ASEAN Warehousing And Distribution Logistics Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

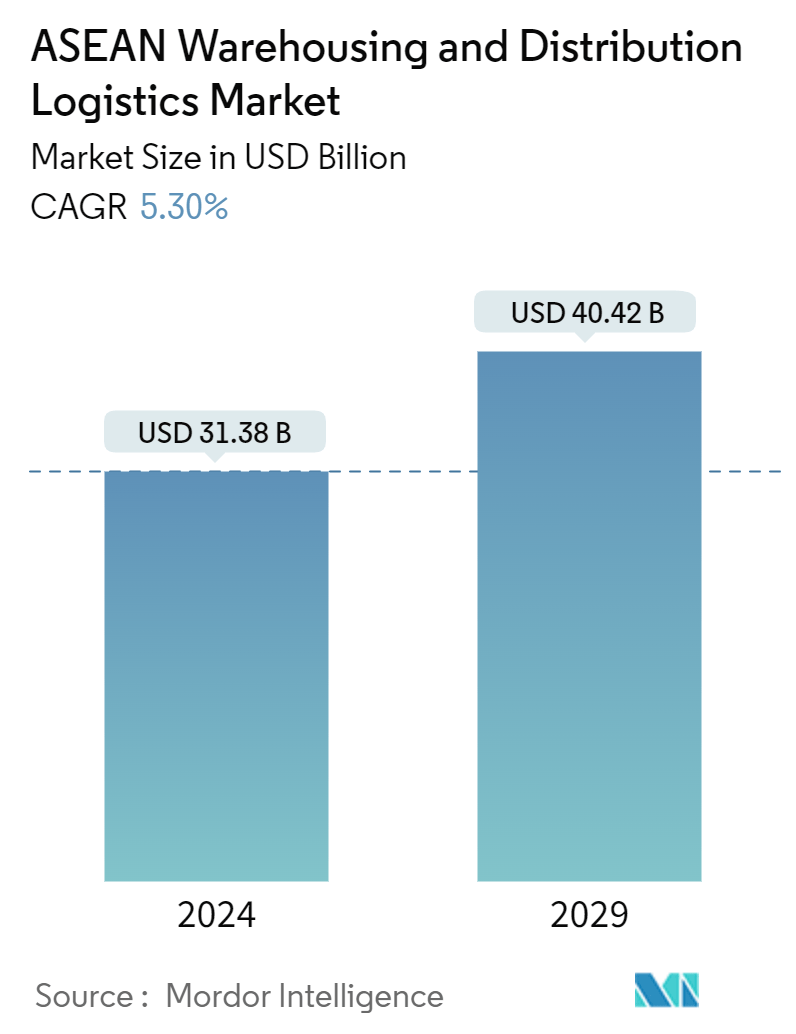

| Market Size (2024) | USD 31.38 Billion |

| Market Size (2029) | USD 40.42 Billion |

| CAGR (2024 - 2029) | 5.30 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

ASEAN Warehousing And Distribution Logistics Market Analysis

The ASEAN Warehousing And Distribution Logistics Market size is estimated at USD 31.38 billion in 2024, and is expected to reach USD 40.42 billion by 2029, growing at a CAGR of 5.30% during the forecast period (2024-2029).

As one of the world’s fastest-growing economies, Southeast Asia has benefitted from a broad-based economic growth model based on global trade, inward investment, and regional and global integration into value chains. However, sustaining this growth momentum will necessitate several reforms to strengthen the region's economic and social resilience. These reforms will include lowering regulatory barriers to competition and market entry to promote innovation, productivity, and efficiency.

Warehousing and distribution logistics in ASEAN are expected to experience rapid growth due to the rapid growth of the e-commerce sector. The high demand for last-mile logistics and the fast-developing transportation infrastructure contribute to the development of ASEAN's warehousing and distribution logistics market. The presence of foreign firms in the region, as well as government initiatives like Adapt and Grow & Go Digital, in addition to the growing logistics industry, is driving the growth of the warehousing and distribution market in the region. Singapore is one of the major countries in ASEAN. With its geographical location and strong freight and logistics business, it is one of the fastest-growing countries in the region. Major players in the region have significantly funded the warehouse infrastructure.

Warehousing demand has been on the rise in some regions, mainly due to the growth of e-commerce. The previous year, BW (Vietnam’s #1 Industrial For-Rent Developer), specializing in developing warehouses and factories to rent, received unprecedented requests. BW’s long-term development strategy allowed it to take advantage of these short-term opportunities effectively by constructing light and contemporary industrial warehouses to cater to the growing manufacturing demand and the explosion of e-commerce growth.

The demand for cold storage is rising, forcing companies to adjust their supply chain strategies. According to the industry report, foreign investors are increasingly interested in building cold storage facilities in Vietnam to benefit from the urbanization process and retail modernization, changing how Vietnam’s big cities get fresh food. The supply chains are expected to become more efficient in the future due to significant infrastructure investment and development, including the construction of the long-awaited Long Thanh International Airport.

ASEAN Warehousing And Distribution Logistics Market Trends

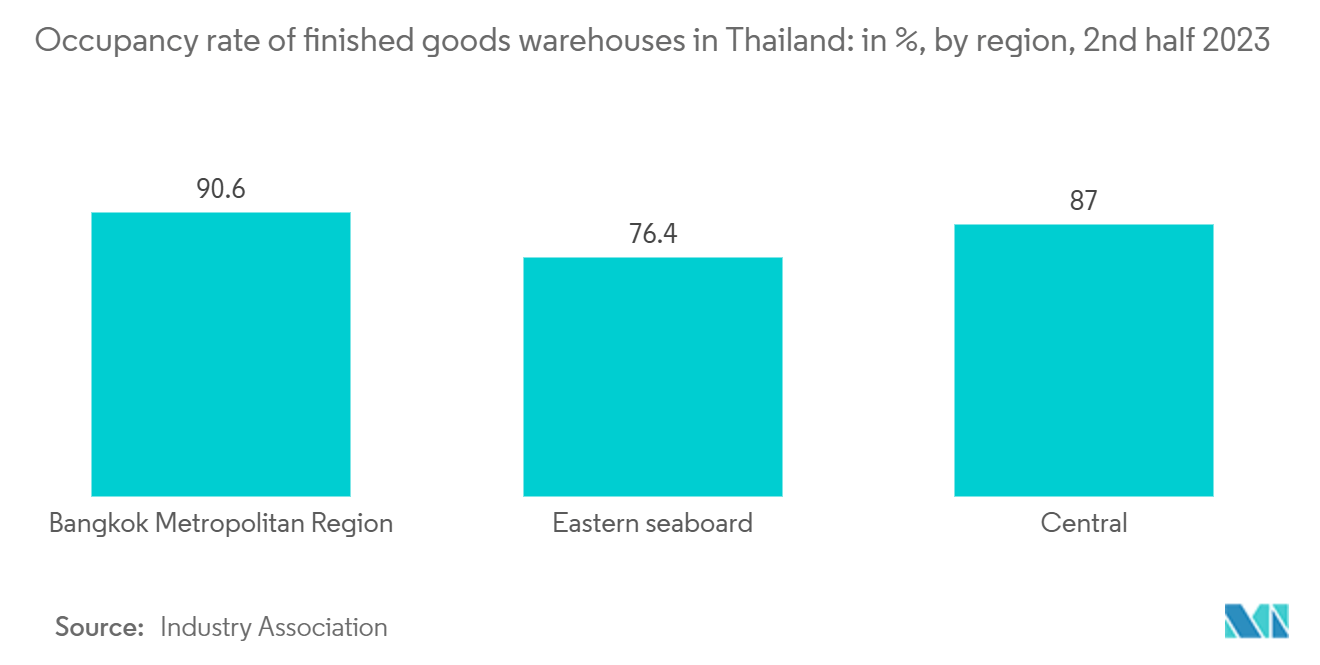

Increase in Warehousing Space in Thailand

Warehouses are not just storage rooms. They house value-added operations such as just-in-time packing, assembly, product customization, etc. Over the past five years, Thailand has seen incredible growth in e-commerce. The e-commerce warehousing cluster is between 15 and 23 km along Bang Na-trat Road in Bangkok.

Thailand has seen massive growth in the retail market in recent years. There has been a steady rise in organized retail or contemporary shopping nationwide. The increasing disposable income of the people in Thailand, the large youth population, and the booming tourism industry have attracted a lot of foreign brands. This has led to an increase in warehousing services.

During the forecast period in Thailand, operators of leased warehouse space will continue to experience business growth in line with a gradual economic upturn, driven mainly by an upturn in the export industry and a recovery in domestic retail. Investment in new supply tends to increase over the next three years. Large players will be at the forefront of this, leading to oversupply in some local markets, increasing competition on pricing, and limiting operators’ ability to increase rents.

Currently, the majority of operations are modernizing their facilities to provide modern warehousing solutions, which, in turn, allows them to expand their client base and generate revenue through additional services. Players are also modernizing their facilities through other means, such as upgrading their warehouse buildings to meet industry standards (for example, the LEED scheme), investing in energy efficiency and environmental protection, and installing facilities that enhance resilience to natural disasters, such as flooding and earthquakes. Warehouses have expanded their floor and ceiling space, increasing the speed and ease of goods movement.

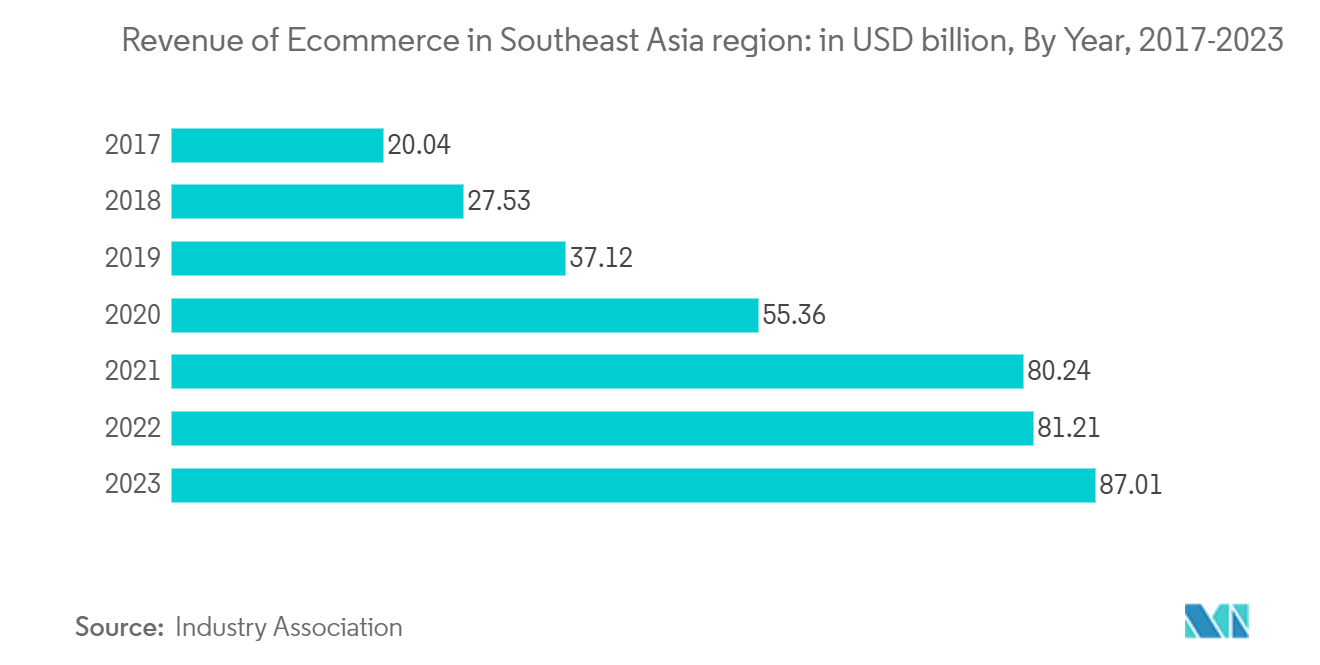

E-commerce Growth in the ASEAN Region is Driving the Market

The current phase of e-commerce in Southeast Asia is about more than just increasing value. Consumers in the region increasingly purchase a wider range of products online through various channels. The region's supply chains will likely require new logistics capabilities to meet this growing demand for fulfillment. Those who already possess these capabilities and those new to the market will benefit the most from these changes.

Southeast Asia is a patchwork quilt of economies at various stages of development; it is only natural that e-commerce penetration rates vary from country to country. Indonesia and Singapore account for approximately 30% of the region’s e-commerce penetration, with the Philippines, Thailand, and Vietnam trailing at around 15% each. The largest Southeast Asian economy, Indonesia, accounts for 51 of the region's GMV growth due to its large consumer market.

As Southeast Asia's e-commerce market moves into the next phase of growth, customers will make more digital purchases across all product categories and channels, and they will also demand and pay more for new and advanced logistics solutions. On the other hand, merchants will be less reliant on Chinese imports and expand their sourcing channels to more Southeast Asian countries as they migrate their supply chains. As a result, they will look to extend their upstream capabilities to access a wider value mix, which will open up more channels for logistics providers.

ASEAN Warehousing And Distribution Logistics Industry Overview

The warehousing and distribution market in the ASEAN region is fragmented, with many players trying to grab a significant chunk of the developing market. Some of the countries in the ASEAN region, like Indonesia and the Philippines, are moderately growing, with many local players and some international players. However, Singapore, Vietnam, and Thailand are highly competitive markets, with the presence of a large number of international players. CEVA, Yusen Logistics, Kerry Logistics, and DHL are among the major players present in the region. Increasing pressure from e-commerce and international trade has allowed the players to develop many warehouses in the region. Due to the long-term domestic presence, local players and distributors have been able to compete with international players.

ASEAN Warehousing And Distribution Logistics Market Leaders

-

Agility Logistics

-

DB Schenker Logistics

-

DHL Group

-

CJ Century Logistics

-

Linfox

*Disclaimer: Major Players sorted in no particular order

ASEAN Warehousing And Distribution Logistics Market News

- October 2023: DHL Supply Chain, the leading provider of contract logistics solutions worldwide, intended to allocate EUR 350 million (USD 385.86 million) for expansion efforts across Southeast Asia within the next five years. This investment aims to enhance warehousing capacity, bolster the workforce, and advance regional sustainability initiatives.

- August 2023: Eve Air Mobility announced signing an MoU with DHL Supply Chain to conduct a Key Requirements and Supply Chain Characteristics Study for Eva’s Electric Vertical Take-off and Landing Aircraft (eVTOL). The primary objective of this partnership is to identify and validate best practices for supplying spare parts and inputs to operators and service centers. The focus will be on batteries and the particular requirements for transporting, storing, and disposing of these devices. The study will also cover other aspects such as transport modes, frequency and delivery plans, logistics partners, locations for advanced inventory, physical and technical infrastructure requirements, and contingency plans.

ASEAN Warehousing And Distribution Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3. EXECUTIVE SUMMERY

4. MARKET INSIGHTS AND DYNAMICS

4.1 Current Market Scenario

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 The strategic placement of warehouses in key locations plays a crucial role

4.2.1.2 Warehousing Spaces are Increasing in the region due to the rise in e-commerce

4.2.2 Restraints

4.2.2.1 The logistics and warehouse distribution market is highly competitive, with both domestic and international players

4.2.2.2 Complex regulatory frameworks, including taxes, permits, and licensing requirements, can create barriers to entry

4.2.3 Opportunities

4.2.3.1 Automation plays a significant role in building the warehouse of the future

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.4 Value Chain / Supply Chain Analysis

4.5 Government Regulations in ASEAN Countries

4.6 Technological Developments in Warehousing

4.7 Insights into Warehousing Rents

4.8 Insights into General Warehousing

4.9 Insights into Dangerous Goods Warehousing

4.10 Insights into Refrigerated Warehousing

4.11 Insights into the Effects of E-commerce Growth

4.12 Insights into Free Zones and Industrial Parks

4.13 Impact of COVID-19 on the market

5. MARKET SEGMENTATION

5.1 By Geography

5.1.1 Singapore

5.1.2 Thailand

5.1.3 Malaysia

5.1.4 Vietnam

5.1.5 Indonesia

5.1.6 Philippines

5.1.7 Rest of ASEAN

6. COMPETITIVE LANDSCAPE

6.1 Overview (Market Concentration and Major Players)

6.2 Company Profiles

6.2.1 DHL Supply Chain

6.2.2 Ceva Logistics

6.2.3 CJ Century Logistics

6.2.4 DB Schenker

6.2.5 Agility

6.2.6 Linfox

6.2.7 Kuehne + Nagel

6.2.8 Yusen Logistics

6.2.9 Kerry Logistics

6.2.10 CWT Ltd

6.2.11 Gemadept

6.2.12 Tiong Nam Logistics

6.2.13 Ych Group

6.2.14 Singapore Post

6.2.15 WHA Corporation

6.2.16 Keppel Logistics*

- *List Not Exhaustive

6.3 Other Companies (Key Information/Overview)

7. FUTURE TRENDS AND OPPORTUNITIES

8. APPENDIX

ASEAN Warehousing And Distribution Logistics Industry Segmentation

Sales logistics and distribution logistics deal with the organization, execution, and management of the transportation of commodities. Holding tangible inventory for eventual sale or distribution is known as warehousing. A complete background analysis of the ASEAN warehousing and distribution logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The ASEAN logistics market is segmented by geography (Singapore, Thailand, Indonesia, Malaysia, Vietnam, the Philippines, and the Rest of ASEAN).

The report offers the market size in value terms in (USD) for all the above-mentioned segments.

| By Geography | |

| Singapore | |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Indonesia | |

| Philippines | |

| Rest of ASEAN |

ASEAN Warehousing And Distribution Logistics Market Research Faqs

How big is the ASEAN Warehousing And Distribution Logistics Market?

The ASEAN Warehousing And Distribution Logistics Market size is expected to reach USD 31.38 billion in 2024 and grow at a CAGR of 5.30% to reach USD 40.42 billion by 2029.

What is the current ASEAN Warehousing And Distribution Logistics Market size?

In 2024, the ASEAN Warehousing And Distribution Logistics Market size is expected to reach USD 31.38 billion.

Who are the key players in ASEAN Warehousing And Distribution Logistics Market?

Agility Logistics, DB Schenker Logistics, DHL Group, CJ Century Logistics and Linfox are the major companies operating in the ASEAN Warehousing And Distribution Logistics Market.

What years does this ASEAN Warehousing And Distribution Logistics Market cover, and what was the market size in 2023?

In 2023, the ASEAN Warehousing And Distribution Logistics Market size was estimated at USD 29.72 billion. The report covers the ASEAN Warehousing And Distribution Logistics Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the ASEAN Warehousing And Distribution Logistics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

ASEAN Warehousing And Distribution Logistics Industry Report

Statistics for the 2024 ASEAN Logistics and Warehouse Distribution market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. ASEAN Logistics and Warehouse Distribution analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.