Milk Packaging Market Size

| Study Period | 2019 - 2029 |

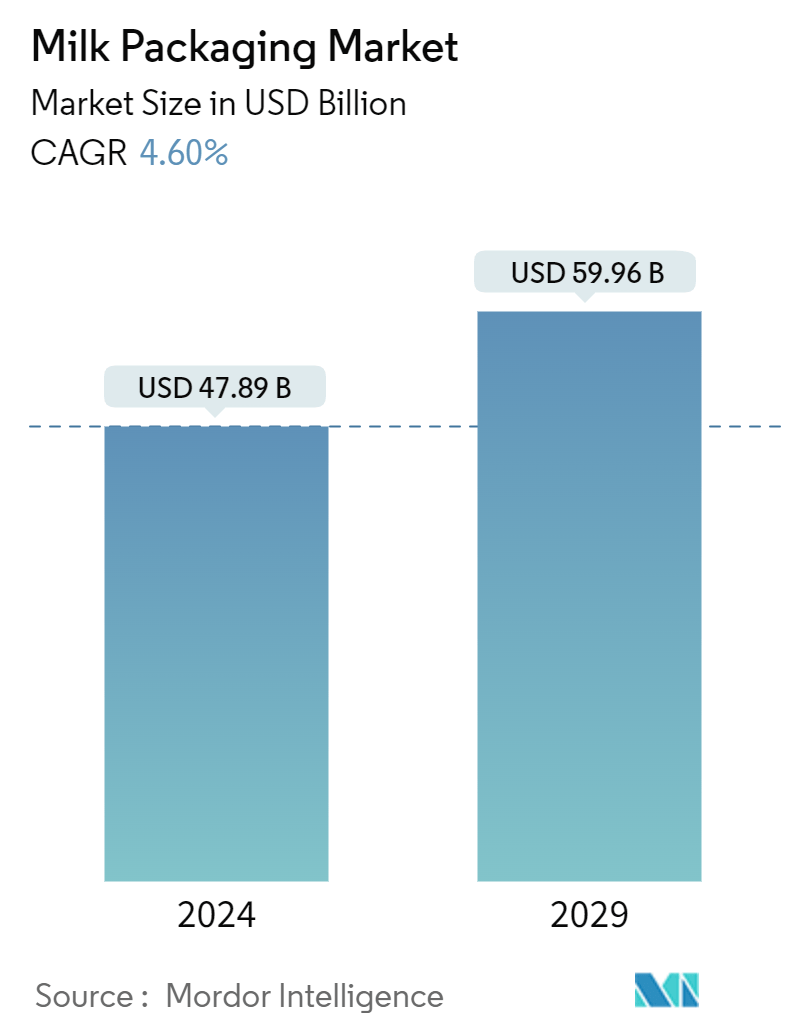

| Market Size (2024) | USD 47.89 Billion |

| Market Size (2029) | USD 59.96 Billion |

| CAGR (2024 - 2029) | 4.60 % |

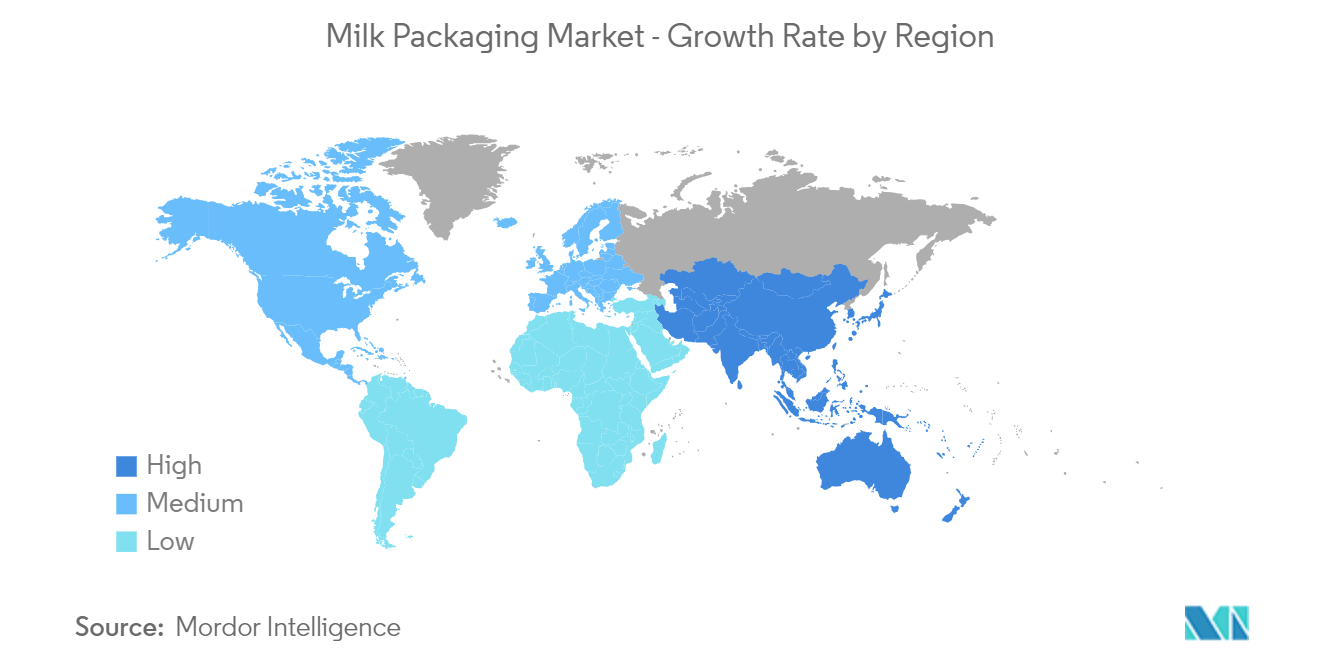

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

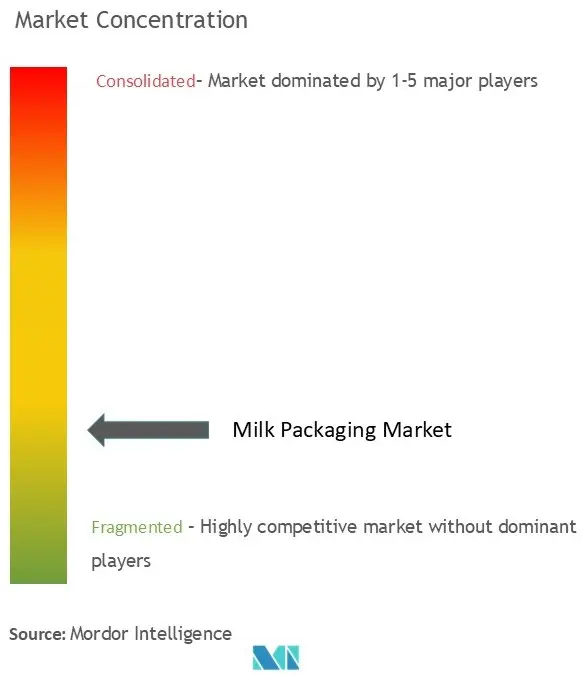

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Milk Packaging Market Analysis

The Milk Packaging Market size is estimated at USD 47.89 billion in 2024, and is expected to reach USD 59.96 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

Milk packaging is essential to protect milk from contamination, spoilage, and degradation by blocking out light, air, and bacteria, thereby extending its shelf life. Proper packaging ensures that milk remains hygienic and safe for consumption by preventing leaks and tampering. With increasing emphasis on environmental impact, packaging innovations focus on using recyclable or biodegradable materials to reduce waste.

- Milk stands as the world's most consumed dairy product. Due to its high moisture and mineral content, vendors face challenges in long-term storage. This difficulty is a primary reason why milk is often traded in forms like milk powder or processed variants. Over 70% of fresh milk is currently packaged in HDPE bottles, diminishing the demand for traditional glass bottle packaging. Factors such as the rise of on-the-go consumption, the convenience of easy pouring, appealing packaging aesthetics, and heightened health awareness evident in the popularity of drinkable dairy alternatives such as soy-based products and sour milk have collectively fueled the demand for innovative milk packaging solutions.

- According to FAO, global milk production is projected to grow by 177 million metric tons by 2025. Also, as reported by NDDB, the western region of India topped the charts in milk procurement for the financial year 2023, averaging over 31 million kg daily. Meanwhile, the southern region secured the second spot, with an average daily procurement exceeding 15 million kg. As lifestyles evolve and urbanization accelerates, consumers are increasingly favoring dairy products over cereals as their primary protein source. This shift is projected to bolster the demand for dairy products, particularly milk, in the coming years. Consequently, these trends are poised to shape the dynamics of the milk packaging market.

- Furthermore, bio-based packages are more sustainable than standard milk cartons, reducing the manufacturer's reliance on fossil-based polyethylene plastic in the lining. With increasing emphasis on environmental impact, packaging innovations focus on using recyclable or biodegradable materials to reduce waste. For instance, in July 2023, Arla Foods partnered with Blue Ocean Closures to develop a fiber-based cap for its milk cartons to cut its plastic consumption by over 500 tonnes yearly. Further, in November 2023, addressing concerns surrounding plastic waste, Freshways launched its LoveMilk brand in 1 liter, 500 ml, and 1-pint Pure-Pak cartons with a new tethered cap. This initiative is being rolled out in the foodservice and wholesale industries.

- However, concerns over the harmful impacts of plastics and non-biodegradable packaging materials have arisen among consumers and manufacturers. In response, companies are shifting toward environmentally friendly biodegradable packaging. Manufacturers are adopting green packaging methods, focusing on lighter materials and encouraging recycling. Furthermore, environmental regulations are anticipated to affect milk production. This is because greenhouse gas emissions from milk packaging account for a notable portion of total emissions in certain countries, making them susceptible to changes in related regulations.

- The ongoing conflict between Russia and Ukraine significantly impacts the growth of the milk packaging market. Damaged infrastructure and transportation hurdles due to the war disrupt the supply chains for both raw and packaging materials. This disruption raises the specter of shortages and inflated costs. Furthermore, the conflict-induced surge in energy prices and inflation could escalate production and packaging expenses, subsequently affecting the pricing and accessibility of milk products.

Milk Packaging Market Trends

Paperboard Milk Packaging to Witness Significant Demand

- As global awareness of eco-friendly packaging materials rises, the milk packaging industry is witnessing a notable shift. Due to its recyclable properties, the paperboard segment is set to emerge as the fastest-growing material in milk packaging. This surge in the paperboard segment can be attributed to its eco-friendly features, which resonate with growing environmental consciousness. Additionally, the clear and prominent information on paperboard packaging is poised to drive its market growth further.

- Various governments and organizations are introducing stricter plastic-use regulations, encouraging companies to switch to alternatives like paper. For instance, in the United States, federal guidelines mandate paper products with minimum recycled content, driving demand and investment in recycling infrastructure. Also, the European Union's Ecolabel scheme ensures paper products meet stringent environmental standards, encouraging sustainable forestry and transparent product information.

- In addition, technological advancements and refined production processes have rendered paper packaging cost-effective and efficient for manufacturers. Firms are increasingly adopting paper packaging to distinguish their products and resonate with eco-conscious consumers. For instance, Nestlé, renowned for its commitment to sustainability, now markets milk in paper-based cartons across multiple regions.

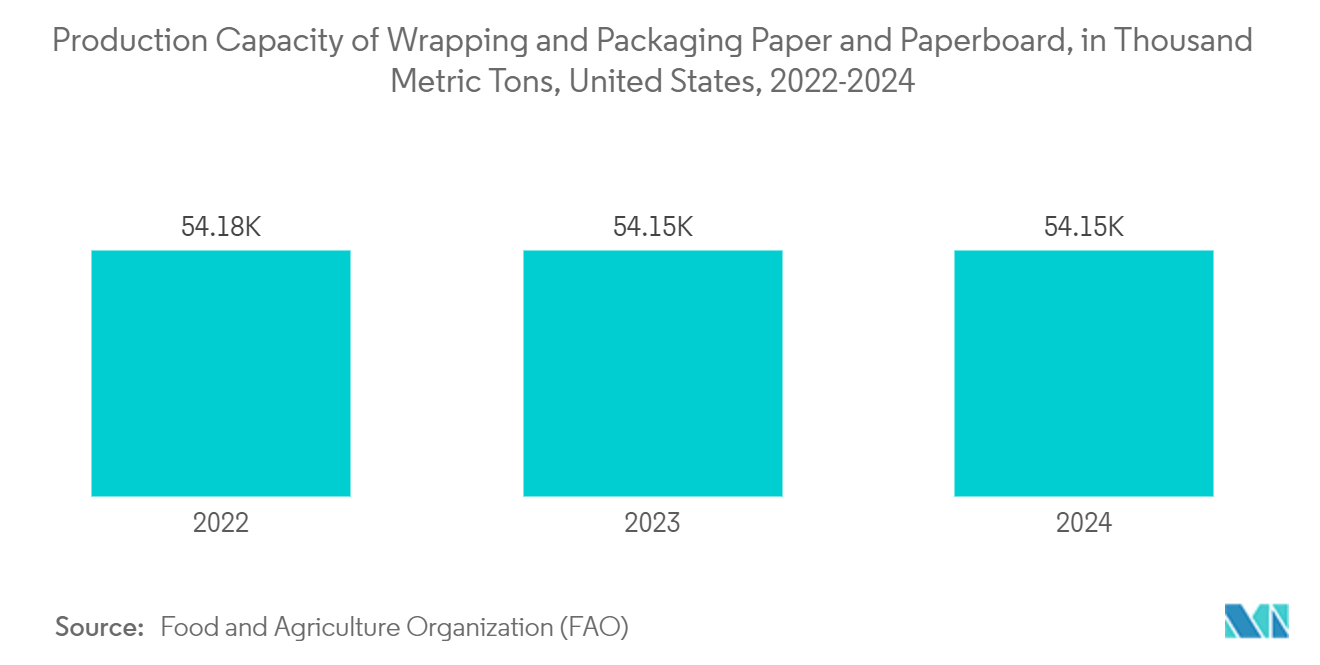

- Moreover, the worldwide paper production business is growing significantly, boosting the market studied. As reported by FAO, the United States produced 54.14 million metric tons of wrapping and packaging paper and paperboard in 2023. Furthermore, data from the National Bureau of Statistics of China indicates that in July 2024, China's processed paper and cardboard production reached around 13.17 million metric tons. Paper packaging is often considered more environmentally friendly than alternatives like plastics. The need for eco-friendly packaging options like milk paper packaging will expand as sustainability becomes a more significant issue for consumers and companies.

Asia-Pacific Expected to Witness Significant Market Growth

- Asia-Pacific has a high potential for lactose-free dairy products as healthy alternatives to lactose-containing products, which will likely complement milk production, propelling the market's growth. Additionally, heightened concerns regarding child nutrition are anticipated to boost milk consumption, further fueling the market's expansion. According to Adani Wilmar, the market size of freshly packaged dairy food is likely to increase to INR 1.6 trillion (USD 19.6 billion) in the financial year 2025. Freshly packaged dairy includes milk, curd, paneer, and yogurt, which have a shelf life of two to three days.

- Rising awareness about the health benefits of dairy products and changing dietary habits among consumers are driving higher milk consumption in the region. Also, as per USDA, as of 2023, the total domestic consumption volume of milk was over 207 million metric tons in India. This was an increase compared to the previous year, when the consumption volume was about 202 million metric tons.

- Furthermore, as urban areas expand and lifestyles become more fast-paced, there is a growing preference for convenient and ready-to-drink milk products, boosting the demand for innovative packaging solutions. Also, higher disposable incomes in developing countries such as India and China increase the purchasing power of customers. Hence, consumer dependence on processed, pre-cooked, and packed foods will likely increase. Such changes in customer spending and preferences are expected to contribute to market growth. According to an official source, in 2023, the retail sales value of dairy products in China totaled CNY 495.06 billion (USD 69.49 billion), increasing from around CNY 473.89 billion (USD 66.52 billion) in 2022. The retail sales value of dairy products was estimated to maintain steady growth and reach approximately CNY 564.72 billion (USD 79.27 billion) by 2024.

- Countries across the region are significantly expanding their paper production, which may further drive the growth of the market studied during the forecast period. According to MOSPI, the revenue from the manufacture of paper and paper products in India is projected to amount to approximately USD 21.3 billion by 2024. Furthermore, as reported by IBEF, India boasts 861 paper mills, of which 526 are currently operational, underscoring the country's substantial capabilities in paper and paperboard production.

- There is a rising emphasis on eco-friendly and recyclable packaging, influencing both manufacturers and consumers toward sustainable packaging options. Thus, these trends are driving the expansion of the milk packaging market in Asia-Pacific, with increasing investments in advanced packaging solutions to meet growing consumer needs.

Milk Packaging Industry Segmentation

The milk packaging market is fragmented as unorganized players directly impact the existence of local and global players in the industry. Local farms use e-commerce and can attract customers by providing convenience and flexibility. Moreover, the growth in milk production is driving the players to develop better packaging solutions, making the milk packaging market highly competitive. Some of the key players in the market are Evergreen Packaging LLC, Elopak AS, Tetra Pak International SA, Stanpac Inc., and Ball Corporation. These players constantly innovate and upgrade their product offerings to cater to the increasing market demand.

- March 2024: Elopak, a Norwegian food packaging company, commenced construction on its inaugural US production facility at the Little Rock Port Authority. With an investment of USD 70 million, the plant is set to manufacture cartons for various products, including milk, juices, plant-based items, and liquid eggs. Installation of production equipment is slated for the fourth quarter of 2024, with the facility aiming for full operational status by the first quarter of 2025.

Milk Packaging Market Leaders

-

Stanpac Inc.

-

Mondi PLC

-

Tetra Pak International SA

-

Ball Corporation

-

Pactiv Evergreen Inc.

*Disclaimer: Major Players sorted in no particular order

Milk Packaging Market News

- July 2024: Berry Global joined forces with Abel & Cole, a player in sustainable food delivery, to provide bottles for the Club Zero Refillable Milk service. These innovative polypropylene (PP) bottles can be refilled up to 16 times before they need recycling. Crafted from widely recyclable PP, these bottles emit fewer greenhouse gases (GHG) during transport and processing than traditional heavier glass bottles, challenging the long-standing norm of using glass for home milk deliveries.

- May 2024: Ball Corporation, a global player in sustainable packaging, announced that it had teamed up with CavinKare, a significant player in the dairy industry. Their collaboration aims to transform dairy packaging, debuting retort two-piece aluminum cans specifically for CavinKare's milkshakes.

Milk Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Health Concerns Among Consumers

4.2.2 Increasing Consumption of Flavored Milk

4.3 Market Restraints

4.3.1 Greenhouse Gas Emissions due to Dairy Activities Leading to Legislative Issues

4.4 Industry Value Chain Analysis

4.5 Industry Attractiveness - Porter's Five Forces Analysis

4.5.1 Bargaining Power of Suppliers

4.5.2 Bargaining Power of Buyers

4.5.3 Threat of New Entrants

4.5.4 Threat of Substitute Products

4.5.5 Intensity of Competitive Rivalry

4.6 Assessment of the Impact of Microeconomic Factors on the Market

5. MARKET SEGMENTATION

5.1 By Packaging Type

5.1.1 Cans

5.1.2 Bottles/Containers

5.1.3 Cartons

5.1.4 Pouches/Bags

5.1.5 Other Packaging Types

5.2 By Material

5.2.1 Plastic

5.2.2 Paperboard

5.2.3 Other Materials

5.3 By Geography

5.3.1 North America

5.3.2 Europe

5.3.3 Asia-Pacific

5.3.4 Latin America

5.3.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Stanpac Inc.

6.1.2 Mondi PLC

6.1.3 Tetra Pak International SA

6.1.4 Ball Corporation

6.1.5 Pactiv Evergreen Inc.

6.1.6 Indevco Group

6.1.7 CKS Packaging Inc.

6.1.8 Elopak AS

6.1.9 Consolidated Container Company LLC ( Loews Corporation)

6.1.10 SIG Combibloc Group Ltd

- *List Not Exhaustive

7. INVESTMENT ANALYSIS

8. FUTURE OF THE MARKET

Milk Packaging Industry Segmentation

Milk packaging is essential to protect, carry, market, and sustain its freshness and convenience. Several reasons exist for ensuring the durable packaging of milk, such as safety, information, ease of storage and handling, and avoiding distribution damages.

The milk packaging market is segmented by packaging type (cans, bottles/containers, cartons, pouches/bags, and other packaging types), material (plastic, paperboard, and other materials), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in value (USD) for all the above segments. The impact of macroeconomic trends on the market is also covered under the scope of the study. Further, the disturbance of the factors affecting the market's evolution in the near future, such as drivers and constraints, has been covered in the study. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Packaging Type | |

| Cans | |

| Bottles/Containers | |

| Cartons | |

| Pouches/Bags | |

| Other Packaging Types |

| By Material | |

| Plastic | |

| Paperboard | |

| Other Materials |

| By Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Milk Packaging Market Research FAQs

How big is the Milk Packaging Market?

The Milk Packaging Market size is expected to reach USD 47.89 billion in 2024 and grow at a CAGR of 4.60% to reach USD 59.96 billion by 2029.

What is the current Milk Packaging Market size?

In 2024, the Milk Packaging Market size is expected to reach USD 47.89 billion.

Who are the key players in Milk Packaging Market?

Stanpac Inc., Mondi PLC, Tetra Pak International SA, Ball Corporation and Pactiv Evergreen Inc. are the major companies operating in the Milk Packaging Market.

Which is the fastest growing region in Milk Packaging Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Milk Packaging Market?

In 2024, the North America accounts for the largest market share in Milk Packaging Market.

What years does this Milk Packaging Market cover, and what was the market size in 2023?

In 2023, the Milk Packaging Market size was estimated at USD 45.69 billion. The report covers the Milk Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Milk Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Milk Packaging Industry Report

Statistics for the 2024 Milk Packaging market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Milk Packaging analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.