Radiopharmaceutical Theranostics Market Size

| Study Period | 2021 - 2029 |

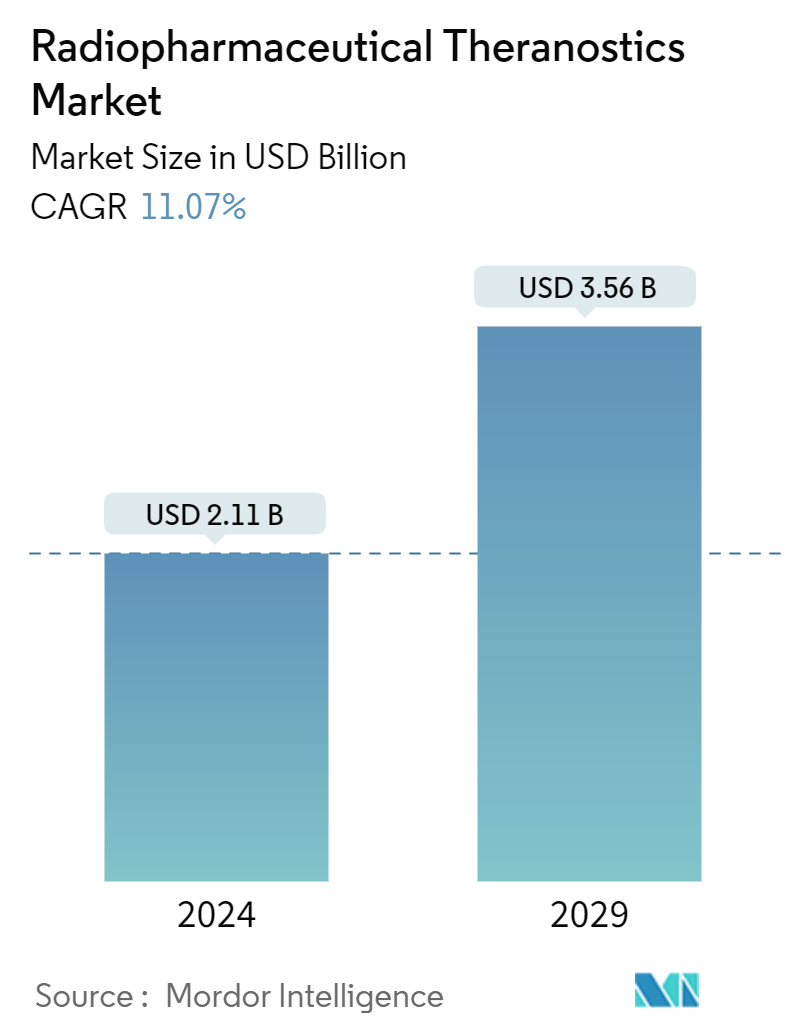

| Market Size (2024) | USD 2.11 Billion |

| Market Size (2029) | USD 3.56 Billion |

| CAGR (2024 - 2029) | 11.07 % |

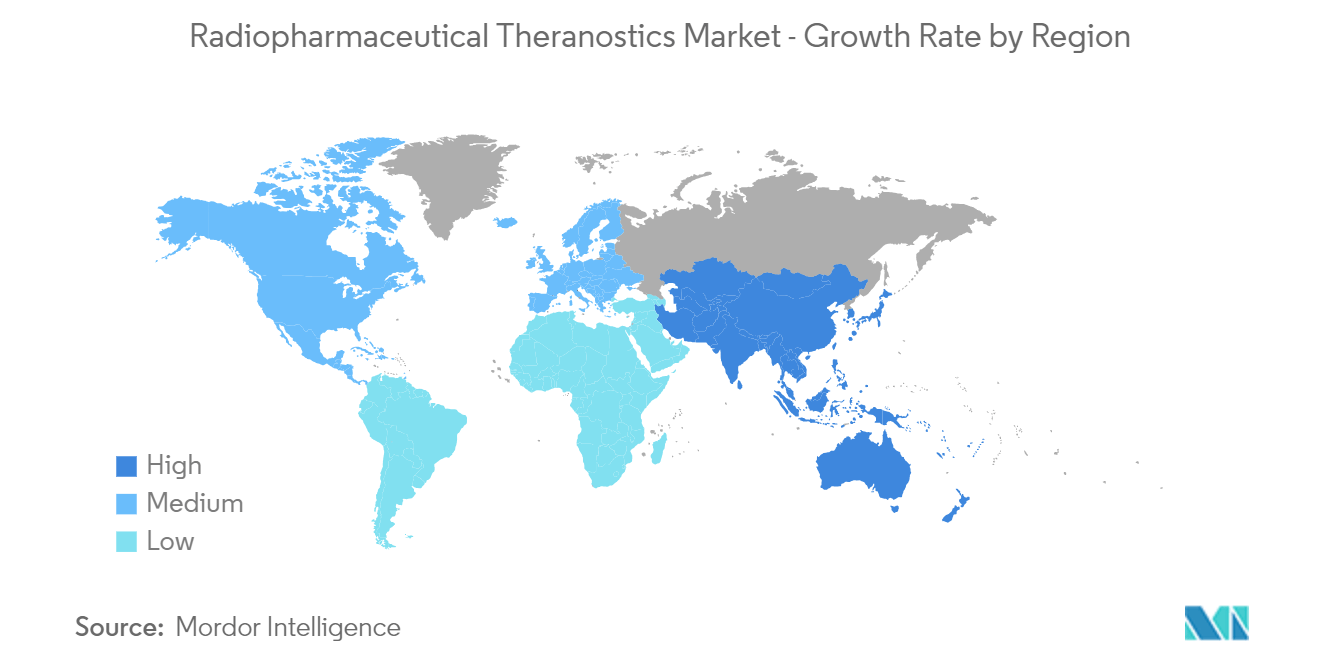

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

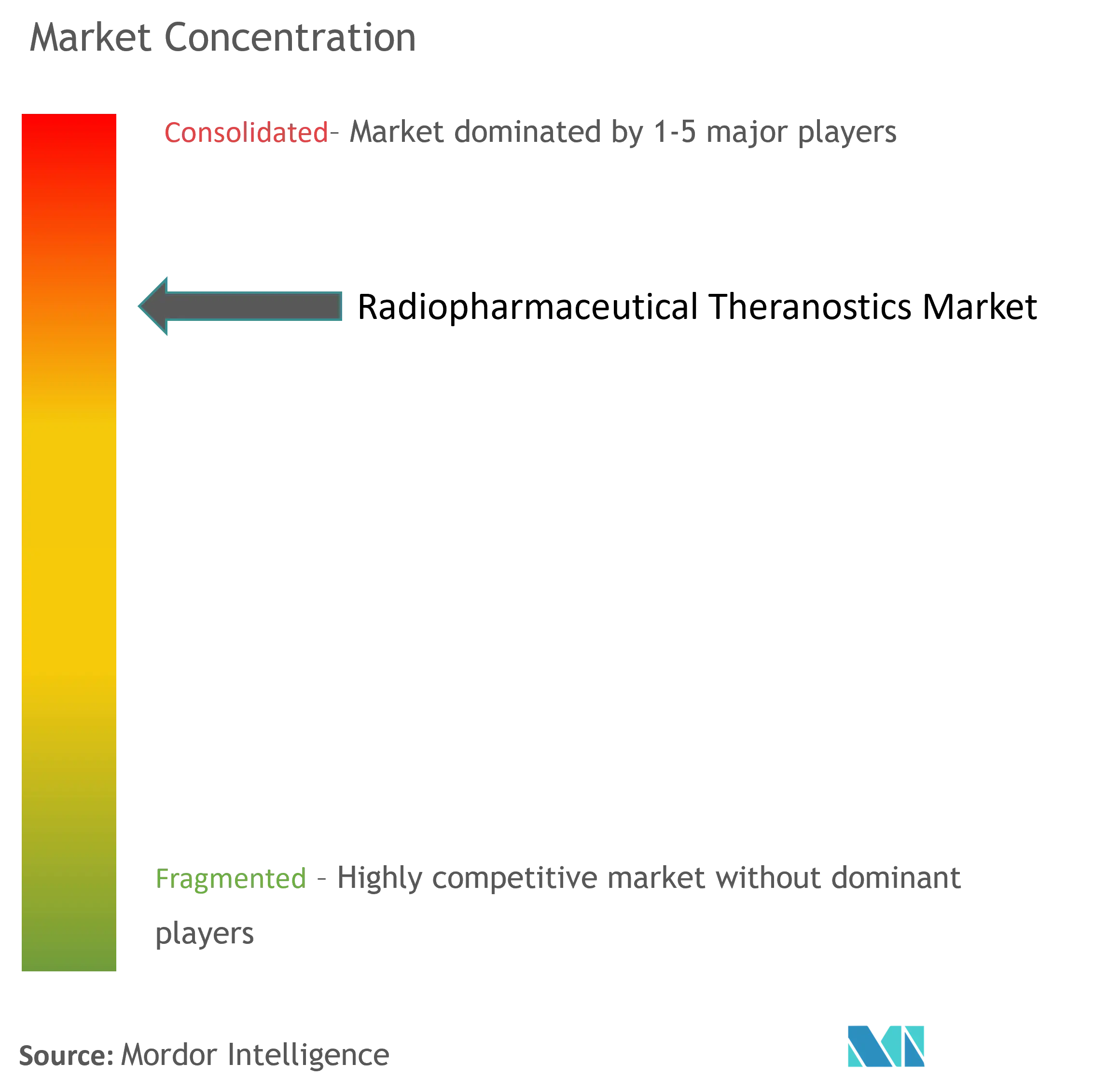

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Radiopharmaceutical Theranostics Market Analysis

The Radiopharmaceutical Theranostics Market size is estimated at USD 2.11 billion in 2024, and is expected to reach USD 3.56 billion by 2029, growing at a CAGR of 11.07% during the forecast period (2024-2029).

The development of targeted cancer therapy, growing emphasis on personalized medicine, and expansion application of radiopharmaceuticals in diagnostics are factors fueling market growth.

Radiotheranostics, which utilizes radiopharmaceuticals, is already a standard treatment for certain cancers, including prostate cancer and neuroendocrine tumors. There is a growing focus on cancer therapies using radiopharmaceuticals, which is expected to drive the market’s growth during the forecast period. For instance, a study published by the American Cancer Society in January 2023 highlighted that the breakthroughs and advancements in imaging technologies paved the way for highly targeted therapies. These therapies specifically target proteins like PSMA (prostate-specific membrane antigen) in prostate cancer and SSTR2 (somatostatin receptor 2) in neuroendocrine tumors, using radiopharmaceuticals such as Lutetium-177 PSMA-617 and Lutetium-177 DOTATATE. Therefore, as targeted cancer therapies continue to advance, the market is set for significant growth.

The advancement in drug design, such as monoclonal antibodies and small molecules conjugated with radioactive isotopes, enables precise targeting of tumor cells and minimizes damage to the healthy cells, which is expected to propel market growth.

For instance, a study published by the Journal of Cell Death Discovery in January 2024 highlighted the use of radiolabeled monoclonal antibodies (mAbs) in treating lymphoma and colorectal cancer. Radiolabeled mAbs, such as 90Y-ibritumomab tiuxetan (Zevalin) and 131I-tositumomab (Bexxar), have been approved for the treatment of B-cell Non-Hodgkin lymphoma and have shown superior outcomes compared to traditional therapies. These antibodies exhibit high specificity for target antigens overexpressed on tumor cells, enabling precise delivery of therapeutic radionuclides. This has resulted in significant improvements in response rates and progression-free survival in patients, exemplifying the potential of radiotheranostics. Thus, with the development of advanced carrier systems, the market for radiopharmaceutical theranostics is expected to grow during the forecast period.

Medical diagnostic procedures rely heavily on radioisotopes. When paired with imaging devices that capture emitted gamma rays, these tools enable the visualization of dynamic processes occurring in different body parts. For instance, as per an article published by the World Nuclear Association in April 2024, it was observed that about 10,000 hospitals globally used radioisotopes in medicine, and about 90% of the procedures were for diagnosis. Technetium-99 (Tc-99m), the predominant radioisotope, constitutes roughly 80% of all nuclear medicine procedures and 85% of global diagnostic scans in this field. Such findings underscore the pivotal role of radioisotopes in imaging, suggesting a rising demand in diagnostic imaging facilities and, consequently, an acceleration in market growth.

Companies’ rising focus on adopting key strategic activities such as collaborations, partnerships, and new product launches is expected to fuel the availability of novel products in the market. For instance, in January 2023, NorthStar Medical Radioisotopes invented a new technology for non-uranium-based medical radioisotope production, Mo-99, for use in diagnostic imaging. Thus, such activities are expected to bolster the adoption of radioisotopes in medical diagnostic procedures, boosting market growth.

Moreover, the increasing focus of the researchers on fueling the production of imaging radioisotopes is further anticipated to propel market growth. For instance, in August 2023, researchers at the University of Wisconsin focused on enhancing the production of scandium radioisotopes. These isotopes hold promise for medical imaging applications, notably in positron emission tomography (PET) scans. The initiative aims to ensure that scandium radioisotopes become a standard offering shortly.

Thus, all aforementioned factors, such as the growing focus on targeted cancer therapy, increasing demand for personalized medicine, the growing application of radioisotopes in the field of diagnostics, and strategic activities by market players, are expected to contribute to market growth over the forecast period. However, supply chain complexity, limited production capacity, and regulatory challenges are expected to hamper market growth over the forecast period.

Radiopharmaceutical Theranostics Market Trends

The Companion Diagnostic Radiopharmaceuticals Segment is Expected to Dominate the Radiopharmaceutical Theranostics Market During the Forecast Period

Companion diagnostic radiopharmaceuticals are specialized imaging agents used in conjunction with targeted therapies to assess the presence or expression of specific biomarkers or molecular targets in patients. These radiopharmaceuticals help identify patients most likely to benefit from a particular treatment, such as targeted therapy and personalized medicine, thereby optimizing therapeutic outcomes and minimizing unnecessary exposure to ineffective treatments.

The increasing emphasis on personalized medicine, innovations in imaging technologies and radiopharmaceutical development, and the growing prevalence of cancer drive the segment.

The increasing use of PET imaging in diagnostics has driven the growth of companion diagnostics radiopharmaceuticals, which are critical for early and accurate diagnosis of diseases like cancer. For instance, as per IMV PET report 2024, from 2022 to 2023, the average number of PET scans conducted per fixed PET site rose by 6.7%, climbing from an estimated 1,401 scans in 2022 to 1,495 in 2023 in the United States. Looking ahead, 67% of PET sites expect an uptick in their procedure volumes over the coming year. Thus, growing PET imaging diagnosis is expected to contribute to segment growth.

Further, innovations in imaging technologies and radiopharmaceutical development enhance the accuracy and effectiveness of companion diagnostics. For instance, as a study published in Science in August 2023, molecular imaging techniques, such as PET and MRI, are increasingly used in conjunction with companion diagnostics to monitor treatment responses dynamically. This integration allows for real-time assessment of tumor heterogeneity and therapeutic efficacy, improving patient management in oncology. Innovations focus on improving specificity and therapeutic effectiveness through novel targeting agents and better radionuclide selection, which can minimize damage to healthy tissues while maximizing treatment efficacy.

In addition, in April 2024, BAMF Health and Nihon Medi-Physics Co. Ltd announced that the first patient in the world was imaged at BAMF Health using the novel molecular imaging agent NMK89 developed by NMP as part of a clinical trial. BAMF Health was chosen, in part, because it had the most advanced total-body PET/CT scanner in the world. Thus, advanced technologies such as PET and SPECT, which are increasingly used in conjunction with companion diagnostics radiopharmaceutical, are likely to contribute to segment growth over the forecast period.

The strategic activities of industry players, such as introducing new companion radiopharmaceuticals, mergers and acquisitions, and collaborations, are expected to increase access to new products, contributing to segment growth. For instance, in June 2024, Lantheus Holdings Inc. acquired global rights to Life Molecular Imaging's RM2, which targets the gastrin-releasing peptide receptor (GRPR). This includes the associated novel, clinical-stage radiotherapeutic, and radiodiagnostic pair, known as 177Lu-DOTA-RM2 and 68Ga-DOTA-RM2 (companion diagnostics). With this acquisition, Lantheus not only bolsters its foothold in prostate cancer but also broadens its pipeline to encompass breast cancer and potentially other malignancies. The deal, valued at an upfront payment of USD 35 million, grants Lantheus global rights to the radiotheranostic pair, alongside potential regulatory milestone payments and royalties.

Similarly, in October 2023, GE Healthcare announced collaborations with SOFIE Biosciences and Nucleus RadioPharma that will play an even larger role in developing and marketing the next generation of molecular imaging pharmaceuticals. SOFIE took this approach through the clinical development of two diagnostic agents called [68Ga]FAPI-46 and [18F]FAPI-74.

Thus, such innovations and collaborations between pharmaceutical and diagnostic companies promote the development and adoption of companion diagnostics, boosting segment growth.

North America is Expected to Dominate the Radiopharmaceutical Theranostics Market

North America's leadership in the radiopharmaceutical theranostics market is propelled by a combination of advanced healthcare infrastructure, research excellence, high disease prevalence, regulatory support, strategic collaborations, and a commitment to adopting cutting-edge technologies in the healthcare sector. These factors collectively position the region as a frontrunner in shaping the future of theranostics solutions for precision medicine.

The landscape of radiopharmaceutical theranostics has notably advanced since the US Food and Drug Administration (FDA) approved radionuclides for treating neuroendocrine tumors and prostate cancer. According to a March 2024 article by Science and Medicine Group, theranostics has gained significant traction, driven by positive research outcomes and the adoption of key radionuclides like gallium-68 (Ga-68) and lutetium-177 (Lu-177). These advancements are fostering rapid progress in the field, positioning theranostics as a potential cornerstone in cancer therapy.

The favorable reimbursement policies enhance accessibility, and the adoption of Lu-177 therapies is anticipated to boost the segment's growth. For instance, as per the state of Lowa Department of Health and Human in September 2023, Lutetium Lu 177 Dotatate (Lutathera) is covered by Medicaid and North Carolina Health Choice programs. It has a maximum reimbursement rate of USD 51,300 per vial (7.4 GBq) when billed with HCPCS code A9699. Lutathera is indicated for treating somatostatin receptor-positive neuroendocrine tumors and is administered every eight weeks for up to four doses.

Similarly, Lutetium Lu 177 Vipivotide Tetraxetan (Pluvicto) agent is also covered under Medicaid, with a maximum reimbursement of USD 229.50 per mCi. It is indicated for metastatic castration-resistant prostate cancer and is administered every six weeks for up to six doses. These reimbursement structures reflect the growing demand for targeted radioligand therapies in oncology and are likely to contribute to segment growth over the forecast period.

Strategies by market players continue to bolster the momentum in the radiopharmaceutical industry. For example, in July 2024, Radiopharm Theranostics secured FDA Investigational New Drug (IND) approval for a Phase 2b imaging trial of F18-Pivalate (RAD 101) targeting brain metastases. This milestone underscores the broadening scope of radiopharmaceutical applications, extending beyond conventional cancer types, and significantly impacts the growth of the radiopharmaceutical theranostics market.

Canada's radiopharmaceutical theranostics industry is experiencing heightened activity. In a notable move, ISOLOGIC Innovative Radiopharmaceuticals unveiled a significant investment of CAD 29.9 million (USD 22 million) in June 2024. This capital injection is set to fortify the radiopharmaceutical landscape, enhance Quebec's pivotal position in Canada's medical isotope supply chain, and drive growth in the radiopharmaceutical theranostics market. The investment is expected to address critical supply chain challenges and meet the increasing demand for PET diagnostic radioisotopes throughout Canada. This initiative highlights the growing importance of radiopharmaceuticals in the country's healthcare ecosystem and reflects a broader commitment to advancing nuclear medicine.

In conclusion, North American companies and research institutions lead the way in advanced technology development. Factors such as key product launches, a dense concentration of market players, and a strong manufacturer presence in the United States are propelling the growth of the radiopharmaceutical theranostics market in the region. Given these dynamics, North America is poised for continued market expansion.

Radiopharmaceutical Theranostics Industry Overview

The radiopharmaceutical theranostics market is consolidated due to the presence of four to five major companies dominating it. Ongoing advancement efforts by major players such as Bayer AG, Cardinal Health, GE HealthCare, Jubilant Radiopharma, and Novartis AG for development, including the discovery of new tracers, ligands, and targeting agents, contribute to the market’s consolidation. These companies continually explore novel approaches, resulting in a diverse array of radiopharmaceutical products.

Radiopharmaceutical Theranostics Market Leaders

-

Bayer AG

-

Cardinal Health

-

GE HealthCare

-

Novartis AG

-

Jubilant Pharmova Limited (Jubilant Radiopharma)

*Disclaimer: Major Players sorted in no particular order

Radiopharmaceutical Theranostics Market News

- August 2024: Radiopharmaceutical biotech company ITM Isotope Technologies Munich received regulatory approval to begin production of the medical radioisotope lutetium-177 at the NOVA facility in Neufahrn, near Munich, Germany.

- June 2024: SHINE Technologies began supplying Blue Earth Therapeutics with lutetium-177 chloride (llumira), a key material for a prostate cancer drug clinical trial. This partnership highlights the critical role of effective supply chain management in ensuring the availability of essential materials for radiopharmaceutical production.

Radiopharmaceutical Theranostics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumption and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Advancements in Targeted Cancer Therapies

4.2.2 Growing Emphasis on Personalized Medicine

4.2.3 Expanding Applications in Diagnostic Imaging

4.3 Market Restraints

4.3.1 Supply Chain Complexities and Limited Production Capacity

4.3.2 Regulatory Challenges and Approval Processes

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Type

5.1.1 Companion Diagnostic Radiopharmaceuticals

5.1.2 Targeted Therapeutic Radiopharmaceuticals

5.2 By Radioisotopes

5.2.1 Technetium-99

5.2.2 Gallium-68

5.2.3 Iodine-131

5.2.4 Lutetium (Lu)- 177

5.2.5 Copper (Cu)- 67 & 64

5.2.6 Other Radioisotopes

5.3 By Source

5.3.1 Nuclear Reactors

5.3.2 Cyclotrons

5.4 By Application

5.4.1 Oncology

5.4.2 Cardiology

5.4.3 Neurology

5.4.4 Other Applications

5.5 By End User

5.5.1 Hospitals

5.5.2 Diagnostic Imaging Centers

5.5.3 Research Institutes

5.5.4 Other End Users

5.6 By Geography

5.6.1 North America

5.6.1.1 United States

5.6.1.2 Canada

5.6.1.3 Mexico

5.6.2 Europe

5.6.2.1 Germany

5.6.2.2 United Kingdom

5.6.2.3 France

5.6.2.4 Italy

5.6.2.5 Spain

5.6.2.6 Rest of Europe

5.6.3 Asia-Pacific

5.6.3.1 China

5.6.3.2 Japan

5.6.3.3 India

5.6.3.4 Australia

5.6.3.5 South Korea

5.6.3.6 Rest of Asia-Pacific

5.6.4 Middle East and Africa

5.6.4.1 GCC

5.6.4.2 South Africa

5.6.4.3 Rest of Middle East and Africa

5.6.5 South America

5.6.5.1 Brazil

5.6.5.2 Argentina

5.6.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Bayer AG

6.1.2 Cardinal Health

6.1.3 GE HealthCare

6.1.4 Jubilant Pharmova Limited (Jubilant Radiopharma)

6.1.5 Novartis AG

6.1.6 Curium

6.1.7 Telix Pharmaceuticals Limited

6.1.8 Lantheus

6.1.9 ARICEUM THERAPEUTICS

6.1.10 NuView Life Sciences

6.1.11 Clarity Pharmaceuticals

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Radiopharmaceutical Theranostics Industry Segmentation

Radiopharmaceutical theranostics involves the development and utilization of radiopharmaceuticals for both diagnostic imaging and targeted therapeutics interventions. This innovative approach integrates both components, enabling personalized treatment strategies, particularly in oncology. Radiopharmaceutical theranostics aims to enhance precision in medicine by combining diagnostic insights with therapeutic applications tailored to individual patient needs.

The radiopharmaceutical theranostics market is segmented by type, radioisotopes, application, end user, and geography. By type, the market is segmented into companion diagnostic radiopharmaceuticals and targeted therapeutic radiopharmaceuticals. By radioisotopes, the market is segmented into technetium-99, gallium-68, iodine-131, lutetium-177, copper-67 and 64, and other radioisotopes. By source, the market is segmented into nuclear reactors and cyclotrons. By application, the market is segmented into oncology, cardiology, neurology, and other applications. By end user, the market is segmented into hospitals, diagnostic imaging centers, research institutes, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| By Type | |

| Companion Diagnostic Radiopharmaceuticals | |

| Targeted Therapeutic Radiopharmaceuticals |

| By Radioisotopes | |

| Technetium-99 | |

| Gallium-68 | |

| Iodine-131 | |

| Lutetium (Lu)- 177 | |

| Copper (Cu)- 67 & 64 | |

| Other Radioisotopes |

| By Source | |

| Nuclear Reactors | |

| Cyclotrons |

| By Application | |

| Oncology | |

| Cardiology | |

| Neurology | |

| Other Applications |

| By End User | |

| Hospitals | |

| Diagnostic Imaging Centers | |

| Research Institutes | |

| Other End Users |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Radiopharmaceutical Theranostics Market Research FAQs

How big is the Radiopharmaceutical Theranostics Market?

The Radiopharmaceutical Theranostics Market size is expected to reach USD 2.11 billion in 2024 and grow at a CAGR of 11.07% to reach USD 3.56 billion by 2029.

What is the current Radiopharmaceutical Theranostics Market size?

In 2024, the Radiopharmaceutical Theranostics Market size is expected to reach USD 2.11 billion.

Who are the key players in Radiopharmaceutical Theranostics Market?

Bayer AG, Cardinal Health, GE HealthCare, Novartis AG and Jubilant Pharmova Limited (Jubilant Radiopharma) are the major companies operating in the Radiopharmaceutical Theranostics Market.

Which is the fastest growing region in Radiopharmaceutical Theranostics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Radiopharmaceutical Theranostics Market?

In 2024, the North America accounts for the largest market share in Radiopharmaceutical Theranostics Market.

What years does this Radiopharmaceutical Theranostics Market cover, and what was the market size in 2023?

In 2023, the Radiopharmaceutical Theranostics Market size was estimated at USD 1.88 billion. The report covers the Radiopharmaceutical Theranostics Market historical market size for years: 2021, 2022 and 2023. The report also forecasts the Radiopharmaceutical Theranostics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Radiopharmaceutical Theranostics Industry Report

Statistics for the 2024 Radiopharmaceutical Theranostics market share, size and revenue growth rate, created by ����vlog��ý™ Industry Reports. Radiopharmaceutical Theranostics analysis includes a market forecast outlook for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.