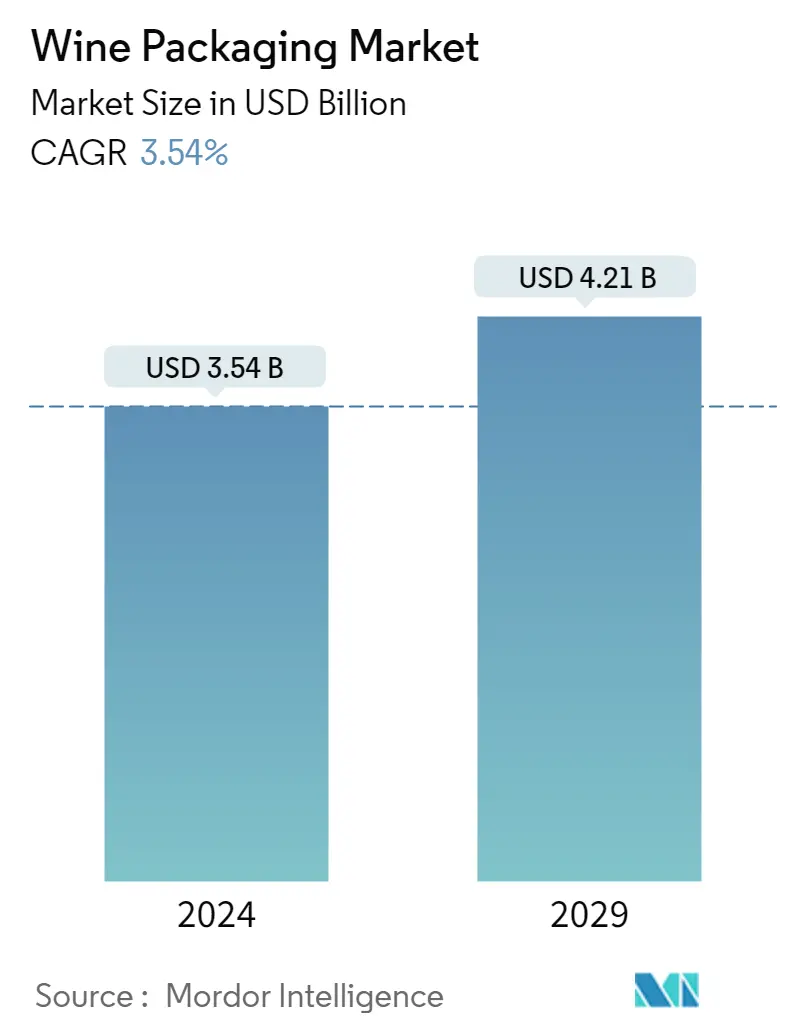

United States Wine Packaging Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 3.54 Billion |

| Market Size (2029) | USD 4.21 Billion |

| CAGR (2024 - 2029) | 3.54 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

United States Wine Packaging Market Analysis

The Wine Packaging Market size is estimated at USD 3.54 billion in 2024, and is expected to reach USD 4.21 billion by 2029, growing at a CAGR of 3.54% during the forecast period (2024-2029).

With the consumer demand for smaller packaging, the wine packaging market in the United States is witnessing the adoption of non-glass bottle-based alternatives such as bags in boxes, pouches, cans, paper bottles, among others.

- With the COVID-19 pandemic, the wine packaging market in the United States is expected to witness growth. Also, wine packaging manufacturers have been flooded with a pool of issues that are expected to persist for the short-term. Some of the effects of lockdown include the lack of availability of raw materials used in the manufacturing process, supply chain disruptions, fluctuating prices, and labor shortages that could cause shipping problems, and production of the final product to inflate and go beyond budget, etc.

- The wine packaging popularity in the region is vastly dependent on consumer age and usages. For example, for events like music festivals, friendly gatherings, and sports games, cans, pouches, and small bag-in-a-box are gaining popularity among consumers.

- Packaging such as bags in boxes (BIB) weighs less than glass bottles. They don't break and can be sealed at any time. In addition, it offers benefits such as low logistics costs and ease of transport, large print area for marketing purposes, (to manufacturers) ideal stacking capacity, and saves space. It also saves purchasing and transportation costs to the bulk purchaser. It is up to 40% less expensive than wine in glass bottles (to end consumers) and have recycling and upcycling options.

- The manufacturers in the wine packaging market are constantly innovating and developing new packaging products to gain a competitive advantage in the market.

- Amcor launched Easypeel that uses a one-piece aluminum capsule engineered to open wine bottles along a clean line. Unlike other technologies that depend on pull tabs, EASYPEEL allows consumers and professionals to use traditional bottle openers.

United States Wine Packaging Market Trends

This section covers the major market trends shaping the US Wine Packaging Market according to our research experts:

Glass as a packaging material has largest revenue share in Wine Packaging Market.

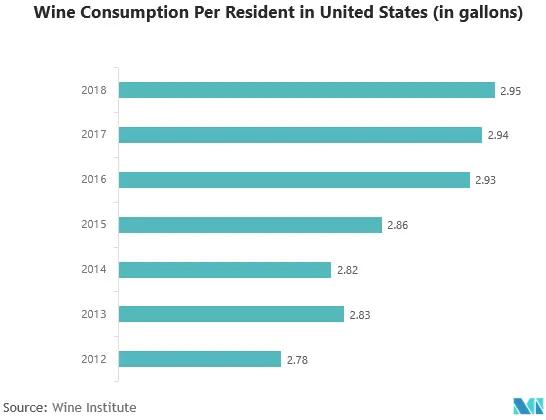

- Glass packaging is the most dominant form of wine packaging. The properties of glass are well suited to the nature of wine, not matched by plastic or even metals. According to the report titled, Beverage Information Group, in July 2020, the consumption of table wine amounted to approximately 310.72 million 9-liter cases in the United States in 2019.

- In January 2020, Ardagh Group, Glass - North America, the largest domestic manufacturer of glass bottles in the US wine market, introduced six new sophisticated glass wine bottle designs.

- The ongoing trade war between the United States and China may impact the country's glass packaging market. More than 50% of the glass bottles used in the US wine industry are imported from China; and due to increase in the tariff rate imposed on Chinese imports, the need for improving glass manufacturing infrastructure is expected to grow, leading to a rise in the overall cost of the product in coming years.

- Wine manufacturers are becoming increasingly more innovative in order to attract customers with their packaging, and are producing new concepts and designs.

Bag In Box is the fastest growing product type in Wine Packaging Market.

- The bag in box (BIB) wine packaging was first introduced by William R Scholle, a U.S chemical engineer in 1995. The BIB packaging can preserve wine for up to 8 weeks after opening compared to 2-3 days offered by glass bottles and thus lower the carbon footprint.

- BIB packaging is portable-friendly and is also applicable for institutional servings. For instance, the packaging is designed to be shatterproof, allowing them to be used in stadiums, concerts, and amusement parks. Also, the boxes are manufactured with air-tight characteristics to extend the freshness of wine.

- The BIB type packaging consists mainly three parts: pouches, corrugated cardboard, caps/closures. The caps and closures are ideally made of plastic, but vendors in the market are investing in environmentally friendly closures such as bio-based caps. For instance,Tetra Pak international SA ordered bio-based caps made of renewable HDPE (High-Density Poly-Ethylene), derived from sugarcane for pouches closures.

- According to Smurfit Kappa, during the COVID-19 pandemic consumer demand for this type of packaging surged in the UK and France as it attracted about 3.7 million consumers in the region, A similar trend was seen in the U.S as well. This boosted the need for export the packaging for the vendors in the United States.

United States Wine Packaging Industry Overview

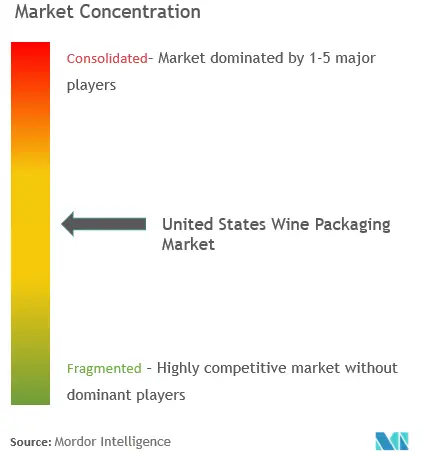

The major players include Ball Corporation, AMCOR PLC, Ardagh Group, Siligan Holding Inc., Owens-Illinois Inc., and others. The market is moderately fragmented and highly competitive without any dominating player. Hence, the market concentration is medium.

January 2021 - To serve the United States market, Ardagh Group SA expanded its production of wine bottles in its Oklahoma facility, including the bottles manufactured for Rombauer Vineyards. The expansion will provide a shorter, less complex supply chain and a stable supply of high-quality glass bottles to its customers.

June 2020 - Tetra Pak, a subsidiary of Tetra Laval, announced to collaborate with British multi award-winning start-up Garçon Wines to make their signature and more sustainable flat wine bottles made with post-consumer recycled (PCR) PET plastic available to the U.S. market.

Feburary 2020 - AMCOR PLC collaborated with British multi award-winning start-up Garçon Wines to make their signature and more sustainable flat wine bottles available to the U.S. market. Amcor and Garçon Wines, also produced flat wine bottles made with post-consumer recycled (PCR) PET plastic in the U.S. PET bottles are unbreakable, beach and pool-friendly, and the designs are only limited by the imagination. There are also environmental benefits: bottles are lightweight, infinitely recyclable and have a lower carbon footprint than glass bottles or aluminum cans.

United States Wine Packaging Market Leaders

-

AMCOR PLC

-

Ball Corporation

-

Owens–Illinois Inc.

-

Ardagh Group

-

Silgan Holdings Inc.

*Disclaimer: Major Players sorted in no particular order

United States Wine Packaging Market Report - Table of Contents

-

1. INTRODUCTION

-

1.1 Study Deliverables

-

1.2 Study Assumptions

-

1.3 Scope of the Study

-

-

2. RESEARCH METHODOLOGY

-

3. EXECUTIVE SUMMARY

-

4. MARKET INSIGHTS

-

4.1 Market Overview

-

4.2 Industry Value Chain Analysis

-

4.3 Market Drivers

-

4.3.1 Emergence of non-glass bottle-based alternatives

-

4.3.2 Innovations in packaging

-

-

4.4 Market Challenges

-

4.4.1 Dynamic nature of material-related regulations

-

-

4.5 Industry Attractiveness - Porter's Five Forces Analysis

-

4.5.1 Threat of New Entrants

-

4.5.2 Bargaining Power of Suppliers

-

4.5.3 Bargaining Power of Consumers

-

4.5.4 Threat of Substitute Products

-

4.5.5 Intensity of Competitive Rivalry

-

-

4.6 Major innovations in Wine Packaging

-

-

5. IMPACT OF COVID-19 ON THE WINE PACKAGING INDUSTRY

-

6. MARKET SEGMENTATION

-

6.1 Material

-

6.1.1 Plastic

-

6.1.2 Paper

-

6.1.3 Glass

-

6.1.4 Other Materials

-

-

6.2 Product Type

-

6.2.1 Glass Bottles

-

6.2.2 Plastic Bottles

-

6.2.3 Bag In Box

-

6.2.4 Closures

-

6.2.5 Other Product Types

-

-

-

7. COMPETITIVE INTELLIGENCE

-

7.1 Ball Corporation

-

7.2 AMCOR PLC

-

7.3 Scholle IPN Corporation

-

7.4 CCL Industries Inc.

-

7.5 Owens Illinois Inc.

-

7.6 Saverglass SAS

-

7.7 Plastipak Holding Inc.

-

7.8 Tetra Laval International SA

-

7.9 Ardagh Group

-

7.10 Encore Glass

-

7.11 Silgan Holding Inc.

-

-

8. FUTURE OUTLOOK OF THE MARKET

United States Wine Packaging Industry Segmentation

The wine packaging market uses various materials and product types for the packaging of wines. Segmentation is done the basis of material (glass, metal, paper, etc.) and product type (Glass bottles, Plastic bottles, Bag in Box, etc)

| Material | |

| Plastic | |

| Paper | |

| Glass | |

| Other Materials |

| Product Type | |

| Glass Bottles | |

| Plastic Bottles | |

| Bag In Box | |

| Closures | |

| Other Product Types |

United States Wine Packaging Market Research FAQs

How big is the Wine Packaging Market?

The Wine Packaging Market size is expected to reach USD 3.54 billion in 2024 and grow at a CAGR of 3.54% to reach USD 4.21 billion by 2029.

What is the current Wine Packaging Market size?

In 2024, the Wine Packaging Market size is expected to reach USD 3.54 billion.

Who are the key players in Wine Packaging Market?

AMCOR PLC, Ball Corporation, Owens–Illinois Inc., Ardagh Group and Silgan Holdings Inc. are the major companies operating in the Wine Packaging Market.

What years does this Wine Packaging Market cover, and what was the market size in 2023?

In 2023, the Wine Packaging Market size was estimated at USD 3.42 billion. The report covers the Wine Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Wine Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

United States Wine Packaging Industry Report

Statistics for the 2024 United States Wine Packaging market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. United States Wine Packaging analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.