Value-based Healthcare Services Market Size

| Study Period | 2019 - 2029 |

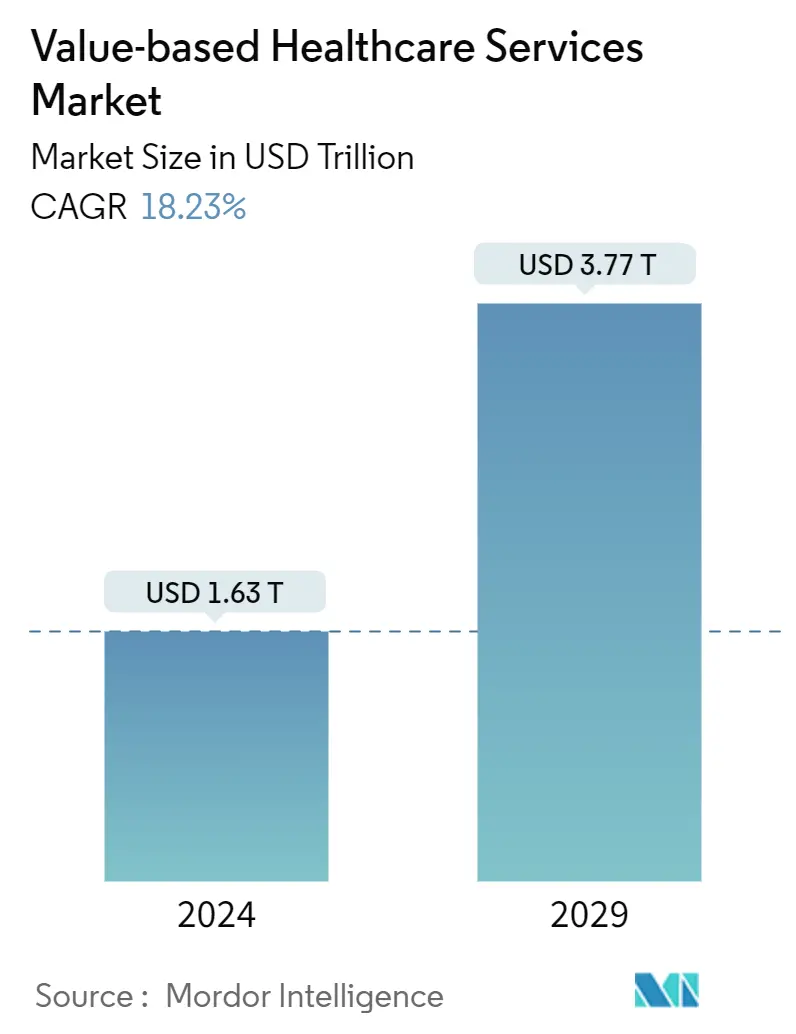

| Market Size (2024) | USD 1.63 Trillion |

| Market Size (2029) | USD 3.77 Trillion |

| CAGR (2024 - 2029) | 18.23 % |

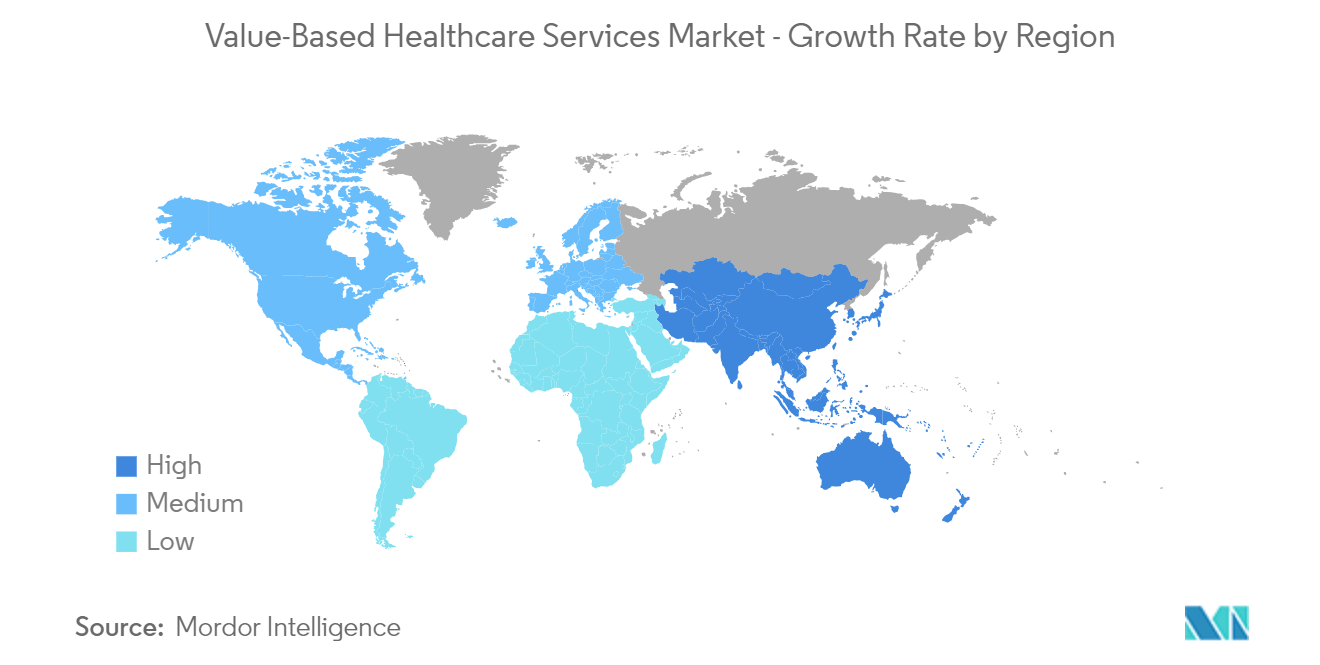

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Value-based Healthcare Services Market Analysis

The Value-based Healthcare Services Market size is estimated at USD 1.63 trillion in 2024, and is expected to reach USD 3.77 trillion by 2029, growing at a CAGR of 18.23% during the forecast period (2024-2029).

- COVID-19 posed significant challenges for healthcare organizations. The need to quickly ramp up testing and tracing strategies and maintain continuity of care for patients with ongoing medical and social needs increased the demand for value-based healthcare services during the pandemic. Many value-based providers (VBP) also used claims and clinical data to create algorithms and other tools to identify and support high-risk individuals. This increased the rapid adaptation of accountable care organizations to provide quality care to vulnerable patients during the pandemic.

- For instance, as per an article published in Healthcare, in June 2022, Aledade, a VBP enabler, operated 39 Medicare Shared Savings Program (MSSP) accountable care organizations across 27 states, with a total of 467 practices and 440,000 patients attributed to such programs during the spring of the pandemic period. Thus, the high utilization of value-based services has increased the market growth during the pandemic. Moreover, with the growing demand for healthcare delivery services and integrated care models, the studied market is expected to grow over the forecast period.

- Factors such as the rising incidence of chronic diseases, increasing government initiatives, and the growing demand for more integrated care delivery models are expected to boost market growth over the forecast period.

- The increasing burden of chronic diseases among the population raises the need for value-based healthcare services to cut down unnecessary healthcare spending, propelling market growth. For instance, according to 2022 statistics published by the International Diabetes Federation, about 536 million people were living with diabetes globally in 2021, and this number is projected to reach 643 million and 784 million by 2030 and 2045, respectively.

- Additionally, according to an article published in the European Respiratory Journal, in November 2021, about 36.5 million Europeans were suffering from chronic obstructive pulmonary disease (COPD) during the pandemic, and projected to reach 49.5 million by 2050, which represents a 35.2% relative increase in number of patients. This increases the demand for value-based care models, which helps in reducing uncertainty for chronic disease patients and improving their interactions with providers, hence providing medical and financial benefits to patients. Such factors are anticipated to augment the market growth over the forecast period.

- Furthermore, novel approaches and programs are being introduced by the government and organizations as a result of the rising emphasis on promoting value-based healthcare services among providers and patients. For instance, in January 2023, the National Health Authority (NHA) introduced a new system to measure and grade hospital performance under the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY) scheme to move the focus of measuring the hospital's performance from volume to value of healthcare services.

- Moreover, according to the data published by the Rural Health Value, in February 2023, the Department of Health and Human Services (HHS) developed several value-based initiatives, particularly through the Centres for Medicare and Medicaid Services (CMS) and its Centre for Medicare and Medicaid Innovation (CMMI) to assist rural leaders and communities in identifying HHS value-based initiatives suitable for rural participation. Such initiatives are anticipated to expand the use of integrated care models for effectively managing patient disease, thereby boosting market growth.

- Therefore, owing to the aforementioned factors, such as the high burden of chronic diseases, rising government initiatives, and the growing demand for value-based care delivery models, the studied market is anticipated to grow over the forecast period. However, challenges in balancing two reimbursement and payment mechanisms are likely to hinder the growth of the value-based healthcare services market over the forecast period.

Value-based Healthcare Services Market Trends

Shared Savings Segment Expects to Register a High CAGR Over the Forecast Period

- The shared saving is a value-based model that encourages a group of doctors, hospitals, and other healthcare providers to form an accountable care organization (ACO) to provide coordinated and high-quality care to their Medicare beneficiaries. This model offers a high level of financial reward as compared to other models, such as pay-for-performance models. This coordinated care guarantees that patients receive the appropriate treatment at the right moment by minimizing provider fragmentation. The Affordable Care Act established the shared savings program, which is the largest accountable care initiative and a permanent program in Medicare.

- The shared savings segment is anticipated to witness significant growth over the forecast period owing to factors such as rising government initiatives to launch new models and programs as well as the several advantages offered by the shared saving models, including minimizing needless duplication of services and eliminating medical mistakes.

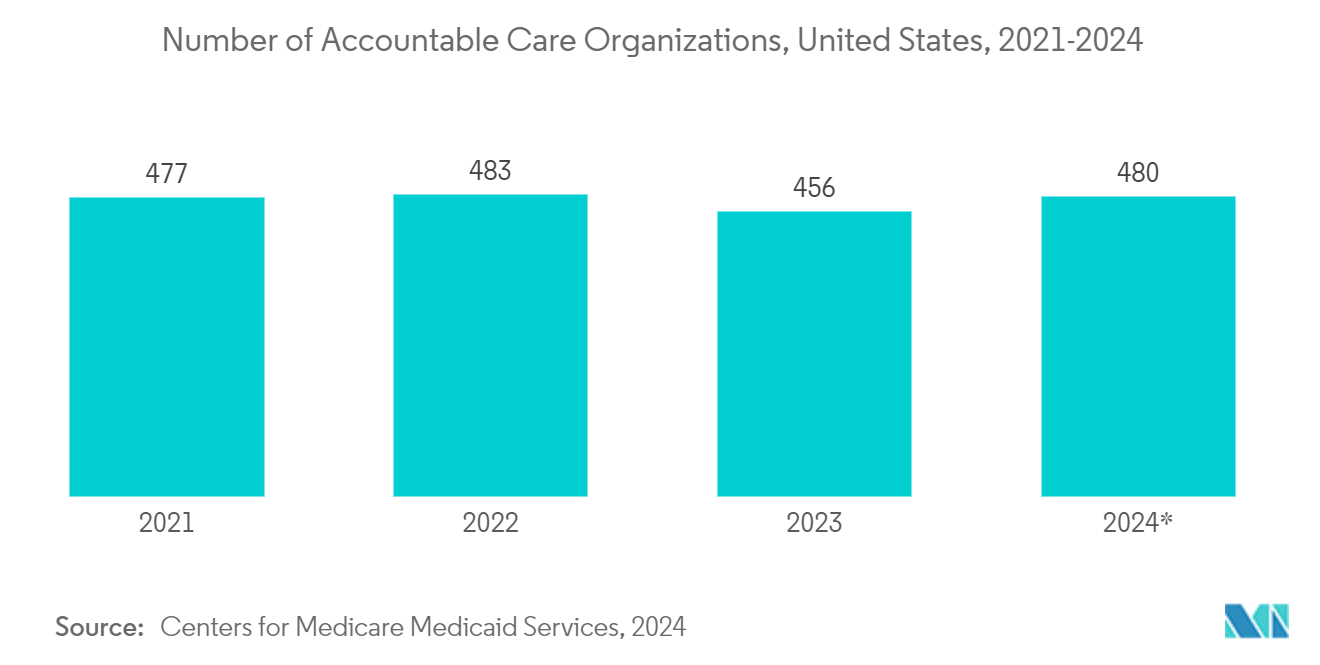

- The growing initiatives to bring healthcare providers as accountable care organizations help to improve the sustainability of the Medicare program while providing Medicare patients with high-quality treatment. For instance, in January 2023, CMS launched three innovative accountable care initiatives: the Medicare Shared Savings Programme, Community Health (ACO REACH) Model, and the Kidney Care Choices (KCC) Model and Accountable Care Organisation Realising Equity, Access Model. These initiatives are expected to deliver higher-quality care to more than 13.2 million people with Medicare in 2023. Thus, such initiatives are anticipated to fuel the segment growth over the forecast period.

- Furthermore, as per the data published in the Shared Savings Program Fast Facts, in January 2023, the shared savings program has 483 ACOs and 11 million assigned beneficiaries in 2022, as compared to 477 ACOs and 10.7 million assigned beneficiaries in 2021. ����vlog��ý 2 billion earned shared savings were recorded by CMS in the year 2021. Thus, the increasing number of ACOs in shared savings programs is anticipated to fuel segment growth.

- Therefore, owing to the aforementioned factors, the shared savings segment is expected to grow over the forecast period.

North America is Expected to Have the Significant Market Share Over the Forecast Period

- North America is anticipated to hold a significant share of the market over the forecast period owing to factors such as the rising prevalence of chronic diseases, increasing geriatric population, and presence of well-established healthcare infrastructure, along with high healthcare spending. In addition, the presence of favorable Medicare reimbursement policies is also expected to boost the market growth in the region.

- The government's increasing focus on promoting the adoption and transformation of various fee-for-service models into value-based healthcare models is also anticipated to fuel market growth. For instance, CMS has introduced various value-based care models, such as the Medicare Shared Savings Programme, Next Generation ACO model, and Pioneer Accountable Care Organisation (ACO) model, to change how healthcare providers are compensated for the services they provide to patients. Also, in September 2021, CMS, the Department of Health and Human Services (HHS), released a rule stating the expansion of the Home Health Value-Based Purchasing (HHVBP) model to all Medicare-certified HHAs in the 50 states, territories, and the District of Columbia. The expanded model aims to increase the quality and efficiency of home health care to improve patients' experience and to address health concerns before the requirement of an emergency department visit. Thus, such government initiatives are expected to increase the adoption of value-based care models, thereby propelling market growth.

- Furthermore, the rise in healthcare expenditure in the region is expected to increase the adoption of value-based services for home healthcare, hence contributing to market growth. For instance, as per the Centers for Medicare and Medicaid Services (CMS) August 2022 update, the national health expenditure (NHE) grew 2.7% to USD 4.3 trillion in 2021, or USD 12,914 per person, which accounted for 18.3% of Gross Domestic Product (GDP) of the country. Additionally, as per the source mentioned above, medicare spending grew 8.4% to USD 900.8 billion in 2021, and Medicaid spending grew 9.2% to USD 734.0 billion in 2021.

- Moreover, the rising focus of the companies to launch various value-based services in the region is also contributing to market growth. For instance, in June 2021, Curation Health expanded its value-based services, including the Value-Based Care Strategic Planning program and Provider Incentive Management program. These new services empower providers and health plans to collaborate in value-based agreements more effectively.

- Therefore, owing to the aforementioned factors, the studied market is expected to grow over the forecast period.

Value-based Healthcare Services Industry Overview

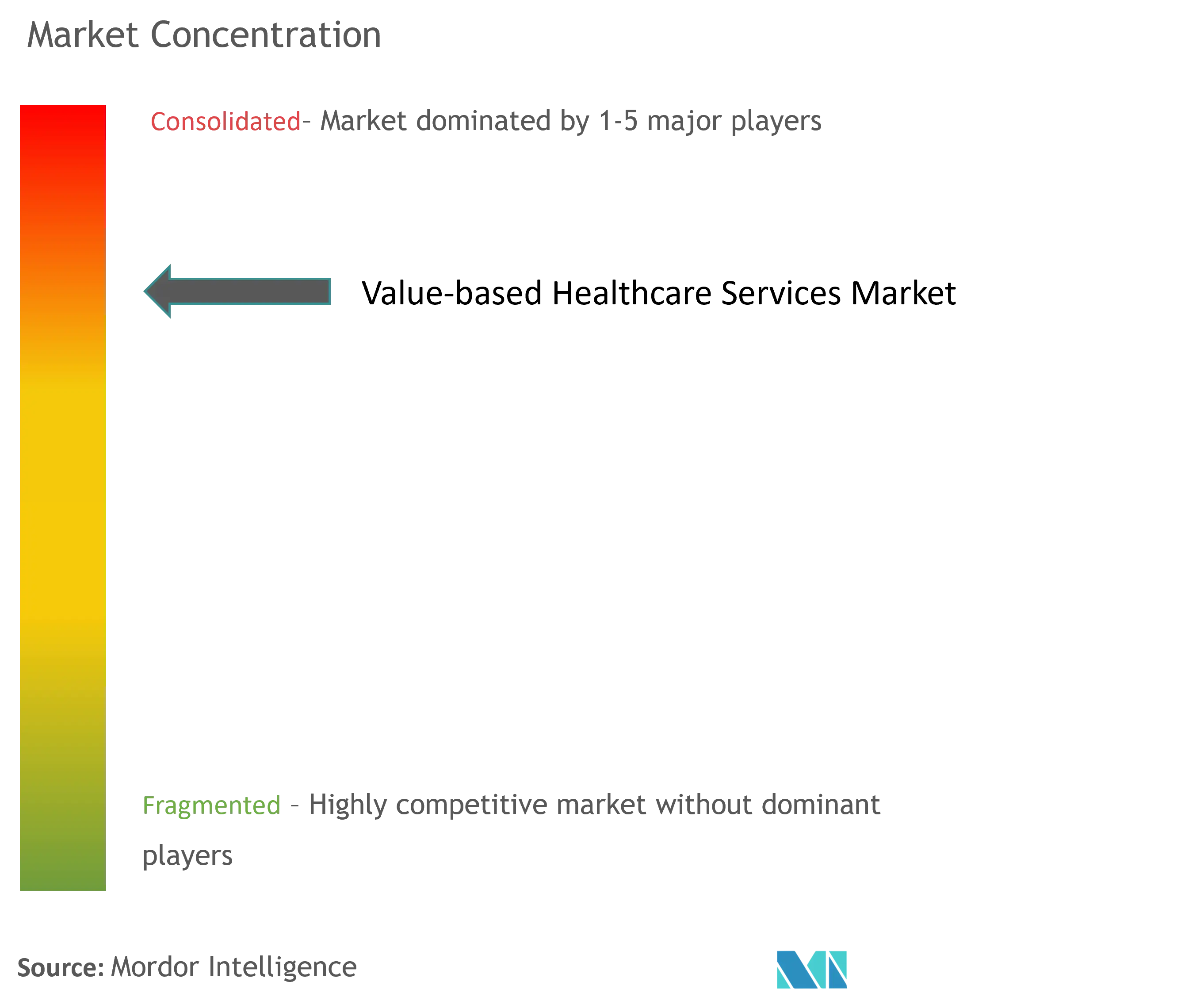

The market for value-based healthcare services is moderately consolidated, with the presence of a few players in the industry. Companies like MVP Health Care, Blue Cross and Blue Shield of Minnesota, Humana, Blue Cross and Blue Shield of North Carolina, UNITEDHEALTH GROUP, Aetna Inc., Cigna Healthcare, Anthem Insurance Companies, Inc., and Kaiser Permanente hold a substantial market share in the value-based healthcare services market.

Value-based Healthcare Services Market Leaders

-

MVP Health Care

-

Humana

-

Blue Cross and Blue Shield of North Carolina

-

UNITEDHEALTH GROUP

-

Cigna Healthcare

*Disclaimer: Major Players sorted in no particular order

Value-based Healthcare Services Market News

- April 2023: Kaiser Foundation Hospitals and Geisinger Health launched Risant Health, a new non-profit organization, to expand and accelerate the adoption of value-based care in diverse, multi-payer, multi-provider, community-based health system environments.

- February 2023: Blue Cross and Blue Shield of Minnesota and Homeward entered into a full-risk value-based care arrangement to increase access in rural Minnesota.

Value-based Healthcare Services Market Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Incidence of Chronic Diseases and Increasing Government Initiatives

4.2.2 Growing Demand For More Integrated Care Delivery Models

4.3 Market Restraints

4.3.1 Challenges in Balancing Two Reimbursement Types and Payment Mechanisms

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Models

5.1.1 Bundled Payments

5.1.2 Pay for Performance

5.1.3 Patient-Centered Medical Home (PCMH)

5.1.4 Shared Savings

5.1.5 Other Models

5.2 By Providers

5.2.1 Home Health Care

5.2.2 Hospital Therapy

5.2.3 Other Providers

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 MVP Health Care

6.1.2 Blue Cross and Blue Shield of Minnesota

6.1.3 Humana

6.1.4 Blue Cross and Blue Shield of North Carolina

6.1.5 UNITEDHEALTH GROUP

6.1.6 Aetna Inc.

6.1.7 Cigna Healthcare

6.1.8 Anthem Insurance Companies, Inc.

6.1.9 Kaiser Permanente

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Value-based Healthcare Services Industry Segmentation

Value-based care is a medical services model in which practitioners and providers are paid based on the quality of their care.

The value-based healthcare services market is segmented by models, providers, and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). By models, the market is segmented into bundled payments, pay for performance, patient-centered medical home, shared savings, and other models. By providers, the market is segmented into home health care, hospital therapy, and other providers. The report also covers the market sizes and forecasts for the value-based healthcare services market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Models | |

| Bundled Payments | |

| Pay for Performance | |

| Patient-Centered Medical Home (PCMH) | |

| Shared Savings | |

| Other Models |

| By Providers | |

| Home Health Care | |

| Hospital Therapy | |

| Other Providers |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Value-based Healthcare Services Market Market Research Faqs

How big is the Value-based Healthcare Services Market?

The Value-based Healthcare Services Market size is expected to reach USD 1.63 trillion in 2024 and grow at a CAGR of 18.23% to reach USD 3.77 trillion by 2029.

What is the current Value-based Healthcare Services Market size?

In 2024, the Value-based Healthcare Services Market size is expected to reach USD 1.63 trillion.

Who are the key players in Value-based Healthcare Services Market?

MVP Health Care, Humana, Blue Cross and Blue Shield of North Carolina, UNITEDHEALTH GROUP and Cigna Healthcare are the major companies operating in the Value-based Healthcare Services Market.

Which is the fastest growing region in Value-based Healthcare Services Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Value-based Healthcare Services Market?

In 2024, the North America accounts for the largest market share in Value-based Healthcare Services Market.

What years does this Value-based Healthcare Services Market cover, and what was the market size in 2023?

In 2023, the Value-based Healthcare Services Market size was estimated at USD 1.33 trillion. The report covers the Value-based Healthcare Services Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Value-based Healthcare Services Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Value-based Healthcare Services Market Industry Report

Statistics for the 2024 Value-based Healthcare Services market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Value-based Healthcare Services analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.