Market Size of Radiopharmaceutical Theranostics Industry

| Study Period | 2021 - 2029 |

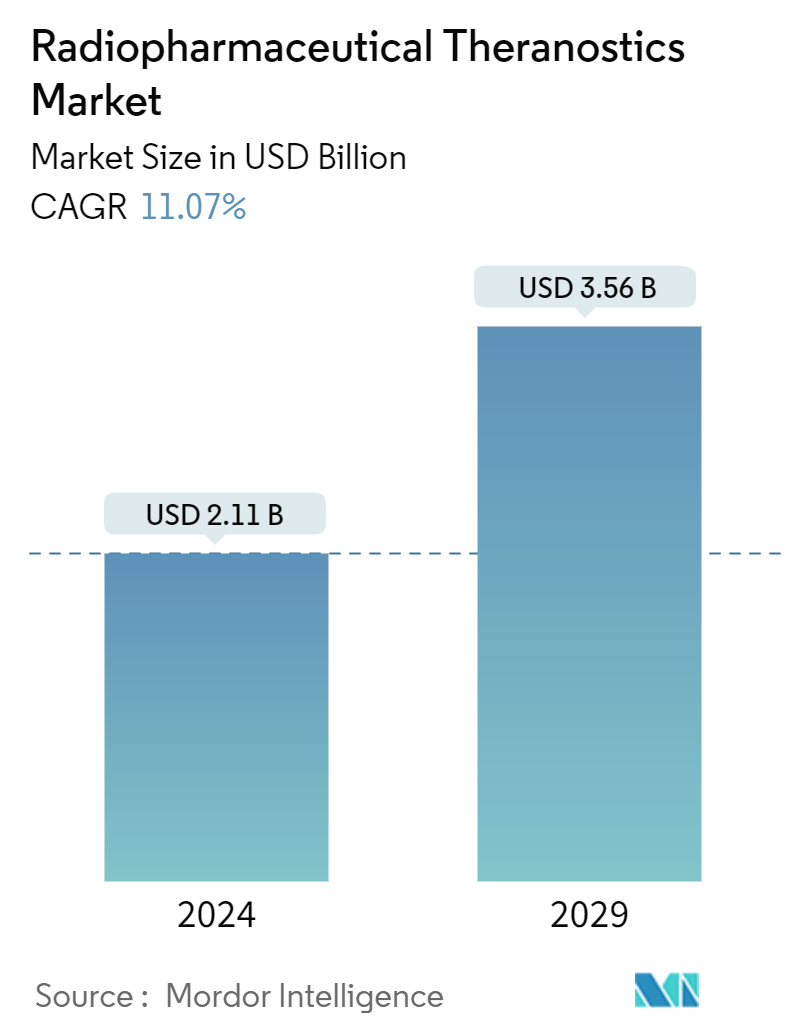

| Market Size (2024) | USD 2.11 Billion |

| Market Size (2029) | USD 3.56 Billion |

| CAGR (2024 - 2029) | 11.07 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Radiopharmaceutical Theranostics Market Analysis

The Radiopharmaceutical Theranostics Market size is estimated at USD 2.11 billion in 2024, and is expected to reach USD 3.56 billion by 2029, growing at a CAGR of 11.07% during the forecast period (2024-2029).

The development of targeted cancer therapy, growing emphasis on personalized medicine, and expansion application of radiopharmaceuticals in diagnostics are factors fueling market growth.

Radiotheranostics, which utilizes radiopharmaceuticals, is already a standard treatment for certain cancers, including prostate cancer and neuroendocrine tumors. There is a growing focus on cancer therapies using radiopharmaceuticals, which is expected to drive the market’s growth during the forecast period. For instance, a study published by the American Cancer Society in January 2023 highlighted that the breakthroughs and advancements in imaging technologies paved the way for highly targeted therapies. These therapies specifically target proteins like PSMA (prostate-specific membrane antigen) in prostate cancer and SSTR2 (somatostatin receptor 2) in neuroendocrine tumors, using radiopharmaceuticals such as Lutetium-177 PSMA-617 and Lutetium-177 DOTATATE. Therefore, as targeted cancer therapies continue to advance, the market is set for significant growth.

The advancement in drug design, such as monoclonal antibodies and small molecules conjugated with radioactive isotopes, enables precise targeting of tumor cells and minimizes damage to the healthy cells, which is expected to propel market growth.

For instance, a study published by the Journal of Cell Death Discovery in January 2024 highlighted the use of radiolabeled monoclonal antibodies (mAbs) in treating lymphoma and colorectal cancer. Radiolabeled mAbs, such as 90Y-ibritumomab tiuxetan (Zevalin) and 131I-tositumomab (Bexxar), have been approved for the treatment of B-cell Non-Hodgkin lymphoma and have shown superior outcomes compared to traditional therapies. These antibodies exhibit high specificity for target antigens overexpressed on tumor cells, enabling precise delivery of therapeutic radionuclides. This has resulted in significant improvements in response rates and progression-free survival in patients, exemplifying the potential of radiotheranostics. Thus, with the development of advanced carrier systems, the market for radiopharmaceutical theranostics is expected to grow during the forecast period.

Medical diagnostic procedures rely heavily on radioisotopes. When paired with imaging devices that capture emitted gamma rays, these tools enable the visualization of dynamic processes occurring in different body parts. For instance, as per an article published by the World Nuclear Association in April 2024, it was observed that about 10,000 hospitals globally used radioisotopes in medicine, and about 90% of the procedures were for diagnosis. Technetium-99 (Tc-99m), the predominant radioisotope, constitutes roughly 80% of all nuclear medicine procedures and 85% of global diagnostic scans in this field. Such findings underscore the pivotal role of radioisotopes in imaging, suggesting a rising demand in diagnostic imaging facilities and, consequently, an acceleration in market growth.

Companies’ rising focus on adopting key strategic activities such as collaborations, partnerships, and new product launches is expected to fuel the availability of novel products in the market. For instance, in January 2023, NorthStar Medical Radioisotopes invented a new technology for non-uranium-based medical radioisotope production, Mo-99, for use in diagnostic imaging. Thus, such activities are expected to bolster the adoption of radioisotopes in medical diagnostic procedures, boosting market growth.

Moreover, the increasing focus of the researchers on fueling the production of imaging radioisotopes is further anticipated to propel market growth. For instance, in August 2023, researchers at the University of Wisconsin focused on enhancing the production of scandium radioisotopes. These isotopes hold promise for medical imaging applications, notably in positron emission tomography (PET) scans. The initiative aims to ensure that scandium radioisotopes become a standard offering shortly.

Thus, all aforementioned factors, such as the growing focus on targeted cancer therapy, increasing demand for personalized medicine, the growing application of radioisotopes in the field of diagnostics, and strategic activities by market players, are expected to contribute to market growth over the forecast period. However, supply chain complexity, limited production capacity, and regulatory challenges are expected to hamper market growth over the forecast period.

Radiopharmaceutical Theranostics Industry Segmentation

Radiopharmaceutical theranostics involves the development and utilization of radiopharmaceuticals for both diagnostic imaging and targeted therapeutics interventions. This innovative approach integrates both components, enabling personalized treatment strategies, particularly in oncology. Radiopharmaceutical theranostics aims to enhance precision in medicine by combining diagnostic insights with therapeutic applications tailored to individual patient needs.

The radiopharmaceutical theranostics market is segmented by type, radioisotopes, application, end user, and geography. By type, the market is segmented into companion diagnostic radiopharmaceuticals and targeted therapeutic radiopharmaceuticals. By radioisotopes, the market is segmented into technetium-99, gallium-68, iodine-131, lutetium-177, copper-67 and 64, and other radioisotopes. By source, the market is segmented into nuclear reactors and cyclotrons. By application, the market is segmented into oncology, cardiology, neurology, and other applications. By end user, the market is segmented into hospitals, diagnostic imaging centers, research institutes, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| By Type | |

| Companion Diagnostic Radiopharmaceuticals | |

| Targeted Therapeutic Radiopharmaceuticals |

| By Radioisotopes | |

| Technetium-99 | |

| Gallium-68 | |

| Iodine-131 | |

| Lutetium (Lu)- 177 | |

| Copper (Cu)- 67 & 64 | |

| Other Radioisotopes |

| By Source | |

| Nuclear Reactors | |

| Cyclotrons |

| By Application | |

| Oncology | |

| Cardiology | |

| Neurology | |

| Other Applications |

| By End User | |

| Hospitals | |

| Diagnostic Imaging Centers | |

| Research Institutes | |

| Other End Users |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Radiopharmaceutical Theranostics Market Size Summary

The radiopharmaceutical theranostics market is poised for significant growth, driven by advancements in targeted cancer therapies and the increasing demand for personalized medicine. The market's expansion is fueled by the integration of radiopharmaceuticals in oncology, where they enhance precision in diagnosis and treatment through applications like imaging and targeted radiation therapy. The COVID-19 pandemic initially disrupted the market by affecting clinical trials and supply chains, but it also underscored the importance of early disease detection and preventive healthcare. Innovations in imaging modalities and the development of radiopharmaceuticals have improved diagnostic accuracy, contributing to more effective and targeted treatments. The market is characterized by ongoing research and development, with numerous radiopharmaceuticals in clinical practice and many more under development, reflecting the dynamic nature of the industry.

North America leads the radiopharmaceutical theranostics market, supported by advanced healthcare infrastructure, strategic collaborations, and regulatory support. The region's companies engage in partnerships to enhance the development and commercialization of theranostics products, with significant contributions from major players like Bayer AG, Cardinal Health, and GE HealthCare. These companies are actively involved in discovering new tracers and targeting agents, contributing to market consolidation. The regulatory landscape, particularly in the United States, plays a crucial role in approving and regulating radiopharmaceuticals, facilitating their integration into clinical practice. The market's growth is further bolstered by strategic acquisitions and collaborations, as seen with companies like Radiopharm Theranostics and their partnerships aimed at developing novel radiopharmaceuticals for complex cancers.

Radiopharmaceutical Theranostics Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Advancements in Targeted Cancer Therapies

-

1.2.2 Growing Emphasis on Personalized Medicine

-

1.2.3 Expanding Applications in Diagnostic Imaging

-

-

1.3 Market Restraints

-

1.3.1 Supply Chain Complexities and Limited Production Capacity

-

1.3.2 Regulatory Challenges and Approval Processes

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD)

-

2.1 By Type

-

2.1.1 Companion Diagnostic Radiopharmaceuticals

-

2.1.2 Targeted Therapeutic Radiopharmaceuticals

-

-

2.2 By Radioisotopes

-

2.2.1 Technetium-99

-

2.2.2 Gallium-68

-

2.2.3 Iodine-131

-

2.2.4 Lutetium (Lu)- 177

-

2.2.5 Copper (Cu)- 67 & 64

-

2.2.6 Other Radioisotopes

-

-

2.3 By Source

-

2.3.1 Nuclear Reactors

-

2.3.2 Cyclotrons

-

-

2.4 By Application

-

2.4.1 Oncology

-

2.4.2 Cardiology

-

2.4.3 Neurology

-

2.4.4 Other Applications

-

-

2.5 By End User

-

2.5.1 Hospitals

-

2.5.2 Diagnostic Imaging Centers

-

2.5.3 Research Institutes

-

2.5.4 Other End Users

-

-

2.6 By Geography

-

2.6.1 North America

-

2.6.1.1 United States

-

2.6.1.2 Canada

-

2.6.1.3 Mexico

-

-

2.6.2 Europe

-

2.6.2.1 Germany

-

2.6.2.2 United Kingdom

-

2.6.2.3 France

-

2.6.2.4 Italy

-

2.6.2.5 Spain

-

2.6.2.6 Rest of Europe

-

-

2.6.3 Asia-Pacific

-

2.6.3.1 China

-

2.6.3.2 Japan

-

2.6.3.3 India

-

2.6.3.4 Australia

-

2.6.3.5 South Korea

-

2.6.3.6 Rest of Asia-Pacific

-

-

2.6.4 Middle East and Africa

-

2.6.4.1 GCC

-

2.6.4.2 South Africa

-

2.6.4.3 Rest of Middle East and Africa

-

-

2.6.5 South America

-

2.6.5.1 Brazil

-

2.6.5.2 Argentina

-

2.6.5.3 Rest of South America

-

-

-

Radiopharmaceutical Theranostics Market Size FAQs

How big is the Radiopharmaceutical Theranostics Market?

The Radiopharmaceutical Theranostics Market size is expected to reach USD 2.11 billion in 2024 and grow at a CAGR of 11.07% to reach USD 3.56 billion by 2029.

What is the current Radiopharmaceutical Theranostics Market size?

In 2024, the Radiopharmaceutical Theranostics Market size is expected to reach USD 2.11 billion.