Gas Detector Market Size

| Study Period | 2019 - 2029 |

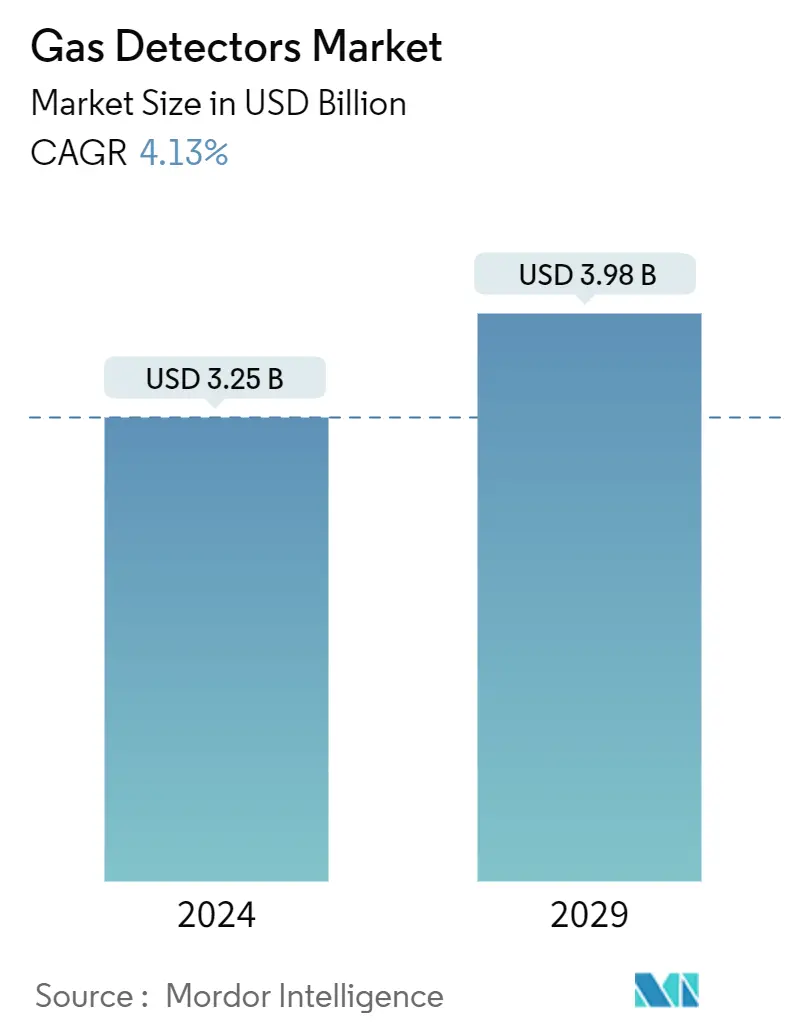

| Market Size (2024) | USD 3.25 Billion |

| Market Size (2029) | USD 3.98 Billion |

| CAGR (2024 - 2029) | 4.13 % |

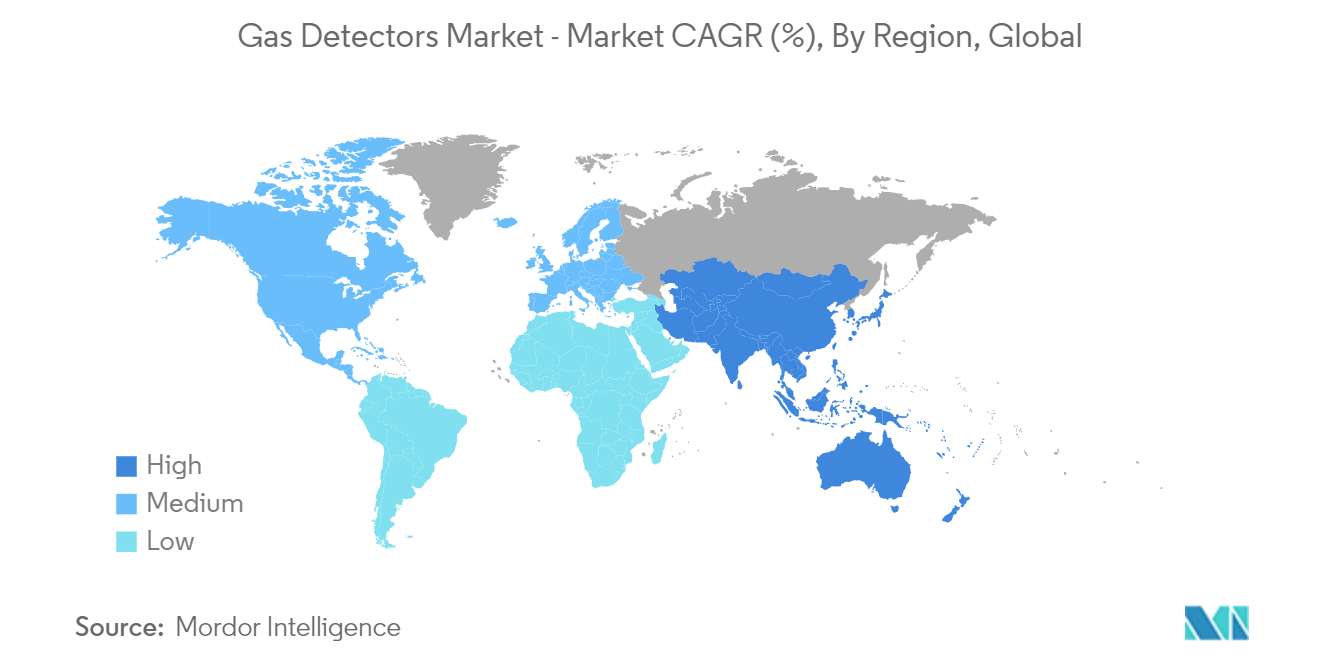

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

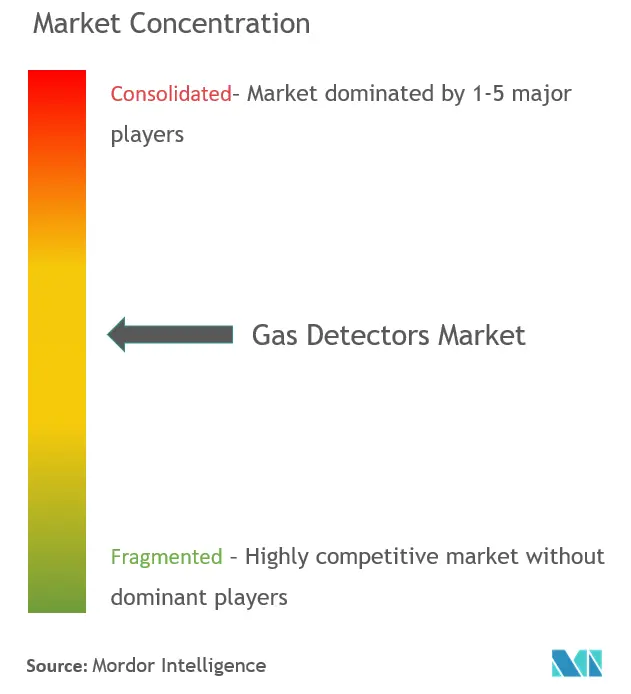

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Gas Detector Market Analysis

The Gas Detectors Market size is estimated at USD 3.25 billion in 2024, and is expected to reach USD 3.98 billion by 2029, growing at a CAGR of 4.13% during the forecast period (2024-2029).

- Several factors, like the increasing awareness of workplace safety, advancements in technology leading to enhancements in accuracy, reliability, use of gas detectors, rapid industrialization, and growing focus on environmental monitoring, are anticipated to drive the growth of the studied market significantly.

- Several major market vendors are developing advanced gas detectors with applications across clinical assays, environmental emission control, explosive detection, agricultural storage, shipping, and workplace hazard monitoring. For instance, in July 2023, ATO Inc. introduced its new line of multi-gas detectors for confined spaces and other complex environments. It is claimed to improve worker safety by quickly identifying poisonous compounds, flammable gases, and oxygen levels by monitoring up to four different gases simultaneously.

- Stringent government regulations have also resulted in the efficiency enhancement of combustion within the vehicle to limit the emission of harmful pollutants. This has further increased the adoption of gas sensors and detectors, therefore gaining applications in providing real-time feedback to emission management systems of automobiles. In June 2023, the Biden-Harris Administration launched a whole-of-government initiative to significantly reduce greenhouse gas emissions. In addition, President Biden's national goal is to cut global methane emissions by 30 percent below 2020 levels by 2030, which also plays an important role in the penetration of gas detectors in the automotive industry. The increasing cases of gas leaks in various end-user industries are further creating a demand for gas detectors.

- Wireless/portable gas detectors are also witnessing widespread adoption owing to their reduced initial implementation costs and recurrent savings, lower maintenance costs, better workforce management, faster resource workflow, and improved safety. Moreover, the development of sensor capabilities and miniaturization, coupled with improved communication capabilities, enables the integration of IoT sensors into numerous machines and devices without compromising the detection of toxic or flammable gases at safe distances. As IoT sensors' cost is declining, industries dealing with hazardous/explosive materials have started integrating these sensors into their day-to-day operations to improve environmental safety and operational efficiency.

- Governmental agencies have been taking proactive measures to enforce the use of gas detectors in potentially hazardous locations, where they are seen as a vital cog for triggering emergency procedures across several industries in case of an abnormal increase in the concentration of gases that are actively employed for monitoring the air quality and detection of combustible gases primarily in the chemical, industrial, medical, and automotive industries. With increased R&D efforts, along with the technological advancements by some prominent players, technologies such as tunable diode lasers (TDLA) are being developed, which detect and measure gases at a low density of air, thereby offering several measurement advantages, such as highly stable calibration and less cross-interference from the presence of other gases.

- On the flip side, the lack of skilled labor is an essential restraining factor for the gas detector market. Training associated with specific applications of gas leak detectors is essential, and the shortage of skilled personnel could hinder the adoption and effective use of gas detectors.

- Further, the high cost of production of wireless gas detectors and the inability of the detectors to restrict probable fire hazards could hinder the widespread adoption of gas detectors.

Gas Detector Market Trends

Oil and Gas Sector is Expected to Hold Major Share

- The market for gas detectors is expected to continue to rise, especially in the industrial sector, as there is an increasing need for gas monitoring amenities to identify the presence of hazardous gases. The use of IoT in the oil and gas sector has resulted in improved field communication, real-time monitoring, digital infrastructure for oil fields, decreased maintenance costs, lower power consumption, more production, and increased safety and security for workers and assets. For instance, petrol waste is a serious problem that must be resolved. Liquefied petroleum gas is highly combustible and dangerous to both people and property. When used in conjunction with IoT, gas detectors can significantly aid in gas detection and prevent gas wastage.

- According to the Organization of the Petroleum Exporting Countries, the global demand for crude oil (including biofuels) in 2022 amounted to over 99.57 million barrels per day, and it is estimated to increase to approximately 101.89 million barrels per day in 2023. Also, according to EIA, the worldwide consumption of liquid fuels is forecasted to reach approximately 102.14 million barrels per day by the end of 2023. The increasing demand for crude oil and fuel is likely to boost the growth of the studied market.

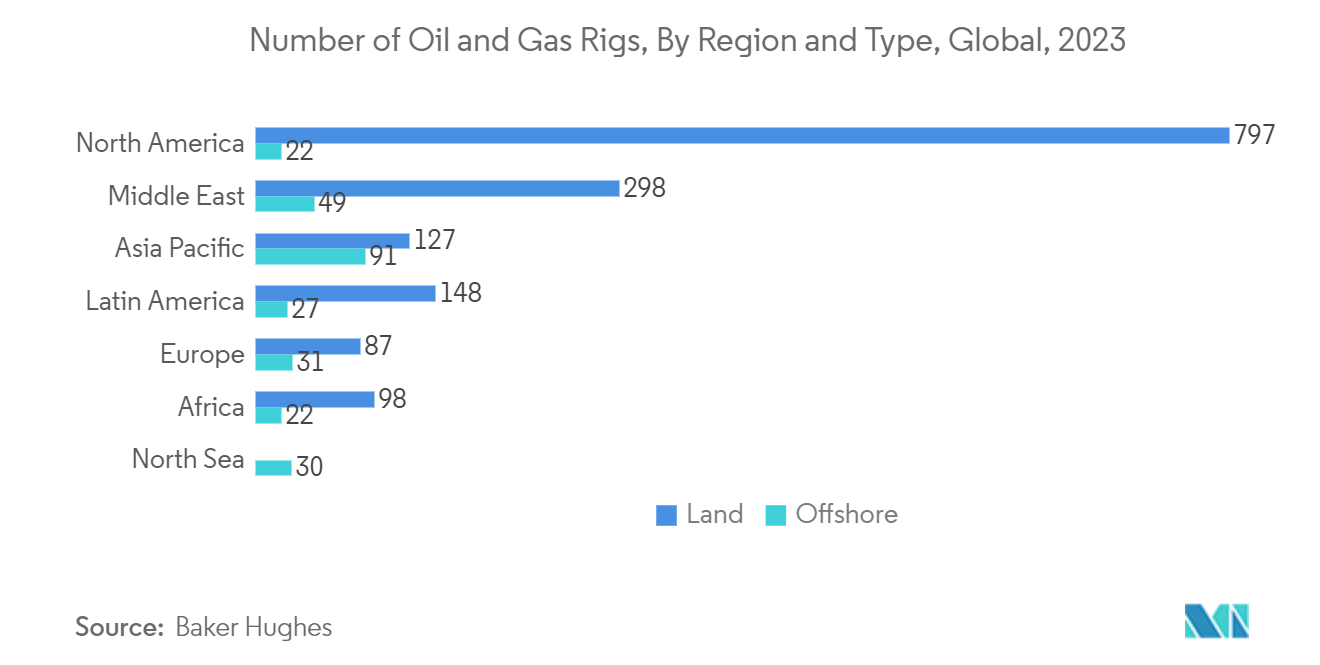

- North America is estimated to witness robust growth owing to the presence of numerous oil rigs. According to Baker Hughes, North America hosts the most oil and gas rigs worldwide. As of November 2023, there were 797 land rigs in that region, with a further 22 rigs located offshore. By the end of 2023, there were 1,555 operational onshore oil rigs globally, compared with 272 offshore rigs.

- The National Outer Continental Shelf Oil and Gas Leasing Program for 2019-24, approved by the U.S. Department of the Interior (DoI), allows for offshore exploratory drilling on nearly 90% of the Outer Continental Shelf (OCS) acreage, and this is expected to create new opportunities for the market vendors under consideration.

- According to the RegData's Industry Regulation Index, the oil and gas extraction industry is among the top 10 most regulated industries in the United States. Regulatories like the Bureau of Safety and Environmental Enforcement (BSEE) - which enforces safety and environmental protection regulations for the offshore oil & natural gas industry in the United States - are also prevalent across regions like Europe. The strict rules imposed by such institutions facilitate the development of the gas detector market.

- According to the Oil & Gas Journal, companies that are utilizing advanced technologies to manage safety & operations performance are reported to have approximately 8 percent less unscheduled asset downtime (over those who do not), experience about 13 percent reduction in compliance-related costs, 8 percent fewer regulation citations, and realize operating margins 2 percent or greater than targeted in the corporate plan. Then, numerous benefits offered by gas detectors would augment the market demand during the forecast period.

North America is Expected to Hold Significant Share

- North America is witnessing the growth of gas detectors due to the presence of major vendors and government regulations regarding limiting gas emissions. In the North American region, the Environmental Protection Agency (EPA) and the U.S. Occupational Safety and Health Administration (OSHA) strictly implement industrial safety, driving the adoption of gas detectors.

- Almost all businesses in the United States are subject to OSHA standards, so they are a significant concern for employers and employees in various industries. The Environmental Protection Agency has released the New Source Performance Standards to measure and limit methane emissions from new, reconstructed, or modified assets.

- The EPA has also mandated the use of gas detectors in the mining industry. USA-based Carroll Technologies Group is a pioneer in offering handheld gas detectors for the mining industry. One of the products is the Mine Safety Appliances (MSA) Altair 4X Detector, which alerts the miner within 15 seconds of detection.

- Additionally, North America has one of the most active mining industries in the world. According to the Mining Association of Canada, Canada ranks among the top 5 members for the global production of 13 minerals and metals such as uranium, nickel, cobalt, potash, aluminum, diamonds, titanium, and gold. Further, according to the U.S. Geological Survey, in 2022, the capacity utilization of the United States' mining industry stood at an estimated 87 percent, which increased from 81 percent in 2021. Such instances are anticipated to offer lucrative opportunities for the growth of the studied market.

- The region is the primary hub for all the major manufacturing establishments worldwide. The regional authority further demands high safety concerns in countries such as the United States and Canada, which also encourages gas detectors to be deployed across the respective industries. Moreover, in October 2022, the United States Department of Labor's Mine Safety and Health Administration (MSHA) awarded USD 985,284 in grant funding to support safety courses and other programs.

Gas Detector Industry Overview

The gas detectors market is semi-consolidated and consists of several major players. In terms of market share, few major players currently dominate the market. With a prominent share in the market, these major players are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market share and profitability. The competition, rapid technological advancements, and frequent changes in consumer preferences are expected to threaten the growth of companies during the forecast period.

In October 2023 - Blackline Safety Corp. announced a significant upgrade to its G6 single-gas detector, adding new features and service plans to the life-saving wearable device. G6 features the same real-time connectivity as the company's G7 product line. Additional new features include an emergency SOS that workers can trigger in critical situations to get assistance and an expanded suite of data and reporting analytics. The device also supports indoor location technology.

In October 2022, Drager Marine & Offshore announced the release of the mobile gas detector, the X-am 2800. The new product simultaneously measured up to four different gases for application in confined spaces to safeguard employees working in areas at risk of explosive atmospheres, oxygen depletion, or those where toxic substances may be present.

Gas Detector Market Leaders

-

Honeywell International Inc.

-

Emerson Electric Company

-

MSA Safety Inc.

-

SENSIT Technologies

-

Drägerwerk AG & Co KgaA

*Disclaimer: Major Players sorted in no particular order

Gas Detector Market News

- December 2023 - CO2Meter, one of the leading manufacturers in gas detection solutions announced the release of an industrial gas detector designed to monitor gases in industrial environments. The highly anticipated CM-900 industrial gas safety series would measure either oxygen or carbon dioxide, protecting employees working near and around hazardous gases in the field. The environmentally adaptive industrial enclosure also creates advantages for both harsh and wash-down environments.

- September 2022: Riken Keiki Co. Ltd. developed an SD-3 fixed explosion-proof gas detector with global standards. It is an explosion-proof stationary gas detector for continuously monitoring flammable gas, toxic gas, and oxygen in the atmosphere.

Gas Detector Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitute Products

4.2.5 Intensity of Competitive Rivalry

4.3 Technology Snapshot

4.4 Assessment of the Impact of COVID-19

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Awareness about Hazards across Major Industries

5.1.2 Stringent Government Regulations for Safety of Workers

5.1.3 Companies Focusing on Smart Detectors

5.2 Market Restraints

5.2.1 Intense Competition in the Market

6. MARKET SEGMENTATION

6.1 By Communication Type

6.1.1 Wired

6.1.2 Wireless

6.2 By Type of Detector

6.2.1 Fixed

6.2.2 Portable and Transportable

6.3 By End-User Industry

6.3.1 Oil and Gas

6.3.2 Chemicals and Petrochemicals

6.3.3 Water and Wastewater

6.3.4 Metal and Mining

6.3.5 Utilities

6.3.6 Other End-User Industries

6.4 By Geography

6.4.1 North America

6.4.2 Europe

6.4.3 Asia Pacific

6.4.4 Latin America

6.4.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 Honeywell International Inc.

7.1.2 Dragerwerk AG & Co. KGaA

7.1.3 MSA Safety Inc.

7.1.4 Emerson Electric Company

7.1.5 SENSIT Technologies, LLC

7.1.6 Industrial Scientific Corporatioh

7.1.7 New Cosmos Electric Co. Ltd

7.1.8 Trolex Ltd

7.1.9 Crowncon Detection Instruments Limited

7.1.10 Hanwei Electronics Group Corporation

7.1.11 International Gas Detectors Ltd

7.1.12 Sensidyne LP

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Gas Detector Industry Segmentation

The presence of gases can be detected using a gas detector, which is frequently integrated into a safety system. Operators in the area where the leak is happening may hear a gas detector warning, which will give them a chance to flee.

The gas detectors market is segmented by communication type (wired and wireless), type of detector (fixed, portable, and transportable), end-user industry (oil and gas, chemicals and petrochemicals, water and wastewater, metal and mining, utilities), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Communication Type | |

| Wired | |

| Wireless |

| By Type of Detector | |

| Fixed | |

| Portable and Transportable |

| By End-User Industry | |

| Oil and Gas | |

| Chemicals and Petrochemicals | |

| Water and Wastewater | |

| Metal and Mining | |

| Utilities | |

| Other End-User Industries |

| By Geography | |

| North America | |

| Europe | |

| Asia Pacific | |

| Latin America | |

| Middle East and Africa |

Gas Detector Market Research FAQs

How big is the Gas Detectors Market?

The Gas Detectors Market size is expected to reach USD 3.25 billion in 2024 and grow at a CAGR of 4.13% to reach USD 3.98 billion by 2029.

What is the current Gas Detectors Market size?

In 2024, the Gas Detectors Market size is expected to reach USD 3.25 billion.

Who are the key players in Gas Detectors Market?

Honeywell International Inc., Emerson Electric Company, MSA Safety Inc., SENSIT Technologies and Drägerwerk AG & Co KgaA are the major companies operating in the Gas Detectors Market.

Which is the fastest growing region in Gas Detectors Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Gas Detectors Market?

In 2024, the North America accounts for the largest market share in Gas Detectors Market.

What years does this Gas Detectors Market cover, and what was the market size in 2023?

In 2023, the Gas Detectors Market size was estimated at USD 3.12 billion. The report covers the Gas Detectors Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Gas Detectors Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Industrial Gas Detectors Industry Report

Statistics for the 2024 Gas Detectors market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Gas Detectors analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.