Cold Chain Logistics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the US Cold Chain Logistics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

US Cold Chain Logistics Industry Report

Statistics for the 2024 US Cold Chain Logistics market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. US Cold Chain Logistics analysis includes a market forecast outlook 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.